If you've ever spent hours untangling receipts only to discover that expenses were posted to the wrong account, you're not alone. In the UAE, inefficient expense tracking is a common problem. A 2024 report found that 21% of employees and entrepreneurs skip submitting expenses because the process is too complex, costing businesses an average of AED 13,206 per employee each year for at least a third of their workforce.

A well-structured chart of accounts brings order to financial records. It ensures every dirham is correctly categorised, makes VAT filing more straightforward, and improves the accuracy of financial reporting.

In this guide, you will learn why a chart of accounts is important for UAE SMEs, see a sample chart of accounts, and pick up practical tips for keeping it compliant, simple, and scalable.

Key Takeaways

- A chart of accounts is the backbone of financial clarity — it ensures every transaction is correctly categorised, simplifying VAT compliance, audits, and management reporting.

- Simplicity is powerful — a clear, well-structured COA with consistent naming and numbering avoids confusion, reduces errors, and keeps books easy to manage.

- Compliance starts with structure — separating VAT accounts and tailoring your COA to UAE regulations supports accurate filings and protects against costly mistakes.

- Scalability matters — reviewing and updating your COA regularly ensures it grows with your business, giving you insights to cut waste and boost profitability.

- Automation is the game-changer — tools like Alaan integrate payments, VAT compliance, and accounting software with your COA, keeping records always accurate, audit-ready, and decision-focused.

What is a Chart of Accounts?

A chart of accounts is the complete list of all the categories your business uses to record financial transactions. Each category, called an account, has a unique code or number. This structure makes it easier to record, track, and report on your company’s finances.

Think of it as the index of your accounting system, if your financial records were a book, the chart of accounts would tell you exactly where to find every type of transaction, from rent payments to sales revenue.

Also Read: Understanding the Role of Ledgers in Accounting

Why is a Chart of Accounts Important?

A chart of accounts is the structural blueprint of the financial system. When designed thoughtfully, it makes compliance easier, decisions faster, and growth smoother.

- Keeps your financial records consistent: Without a standard COA, two employees might record the same type of transaction under different names. Over time, this inconsistency distorts reports and slows reconciliations. A clear COA ensures uniformity so every payment, invoice, or refund lands in the right place every time.

- Supports VAT and corporate tax accuracy: Since VAT was introduced in 2018 and corporate tax in 2023, UAE businesses have faced stricter reporting rules. A properly segmented COA makes it simple to filter taxable and non-taxable transactions, apply the right tax codes, and generate compliant reports without combing through thousands of entries.

- Reduces audit stress: When your COA is logically structured, auditors and compliance officers can navigate your books without constant clarification requests. This speeds up the process and builds credibility with banks, investors, and regulators.

- Turns data into decisions: Beyond compliance, a well-planned COA is a management tool. It lets you break down revenue by product line, track costs by department, or compare profitability across branches, giving you insight to cut waste, allocate resources, and spot new opportunities.

In short, the chart of accounts is the backbone of financial clarity. It is as critical to a growing SME as a solid business plan, and ignoring it can quietly erode profitability.

Key Components of a Chart of Accounts

A good chart of accounts balances detail with simplicity. Too few accounts, and you lose visibility. Too many, and bookkeeping becomes messy.

A typical chart of accounts includes five main categories:

- Assets: What the business owns (e.g., cash, accounts receivable, equipment).

- Liabilities: What the business owes (e.g., loans, accounts payable).

- Equity: The owner's stake in the business.

- Revenue: Income from sales or services.

- Expenses: Costs incurred to run the business.

Pro Tip: Use a four-digit numbering system, leaving gaps between codes (e.g., 1010, 1020, 1030) so you can add new accounts later without disrupting the structure.

Sample Chart of Accounts for UAE SMEs

The table below shows a full set of account samples designed with VAT compliance and scalability in mind. You can adapt this chart of accounts example to fit your industry and size.

Assets

Liabilities

Equity

Revenue

Expenses

Best Practices for Setting Up and Maintaining Your Chart of Accounts

Keeping a chart of accounts effective comes down to clarity, compliance, and control. Here's how to get it right:

- Keep it simple, but detailed enough: Start with the five main categories (assets, liabilities, equity, revenue, expenses) and expand only when necessary. Avoid cluttering with unused accounts.

- Review and update annually: Remove inactive accounts and adjust as your business grows or reporting needs change.

- Align with your accounting software: Match your COA structure to your platform (QuickBooks, Xero, Zoho Books) to avoid mismatches and errors.

- Involve your accountant early: Set it up correctly from the start to save time and prevent compliance issues later.

- Track non-deductible expenses separately: In the UAE, fines and penalties are not VAT-deductible; keeping them apart prevents accidental claims.

Also Read: What are Accounts Payable and Accounts Receivable?

Common Mistakes Businesses Make with Their Chart of Accounts

Even well-intentioned setups can create problems if the COA isn't structured or maintained correctly. SMEs should avoid these common pitfalls:

- Overcomplicating the COA: Adding too many accounts makes reports harder to read and increases the risk of coding errors.

- Using inconsistent naming conventions: Mixing "Office Rent" with "Rent – Office" leads to confusion and inconsistent entries.

- Not separating VAT accounts: Failing to track VAT payable and VAT receivable separately complicates compliance and increases the risk of filing mistakes.

- Skipping annual reviews: Outdated or unused accounts clutter reports and make analysis less accurate.

- Lumping all revenue into one account: This hides which products or services are actually profitable.

- Recording personal expenses in business accounts: This skews financial data and can cause compliance issues during audits.

- Not training staff on COA usage: If employees aren't clear on which accounts to use, errors will multiply over time.

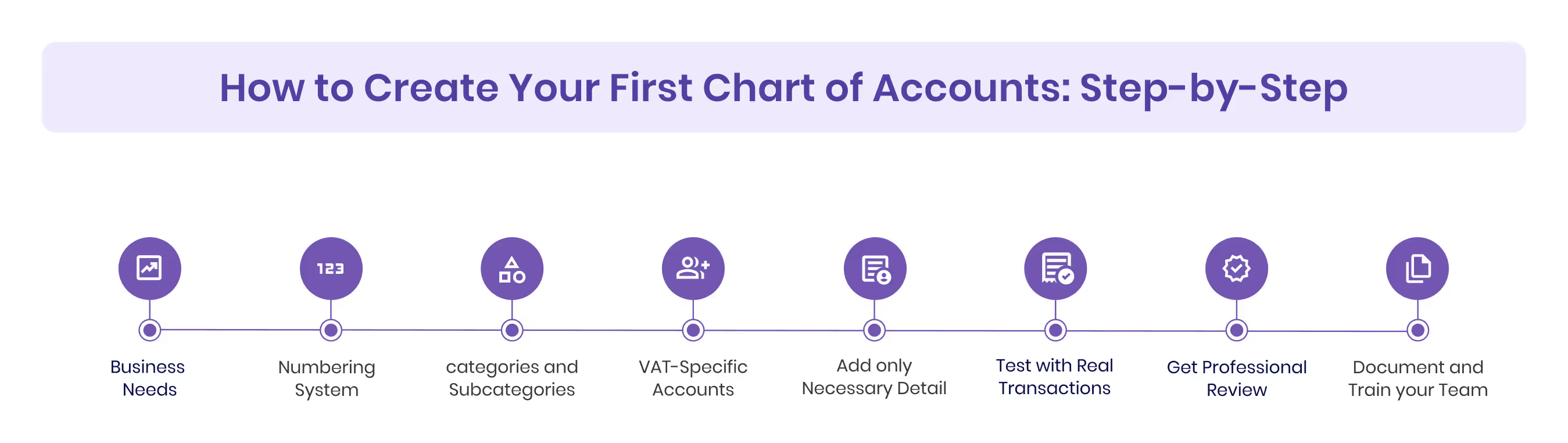

How to Create Your First Chart of Accounts: Step-by-Step

Setting up your first COA doesn't have to be overwhelming. Follow these steps to build a structure that's clear, compliant, and scalable.

- Step 1: Define your business needs: List your income sources, expense categories, assets, and liabilities. A retail store's COA will differ from a consultancy's.

- Step 2: Choose a numbering system: Use a four-digit code structure, grouping accounts by category (e.g., 1xxx for assets, 2xxx for liabilities). Leave gaps for future additions.

- Step 3: Set up main categories and subcategories: Start with assets, liabilities, equity, revenue, and expenses. Add subcategories for more detail.

- Step 4: Create VAT-specific accounts: Add separate codes for VAT payable and VAT receivable to make quarterly filing with the Federal Tax Authority simple.

- Step 5: Add only necessary detail: Your first COA doesn't need every possible code. Use a sample chart of accounts as a guide and add more later if needed.

- Step 6: Test with real transactions: Run a few entries through your accounting software to check if the structure works for your reporting needs.

- Step 7: Get professional review: Ask your accountant to review the full set of account samples before going live, ensuring compliance and avoiding restructuring later.

- Step 8: Document and train your team – Keep a COA guide handy so employees post transactions correctly from day one.

Using a chart of accounts example designed for UAE compliance will save you time and prevent costly errors.

Alaan: Helping UAE SMEs Stay Organised and Compliant

Most UAE SMEs don't struggle to create a chart of accounts. They struggle to keep it alive. New vendors, changing VAT rules, missed receipts, and the small gaps that quietly wreck financial clarity. That's where Alaan comes in. We connect every payment, category, and compliance step so your books are always ready for decisions.

Automatic Mapping for Effortless Accuracy

- At Alaan, we make your COA part of your daily operations. Every payment made with our smart corporate cards is automatically categorised and mapped to the correct COA account in real time. This means no more end-of-month spreadsheet marathons and no confusion over where a cost should be posted.

VAT Compliance Built In

- Because VAT compliance is a constant requirement in the UAE, our platform ensures VAT payable and VAT receivable accounts are updated instantly. This approach makes quarterly VAT compliance submissions to the Federal Tax Authority faster, more accurate, and far less stressful.

Integration That Keeps Books and COA in Sync

- Your COA doesn't stand alone, and neither should your expense management. Alaan integrates seamlessly with popular accounting tools like Xero, QuickBooks, NetSuite, and Microsoft Dynamics. This guarantees your books and your COA remain in sync, supporting error-free reporting and smooth audits.

Insights That Support Better Decisions

- As your business grows, our AI-powered insights highlight spending patterns, identify cost-saving opportunities, and help you adjust budgets proactively. From real-time expense tracking to automated approval workflows, Alaan equips SMEs with the tools to keep records clean, compliant, and ready for decision-making.

Trusted by 1,000+ UAE Businesses

- More than 1,000 UAE businesses, from growing startups to established enterprises, trust Alaan to maintain their financial clarity and control. When your COA and expense management work hand in hand, you're not just managing numbers, you're building a stronger foundation for sustainable growth.

Conclusion

A clear and well-maintained chart of accounts is the foundation of reliable financial reporting, smooth VAT compliance, and smarter business decisions. For SMEs, the stakes are higher than ever, with regulatory requirements, tight competition, and growth ambitions all demanding precision and control over financial data.

Creating your COA is just the beginning. The real value comes from keeping it accurate, relevant, and closely tied to your day-to-day transactions. That's where having the right tools makes all the difference.

Ready to keep your COA in perfect shape and your business audit-ready at all times?

Book a demo today to see how Alaan can simplify your expense management and strengthen your financial foundation.

FAQs

1. What’s included in a full set of accounts in the UAE?

A full set of accounts generally covers your balance sheet, income statement, cash flow statement, and the underlying general ledger accounts listed in your chart of accounts. For SMEs, having these linked correctly ensures financial transparency and readiness for audits.

2. How does a chart of accounts improve decision-making?

By categorising income, expenses, assets, and liabilities in a structured way, a COA allows you to see exactly which areas of the business are performing well and which need attention. This clarity supports more informed budgeting and investment decisions.

3. What's an example of a chart of accounts for a service-based SME?

A chart of accounts example for a marketing agency might include revenue accounts for design services, consultancy fees, and campaign management, plus expense accounts for software subscriptions, client entertainment, and subcontractor fees.

4. How can I avoid overcomplicating my chart of accounts?

Limit the number of accounts to what's necessary for reporting and compliance. Too many accounts create confusion and increase the risk of errors. Focus on relevance rather than trying to account for every possible scenario.

5. Is it necessary to tailor my COA for UAE regulations?

Yes, tailoring ensures you capture VAT requirements, corporate tax categories, and any industry-specific compliance needs. A generic COA template may not reflect local laws or business norms.

6. Can accounting software automatically update my COA?

Yes, when integrated with expense management platforms like Alaan, your COA can update automatically as transactions occur. This reduces manual entry, keeps VAT accounts accurate, and ensures reports are always current.

%201.avif)