Accrued Expenses: Definition, Types, and Differences

Accrued expenses means

.svg)

In the dynamic business environment of the UAE, financial accuracy is not just a regulatory requirement—it’s a strategic advantage. Timely and accurate financial reporting is fundamental to sound business decision-making and regulatory compliance, especially in the UAE, where adherence to IFRS is mandatory. In today’s complex operating environment, even a seemingly minor oversight, such as failing to record an expense in the period it was incurred, can result in misstated profits and compliance risks.

This challenge is more common than many realise. A recent study revealed that 96% of global finance leaders are concerned about the integrity and reliability of non-financial data in corporate reporting, underscoring the importance of strengthening internal financial controls.

Accrued expenses play a critical role in ensuring that financial statements reflect a true and fair view of a company’s obligations. Fortunately, modern finance platforms—such as Alaan—are enabling UAE businesses to automate and streamline the accrual process, enhancing both accuracy and efficiency.

This article delves into the concept of accrued expenses, their impact on financial statements, and how platforms like Alaan are helping UAE businesses streamline their financial processes, ensuring accuracy and compliance.

Definition of Accrued Expenses

Accrued expenses are a key component of the accrual accounting system, commonly used by UAE businesses to ensure financial transparency. These are expenses a company has incurred during an accounting period but has not yet paid or been invoiced for. This includes utilities consumed, services rendered, or employee wages earned before the end of the accounting period.

For example, suppose your business in Dubai pays salaries on the 5th of the following month. In that case, the portion of employee wages earned during the final week of the month must still be recorded as an expense, even if you haven’t disbursed the payment yet.

Recording these obligations under current liabilities ensures your financial statements accurately reflect what your business owes, aligning with IFRS and local auditing expectations.

Types of Accrued Expenses

In the UAE, common types of accrued expenses include:

- Salaries and Wages: Many UAE companies have payroll cycles that don’t align perfectly with the month-end, making salary accrual necessary. This ensures employee compensation is recorded in the period it's earned, not just when paid.

- Commissions: Especially in industries like real estate or sales-driven services, commissions often need to be estimated and accrued ahead of invoicing.

- Interest: For companies with loan obligations, interest accrues daily but might be payable quarterly. It's essential to record the interest expense monthly.

- Utilities: Invoices from DEWA, ADDC, or other regional providers might arrive late. Accruing estimated electricity, water, or internet charges ensures monthly reports remain consistent.

- Goods and Services Received: If goods or professional services (like consulting or marketing) are delivered but the invoice is still pending, these must be accrued.

Additional examples may include marketing retainers, IT support contracts, or maintenance services where payments are due periodically, but the invoices arrive after the fact.

Accrued Expenses on Financial Statements

Accrued expenses play a crucial role in ensuring the accuracy and transparency of a company’s financial statements. As part of the accrual accounting method, accrued expenses are recorded as liabilities even if the actual cash payment hasn’t been made yet. This process ensures that financial statements reflect a company’s financial position more accurately, aligning with the principle that expenses should be recognized when incurred, not necessarily when paid.

In this section, we will delve into how accrued expenses are presented on the key financial statements—the balance sheet and the income statement—and why their accurate reporting is essential for businesses.

1. Accrued Expenses on the Balance Sheet

Accrued expenses are reported under current liabilities on the balance sheet. Since they represent obligations that must be settled within a short period, typically within 12 months, they are considered short-term liabilities. Examples of accrued expenses might include employee wages, utility bills, and taxes owed that have been incurred but are not yet paid.

When these expenses are recognized, they increase the liabilities section of the balance sheet. Here’s how they are typically reflected:

- Accrued Expenses (Liabilities): This entry shows the total amount of unpaid expenses that are due within the next accounting period. The company needs to record these even before receiving the corresponding invoice.

For instance, if a business has incurred $5,000 in wages for its employees in December, but the payment will be made in January, the accrued wages of $5,000 would be listed under current liabilities on the balance sheet for the December reporting period.

2. Accrued Expenses on the Income Statement

On the income statement, accrued expenses impact the operating expenses of the company. Since the expense is recorded when incurred (not when paid), the company’s financial performance is reflected accurately, and the expense is deducted from the revenue for that period.

For example, if a business incurs $3,000 in utilities for the month of December, even if the payment will be made later, this $3,000 utility expense will be reflected in the income statement for December. This ensures that the company’s net income is not overstated by the delayed payment.

- Operating Expenses: Accrued expenses are included in operating expenses (like wages, utilities, or taxes), which directly affect the company’s profit or loss.

This principle of matching expenses to the period in which they occur ensures that the income statement presents an accurate picture of profitability, irrespective of when payments are actually made.

Why Accrued Expenses Matter on Financial Statements

- Accurate Financial Position: By recognizing expenses as they occur (even if not yet paid), accrued expenses ensure that the balance sheet accurately reflects the company’s obligations.

- Correct Profit Reporting: Including accrued expenses on the income statement prevents a company from overstating profits in a period when expenses related to that period have not yet been recorded.

- Compliance: Accrued expenses help businesses stay compliant with accrual accounting standards, which is especially important for audits and tax reporting.

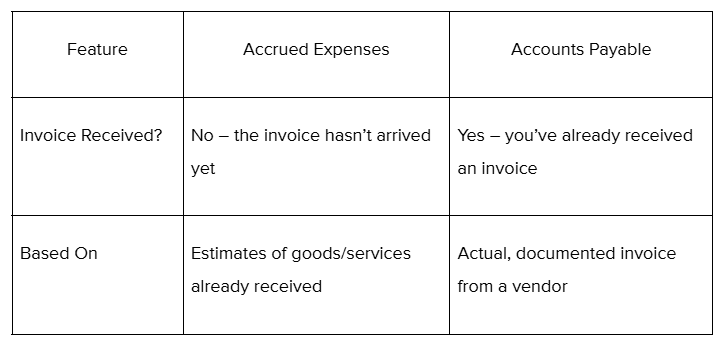

Differences Between Accrued Expenses and Accounts Payable

When managing business finances, it’s essential to understand the nuances between accrued expenses and accounts payable. While both are types of liabilities that involve money owed by the company, they are distinct in how and when they are recognized in financial statements. Knowing the difference between these two is crucial for accurate financial reporting and effective cash flow management.

Here, we’ll break down the key differences between accrued expenses and accounts payable, so you can better understand their impact on your financial statements and overall accounting practices.

Accrued expenses rely on anticipated costs based on services or goods already consumed, while accounts payable are documented liabilities with supporting invoices. Recognising this difference ensures your financials reflect economic activity in the correct period—an essential part of accrual accounting and IFRS compliance in the UAE.

How to Record and Adjust Accrued Expenses (With Journal Entry Examples)

Recording accrued expenses ensures your financial statements reflect all obligations incurred during a given period—even if the payment hasn’t been made or an invoice hasn’t been received. This is critical for accurate reporting under IFRS and UAE corporate tax laws.

Step 1: Recognise the Accrued Expense

When your business receives goods or services but hasn’t been invoiced or made the payment, you must record an expense and a matching liability:

- Debit: Expense Account (e.g., Utilities, Wages, Interest)

- Credit: Accrued Liabilities (a current liability on your balance sheet)

This entry is repeated as needed (monthly or quarterly), depending on the accrual.

Step 2: Reversal or Adjustment Upon Payment

Once the invoice arrives and you make the payment, reverse the accrual and record the actual payment:

- Debit: Accrued Liabilities

- Credit: Bank / Accounts Payable

This clears the estimate and ensures accurate matching of expenses with actual cash outflows.

Example: Monthly Accrual for DEWA Utilities

Scenario: Your business is invoiced quarterly by DEWA for electricity, averaging AED 1,500 per month. To match monthly utility usage, you accrue this amount monthly, even though payment happens at the end of the quarter.

Month-End Accrual Entry (for January):

- Debit: Utilities Expense (AED 1,500)

- Credit: Accrued Utilities (AED 1,500)

Repeat this entry at the end of February and March.

Invoice Received (end of March): AED 4,500

Reversal Entry:

- Debit: Accrued Utilities (AED 4,500)

- Credit: Utilities Expense (AED 4,500)

Payment Entry:

- Debit: Utilities Expense (AED 4,500)

- Credit: Bank (AED 4,500)

💡 Why do this? This process ensures your January–March financials reflect utility consumption even before DEWA sends the bill. Once invoiced, the reversal clears your accruals and records the real amount paid.

Best Practices for Managing Accrued Expenses in the UAE

Effectively managing accrued expenses helps ensure compliance with IFRS, improves financial accuracy, and prevents unpleasant surprises during audits or tax filings. Here are some best practices that UAE businesses should adopt

1. Create Clear Accrual Policies

Define when and how expenses should be accrued. For example, expenses above a certain threshold (say AED 500) should always be accrued if not yet invoiced.

2. Use Templates and Recurring Schedules

Standardise frequent accruals—salaries, rents, and utilities. Use recurring journal templates to streamline month-end processes.

3. Monitor and Reconcile Regularly

Review accrued vs actual expenses monthly. Adjust for over- or under-estimates and reverse accruals where appropriate.

4. Involve Department Heads

Encourage reporting from operations, HR, or procurement to ensure no unbilled expenses are missed.

5. Leverage Technology

Using platforms like Alaan reduces manual errors, improves approval workflows, and enables real-time financial oversight—all critical in a UAE compliance environment.

How Alaan Helps UAE Businesses Automate Accrued Expenses

Managing accrued expenses manually—especially across teams, departments, and multiple vendors—can quickly become a drain on resources and accuracy. Alaan simplifies this process by automating expense tracking, documentation, and accounting entries, keeping your books clean, compliant, and audit-ready year-round.

Here’s how we make it effortless:

1. Real-Time Expense Tracking, Even Without Invoices

Alaan captures every transaction in real time—even if you haven’t received the invoice yet. This allows finance teams to track unbilled or recurring services (like utilities, subscriptions, or retainers) and proactively accrue them before month-end.

2. Automatic Accrual Tagging and Categorisation

Our platform automatically tags transactions based on vendor, department, or spend category. You can configure rules to flag certain expenses for accrual (e.g., unpaid invoices over AED 1,000), ensuring that no expense slips through the cracks.

3. Seamless Accounting Integration

Alaan syncs with UAE-compliant accounting systems like Xero, Zoho Books, and QuickBooks, ensuring that your accrual entries flow directly into your GL. No manual input. No reconciliation mess.

4. Audit-Ready Documentation for Every Entry

Each expense is backed by digital receipts, approval logs, timestamps, and GL mappings—all stored securely and easily searchable from your dashboard.

5. Built-In Controls and Workflows

You can set granular controls like:

- Expense approval flows by department

- Vendor-specific policies

- Recurring expense alerts

This ensures every transaction is reviewed, policy-compliant, and properly accrued or approved before month-end.

6. Real-Time Reporting and Visibility

Finance teams get a live view of outstanding obligations, pending accruals, and estimated month-end liabilities—all in one place.

Conclusion

Getting a handle on accrued expenses is more than an accounting exercise—it’s a strategic move toward financial transparency, regulatory compliance, and smarter business decisions.

In the UAE, where IFRS adherence is non-negotiable and timely reporting is a competitive necessity, poor accrual processes can create costly setbacks. In fact, as per a 2024 KPMG UAE survey, nearly 36% of SMEs cited manual accruals as a cause of reporting delays during month-end closes.

Fortunately, we now have smarter options. With platforms like Alaan, we can automate accrual tracking, gain real-time financial visibility, and eliminate the manual guesswork that often comes with traditional accounting methods. This means we can ensure that every liability is accurately accounted for, even before the invoice arrives, allowing us to stay on top of our financial commitments and make more informed decisions.

If you’re ready to streamline your financial processes and ensure greater accuracy in your reporting, explore how Alaan can help. Reach out to us today and see how automation can transform the way you manage your finances.

FAQs

Related blog posts

-min.jpg)

If your company has expenses, Alaan is the solution for you

More control | More savings | More automation