Expense reimbursement seems simple on the surface: an employee pays for something on behalf of the company, submits the receipt, and gets paid back. But under UAE VAT and corporate tax rules, the treatment is far more nuanced. A reimbursement can either be tax-neutral, VAT-recoverable, or even classified as a taxable supply, depending on how the transaction was structured and who ultimately benefited from it.

This is where many UAE companies run into trouble. Misclassifying reimbursements, charging the wrong VAT, or recovering VAT where it does not apply can create discrepancies across VAT returns, accounting books, and corporate tax filings. These inconsistencies expose the business to penalties, denied deductions, and significant audit risk.

Finance teams, HR departments, and accountants, therefore, need absolute clarity on when a reimbursement is considered taxable, when it is exempt, and what documentation is required to support the classification. The distinction between reimbursement and disbursement, a core concept in UAE VAT law, sits at the heart of this evaluation.

A structured understanding helps organisations avoid errors, maintain compliance, and prevent conflict between employees and finance teams.

Key Takeaways

- Reimbursements are taxable when the company, not the employee, receives the benefit.

- Disbursements handled in an agency capacity fall outside UAE VAT.

- VAT recovery requires proper invoices, correct documentation, and consistent classification.

- Allowances and reimbursements must be treated differently for corporate tax.

What Makes an Expense Reimbursement Taxable in the UAE

The taxability of reimbursements under UAE VAT depends on whether the company is treated as the principal or the agent in the transaction. This distinction determines whether VAT applies and how the expense is recorded.

The role of a taxable supply in UAE VAT

A reimbursement is treated as a taxable supply when the company provides something of value and receives consideration in return. In practice, this means the company must treat the reimbursement as output VAT because it is effectively “selling” or “recharging” a cost to an employee, vendor, or another entity within the group.

When a business acts as a principal

Reimbursements fall under VAT when the goods or services benefit the company directly. For example, if an employee pays for a software subscription, supplies, or a hotel stay for a business trip, the company is the true recipient of the service. When the company pays the employee back, that reimbursement becomes part of the company’s own business activity, and VAT must be considered accordingly.

When VAT must be charged on reimbursement

VAT becomes payable in cases where a company:

- pays a supplier for services it receives, then recharges the cost

- recovers costs from employees or business partners

- passes expenses to a group entity as part of shared services

- invoices back expenses incurred for its own operations

These reimbursements are not VAT-free simply because the company is “only recovering costs.” FTA expects correct VAT treatment whenever the business acts as the principal.

Also read: Understanding Expense Recognition Principles

When Reimbursements Are Not Taxable

Not all payments recovered from employees or other parties fall under VAT. The exception applies when the business is acting as an agent, not the beneficiary.

Disbursements handled in an agency capacity

A disbursement occurs when an employee (or business) pays a cost on behalf of another party, without receiving any benefit from the transaction. Here, the company simply acts as a payment conduit.

Example:

An employee pays a government fee for attestation or visa processing in their personal name and later recovers the money. Since the company is not the recipient of the service, the recovery falls outside VAT.

Conditions FTA uses to classify disbursements

A payment generally qualifies as a disbursement when:

- The cost legally belongs to the employee or the third party

- The company does not receive any benefit

- The invoice is issued in the name of the employee or third party

- The exact amount is recovered without markup

- The company is merely facilitating payment

If any of these conditions fail, the transaction risks being reclassified as a taxable reimbursement.

Examples relevant to UAE businesses

Common non-taxable disbursements include:

- visa or immigration charges paid on behalf of the employee

- ministry or government service fees

- penalties or legal charges where the employee is responsible

- certain travel bookings where the employee is the named recipient

Clarity in documentation is critical, as FTA examines beneficiary identity, invoice details, and business purpose when determining VAT applicability.

Also read: VAT Compliance Health Check

VAT Documentation Required for Reimbursements

Correct VAT treatment depends not only on classification but also on the quality of documentation supporting each transaction. The FTA places significant weight on evidence that shows who received the goods or services, whether the cost was for business purposes, and whether the invoice meets all VAT requirements.

Valid VAT invoice requirements

A reimbursement is only eligible for VAT recovery when a proper tax invoice is available. A compliant UAE VAT invoice must include:

- Supplier name, address, and TRN

- Invoice number and date

- Description of goods or services

- VAT rate and VAT amount

- Total amount inclusive of VAT

Missing TRNs, inaccurate descriptions, or handwritten bill slips are common reasons why VAT claims are rejected.

Evidence needed to justify the business purpose

VAT recovery is tied directly to business use. Organisations should maintain:

- Approval trails for the purchase

- Cost centre or project allocation

- Proof that the service benefited the company (e.g., event participation, business travel itinerary, software access logs)

These records help support the company’s position during audits or VAT assessments.

Why inconsistent documentation leads to VAT disallowance

If documentation does not clearly show that the expense belongs to the business, the FTA may deny VAT recovery, require additional support, impose penalties for incorrect filing, and even question the classification of reimbursements vs disbursements.

In high-volume environments, where hundreds of small employee expenses flow into ERP systems each month, these inconsistencies add up quickly.

Also read: Post Expenses to VAT and ERP Systems

Are Employee Expense Reimbursements Taxable for Corporate Tax Purposes?

Corporate tax treatment is separate from VAT, but both rely on accurate classification of expenses. The focus for corporate tax is whether the cost is wholly and exclusively for business purposes and whether it is a reimbursement or an allowance.

Difference between business reimbursements and personal reimbursements

Business reimbursements, such as travel, accommodation, software, supplies or client-related costs, are generally deductible under UAE corporate tax as long as the benefit relates to the company’s activities.

Personal reimbursements, however, are not deductible. These include:

- fuel for personal travel

- family travel or accommodation

- personal telecom charges

- gifts or discretionary spending unrelated to business

If a cost does not support business operations, it cannot reduce taxable income.

Treatment of employee allowances vs reimbursements

Allowances are not the same as reimbursements. An allowance (such as a fixed fuel or phone allowance):

- is treated as employee income or benefit

- is not linked to the exact spend

- may not qualify as a business deduction

Reimbursements, by contrast, are tied to actual documented costs incurred on behalf of the company.

This distinction matters because many UAE businesses mistakenly deduct allowances as if they were reimbursements, creating compliance issues during tax reviews.

[cta-6]

How mixed-purpose expenses should be handled

Many expenses include both personal and business components, for example, travel that involves weekend extensions or telecom bills where personal usage is mixed with business calls. In such cases, companies should apply a reasonable allocation method, document the basis for allocation, and remain consistent across employees and periods.

A well-structured approach reduces the risk of the FTA questioning the deductibility of such expenses.

Also read: UAE Corporate Tax Deductions Guide

Can a Company Withhold Employee Expense Reimbursement?

Companies are often unsure when they are allowed to reject or delay reimbursement requests. UAE labour regulations do not obligate businesses to reimburse expenses automatically; reimbursement depends on the internal expense policy and the nature of the cost.

Conditions under which reimbursement may be withheld

A company can reasonably withhold reimbursement when:

- The employee does not submit valid VAT invoices

- The expense violates the company’s travel or spending policy

- The cost is personal rather than business-related

- The amount exceeds permitted limits without approval

- The employee repeatedly submits non-compliant claims

Finance teams must apply these rules consistently to avoid disputes or perceived unfairness.

Why companies need structured reimbursement policies

A clear reimbursement policy protects both sides. Employees know exactly what will be reimbursed, what documentation is required, and how approvals work. Finance teams benefit from consistent records, easier VAT treatment, and fewer exceptions to investigate.

Policies that lack structure often result in:

- uneven treatment across departments

- duplicate or fraudulent submissions

- VAT errors due to missing documents

- month-end delays caused by manual checks

A well-drafted policy reduces friction and strengthens compliance across the organisation.

Also read: Effective Business Spending Policies

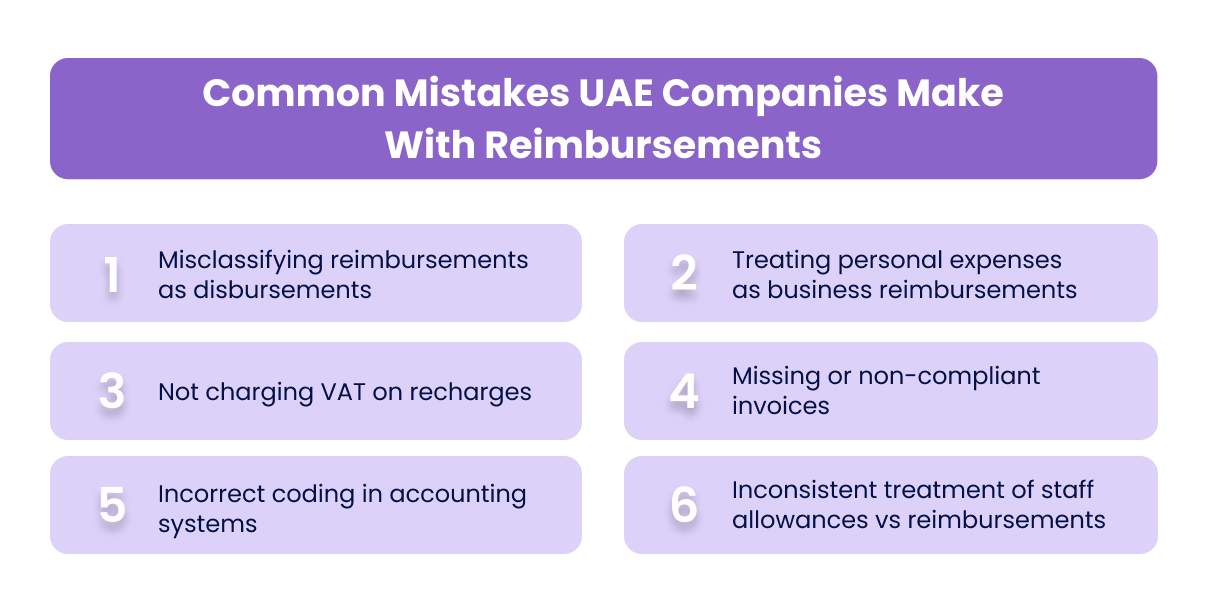

Common Mistakes UAE Companies Make With Reimbursements

Despite clear VAT guidance, many UAE organisations continue to misclassify reimbursements or apply incorrect tax treatments. These mistakes often arise from operational shortcuts, inconsistent documentation, or a misunderstanding of whether the company or the employee is the true beneficiary of the transaction.

1. Misclassifying reimbursements as disbursements

Some businesses assume that if they are simply “recovering money,” the transaction sits outside VAT. However, when the company is the actual recipient of the goods or services, the recovery becomes a taxable supply. Misclassification is one of the most common reasons for VAT reassessments.

2. Treating personal expenses as business reimbursements

Fuel for personal travel, family-related expenses, leisure activities during work trips, or personal telecom charges are frequently submitted as business costs. These expenses are not deductible for corporate tax and may also invalidate VAT claims. Repeated occurrences signal weak internal controls.

3. Not charging VAT on recharges

Businesses often charge costs to employees or group entities without applying output VAT. Under UAE VAT law, if the company is recovering costs as a principal, the recharge is a taxable supply, and VAT must be applied. Failure to charge VAT leads to underpaid output tax and potential penalties.

4. Missing or non-compliant invoices

Receipts lacking TRNs, handwritten bills, or invoices issued in the employee’s name instead of the company’s name pose compliance challenges. VAT recovery may be denied, and reimbursements may require reclassification.

5. Incorrect coding in accounting systems

Without clarity in the chart-of-accounts mapping, reimbursements may be coded incorrectly, for example, being treated as allowances, business development expenses, or employee benefits. This creates inconsistencies across VAT returns, general ledgers, and corporate tax filings.

6. Inconsistent treatment of staff allowances vs reimbursements

Allowances (fuel, phone, travel) are frequently recorded as reimbursements, even though they represent employee benefits and not business expenses. The mismatch affects both expense deductibility and payroll tax interpretation.

Also read: Track and Manage Business Expenses

How Alaan Helps Companies Manage Taxable and Non-Taxable Reimbursements

Finance teams often struggle with reimbursements because of missing invoices, misclassification, delayed submissions, and the sheer manual effort involved in validating each claim. Alaan eliminates much of this friction by giving organisations real-time visibility, automated checks, and structured workflows.

Automated receipt capture and VAT validation

Employees upload receipts through the Alaan app or Chrome extension at the moment of spend. Alaan Intelligence reads TRNs, VAT amounts, supplier details, and descriptions, flagging incomplete or non-compliant invoices. This prevents incorrect VAT claims from entering the accounting system.

Real-time categorisation for reimbursements vs allowances

Alaan distinguishes between reimbursements, allowances, and business expenses using custom rules defined by the finance team. This ensures each transaction is mapped to the correct category, helping companies comply with both VAT and corporate tax requirements.

Policy controls to prevent non-compliant claims

Finance leaders can set rules that block or flag expenses that violate company policies, such as personal purchases, missing receipts, or claims beyond specified limits. This reduces exceptions and increases adherence to internal guidelines.

ERP sync ensuring correct VAT and tax treatment

Alaan integrates seamlessly with accounting systems, ensuring transactions flow into the ERP with accurate coding, VAT treatment, and cost-centre allocation. This eliminates manual entry and ensures reimbursements are booked consistently across periods.

[cta-9]

Conclusion

The taxability of expense reimbursements in the UAE hinges on a single principle: who ultimately benefits from the expense. When the business is the beneficiary, the reimbursement often becomes a taxable supply under VAT. When the employee is the beneficiary, and the company merely facilitates payment, the transaction typically falls outside VAT.

Getting this distinction wrong affects VAT recovery, corporate tax deductibility, and audit readiness. When supported by structured reimbursement policies, clear documentation standards, and automated spend controls, finance teams can ensure that every reimbursement is treated accurately and consistently.

At Alaan, we help UAE businesses manage reimbursements with real-time receipt validation, VAT checks, policy-driven approvals, and accurate ERP syncing, reducing manual work and preventing compliance errors before they occur.

If you want to strengthen reimbursement governance and minimise audit risk, book a demo to see how Alaan simplifies the entire workflow.

Frequently Asked Questions (FAQs)

1. Are employee expense reimbursements taxable under UAE VAT?

Yes, reimbursements are taxable when the company is the actual recipient of the goods or services. VAT must be charged when the company recovers such costs.

2. When are reimbursements considered disbursements and not taxable?

When the company acts as an agent, and the employee or third party is the legal beneficiary of the service. The amount recovered must match the exact cost.

3. Can a company withhold reimbursement from an employee?

Yes, if the employee submits personal expenses, missing receipts, non-compliant invoices, or claims outside policy limits. Companies must apply rules consistently.

4. Are reimbursements deductible under UAE corporate tax?

Reimbursements for legitimate business expenses are deductible. Personal expenses and allowances treated as benefits are not.

5. Do companies need to charge output VAT when recharging expenses?

If the business is acting as a principal and passing costs onward, output VAT applies. Failing to charge VAT is a common compliance issue.

6. How does Alaan simplify reimbursement management?

Alaan automates receipt capture, validates VAT details, enforces policy rules, and syncs each transaction into the ERP with correct tax treatment.

%201.avif)