Understanding UAE business entertainment expenses and deductions is essential for to optimise tax efficiency and ensure compliance under the 2025 UAE corporate tax framework.

As per current regulations, businesses deduct up to 50% of entertainment expenses related to clients, suppliers, or business partners, while expenses for staff entertainment are fully deductible.

Proper categorisation, supported by thorough documentation such as invoices and business purpose evidence, is important to avoid tax adjustments and penalties.

This blog provides clarity on the complexities of entertainment expenses, practical guidance on record-keeping, and insights into optimising deductions within the legal framework.

Key Takeaways

- Under the 2025 UAE Corporate Tax Law, 50% of business-related entertainment expenses (such as meals, events, and accommodation for clients, suppliers, and business partners) are deductible.

- While staff entertainment expenses (e.g., company parties, staff events) are 100% deductible, misclassification may lead to tax adjustments and penalties.

- VAT on business entertainment expenses is generally non-recoverable for client-related costs but recoverable for staff-related entertainment, requiring careful VAT treatment and compliance with documentation standards.

- Strong record-keeping, including detailed invoices and proof of business purpose, is mandatory to substantiate deductions and withstand audit scrutiny under UAE regulations.

- Implementing strict internal expense approval policies and using digital expense tracking tools significantly reduces risks related to mixed-purpose entertainment events and misclassification.

What is Business Entertainment Expense?

Business entertainment expenses are costs incurred by a company to entertain clients, suppliers, business partners, or employees in a professional context to improve business relationships, promote goodwill, or reward staff.

These expenses typically include meals, events, tickets, accommodation, transportation, or facilities utilised to engage and entertain stakeholders in connection with business activities. Such expenses must have a clear business purpose and be properly documented to qualify as deductible under tax laws.

Here is a detailed list of activities that count as business entertainment:

- Meals and refreshments are provided to clients, suppliers, or business partners during meetings or events.

- Costs of organising corporate events, dinners, conferences, or seminars aimed at client or partner engagement.

- Admission fees for business-related events such as trade shows, exhibitions, or cultural performances.

- Accommodation or travel expenses directly connected to business entertainment activities.

- Entertainment facilities expenses, including venue hire or recreational activities arranged for clients or partners.

- Staff entertainment expenses, such as company parties, team-building events, or staff appreciation functions

To fully use the benefits and ensure compliance regarding business entertainment expenses, it is critical to understand their deductibility and related VAT treatment under the 2025 UAE Corporate Tax Law.

Is Business Entertainment Tax Deductible?

Business entertainment expenses have specific deductibility rules and VAT implications that must be carefully managed. Below is a focused overview of these provisions:

Business-Related Entertainment (Clients, Suppliers, Partners):

Expenses such as meals, event tickets, or accommodation for external stakeholders are deductible at 50%. This partial deduction recognises these costs as partly benefiting the business but requires careful allocation to avoid misclassification.

Staff Entertainment Expenses:

Internal events, including company parties, team-building activities, and staff appreciation functions are fully deductible at 100%, reflecting their importance for employee engagement and welfare.

Record-Keeping and Categorisation:

Maintaining detailed documentation—invoices, receipts, and clear justifications of the business purpose, is mandatory. Without this, claims risk rejection and may trigger tax penalties or adjustments.

VAT Treatment:

VAT incurred on business-related (client and partner) entertainment expenses is generally non-recoverable, meaning businesses cannot claim this VAT as input tax. Conversely, VAT on staff-related entertainment expenses is recoverable, necessitating strict adherence to VAT accounting rules to optimise tax recovery.

To understand the complexities of business entertainment expenses, it's essential to be well-versed in the regulatory framework that governs these costs in the UAE.

Regulatory Framework for Business Entertainment Expenses in the UAE

The UAE's regulatory framework underpins the treatment of business entertainment expenses, aligning with the 2025 Corporate Tax Law and existing VAT regulations. This framework sets clear limits on deductibility and VAT recoverability, ensuring that businesses meet compliance standards while optimising tax efficiency.

The framework’s core elements include:

- Corporate Tax Deductibility Rules: The UAE Corporate Tax Law specifies that only 50% of entertainment expenses related to clients, suppliers, or business partners are deductible, reflecting partial business benefit. Conversely, entertainment expenses incurred for staff are fully deductible at 100%, recognising their role in promoting employee welfare.

- VAT Treatment: VAT on business entertainment expenses generally follows the same split. VAT on client-related entertainment is non-recoverable, meaning input VAT cannot be claimed, while VAT on staff entertainment is recoverable.

- Documentation and Record-Keeping: To substantiate claims, companies must maintain detailed invoices, receipts, and evidence of the business purpose for all entertainment expenses. This documentation is vital to avoid tax adjustments or penalties during audits.

- Applicable Articles: Key legal provisions include Articles 28 and 32 of the UAE Corporate Tax Law, which outline the deductibility limits, and the UAE VAT Law, which elaborates on VAT recoverability concerning entertainment expenses.

Below is a detailed table illustrating typical business entertainment expenses in the UAE, their deductible percentages under the 2025 Corporate Tax Law, and specific examples for each category.

Understanding entertainment expense deductions under the UAE Corporate Tax Law requires strict attention to what is allowable and, equally important, clarity around non-deductible costs.

Deduction Rules: What is and Isn’t Deductible?

Understanding exactly what can, and cannot, be deducted as a business entertainment expense is vital for UAE companies aiming to reduce taxable income lawfully and avoid compliance risks. The rules are clear and precise for both claims and exclusions, helping executives deal with the corporate tax system with confidence.

The list of allowable deductions is as follows:

- Entertainment expenses for clients, suppliers, or business partners (e.g., meals, event tickets, accommodation directly linked to business) are capped at a 50% tax deduction.

- Staff entertainment expenses (e.g., company parties, staff-only events, or internal meals) are 100% tax-deductible.

- Mixed events (involving both staff and clients) require allocating the expense: 50% may be claimed for client portions, 100% for staff involvement, with segregation and documentation essential.

- Valid invoices, a clear description of business purpose, and proper attendee records must substantiate all claims.

Besides the deductions, the list of strictly non-deductible entertainment expenses

- Personal entertainment unrelated to business activity (family outings, personal celebrations).

- Expenses incurred for non-business guests, family members, or friends, even if attending with staff or clients.

- Leisure, resort, or recreational spending is not directly linked to business objectives.

- Unsubstantiated costs with missing or inadequate documentation (no valid invoice, unclear purpose, incomplete attendee list).

- Expenses expressly prohibited under UAE tax law, such as gifts, donations, or sponsorships not linked to allowable business engagement.

- Costs claimed for entertainment are already reimbursed by third parties or subject to double deduction.

Precise calculation of employee entertainment expenses requires a structured, compliance-driven process so that UAE businesses can claim permissible deductions and maintain audit-ready records.

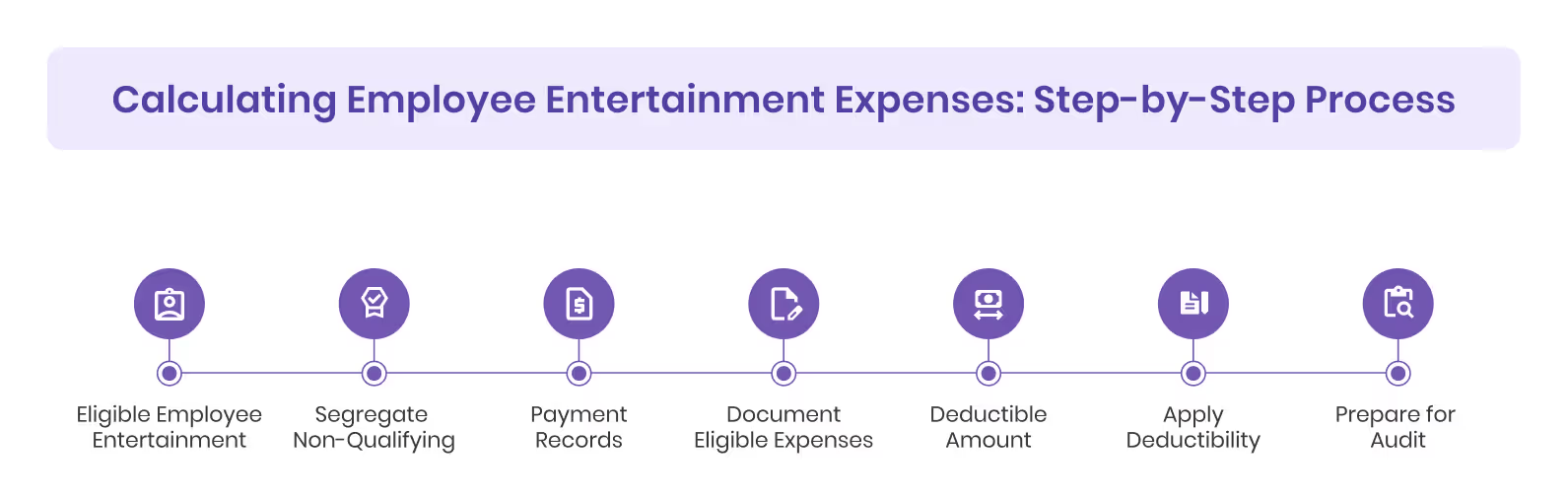

Calculating Employee Entertainment Expenses: Step-by-Step Process

Understanding how to calculate employee entertainment expenses accurately is essential for both efficient tax planning and regulatory compliance. Each step should be executed methodically to avoid errors and support full deductibility under the UAE Corporate Tax Law.

By following the steps mentioned below, UAE businesses can create a transparent record of employee entertainment expenses:

Step 1: Identify Eligible Employee Entertainment Activities

Begin by specifying which activities qualify. Only expenses for staff-focused events—such as company parties, team-building workshops, employee appreciation events, and internal meals, meet the criteria for 100% deductibility.

Step 2: Segregate Non-Qualifying and Mixed Expenses

Exclude any costs incurred for clients or external guests. For mixed events (involving staff and clients), split the expense: calculate the direct staff portion for full deduction and allocate the rest as client entertainment, which is only 50% deductible.

Step 3: Collect and Review Invoices & Payment Records

Gather original invoices and payment confirmations for every eligible expense. Verify that each document matches the claimed event, attendee list, and stated business purpose to ensure clarity and compliance.

Step 4: Document Eligible Expenses in a Detailed Log

Maintain a detailed expense log for each employee entertainment item, including:

- Date of expense

- Type of event/activity

- Purpose and relevance for business

- List of attendees (names, roles)

- Location/venue

- Total cost incurred

- Amount claimed for deduction

- Invoice and receipt references

This log serves as the backbone for compliance and is critical during any tax audit.

Step 5: Calculate Total Deductible Amount

Sum the total verified expenses for eligible staff entertainment events. For mixed-purpose events, only include the proportion applicable to employees. Ensure that no double-counting or inclusion of non-business costs occurs.

Step 6: Apply Deductibility Criteria

Confirm that all calculated employee entertainment expenses are in full alignment with the 2025 UAE Corporate Tax Law (i.e., 100% deductible for staff-only events). For any portion related to clients or suppliers, apply the relevant 50% cap separately.

Step 7: Prepare for Audit and Tax Submission

Verify the completeness and accuracy of all documentation and logs. Cross-check each expense against internal policy and statutory requirements (legal references, compliance frameworks), ensuring all potential queries from UAE tax authorities are pre-emptively addressed.

Building on the detailed process of calculating and documenting employee entertainment expenses, it is equally vital for finance leaders to adopt practical strategies to optimise these costs effectively without compromising compliance or business relationships.

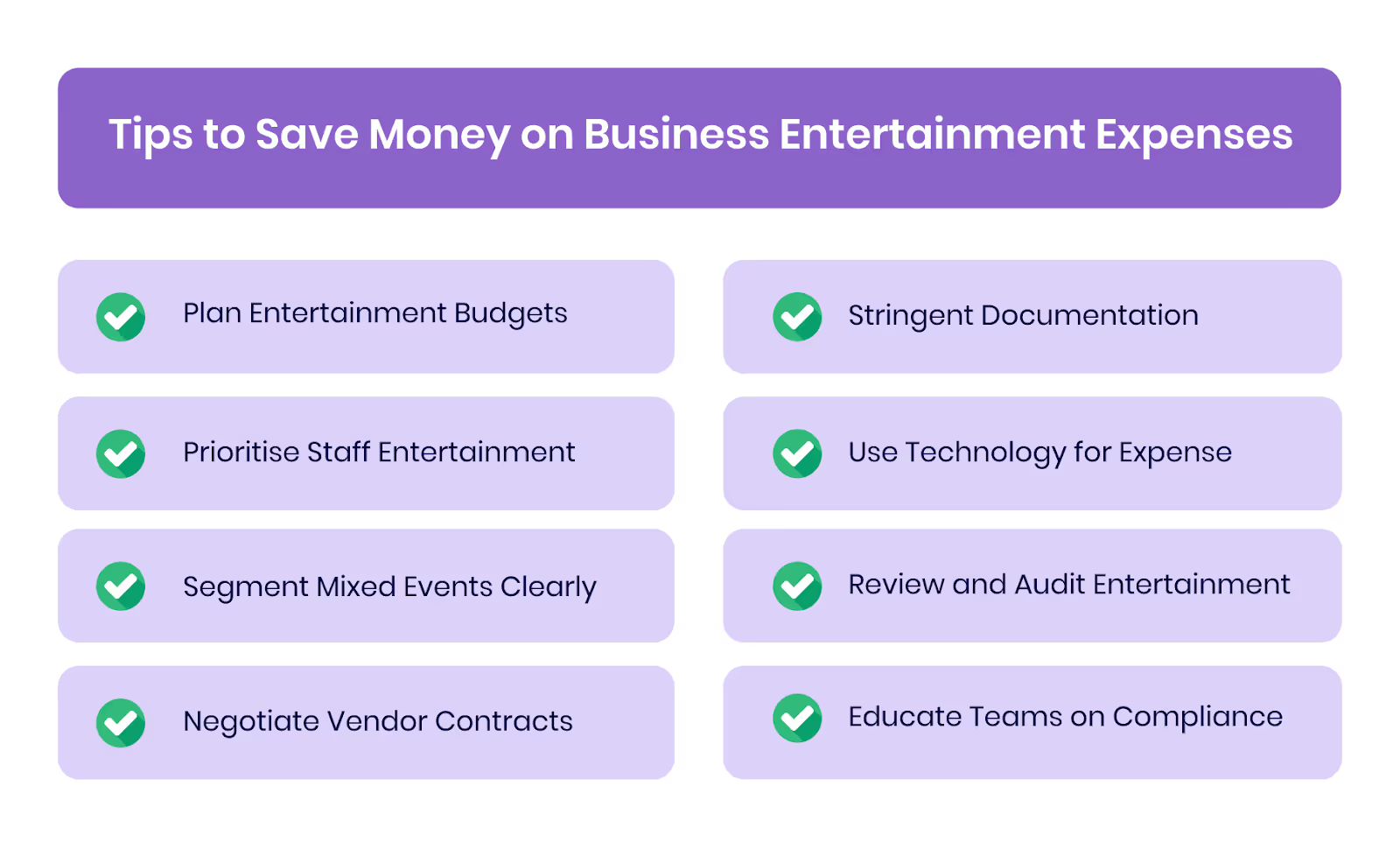

Tips to Save Money on Business Entertainment Expenses

Strategically managing business entertainment expenditure can significantly enhance a company's financial efficiency while maintaining the value of client and staff engagement. The following specific and actionable tips help Middle East businesses control costs, stay within deductibility limits, and avoid unnecessary VAT liabilities.

1. Plan Entertainment Budgets Within Deduction Limits:

Design entertainment budgets around the 50% deductibility cap for client-related expenses and the 100% allowance for staff events. Avoid exceeding these thresholds to prevent unrecoverable costs and tax adjustments.

2. Prioritise Staff Entertainment for Full Deduction Benefits:

Given that staff entertainment expenses are fully deductible and VAT recoverable, focus on meaningful internal events that boost morale yet offer full tax and VAT advantages.

3. Segment Mixed Events Clearly:

For events involving both clients and employees, carefully allocate costs by attendee category. This ensures only the permissible portions are claimed, optimising tax deductions and reducing audit risks.

4. Negotiate Vendor Contracts and Seek Volume Discounts:

Engage suppliers and event venues with a clear understanding of your budget constraints, aiming for discounts on catering, accommodation, or event space. Regional vendors familiar with MENA business practices might offer tailored, cost-effective packages.

5. Implement Stringent Documentation Practices:

Maintain proper documentation, including detailed attendee lists and clear business purposes, to avoid rejected claims. This reduces the risk of penalties and maximises allowable deductions.

6. Use Technology for Expense Tracking:

Use digital tools and software to monitor, categorise, and report entertainment expenses in real time. This increases transparency, enhances compliance, and aids strategic decision-making.

7. Review and Audit Entertainment Expenses Regularly:

Conduct periodic internal audits to identify cost-saving opportunities, detect misclassifications, and ensure adherence to corporate tax and VAT regulations.

8. Educate Teams on Compliance and Cost Efficiency:

Train staff responsible for organising or approving entertainment expenses on relevant tax laws and company policies, fostering prudent spending aligned with regulatory requirements.

Building on its expertise in managing business entertainment expenses, Alaan combines corporate card solutions with advanced spend management tools to help businesses control costs and optimise tax benefits.

How Alaan Helps Manage Business Entertainment Expenses

Alaan’s financial platform is designed to tackle the complexities of business entertainment expenses under UAE corporate tax and VAT regulations by integrating corporate card services and advanced spend management capabilities. This ensures finance leaders gain superior visibility, compliance, and operational efficiency.

1. Corporate Cards with Spending Controls:

Issue corporate cards to employees or teams with pre-set limits linked to approved entertainment categories. This ensures compliance with the 50% deduction cap for client entertainment and 100% for staff events, while preventing unauthorised spend.

2. Real-Time Expense Tracking & Categorisation:

Automatically track and categorise expenses by type—client or staff—applying correct deduction rules and VAT treatment (recoverable for staff, non-recoverable for clients).

3. Integrated Documentation & Compliance:

Attach receipts, invoices, and business purpose proof to each card transaction. Built-in compliance checks flag non-deductible or over-limit spend.

4. Custom Policies & Approval Workflows:

Set strict category-based rules, thresholds, and approval processes to enforce budget discipline and accurate classification.

5. Analytics & Seamless System Integration:

Generate detailed spend reports and integrate directly with accounting/ERP systems to support accurate UAE corporate tax filings and VAT returns.

Take control of your business entertainment spending with precision. Book a demo with Alaan today to see how our corporate card and spend management solutions can help you save money, stay compliant, and maximise deductions under UAE tax law.

Conclusion

Efficiently managing business entertainment expenses in the UAE requires more than just awareness of deduction percentages; it demands precise classification, meticulous documentation, and strict adherence to corporate tax and VAT regulations.

By applying the 50% cap for client-related events, use the full 100% allowance for staff entertainment, and maintaining accurate VAT treatment, finance leaders can optimise tax savings while reducing compliance risks.

Transform the way your business handles entertainment expenses.

Book your free Alaan demo today and see how you can cut costs, eliminate compliance headaches, and unlock maximum value from every business entertainment expense under the UAE’s 2025 tax framework.

Frequently Asked Questions (FAQs)

1. What types of entertainment expenses require approval before payment in the UAE?

Expenses involving client entertainment above a set threshold, mixed events, or high-value staff functions generally require prior approval to ensure budget control and compliance with corporate tax rules.

2. Can entertainment expenses related to virtual events be claimed as tax-deductible?

Yes, virtual event costs for clients or staff are deductible under the same 50% (client) and 100% (staff) rules, provided proper documentation and business purpose are maintained.

3. Are gifts to clients or staff considered business entertainment expenses?

No, gifts are typically classified separately and not covered under entertainment expense deductions; they may have distinct tax treatment and documentation requirements.

4. How should businesses account for VAT on overseas entertainment expenses for clients or staff?

VAT treatment depends on the local tax laws where the expense is incurred; generally, UAE VAT recovery rules apply only within UAE jurisdiction, so careful cross-border tax advice is necessary.

5. Is there a limit to the frequency of deductible staff entertainment events?

No explicit legal limit exists; however, expenses must be reasonable, comply with company policy, and have proper documentation to ensure full deductibility.

6. Can businesses claim entertainment expenses for third-party organisers hosting client events?

Yes, but only if the expense is invoiced directly to the business with detailed proof of business purpose, and the deduction limits and VAT rules are applied accordingly.

%201.avif)