Managing VAT obligations in the UAE can sometimes feel complex, especially when it comes to deregistration. Despite this, the country maintains one of the highest tax compliance rates in the world, with 98.8% of VAT-registered businesses submitting their returns on time.

This shows that while most businesses stay on track, challenges like VAT deregistration can still feel daunting. For companies that no longer meet the registration threshold or have ceased operations, deregistration is a crucial step to prevent unnecessary penalties.

This guide explains the VAT deregistration process, outlines the necessary steps, and shows common challenges, helping you approach this task with confidence and stay fully compliant.

Key Takeaways:

- VAT deregistration in the UAE is required when a business’s turnover falls below the threshold, operations cease, or it shifts to exempt supplies.

- Mandatory deregistration applies when businesses no longer meet VAT registration criteria, while voluntary deregistration is possible for companies with lower turnover or strategic needs.

- The process requires submitting key documents like VAT returns, proof of turnover, and settlement of outstanding VAT liabilities.

- Post-deregistration, businesses must stop charging VAT, maintain records for five years, and stay compliant with other regulations to avoid penalties.

- Challenges during deregistration include delays in approval, settling VAT liabilities, and ensuring all returns and documentation are accurate.

Understanding VAT Deregistration in the UAE

VAT deregistration is the process by which a business cancels its VAT registration with the Federal Tax Authority (FTA). It applies when a company no longer needs to remain registered for VAT. This can happen either because the business no longer meets the criteria set by the FTA or because it chooses to opt out voluntarily.

In most cases, deregistration takes place when a company’s annual turnover falls below the mandatory VAT registration threshold or when the business shuts down operations. The purpose of VAT deregistration is to ease businesses from tax obligations once they no longer qualify for or need VAT registration.

That said, the process must be handled carefully. Following the proper steps ensures compliance and helps businesses avoid penalties or unnecessary complications with the tax authority.

Once you know what VAT deregistration is, it becomes helpful to explore under which situations a business may need to apply for it.

Also Read: Filing and Making VAT Payments in the UAE

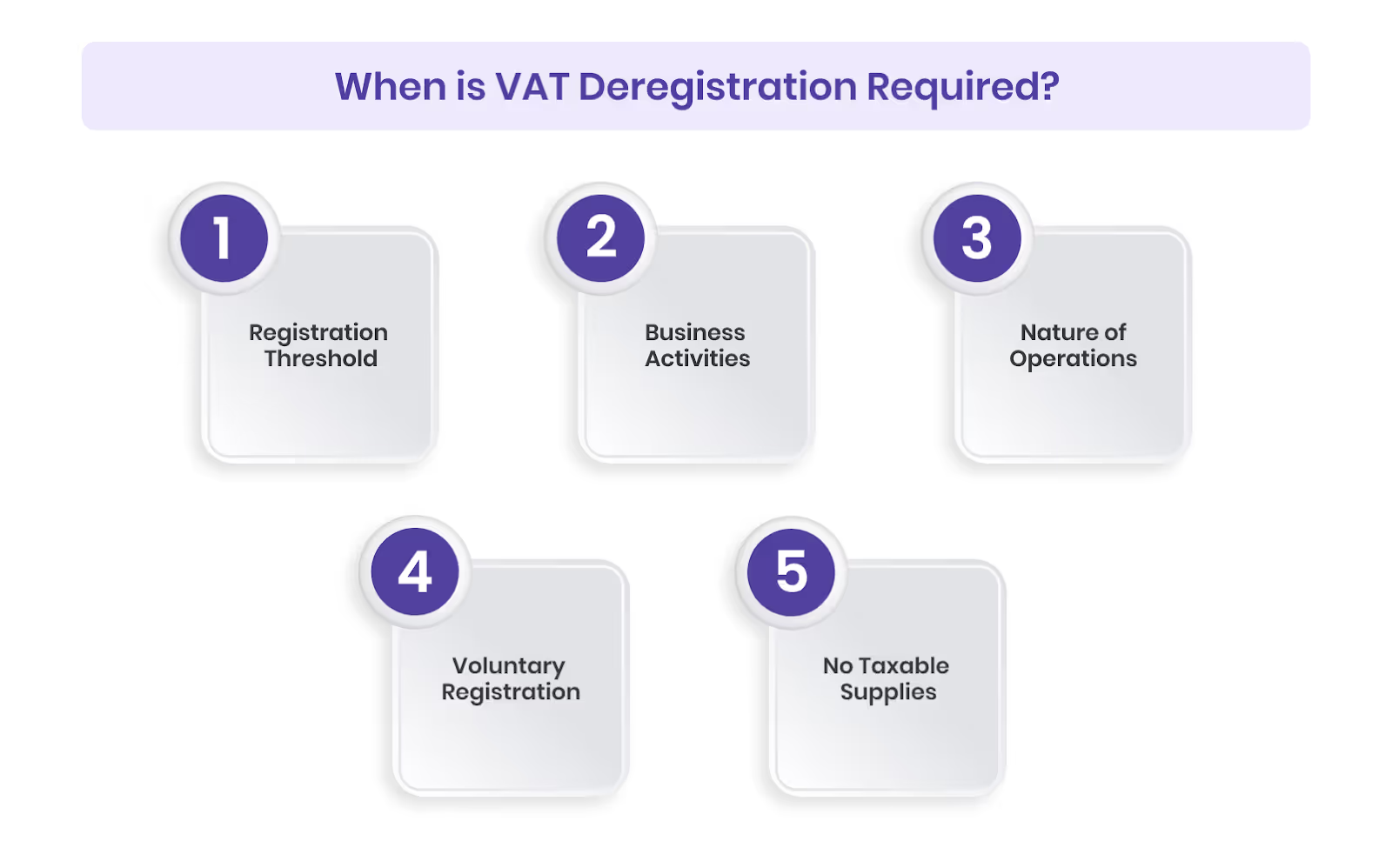

When is VAT Deregistration Required?

VAT deregistration in the UAE becomes necessary under certain circumstances, mainly when a business no longer qualifies for mandatory VAT registration. This could happen due to a drop in turnover, the closure of the company, or a change in how the business operates.

Deregistration is required in the following cases:

1. When Annual Turnover Falls Below the Mandatory Registration Threshold

One of the most common reasons for VAT deregistration is when a business’s annual taxable turnover drops below the mandatory threshold of AED 375,000. If, within 12 months, the value of taxable supplies falls under this limit, the business no longer needs to stay VAT-registered.

For example, if a business records AED 350,000 in taxable turnover in a year, it may apply for deregistration. In such situations, the company is relieved from the responsibility of charging VAT on its sales and submitting VAT returns.

2. Permanent Closure of Business Activities

If a business permanently shuts down or dissolves, it must also apply for VAT deregistration. This typically occurs when a company ceases to operate, sells all its assets, or is dissolved as a taxable entity.

For instance, a company that decides to close its operations in the UAE is required to deregister for VAT once business activities officially stop.

In these cases, all VAT returns are filed up to the date of closure, and any pending tax dues are settled before deregistration.

3. Change in Business Structure or Nature of Operations

VAT deregistration may also be required when a company undergoes major changes in its operations or structure that affect VAT obligations. For instance, if a business stops making taxable supplies and only deals with VAT-exempt goods or services, it may no longer need VAT registration.

If a company merges with or is acquired by another entity, the existing VAT registration may be cancelled, and a new registration may be applied under the new business structure.

4. Not Meeting the Voluntary Registration Threshold

Businesses that opted for voluntary VAT registration may also find themselves eligible for deregistration if their turnover drops below the voluntary threshold of AED 187,500. This is more common among smaller businesses or those with low or irregular taxable supplies.

For instance, a business that voluntarily registered for VAT but later records turnover below AED 187,500 can apply for deregistration.

5. No Taxable Supplies

A business that no longer makes taxable supplies can also apply for VAT deregistration. This happens when the company stops selling goods or services that fall under VAT, and instead shifts to activities that are exempt or zero-rated.

For example, if a business previously sold taxable products but later transitions to offering only exempt financial services, it may no longer need to stay VAT-registered.

Knowing the circumstances for deregistration helps in understanding the different types and how each applies to various business scenarios.

Different Types of VAT Deregistration

In the UAE, VAT deregistration can take place under two main scenarios: mandatory deregistration and voluntary deregistration. Both allow businesses to cancel their VAT registration with the Federal Tax Authority (FTA), but the conditions and reasons for each are different.

1. Mandatory VAT Deregistration

Mandatory deregistration applies when a business is legally required to cancel its VAT registration due to changes in its financial position or operations. This process is not optional; businesses must initiate it to remain compliant with UAE VAT law.

Situations that require mandatory VAT deregistration include:

- Business Ceases Operations: If a company permanently closes down, is liquidated, or dissolved, it must apply for VAT deregistration.

- Business Shifts to Exempt Supplies: When a business moves to dealing exclusively in VAT-exempt goods or services, it no longer qualifies for VAT registration.

- Turnover Below the Mandatory Threshold: If a business’s taxable turnover falls below AED 375,000 in 12 months, deregistration is required.

2. Voluntary VAT Deregistration

Voluntary deregistration happens when a business chooses to cancel its VAT registration, even though it is not strictly required to by law. This usually occurs when VAT registration no longer suits the company’s operations or strategy.

Situations that allow voluntary VAT deregistration include:

- Turnover Below the Voluntary Threshold: Businesses that registered voluntarily (with turnover under AED 375,000) can deregister if their turnover drops below AED 187,500.

- Strategic or Operational Reasons: A business may decide deregistration is the better option if it no longer makes taxable supplies, or if staying VAT-registered is proving too costly or unnecessary for its current model.

After understanding the types, the next step is identifying the documents needed to support a smooth deregistration process.

Key Documents Needed for VAT Deregistration in the UAE

When applying for VAT deregistration in the UAE, businesses must provide certain documents to the Federal Tax Authority (FTA) to ensure the request is processed smoothly and without delays.

These documents serve as proof that the business has met all compliance requirements and is eligible for deregistration. Below are the key documents required for VAT Deregistration.

1. Trade Licence or Business Closure Certificate

A copy of the valid trade licence or an official closure certificate issued by the relevant authority is required. This is especially important for businesses that have permanently shut down, as it confirms the company is no longer in operation.

2. VAT Returns for the Last Tax Period

The final VAT return covering the last taxable period must be submitted. This return should include all taxable supplies, input VAT, and any outstanding liabilities, ensuring the business has completed its VAT obligations before applying for deregistration.

3. Proof of Turnover Below VAT Registration Threshold

If deregistration is being requested because turnover has fallen below the mandatory threshold of AED 375,000, supporting evidence such as audited financial statements or turnover reports must be provided. This shows that the business no longer meets the VAT registration requirement.

4. Final VAT Liability Settlement Proof

Documents confirming the payment of all outstanding VAT dues, including VAT on stock, assets, or services, are required. This may include payment receipts, bank transfer slips, or FTA-issued confirmation letters.

5. Bank Account Statement or Proof of Payment

A copy of the business’s bank statement or receipts confirming settlement of VAT dues must also be submitted. This helps validate that all final payments to the FTA have been cleared.

Alongside the required documents, businesses can follow a structured process to officially apply for VAT deregistration through the FTA.

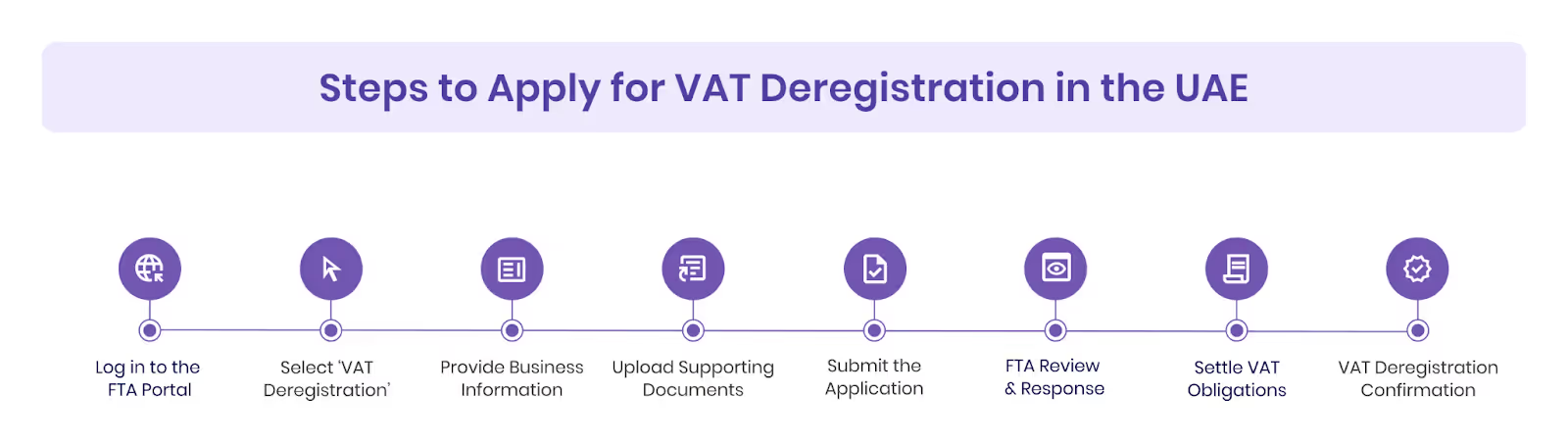

Steps to Apply for VAT Deregistration in the UAE

Applying for VAT deregistration in the UAE is a formal process managed through the Federal Tax Authority (FTA). By following the steps carefully, businesses can ensure compliance and avoid penalties for late or incorrect deregistration.

1. Log in to the FTA Portal

Start by accessing the official FTA e-Services portal with your registered login details. Only the business’s authorised signatory is permitted to submit the VAT deregistration request.

2. Select ‘VAT Deregistration’

From the portal dashboard, choose the VAT deregistration option. You’ll be asked to specify the reason, such as business closure, turnover falling below the threshold, or shifting to exempt supplies.

3. Provide Business Information

Enter the required details, including:

- Trade licence number

- Tax Registration Number (TRN)

- Last taxable period details

- Proposed effective date of deregistration

4. Upload Supporting Documents

Attach the documents that support your application. These may include:

- Trade licence or closure certificate

- Financial statements or turnover records

- Previously filed VAT returns

5. Submit the Application

Double-check all the information for accuracy before submitting the request online. Once submitted, you’ll receive an acknowledgement and a reference number from the FTA.

6. FTA Review and Response

The FTA will review your application and may request further details or clarifications. After verification, they will either approve or reject the request.

7. Settle VAT Obligations

Before approval, ensure that all VAT dues are settled. This includes outstanding returns, unpaid liabilities, and VAT due on stock, assets, or services where applicable.

8. Receive VAT Deregistration Confirmation

Once approved, the FTA will issue a VAT deregistration certificate. This certificate serves as official confirmation that your business is no longer VAT-registered.

Even after deregistration, businesses are required by UAE VAT law to maintain their VAT records for at least five years to meet compliance and audit requirements.

Once the application is submitted and approved, there are post-deregistration responsibilities that businesses need to manage carefully.

Also Read: How to Manage VAT in QuickBooks for UAE and KSA

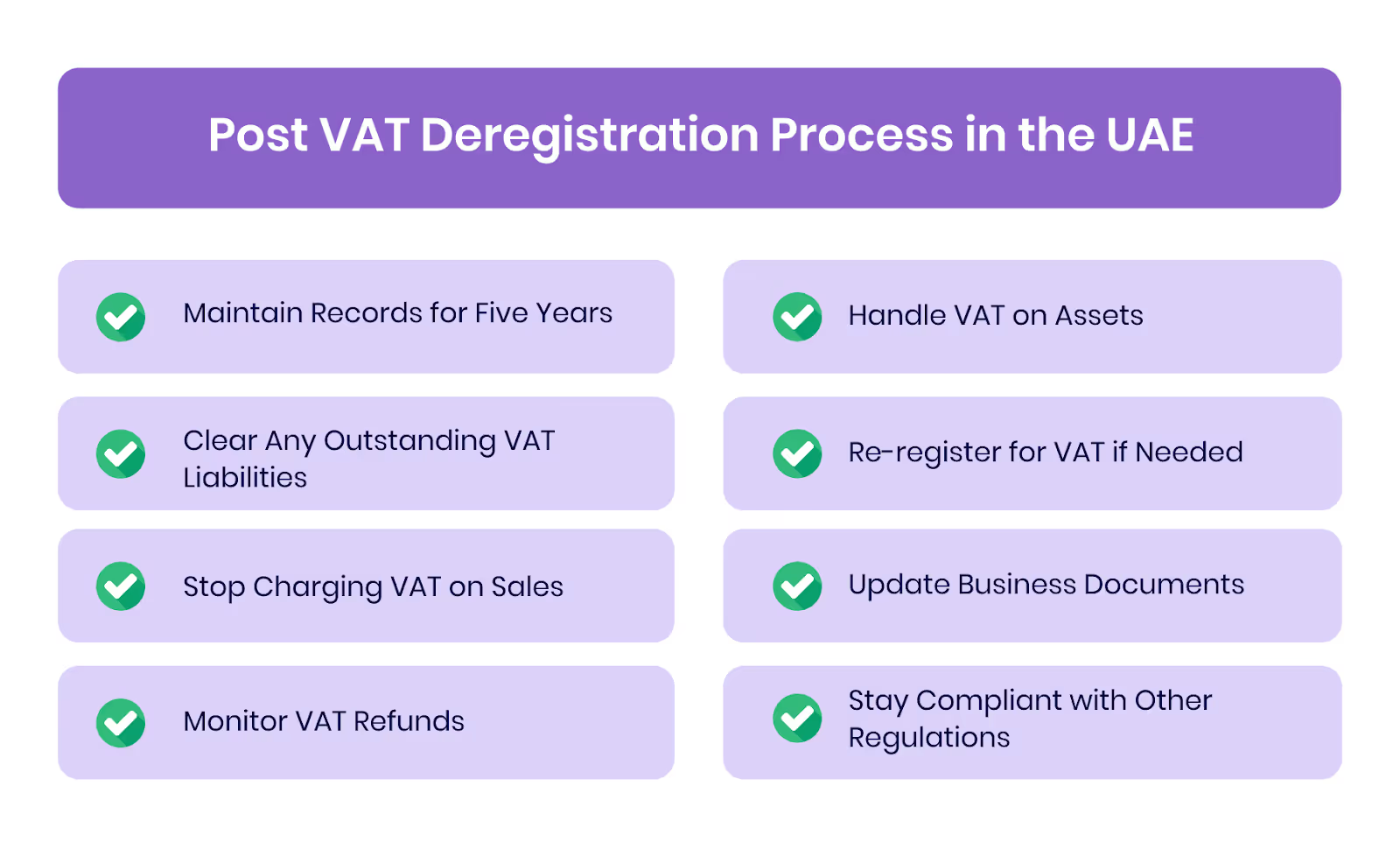

Post VAT Deregistration Process in the UAE

Once a business has completed the VAT deregistration process in the UAE, it still has a few important responsibilities to attend to. Deregistration simply shifts the obligations. To ensure a smooth transition, businesses should pay attention to the following post-deregistration steps.

1. Maintain Records for Five Years

Even after deregistration, businesses are legally required to keep their VAT records for at least five years. These records include:

- Issued and received invoices

- VAT returns filed during the registration period

- Correspondence with the FTA

- Proof of VAT payments and refunds

2. Stop Charging VAT on Sales

Once deregistered, businesses can no longer charge VAT on supplies. This means:

- Invoices should not include VAT.

- Accounting systems must be updated to remove VAT calculations.

Failing to do this could lead to errors, such as charging customers VAT without being registered.

3. Monitor VAT Refunds or Claims

If a business is entitled to VAT refunds from excess payments made while registered, the FTA may still process these after deregistration. Businesses should:

- File any refund claims before deregistration is finalised.

- Keep track of outstanding claims or refunds and provide necessary documentation.

4. Handle VAT on Assets

VAT may apply to assets held at the time of deregistration. For example:

- Stock: Businesses must calculate and remit VAT on unsold goods.

- Capital goods: Assets like machinery or property may attract VAT if they are sold or repurposed for non-business use after deregistration.

5. Re-register for VAT if Needed

If a business’s taxable turnover rises above AED 375,000 in the future, it must reapply for VAT registration through the FTA portal and resume VAT compliance.

6. Update Business Documents and Processes

Post-deregistration, businesses should make updates across their operations, including:

- Invoices: Remove VAT details and TRN references.

- Accounting systems: Delete VAT codes to prevent errors.

- Website and marketing materials: Remove any mention of VAT registration or pricing that includes VAT.

7. Stay Compliant with Other Regulations

Even without VAT registration, businesses must continue to follow UAE corporate and tax regulations. This includes proper bookkeeping, filing required documents, and keeping up with any legal or regulatory changes.

While completing the post-deregistration steps, businesses may still encounter certain challenges that can affect the overall process.

Common Challenges Faced During VAT Deregistration

While VAT deregistration in the UAE is generally a clear process, many businesses run into challenges that can slow things down or make the procedure more complex. Being aware of these issues in advance can help companies to prepare better and avoid unnecessary delays.

Below are some of the most common challenges faced during VAT deregistration and their solutions:

How Alaan Simplifies VAT Deregistration for UAE Businesses?

VAT deregistration can be a complex task for UAE businesses. At Alaan, we have made this process simpler by offering an automated platform that ensures compliance while simplifying financial reporting and record-keeping. Here’s how Alaan helps firms:

- Automated VAT Data Tracking: Alaan automatically tracks and categorises VAT-related expenses, maintaining accurate records for deregistration. This reduces administrative workload and minimises errors.

- Real-Time Financial Reporting: Gain immediate visibility into your financial position, track outstanding VAT liabilities, and stay compliant throughout the deregistration process.

- Simplified Document Management: Store and retrieve all VAT-related documents, including invoices and receipts, in a centralised system. Records remain organised and audit-ready for FTA submissions.

- Error Reduction and Compliance Assurance: Automation of VAT data entry and verification helps minimise errors, ensuring adherence to Federal Tax Authority (FTA) standards during deregistration.

- Accounting Software Integration: Alaan integrates smoothly with platforms like QuickBooks and Xero, ensuring all VAT data is accurately reflected in financial reports, simplifying the overall deregistration process.

Schedule a demo to learn more.

Wrapping Up

VAT deregistration in the UAE is a key step for businesses that no longer need to remain VAT-registered, whether due to changes in turnover or business closure. Completing the process correctly helps ensure compliance, avoid penalties, and maintain seamless operations.

At Alaan, we recognise the challenges VAT deregistration can pose for business finance. Our platform offers intuitive tools to manage VAT compliance, automate financial reporting, and guide you through a smooth deregistration process.

Book a quick demo today to learn how Alaan can simplify VAT deregistration, ensure compliance, and simplify your financial reporting and documentation processes.

FAQs

1. How long does it take to complete the VAT Deregistration process?

The VAT deregistration process usually takes 2–4 weeks, depending on the completeness of the application and documentation. The FTA may request additional information before issuing confirmation.

2. Can I still charge VAT after deregistration?

No, once deregistration is approved, VAT cannot be charged on goods or services. Any outstanding VAT must be cleared before deregistration is finalised.

3. What are the consequences of failing to settle VAT dues before deregistration?

If dues are unpaid, the FTA will not process the deregistration, and penalties may be applied. So, VAT on assets, stock, or services must be settled beforehand.

4. Can VAT be refunded after deregistration?

Yes, eligible VAT refunds can still be claimed after deregistration, but submit the refund request before completing the process.

5. How can I ensure compliance during VAT deregistration?

File all VAT returns, pay outstanding dues, and submit all necessary documents correctly. Consult a tax expert if any step is unclear.

%201.avif)