In the UAE’s fast-paced business environment, even profitable small businesses can face cash flow disruptions due to late payments and operational delays. For many SMEs, these bottlenecks result in postponed supplier payments, missed payroll, and stalled growth opportunities.

Card payment solutions offer a practical way to bridge these gaps by speeding up receivables, improving liquidity, and giving businesses real-time visibility into transactions. This shift isn’t just a passing trend, according to GlobalData, card payments in the UAE are expected to reach AED 565.5 billion by 2025, growing at 11% annually.

Whether you’re running a retail outlet, a consultancy, or an e-commerce store, accepting card payments can help you maintain healthy cash flow, strengthen compliance with UAE VAT and Central Bank regulations, and enhance the customer experience.

This blog details how to set up card payments for small businesses in the UAE, providing actionable steps and techniques to help founders and CFOs improve their company's financial resilience.

Key Takeaways

- Selecting the right merchant provider and payment infrastructure, fully compliant with UAE VAT and Central Bank mandates, is essential for secure, seamless operations.

- Costs and settlement times vary significantly between providers; a comprehensive side-by-side analysis prevents hidden charges and compliance pitfalls.

- Card payment adoption accelerates cash flow cycles, improves audit trails, and directly supports regulatory and e-invoicing requirements under UAE law.

Understanding Card Payments

Card payments, including debit and credit card transactions, are essential for modern UAE businesses, enabling electronic fund transfers at physical points of sale or online.

The process involves several key parties: the cardholder, merchant, acquiring bank, payment processor, card network (e.g., Visa, Mastercard), and issuing bank. Transaction authorisation happens instantly, with funds typically settled within one to two business days.

Adopting card payments improves cash flow agility by minimising delays inherent in cash or cheque handling.

Also, electronic payments create reliable audit trails, facilitating VAT compliance and easing statutory reconciliation under UAE regulations.

For businesses facing persistent cash flow challenges, let's examine the benefits of card payment acceptance, a critical strategic priority.

What are The Benefits of Accepting Card Payments?

For businesses dealing with liquidity challenges and shifting regulatory demands, accepting card payments delivers targeted advantages that directly address pressing operational needs.

Below are some of the benefits of accepting card payments for small businesses:

- Accelerated Revenue and Cash Flow: Over 70% of UAE retailers report higher revenue and increased customer footfall since adopting digital and card payment solutions. Card transactions expedite settlement to as little as one to two days, reducing working capital gaps and supporting more reliable cash flow management.

- Operational Security and Cost Reduction: Minimising the use of physical cash directly reduces security risks and administrative overheads. Innovative UAE programmes such as Jaywan deliver localised, cost-effective processing and keep more transaction value within the country’s economy.

- Enhanced Professional Image and Customer Confidence: Card acceptance signals credibility and professionalism, boosting client trust and satisfaction. In a market where digital payment is now the norm, businesses without these capabilities risk being seen as outdated and losing clients to more agile competitors.

- Regulatory Compliance and Integration: Card payments facilitate VAT reconciliation and create reliable digital trails, supporting audit-readiness and compliance with UAE's Federal Tax Authority standards. Many providers now offer seamless integration with local accounting systems and ERP platforms, ensuring ongoing regulatory alignment and operational efficiency.

- Competitive and Strategic Advantage: Adopting card payments is a strategic differentiator in B2B and B2C settings, as commercial cards offer extended credit, rebates, and automation options that optimise both buyer and supplier cash cycles, directly supporting cost management and supplier relations.

Selecting the right card payment acceptance method is important for enterprises that want to optimise the transaction speed and ensure full compliance with stringent local regulatory standards.

Payment Acceptance Models for Small Businesses: What’s Available and What Suits Whom?

Each payment acceptance model offers distinct advantages in terms of speed, security, regulatory alignment, and customer convenience. You should prioritise solutions that align with both operational workflows and compliance objectives.

Below is an overview of the most relevant models available in the UAE:

1. In-Person Payments (POS Terminals):

- Physical card terminals facilitate debit and credit transactions at retail counters, providing seamless integration with cash registers and inventory systems.

- Equipped with contactless, chip, and magnetic stripe support, POS solutions are fully compliant with PCI DSS standards and Central Bank of the UAE mandates.

- Best suited for: High-volume retail, F&B outlets, and service businesses prioritising rapid checkout and in-store customer experience.

2. Mobile Card Readers:

- Portable devices paired with smartphones or tablets enable card payments on the go, ideal for delivery, events, or field services.

- Offer digital receipts and real-time sales tracking, with robust encryption and compliance with local acquirer requirements.

- Best suited for: SMEs with mobile operations, freelance professionals, market vendors, and service-based field teams.

3. Remote Payment Acceptance (Virtual Terminals, Payment Links):

- Virtual terminals enable card payment authorisation via secure online portals—no physical terminal is required.

- Payment links can be generated for SMS or email, allowing remote clients to complete transactions instantly.

- Both methods streamline non-face-to-face commerce, with electronic trails ensuring VAT and audit alignment.

- Best suited for: Consultancies, remote service providers, B2B contracting, and invoice-based SMEs.

4. Online Payment Gateways:

- Integrated digital platforms handling website or app-based transactions, featuring automatic VAT invoicing and fraud prevention measures.

- Gateways support a wide array of card schemes and digital wallets, facilitating recurring billing and multi-currency support.

- Best suited for: E-commerce, SaaS businesses, and entities engaged in cross-border sales or regular digital purchases.

5. QR Code and Contactless Payments:

- Customers pay by scanning QR codes generated by payment apps (such as Jaywan), removing the need for physical terminals.

- Fast settlement and broad accessibility across local banking infrastructure, with data residency and compliance assured.

- Best suited for: Pop-ups, cafés, events, and quick-turnover venues targeting tech-savvy audiences.

After understanding the basics and benefits of card payment, let’s have a look at the steps to set up card payments in businesses.

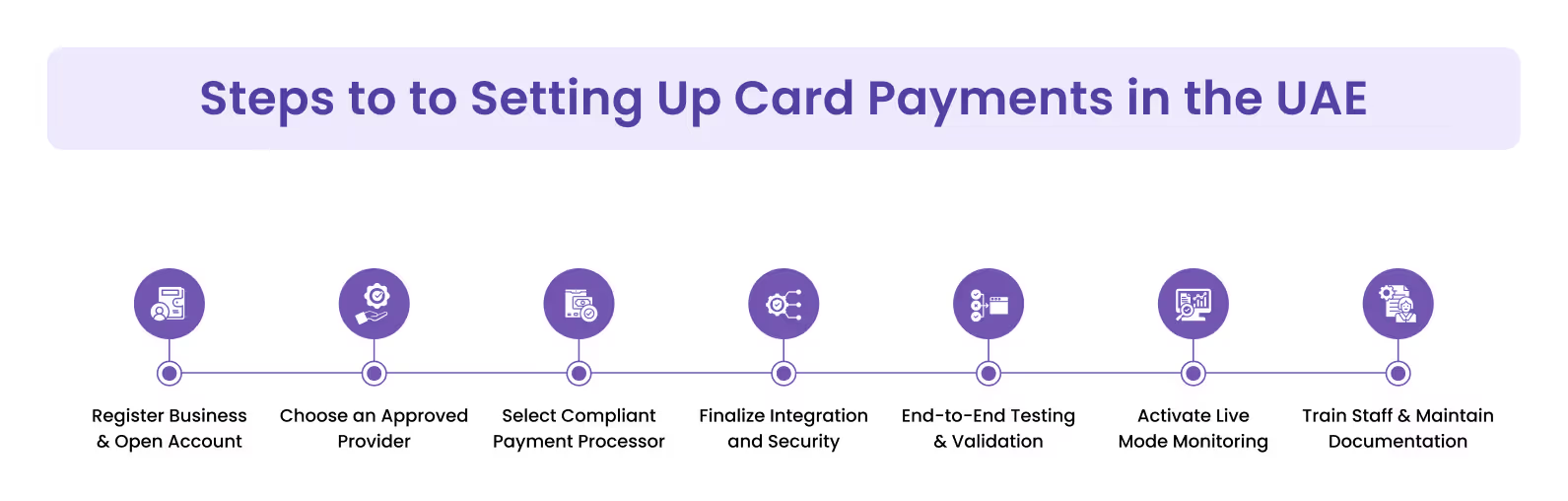

Step-by-Step Guide to Setting Up Card Payments in the UAE

Setting up card payments involves a sequence of technical, regulatory, and operational actions, each with legal and financial implications. The following detailed steps ensure your business is both compliant and efficiently positioned for reliable receivables and a strong customer experience in the UAE.

1. Establish a UAE-registered Business and Corporate Bank Account

- Register your company with the appropriate mainland or free zone authority. Secure all relevant licences (trade, VAT). A valid trade licence is mandatory for all PSP and merchant account applications.

- Open a corporate bank account with a UAE bank, a regulatory prerequisite for payment processing and settlement.

2. Select an Approved Merchant Account Provider

- Merchant accounts hold card transaction proceeds pending settlement to your main business account.

- Choose from banks or PSPs authorised by the UAE Central Bank. Prioritise options with AED settlement and rapid payout capability.

- Prepare all due diligence documents, including trade license, corporate documents, Emirates ID of shareholders/directors, business address proof, and recent bank statements.

3. Evaluate and Choose a Compliant Payment Gateway or Processor

- Assess providers for local compliance (PCI DSS, VAT e-invoicing, data privacy), UAE Central Bank licensing, and region-specific integrations (ERP, accounting platforms).

- Compare integration models: POS terminals for in-person, online gateways for eCommerce, and payment links for remote or invoice-driven businesses.

4. Complete Technical Integration and Security Setup

- For online businesses, integrate the chosen payment gateway APIs into your website or application. For POS, activate and configure physical terminals or pair with mobile devices.

- Ensure your system supports essential payment methods (Visa, Mastercard, Apple Pay, Google Pay, and local cards). Set transactions in AED to avoid conversion issues.

- Activate 3D Secure authentication and SCA where required. Confirm fraud detection and automated reconciliation features.

5. Conduct End-to-End Testing and Compliance Validation

- Use test modes provided by most gateways to simulate successful and failed transactions.

- Audit VAT, invoice generation, and integration points for errors. Check compliance with PCI DSS, local data residency, and Central Bank standards before going live.

6. Activate Live Mode and Monitor Operations

- Switch to live credentials in all platforms and double-check payout settings for daily or weekly AED settlements.

- Continuously monitor transaction activity, chargebacks, decline rates, and compliance notifications to maintain uninterrupted, secure operations.

7. Educate Staff and Maintain Documentation

- Train relevant staff on PCI DSS requirements, refund/chargeback procedures, and daily reconciliation workflows.

- Retain all compliance and transaction documentation for VAT audits and financial reporting.

After successfully setting up card payments, it is also crucial to mitigate compliance risks and protect your revenue while accepting card payments.

Compliance Control and Risk Management in Card Payment Acceptance

Ensuring string compliance and effective risk management in card payment operations requires precise alignment with UAE legal mandates and global security standards.

The following are the pivotal domains and controls:

1. PCI DSS Adherence:

All payment acceptance infrastructure, whether in-person, online, or mobile, must comply with Payment Card Industry Data Security Standard (PCI DSS).

This includes strict requirements on cardholder data encryption, tokenisation, and vulnerability scans. Non-compliance exposes businesses to penalties, reputational risk, and potential suspension of payment services.

2. UAE Central Bank Licensing and Oversight:

Only use merchant acquirers and payment processors fully licensed by the Central Bank of the UAE. Regularly review provider status and confirm AED-based settlement to ensure regulatory continuity.

3. VAT and E-invoicing Compliance:

Electronic transaction records should be seamlessly integrated with e-invoicing systems, supporting real-time VAT calculation, automated reconciliation, and audit trails conformant with the UAE Federal Tax Authority (FTA) standards.

4. Data Residency and Privacy Law:

All payment data must be stored and processed as per UAE data residency laws and applicable privacy statutes. This is essential for safeguarding sensitive financial data from cross-border transfer risks.

Pro Tip: Maintain a contingency plan with your payment provider for system outages or breaches, and store compliance records for 5–7 years to meet UAE audit requirements.

Best Practices of Card Payment Implementation for Small Businesses

Securing efficient card payment operations in the UAE relies on upholding precise regulatory alignment and stringent data security. Below are mentioned some best practices to mitigate risks and support business continuity:

- Vendor Due Diligence: Engage only with payment providers licensed by the Central Bank and holding valid PCI DSS certification for full regulatory alignment.

- Strong Data Security: Maintain firewalls, encrypt all transaction data, and conduct regular risk assessments in line with PCI DSS mandates; these measures protect customer information and avert costly breaches.

- Integrated Compliance: Seamlessly connect payment solutions to VAT and e-invoice systems; doing so supports instant audit trails and simplifies statutory reporting under Federal Tax Authority guidelines.

- Staff Training & Access Controls: Train staff on security protocols and limit access to cardholder data, minimising internal and external fraud risks.

- Monitor and Test: Constantly monitor payment systems, automate suspicious activity alerts, and perform regular technology updates to counter evolving threats.

By adopting these practices, UAE SMEs can reduce fraud risk, ensure regulatory compliance, and maintain uninterrupted payment operations.

How Alaan Simplifies Online Payment With Corporate Cards

Alaan’s corporate cards enable UAE companies to instantly issue multiple physical and virtual cards to teams or individuals, each configured with custom budgets, category restrictions, and real-time usage limits, critical for maintaining financial control in a region governed by strict regulatory standards.

This granular control over card issuance and spending ensures adherence to company policies and Dubai's evolving compliance mandates. Benefits of having a corporate card are:

- Instant Issuance and Budget Management: Businesses can create unlimited cards with no additional cost, assign them to departments or projects, and enforce budget limits.

- Integrated Online and Contactless Payments: Alaan cards are fully compatible with digital wallets (Google Pay, Apple Pay) and support seamless online payments, essential for the UAE’s rapidly digitising economy and remote work environments.

- Automated Expense Tracking: The platform uses AI-powered receipt matching and automated expense categorisation. This eliminates manual paperwork and ensures real-time visibility into every online transaction, critical for accurate VAT reporting and statutory compliance.

- Cashback and Cost Efficiency: Unlike traditional cards, Alaan offers up to 2% unlimited cashback on eligible transactions, directly reducing operational costs and enabling reinvestment into business growth.

- Full Regulatory Integration: All spend data and receipts are automatically synchronised with UAE-compliant accounting software, enabling audit-ready records, streamlined VAT filing, and simplified e-invoicing per FTA requirements.

- Enhanced Security: Enterprises can freeze cards instantly and receive fraud alerts in real-time, significantly reducing the risk of misuse or unauthorised transactions.

Alaan's automated integrations and regulatory compliance make online payments faster, more secure, and fully transparent, transforming how small businesses manage spend and maintain audit-ready financial governance. Book a demo today!

Conclusion

In the current business environment, establishing a card payment system is no longer optional; it is fundamental to financial agility and competitive growth.

By prioritising secure, auditable card payment infrastructure, finance leaders empower their organisations to overcome cash flow bottlenecks.

At Alaan, we understand that true business progress hinges on effortless, transparent payment management. Our all-in-one corporate card solution puts precise control, real-time analytics, and seamless regulatory integration at your fingertips, eliminating manual admin and compliance uncertainty.

Schedule a free demo today to begin your seamless payment journey.

Frequently Asked Questions (FAQs)

1. How long does it take for card payment funds to settle into my UAE business account?

Most local providers settle funds within one to two business days, but timelines may vary by provider and payment method.

2. Can I charge a card processing fee to customers in the UAE?

Some UAE businesses apply surcharges (typically 1.5–2.5%) for card transactions, but this should be transparently disclosed and in line with UAE Central Bank guidance.

3. Is a trade licence mandatory for UAE SMEs to accept card payments?

Yes, a valid UAE trade licence is a legal prerequisite for opening a merchant account or payment gateway for commercial card acceptance.

4. What currencies can I accept for card payments in the UAE?

Card payment gateways support AED and major international currencies; settlement is usually in AED, with conversion fees applying for foreign-denominated transactions.

5. Are there instant approval solutions for card payment set-up?

Most providers require standard onboarding and verification, but some offer fast-track digital setup with basic KYC and trade licence submission, enabling live account activation within 1–3 days.

6. How can I reconcile card payments with UAE VAT returns?

Integrate your payment gateway with VAT-compliant accounting software to automatically capture transaction-level data for real-time VAT e-invoicing and reporting to the Federal Tax Authority.

%201.avif)