Managing petty cash seems simple, but in many organisations, it becomes a frequent source of audit findings, missing receipts, VAT issues, and unclear spending trails. Even with digital payments and corporate cards widely available, petty cash persists because teams occasionally need fast, low-value payments that don’t fit procurement cycles or reimbursement workflows.

However, without the right controls, petty cash can quickly become a black box difficult to monitor, reconcile, or justify during audits. This guide explains how to manage petty cash correctly: through clear policies, proper segregation of duties, consistent documentation, and disciplined reconciliation. It also outlines when petty cash should not be used, the risks to monitor, and modern alternatives that provide far better visibility and compliance.

In this blog, we break down everything you need to run a petty cash account effectively, from setting up the fund to managing day-to-day transactions and avoiding common audit problems.

Key Takeaways

- Petty cash should be used only for small, urgent, low-value payments and must be tightly controlled.

- The biggest risks come from missing receipts, vague spending categories, and reconciliation gaps.

- Strong petty cash management requires clear rules, segregation of duties, and regular cash counts.

- Modern alternatives, especially controlled corporate cards, eliminate most petty cash risks.

What Petty Cash Is and Why It Still Exists

Despite the rise of digital payment tools and corporate cards, many organisations continue to maintain a petty cash fund for immediate, low-value needs such as courier services, small office supplies, incidental travel costs, or emergencies that fall outside standard purchasing workflows.

Petty cash is essentially a small pool of cash held on hand to provide speed and convenience. But this convenience also introduces risks: missing receipts, undocumented spending, VAT non-compliance, misuse, and reconciliation discrepancies. For these reasons, modern finance teams increasingly view petty cash as a transitional tool necessary in some cases today but gradually replaced by more controlled digital alternatives.

Before any modernisation can happen, the existing petty cash process must be handled properly, consistently, and in full alignment with accounting and audit requirements.

Also read: Post Expenses to VAT and ERP Systems

When to Use a Petty Cash Fund and When Not To

A petty cash fund is helpful only in specific scenarios. Its purpose is to support small, urgent, infrequent payments where using procurement, reimbursement, or corporate cards would slow down operations unnecessarily.

Common legitimate use cases

- Minor office supplies (pens, batteries, printer ink)

- Courier or document delivery fees

- Low-value parking or transport costs

- Small hospitality items for internal meetings

- Emergency purchases when usual payment channels are unavailable

These are expenses that do not justify a purchase order, a reimbursement cycle or a corporate card transaction.

When petty cash should not be used

- Supplier or vendor payments

- Employee travel expenses meant to be tracked formally

- Recurring costs (utilities, contracts, subscriptions)

- Personal expenses under any circumstance

- Payments requiring VAT-compliant invoices

Using petty cash for these categories creates audit gaps, weakens spend visibility and increases the risk of errors or misuse.

Indicators that petty cash is being misused

- Frequent high-value withdrawals

- Repeated transactions for the same category (suggesting a recurring need)

- Missing or non-VAT-compliant receipts

- Requests that align more with convenience than necessity

The petty cash fund should remain a last-resort mechanism, not a workaround for formal processes.

Also read: Steps for Effective Employee Expense Management in the UAE

How to Set Up a Petty Cash Account

Setting up a petty cash account is straightforward, but the structure matters. The way the fund is established determines how well it can be controlled later. A clear setup process protects both the organisation and the custodian responsible for managing the cash.

1. Decide the fund size and assign a custodian

The fund size should reflect the organisation’s needs, typically enough to cover 2–4 weeks of small expenses without being large enough to create risk.

A single responsible custodian should be appointed, usually someone in admin or finance with day-to-day access. Their role includes holding the cash, recording each transaction and ensuring receipts are collected.

2. Establish policy, limits and permitted categories

Before the fund becomes operational, define:

- the maximum value per transaction,

- which expense categories are allowed,

- what documentation is required,

- who can authorise payments.

This prevents ambiguity and reduces friction for both employees and auditors.

3. Fund the petty cash account and create the initial journal entry

When the fund is first created, cash is withdrawn and recorded as an asset called Petty Cash.

The typical entry is:

- Debit: Petty Cash

- Credit: Cash/Bank

This establishes the float in the accounting system.

4. Communicate rules to staff

Employees sometimes view petty cash as an informal source of small payments. Communicating guidelines approved categories, documentation requirements and reimbursement steps ensures everyone understands that petty cash is governed like any other financial process.

Day-to-Day Petty Cash Process and Handling

Even a well-set-up fund can become chaotic without discipline in daily operations. The petty cash process should be simple, repeatable and clearly documented.

1. Making payments and obtaining receipts

Every petty cash transaction must be supported with a receipt or invoice. For UAE businesses, VAT-compliant invoices are required if the organisation intends to claim VAT. Whenever possible, the employee making the purchase should collect the receipt immediately to avoid gaps later.

2. Recording each transaction

Entries should be logged in a petty cash sheet or petty cash book with fields for:

- date,

- description,

- amount,

- category,

- receipt number,

- remaining balance.

This record is the backbone of petty cash control.

3. Submission and approval of petty cash claims

Although petty cash supports low-value payments, authorisation is still required. Some organisations require pre-approval for any withdrawal; others allow the custodian to approve within limits. Regardless of the model, the approval trail must be visible and reviewable.

4. Replenishment of the petty cash fund

Once the cash on hand drops below a threshold, the custodian submits receipts and the petty cash sheet to finance for replenishment. Finance verifies the entries and issues funds to restore the float to its original amount.

The replenishment journal typically debits the relevant expense accounts and credits Cash/Bank.

Also read: Chart of Accounts: A Practical Guide for UAE Businesses

Controls and Segregation of Duties

Petty cash is a small fund, but without strong controls, it becomes one of the easiest areas for misuse, undocumented spending, and audit findings. A well-managed petty cash system relies on basic but consistent internal controls.

Custodian, approver and reviewer must be different people

The person who holds the cash should not be the one authorising withdrawals or performing reconciliation. This separation prevents conflicts of interest and reduces opportunities for manipulation.

Physical safeguards and access control

Cash should be stored in a locked drawer or safe, and only the custodian should have access. Unrestricted access, whether intentional or due to shared office habits, is one of the fastest ways petty cash becomes unreliable.

Receipt and documentation standards

Finance should define strict documentation requirements:

- original receipts,

- vendor details,

- VAT fields when applicable,

- purpose of spend.

Missing or unclear documentation is the primary reason petty cash expenses are rejected during audits or VAT reviews.

Regular review of transactions and employee requests

Approvers should look for patterns: repeated requests from the same employee, similar amounts, out-of-scope categories or requests that should be routed through procurement instead. These patterns usually indicate misuse or gaps in understanding.

Reconciling and Balancing Petty Cash

Reconciliation is where petty cash integrity becomes visible. The custodian’s balance must match the recorded transactions and receipts at all times. Even small discrepancies erode confidence and create unnecessary audit issues.

Routine cash counts

Depending on transaction volume, counts may be done:

- daily,

- weekly, or

- monthly.

The frequency should match the organisation’s risk level and petty cash usage.

How to perform reconciliation

A reconciliation involves three components:

- Cash on hand

- Receipts and vouchers

- Recorded petty cash balance

These three must align. If not, the custodian must document the variance and investigate the cause of missing receipts, incorrect entries, or unrecorded payments.

Handling discrepancies

Small variances should not be ignored. They signal issues in record-keeping or control. Finance may require compensating entries or escalate repeated discrepancies to management for review.

Replenishing the fund

After validation, finance replenishes the fund to its original amount. The replenishment entry moves expenses from the petty cash sheet into the general ledger. Consistent replenishment ensures controlled, predictable accounting treatment.

Also read: VAT Compliance Health Check

Common Petty Cash Problems and How to Prevent Them

Petty cash issues tend to repeat across organisations because the risks are inherent: cash is easy to misuse, documentation is often weak and oversight can be inconsistent. Understanding the most common failure points helps finance teams prevent them.

1. Missing or unclear receipts

This is the most frequent problem. Receipts are lost, incomplete, or non–VAT compliant, making audit trails weak.

How to prevent it:

Require receipts immediately after spending; set rules for what qualifies as acceptable documentation; reject claims that lack detail.

2. Using petty cash for recurring or high-value expenses

Employees sometimes treat petty cash as a shortcut when formal procurement feels slow. This quickly distorts spending visibility.

How to prevent it:

Define strict category limits and redirect recurring or higher-value needs to approved workflows.

3. Float creep and undocumented reductions in cash

Creeping shortages, AED 20 today, AED 50 next week, indicate weak record-keeping or misuse.

How to prevent it:

Increase count frequency; enforce strong segregation of duties; escalate repeated variances.

4. Personal or mixed-use spending

When rules are unclear, some employees may justify questionable purchases as “work-related.”

How to prevent it:

Communicate boundaries clearly and require pre-approval above certain thresholds.

5. Audit and VAT non-compliance

Non-VAT receipts or poor documentation lead to disallowed claims and compliance issues.

How to prevent it:

Require VAT fields when applicable; train custodians on invoice standards; digitise receipts where possible.

Petty cash problems rarely arise from complex scenarios; they arise from inconsistent discipline. Strengthening the basics delivers the greatest impact.

Petty Cash Accounting Treatment and Reporting (UAE Context)

Petty cash is a balance sheet asset until funds are spent. When expenses occur, proper accounting treatment ensures accuracy in both financial reporting and VAT compliance.

How petty cash appears in the accounting system

- The petty cash fund is recorded as an asset under current assets.

- It remains unchanged unless the organisation increases or decreases the float.

- Expenses are only recognised when the fund is replenished.

This keeps the ledger clean and avoids daily entries that complicate reconciliation.

Recording petty cash expenses

When replenishing the float, the finance team allocates each receipt to the correct expense account office supplies, travel, postage, etc. These entries ensure expenses appear in the correct period and improve reporting accuracy.

VAT considerations for petty cash expenses

To claim VAT on petty cash purchases, invoices must include:

- supplier name and TRN,

- invoice date,

- invoice number,

- VAT amount,

- description of goods or services.

Non-compliant receipts cannot be used for VAT recovery, even if the underlying expense is legitimate.

Audit expectations in the UAE

Auditors expect:

- proper segregation of duties,

- documented reconciliations,

- approval evidence,

- clear petty cash policies,

- complete receipt trails.

Weak petty cash records are one of the most frequent audit observations for SMEs and mid-sized companies.

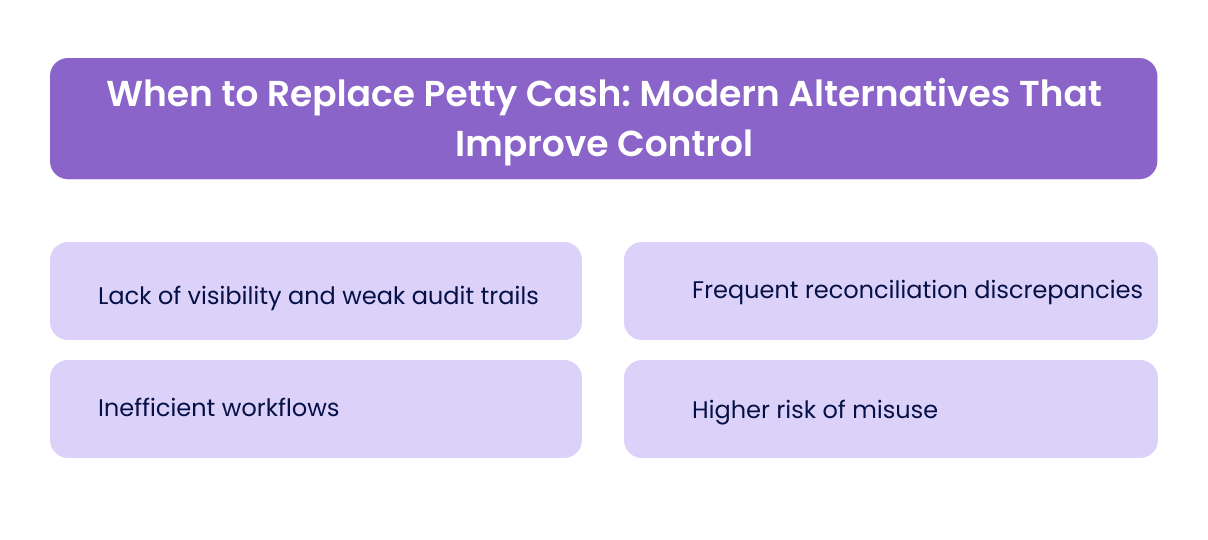

When to Replace Petty Cash: Modern Alternatives That Improve Control

Petty cash was designed for a workplace where payments were infrequent, paper-based, and heavily dependent on physical processes. That environment no longer exists. Today’s finance teams prioritise visibility, auditability and speed, none of which petty cash reliably delivers.

Most organisations eventually replace petty cash when they encounter one or more of these recurring issues:

1. Lack of visibility and weak audit trails

Cash transactions generate limited digital evidence. Even with strict documentation, finance teams face missing receipts, unclear descriptions, and inconsistent categorisation. This creates VAT risks in the UAE and complicates audits.

2. Frequent reconciliation discrepancies

Human error, delayed recording and occasional misuse result in mismatches between the physical cash and recorded balance. Even small variances consume time and erode trust.

3. Inefficient workflows

Employees must visit a custodian, submit paper receipts, and wait for replenishment, a process far slower than digital alternatives. As teams become more distributed, petty cash becomes impractical.

4. Higher risk of misuse

Cash is inherently harder to control than card-based or digital transactions. Even innocent shortcuts, holding receipts for later, rounding off amounts, weaken governance.

Because of these limitations, modern finance teams adopt digital-first alternatives that offer stronger control and complete audit trails.

Modern alternatives to petty cash

These tools eliminate the operational friction of cash handling while offering real-time visibility:

- Corporate cards with low spending limits

Ideal for teams that need occasional small payments with full transaction tracking.

- Prepaid cards for operational teams

Controls can be configured per department, per project or per employee.

- Digital expense management platforms

Employees capture receipts instantly, categories apply automatically, and workflows route approvals with full visibility.

- Centralised purchasing or micro-POs

For businesses with recurring small purchases that should move into procurement workflows.

These options improve governance, simplify accounting, reduce VAT exposure, and free finance teams from the administrative load of tracking physical cash.

[cta-1]

Also read: Modern Expense Management Guide

How Alaan Eliminates the Need for Petty Cash

Alaan enables organisations to retire petty cash by replacing physical funds with controlled corporate cards and automated expense workflows. Instead of managing a cash drawer, finance teams gain real-time visibility, strict control, and fully audit-ready documentation.

With Alaan:

- Corporate cards with granular spending controls

Issue physical or virtual cards with daily limits, merchant-category restrictions, and custom approval workflows. This gives employees the flexibility they need while ensuring spending stays compliant.

- Real-time transaction visibility

Every transaction appears instantly in the dashboard, showing merchant, amount, category and location. No waiting for custodians to update petty cash logs or submit receipts.

- Automated receipt capture & VAT validation

Employees upload receipts through the app or email. Alaan’s AI extracts invoice details, checks VAT fields and flags mismatches automatically. This prevents non-compliant or missing receipts from entering the system.

- No physical cash, no discrepancies

Removing cash eliminates shortages, misuse, and reconciliation problems entirely.

- Seamless ERP integration

All card transactions flow directly into the ERP with the correct coding and documentation. Month-end reconciliation becomes significantly simpler compared to manual petty cash handling.

- Complete audit trail

Auditors get complete digital evidence: transaction details, receipt images, VAT fields, approval logs and timestamps, all in one place.

By shifting from petty cash to Alaan’s corporate card-based controls, organisations gain transparency, reduce compliance risk, and eliminate the operational friction of managing physical funds.

[cta-12]

Essential Best Practices If You Still Use Petty Cash

Even though petty cash is becoming less relevant in modern finance operations, some organisations still rely on it for operational convenience. If you maintain a petty cash fund, keeping the process tight is critical for auditability and VAT compliance.

1. Set a reasonable fund size

Petty cash should cover only small, infrequent needs. Oversized funds increase risk and make reconciliation harder.

2. Allow only specific categories

Limit usage to well-defined expense types such as courier fees or minor office supplies. Prohibit anything related to travel, vendors or recurring operational costs.

3. Require immediate receipt collection

Missing receipts create VAT issues and weaken internal control. Every transaction must have documentation attached on the same day.

4. Conduct periodic surprise counts

Unannounced reconciliations ensure the custodian maintains accurate controls and discourage inappropriate withdrawals.

5. Enforce a clear replenishment threshold

Do not wait until the drawer is empty. Replenish when the balance drops below an agreed level to maintain consistency and reduce large, periodic reviews.

Conclusion

Petty cash once played a crucial role in day-to-day operations. Today, it is more of a transitional tool, still necessary for a few situations but far less efficient, transparent, or compliant than digital alternatives. Finance teams can manage petty cash effectively through strict controls, documentation discipline, and regular reconciliation, but the long-term goal for most organisations is to reduce or eliminate petty cash altogether.

Modern finance functions prioritise real-time visibility, traceability, policy enforcement, and audit readiness. These are difficult to achieve with physical cash funds, fragmented receipts, and manual logs. By shifting toward controlled card-based spending and automated expense systems, companies strengthen governance, reduce error,s and free teams from repetitive reconciliation work.

At Alaan, we help companies move beyond petty cash by providing controlled corporate cards, receipt automation, spend limits, and real-time visibility across every transaction.

If you want better governance, audit-ready records, and a complete alternative to petty cash, book a demo to see how Alaan can modernise your organisation’s spending workflows.

Frequently Asked Questions (FAQs)

1. What types of payments should petty cash be used for?

Only small, one-off expenses such as minor office supplies, courier charges, or incidental transport fees. Anything recurring, vendor-related, or requiring VAT invoices should not be paid through petty cash.

2. What is the ideal petty cash amount for an office?

Most organisations maintain a small float that covers 2–4 weeks of minor expenses. The amount should be low enough to reduce risk but high enough to avoid frequent replenishment.

3. What are the most common petty cash problems?

Missing receipts, undocumented withdrawals, personal expenses, incorrect categorisation, cash shortages, and delayed reconciliations.

4. How often should petty cash be reconciled?

Depending on activity: weekly for active offices, monthly for very low-volume funds. Surprise counts add an additional layer of control.

5. Is petty cash still recommended for modern finance teams?

Not ideally. Card-based controls and automated expense systems offer better visibility, VAT support, and fraud prevention. Petty cash should be used only when no digital alternative exists.

6. How does Alaan help eliminate petty cash?

Alaan provides controlled corporate cards, spend limits, real-time transaction data, instant receipt capture, and ERP integration, removing the need for physical cash and manual reconciliation entirely.

%201.avif)