Accounting teams across the UAE are under growing pressure to meet complex compliance demands, manage VAT filings, and deliver timely reports. Yet, manual processes such as data entry and reconciliation still dominate many finance functions, resulting in delays and costly errors. AI-driven automation is emerging as a proven solution, reducing invoice errors by up to 85% and increasing operational efficiency by as much as 50%.

AI is no longer a futuristic concept for finance teams. From automating journal entries to generating real-time dashboards, AI tools are helping UAE-based firms streamline operations and shift toward more strategic, data-backed decision-making. These tools are transforming back-office workflows while freeing up teams to focus on value-added activities.

This blog examines the top AI accounting tools and trends shaping 2025, specifically tailored to the needs of UAE businesses. You'll learn practical use cases, adoption strategies, and how platforms like Alaan are helping finance teams stay compliant, agile, and future-ready.

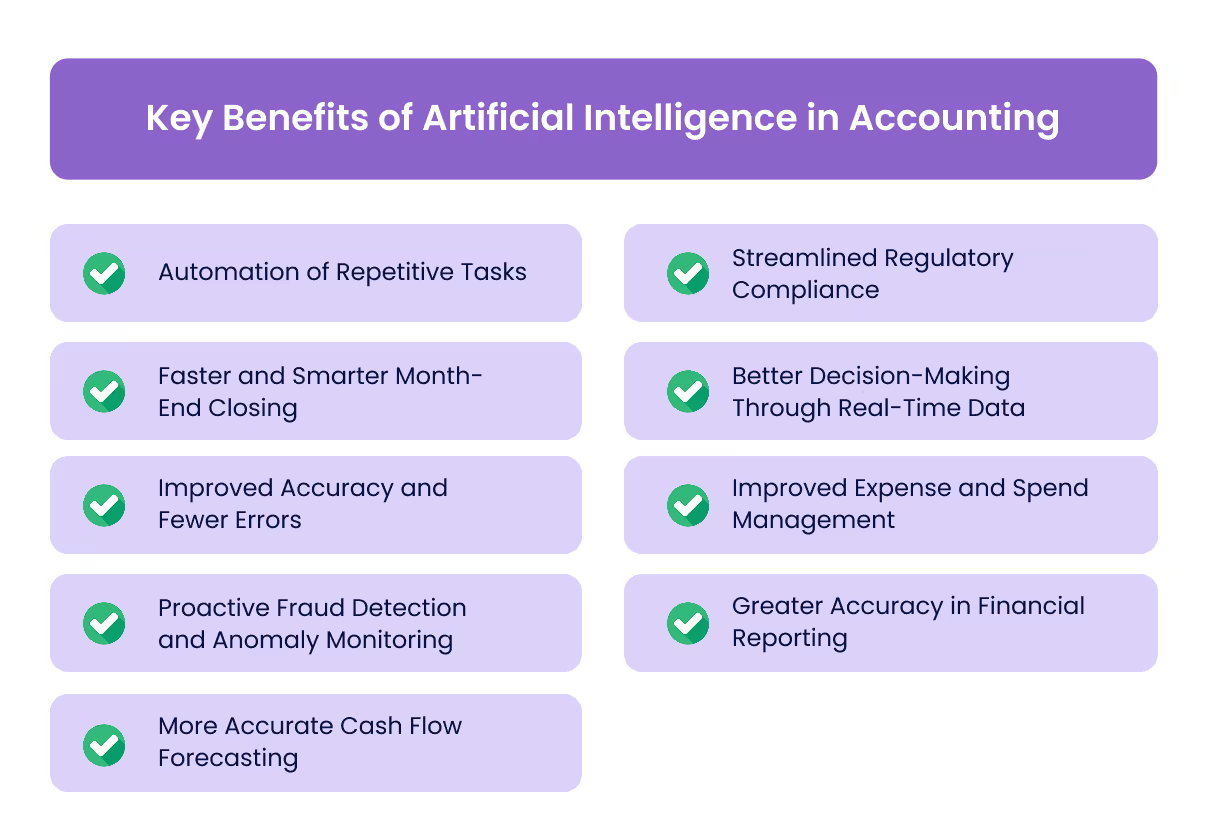

Key Benefits of Artificial Intelligence in Accounting

UAE businesses are under increasing pressure to maintain real-time financial visibility while remaining compliant with tax regulations like VAT, corporate tax, and ESR. Manual accounting processes simply cannot keep pace. Artificial intelligence offers a powerful solution by automating core tasks and turning raw data into strategic insight.

Below are the most valuable benefits of AI in accounting for UAE-based finance teams:

- Automation of Repetitive Tasks

AI streamlines high-volume, manual processes, allowing teams to focus on strategy rather than data entry.

- Automates invoice processing and approval workflows.

- Matches purchase orders to invoices automatically.

- Classifies and codes expenses with minimal human input.

This is particularly valuable for UAE SMEs that handle hundreds of supplier invoices every month and need to ensure accuracy for VAT reclaim.

- Faster and Smarter Month-End Closing

Manual reconciliations and ledger updates often delay the financial close. AI accelerates these processes and increases accuracy at every stage.

- Automatically matches transactions across bank feeds and ledgers in real-time.

- Identifies discrepancies and flags them instantly for resolution.

- Reduces close cycles from weeks to days.

For UAE firms managing multi-entity operations or cross-border transactions, a faster month-end means timely reporting for stakeholders and compliance authorities.

- Improved Accuracy and Fewer Errors

AI reduces human error by using pattern recognition and rule-based validation for financial data.

- Ensures accurate data entry for VAT and compliance reports to ensure timely and accurate reporting.

- Flag anomalies or duplicate transactions automatically.

- Reduces audit risks linked to manual reconciliation.

In a region where financial reporting must align with FTA and MoF regulations, improved accuracy can prevent costly penalties.

- Proactive Fraud Detection and Anomaly Monitoring

AI tools can detect suspicious patterns in vast datasets before they trigger damage. This is crucial in high-compliance jurisdictions like the UAE.

- Flags duplicate payments, unauthorised expense claims, or vendor fraud.

- Learns from previous anomalies to improve future detection.

- Supports internal audits by maintaining digital logs of flagged entries.

Finance heads in the UAE can utilise AI to mitigate fraud exposure and prepare for annual external audits with greater confidence.

- More Accurate Cash Flow Forecasting

Forecasting future liquidity is a crucial function, particularly in industries such as retail, construction, and logistics that are highly cash-sensitive.

- AI analyses historical inflow and outflow trends to build forecasts.

- Accounts for seasonality, vendor payment cycles, and tax deadlines.

- Provides scenario modelling to plan for best- and worst-case conditions.

In the UAE, where working capital planning is crucial for sustaining trade credit and supplier relationships, AI-based forecasting improves agility.

- Streamlined Regulatory Compliance

The UAE’s evolving tax environment demands consistent reporting and up-to-date documentation. AI eases the compliance burden across multiple regulatory frameworks.

- Aligns transaction codes with FTA’s VAT and corporate tax requirements.

- Auto-generates ESR-aligned reporting templates and flags missing data.

- Maintains audit trails to support regulatory inspections.

Using AI for compliance saves time during VAT filing periods and ensures financial reports are audit-ready.

- Better Decision-Making Through Real-Time Data

CFOs and finance leaders often rely on outdated spreadsheets for decision-making. AI transforms that by offering live, digestible insights.

- Integrates data from multiple accounting and ERP systems.

- Creates interactive dashboards for real-time reporting.

- Uses NLP-based tools (like ChatGPT) to summarise financial results.

This enables UAE businesses, particularly those expanding into the KSA or other GCC markets, to make informed decisions based on accurate financial data.

- Improved Expense and Spend Management

With AI, finance teams can track, analyse, and optimise company spending more effectively than ever before.

- Flags overspending by cost centre, category, or project.

- Categorises expenses in real-time for budget alignment.

- Helps build detailed cost-control strategies using data trends.

Given the rising operating costs in the UAE, particularly in areas such as rent, staffing, and compliance, AI-based spend control enables firms to stay within budget and protect their margins.

- Greater Accuracy in Financial Reporting

Errors in financial reports can lead to penalties or reputational damage. AI ensures that reports are clean, consistent, and compliant.

- Pulls data from integrated systems to reduce manual copy-paste errors.

- Identifies data inconsistencies before they’re published.

- Assists with automated formatting and visualisation of financial statements.

For UAE companies that file audited financial statements annually, AI offers peace of mind and saves significant review time.

These benefits demonstrate why AI in accounting is no longer optional. From compliance to forecasting, AI tools offer finance teams in the UAE a smarter way to manage operations, mitigate risk, and make informed strategic decisions. As adoption grows, early movers will gain a clear edge in accuracy, agility, and long-term profitability.

Also Read: Understanding the Role of Ledgers in Accounting

[cta-10]

Will AI Replace Accountants?

With AI becoming increasingly powerful in accounting software, many UAE finance professionals are asking a difficult question: Will artificial intelligence eventually replace human accountants? The answer, backed by global trends and practical realities, is a clear no.

In fact, AI is transforming accounting into a more strategic and collaborative function, rather than eliminating the need for professionals.

- AI Handles Tasks, Not Strategic Thinking

AI excels at automating routine tasks such as data entry, reconciliation, and transaction matching. However, it cannot interpret complex financial contexts or apply judgment to business decisions.

In the UAE, where tax laws are evolving and sector-specific regulations are often changing, only experienced professionals can navigate the nuances and exceptions that AI cannot address.

- Human Judgment Remains Irreplaceable

AI may generate data-driven insights, but it cannot replace the ethical reasoning, risk analysis, or strategic foresight that accountants bring. UAE accountants often work within local frameworks like VAT, ESR, and corporate tax to plan budgets, forecast performance, and guide investments.

These high-stakes decisions require critical thinking and contextual awareness that no algorithm can replicate.

- Client Relationships and Advisory Services Are Human-Driven

Accountants in the UAE are not just financial technicians; they’re trusted advisors. They understand client needs, industry challenges, and cultural expectations in ways AI cannot. While AI can present clean data, it cannot build trust, adapt recommendations to individual business goals, or provide nuanced financial advice tailored to each business's specific needs. Those responsibilities remain deeply human.

- AI Improves Roles, It Doesn’t Replace Them

Rather than replacing jobs, AI is reshaping them. Accountants are shifting into roles that emphasise analysis, insight, and strategic decision-making. Automation reduces the time spent on repetitive tasks, allowing smaller teams to manage more work without compromising accuracy. For UAE businesses that are scaling rapidly or diversifying their operations, this evolution is essential.

AI is not here to replace accountants; it’s here to empower them. As firms across the UAE adopt AI tools, the most successful accountants will be those who use technology to deliver faster insights, make better decisions, and foster stronger client relationships. The future of accounting is collaborative: AI handles the numbers, accountants handle the strategy.

Key AI Trends Shaping Accounting in the UAE for 2025

Artificial Intelligence is reshaping accounting practices in the UAE, accelerating financial operations, improving accuracy, and enabling forward-looking insights. In 2025, the following key AI trends will shape how UAE-based accountants and finance professionals adapt to the evolving expectations of modern clients and regulators:

- AI-Powered Data Structuring and Analysis

AI is increasingly used to convert unstructured financial data into clean, usable formats for real-time decision-making and analysis. UAE firms are adopting tools that process large volumes of bank statements, invoices, and transactional records in seconds.

Key applications include:

- Instant extraction of key financial data from scanned documents.

- Conversion of raw inputs into structured CSV reports for accounting software.

- Time-saving workflows in monthly reconciliations and reporting.

Automating financial data handling reduces manual workload and improves the turnaround time for reporting in UAE-based businesses.

- Predictive Analytics for Proactive Financial Planning

UAE businesses are investing in AI tools that analyse historical patterns and project future outcomes, helping finance teams shift from reactive reporting to strategic advisory roles.

Current uses include:

- Forecasting cash flow based on seasonal sales or recurring payment trends.

- Risk detection involves spotting early signs of financial anomalies.

- Guiding budget allocation based on predicted performance.

Predictive capabilities are allowing accountants in the UAE to advise clients with confidence and precision, backed by data.

- Integrated AI Within Practice Management Platforms

Rather than using separate AI tools, UAE accounting firms are embedding AI directly into their existing systems. This allows contextual insights based on client history and financial records.

Benefits observed include:

- Faster client onboarding with AI-supported document reviews.

- Real-time collaboration through AI-generated insights within client portals.

- Task automation (e.g., reminders, approvals) without leaving core platforms.

Seamless AI integration is enabling accountants to maintain productivity and deliver value without interrupting daily operations.

- AI-Enabled Forensic Accounting and Compliance

With rising scrutiny on tax compliance and financial transparency, UAE companies are turning to AI for forensic audits and regulatory reporting.

Core capabilities now include:

- Flagging suspicious transactions through pattern recognition.

- Automating VAT validation and Corporate Tax categorisation.

- Generating audit-ready reports with traceable logs.

AI is helping UAE accountants meet stringent regulatory standards while safeguarding against fraud and error.

- Intelligent Automation and Hyperautomation in Finance Workflows

Beyond simple task automation, UAE companies are adopting intelligent automation technologies that combine AI, robotic process automation (RPA), and analytics to streamline complex accounting workflows.

Highlights include:

- Orchestrating multi-step financial operations end-to-end.

- Continuous optimisation using data-driven insights.

- Reducing manual intervention for faster close cycles.

Hyperautomation is transforming finance departments into highly efficient and adaptable teams, ready to support dynamic business needs.

The UAE accounting sector in 2025 continues to embrace AI as a collaborative tool that boosts accuracy and efficiency. As AI expands into areas like sustainability reporting and advanced automation, accounting professionals gain new strategic opportunities. Staying ahead in AI adoption is critical for future-ready finance teams across the Emirates.

Also Read: UAE’s Corporate Tax: A primer on navigating the new regulations

Popular AI Tools That Are Transforming Accounting in the UAE?

As UAE businesses shift towards digital-first operations, accounting teams are embracing AI tools to manage tasks more efficiently and reduce manual effort. Here are some of the most impactful AI tools that accountants in the UAE should consider:

- Alaan – AI-Powered Expense Management for UAE Businesses

Alaan is a UAE-native spend management platform that uses AI to streamline business expenses, corporate card usage, and real-time budget controls. It helps finance teams gain control over operational spending while maintaining compliance with VAT and corporate tax rules.

What Alaan offers:

- Instantly issues smart corporate cards with custom limits, vendor locks, and automated approval flows.

- Tracks expenses in real time, matching receipts to transactions and flagging duplicates or errors.

- Syncs directly with platforms like Xero, QuickBooks, and Microsoft Dynamics for seamless reconciliation.

- Uses AI to extract VAT data from receipts, validate tax invoices, and maintain FTA-aligned audit trails.

- Provides smart dashboards that show spend insights by department, project, or campaign.

- Includes advanced controls like card freezing and insurance against unauthorised usage.

Why it's a fit for UAE firms: Alaan is designed specifically for local tax regulations and multi-currency spending needs. It’s especially valuable for e-commerce firms, SMEs, and multi-entity businesses that want end-to-end visibility into spend without relying on outdated manual processes.

- Karbon AI – Smarter Email and Task Management

Karbon AI is built into Karbon’s accounting practice management platform. It helps accounting teams manage email and task workflows more intelligently.

What Karbon AI can do:

- Summarise long email threads and internal conversations.

- Draft emails based on short prompts.

- Send personalised client updates based on job progress.

- Adjust tone in outgoing communication.

Why it matters for UAE firms: Karbon AI helps accountants save an average of 18.5 hours per week by improving communication clarity and task efficiency.

- Vic.ai – Invoice Automation and Spend Insights

Vic.ai is designed for mid-to-large firms with high invoice volumes. It automates invoice processing and flags policy violations.

Key capabilities:

- Automates invoice data extraction and approval workflows.

- Detects anomalies and ensures compliance with company policy.

- Provides financial reporting insights for better decisions.

- Maintains audit-ready documentation.

For UAE businesses: Vic.ai is ideal for firms focused on compliance and scalability. However, its high setup cost may be a barrier for smaller firms.

- Docyt – Bookkeeping and Reconciliation Automation

Docyt uses AI to simplify general ledger (G/L) tasks and automate revenue reconciliation.

Features include:

- Bookkeeping automation, including bill payments and transaction categorisation.

- Financial report generation based on stored data.

- Document extraction and contextual chat summaries.

- Centralised reconciliation matched to bank feeds.

Why it's relevant in the UAE: Docyt suits SMEs that want robust automation without investing in large ERP platforms.

- Blue Dot – AI for Tax Compliance

Blue Dot offers AI-powered insights on employee spending, VAT management, and taxable benefits.

It helps you:

- Detect eligible VAT refunds and benefits.

- Analyse employee spending trends.

- Ensure compliance across regional tax rules.

- Review vendors based on transactions and performance.

Useful for UAE firms: Especially relevant for multinational companies and those managing cross-border VAT refunds.

- Botkeeper – Automated Bookkeeping with Human Oversight

Botkeeper combines AI with human accountants to offer smart, hands-off bookkeeping.

Capabilities include:

- Data extraction, payroll, invoicing, and reconciliation.

- AI-driven reporting dashboards.

- Real-time support from a human team.

Value for UAE firms: Scales with accounting firms as they grow their client base, reducing dependency on manual processes.

- Rows AI – Smart Data Analysis in Spreadsheets

Rows AI is a spreadsheet tool that adds AI-powered analytics and text processing features.

Use cases:

- Summarise or clean up financial datasets.

- Classify transactions automatically.

- Enrich spreadsheet content with public or AI-generated data.

Relevance in the UAE: Helpful for finance teams who still rely on Excel and want to augment it with smart automation.

- Receipt-AI – Fast, Accurate Receipt Management

Receipt-AI extracts key data from receipts and integrates with accounting software like Xero or QuickBooks.

What it offers:

- Receipt capture via SMS or email.

- Automatic categorisation and GL integration.

- Support for bulk uploads.

Fit for UAE accountants: Ideal for small businesses looking to reduce time spent managing expense receipts.

From email automation to invoice processing and VAT compliance, AI tools are helping UAE accountants reduce manual workloads and focus on strategic tasks. Choosing the right tool depends on your firm’s size, needs, and budget. As AI adoption continues to grow in the region, firms that invest early in automation will be better positioned to scale efficiently and stay compliant.

Also Read: How to pick the right accounting software as a CFO

[cta-9]

Conclusion

AI tools are no longer a futuristic concept, but a present-day necessity. In the UAE, where businesses are under increasing pressure to remain agile and audit-ready, AI-driven accounting software offers a significant advantage. From automating bookkeeping and reconciling transactions to analysing VAT spend and predicting financial trends, AI solutions are helping finance teams make faster, smarter, and more compliant decisions.

To stay ahead in this evolving environment, UAE businesses need more than just tools; they require a platform that combines AI, automation, and local relevance.

Alaan was designed specifically to meet these demands. With AI-powered expense management tailored for businesses in the UAE, Alaan simplifies financial operations while ensuring policy control, audit compliance, and real-time visibility.

Explore Alaan’s AI-first platform for finance teams in the UAE today. Book a demo or get started now to see the difference.

FAQs

Q. Can UAE businesses integrate AI tools with local accounting regulations, such as VAT?

A. Yes. Several AI tools, such as Blue Dot, are designed to navigate country-specific VAT rules. However, pairing them with a UAE-localised solution, such as Alaan, ensures better alignment with the Federal Tax Authority (FTA) requirements.

Q. How can AI help with internal fraud prevention in accounting?

A. AI tools such as Vic.ai and Docyt offer anomaly detection and transaction tracking. These features help flag unusual activity, which can be critical for identifying potential internal fraud or policy violations.

Q. What should small businesses in the UAE prioritise when choosing an AI accounting tool?

A. Start with tools that offer automation for high-frequency tasks like expense tracking, invoicing, and bank reconciliation. Ensure they provide Arabic language support, regional compliance, and integration with popular platforms like Zoho Books or QuickBooks.

Q. Are there any AI tools suitable for multilingual finance teams?

A. Yes. Tools like Karbon AI and Botkeeper offer customisable, team-wide collaboration features. However, it's essential to check if these platforms support Arabic or bilingual communication for UAE-based teams.

Q. Is data security a risk with AI accounting tools in the UAE?

A. Data security is a key concern. Choose tools that are hosted on secure cloud infrastructure with GDPR or ISO certifications. Alaan, for instance, ensures enterprise-grade security and compliance for all financial data.