Accruals and prepayments are where otherwise well-run finance teams still lose time during month-end and year-end close. Not because the concepts are unclear, but because timing differences between cash, invoices, and actual consumption are rarely clean in real operations. Services span periods, invoices arrive late, and payments are often made in advance to secure pricing or contracts.

In the UAE, the consequences of getting this wrong are amplified. Research on corporate financial reporting in the UAE has found that published financial statements meet only around 61% of users’ informational needs, with concerns around credibility and timeliness cited as key gaps. Timing adjustments, such as accruals and prepayments, play a direct role in closing that gap by ensuring reported numbers reflect economic reality rather than cash movement alone.

When accruals are misstated, profits are inflated or suppressed. When prepayments are forgotten, assets linger on the balance sheet long after the benefit has been consumed. These issues rarely surface immediately; they typically emerge later as audit adjustments, review comments, or unexplained variances during close.

Accounting for accruals and prepayments is therefore not just a technical exercise. It is a control mechanism that underpins reporting accuracy, audit confidence, and disciplined financial management. Finance teams that handle these adjustments consistently close faster, defend their numbers with confidence, and reduce last-minute corrections that erode trust in the reported results.

In this blog, we look at how accruals and prepayments influence reporting accuracy and share practical guidance to help finance teams reduce close-time errors.

TL;DR

- Accruals and prepayments are control tools, not bookkeeping formalities. They determine whether financials reflect real activity or just cash movement.

- Most reporting errors come from process gaps, rolled balances, missed reversals, and weak ownership, rather than incorrect accounting logic.

- Accruals should behave like temporary bridges, while prepayments should unwind predictably over time. When they don’t, it signals breakdowns in close discipline.

- Consistent schedules, documentation, and monthly reviews reduce audit adjustments more effectively than complex accounting policies.

- Clean, timely transaction data upstream makes period-end adjustments simpler, faster, and easier to defend during audits.

What Accruals And Prepayments Actually Mean In Practice

Before looking at journal entries, it is important to separate theory from how accruals and prepayments behave in day-to-day accounting. Both exist to correct timing mismatches, but they solve different problems.

Accruals Explained

An accrual recognises an expense or income that belongs to the current period, even though no invoice has been received or cash has not yet moved. The economic activity has already occurred. The accounting entry simply acknowledges that reality.

Accrued expenses are the most common form of accrual. These arise when a business has received a service or incurred a cost but has not yet been billed. Typical examples include utilities, professional fees, interest, and salaries earned but unpaid at period end. In these cases, the obligation already exists, so the expense must be recognised along with a corresponding liability.

Accrued income works in the opposite direction. Revenue is recognised because services have been delivered or milestones met, even though billing or cash collection will happen later. Here, the accrual creates an asset rather than a liability.

The defining feature of an accrual is this: the profit or cost belongs to the period that just ended, regardless of when cash or invoices arrive.

Prepayments Explained

Prepayments address the opposite timing issue. They arise when cash moves before the related expense or income should be recognised.

A prepaid expense occurs when a business pays upfront for goods or services that will be consumed over future periods. Common examples include rent paid in advance, annual insurance premiums, software subscriptions, and maintenance contracts. At the time of payment, no expense has yet been incurred. The payment represents a future economic benefit and is therefore recorded as an asset.

Unearned revenue, sometimes called deferred revenue, follows the same logic from the seller’s perspective. Cash is received before services are delivered. Until performance occurs, the amount received represents an obligation rather than earned income.

The defining feature of a prepayment is this: cash has moved, but the expense or income does not yet belong to the current period.

Also Read: Understanding Prepaid Expenses on a Balance Sheet: Definition, Journal Entries, and Examples

Accruals Vs Prepayments: The Accounting Logic

Accruals and prepayments are often taught together, but in practice, they solve two different timing problems. One corrects for costs or income that have already occurred without cash movement. The other defers recognition when cash has moved too early. Understanding this distinction is what prevents misclassification at period end.

At a high level, accruals pull expenses or income into the current period. Prepayments push recognition out to future periods. Both adjustments ensure that profit reflects activity rather than payment timing.

Key Differences Between Accruals And Prepayments

Accruals usually result in temporary balances that reverse once invoices are received or payments are made. Prepayments, on the other hand, require systematic release over time. This difference is important during reconciliations. Accrual balances should not remain static for long periods. Prepayments should reduce consistently as benefits are consumed.

From a control perspective, accruals test whether finance teams understand what has already happened operationally. Prepayments test whether teams are disciplined in spreading costs and income across the correct periods.

Also Read: Difference Between Accrual and Cash Basis Accounting

Accounting For Accruals: Journal Entries And Treatment

Accruals exist to recognise economic reality before paperwork catches up. For finance teams, the challenge is not understanding the concept but applying it consistently without overstatement or omission. Poor accrual discipline is one of the most common reasons for late close adjustments and audit queries.

This section focuses on how accruals should be recorded, reviewed, and cleared in practice.

Accrued Expenses

Accrued expenses arise when a business has already received a service or incurred a cost, but the supplier invoice has not yet been received by the period end. The obligation exists, even though it is not yet documented formally.

Common examples include utilities consumed, professional services delivered, employee salaries earned, interest accrued, and maintenance services already performed.

From an accounting perspective, the expense must be recognised in the period it relates to, with a corresponding liability reflecting the unpaid amount.

Accrued Expense Journal Entry

At period end, the accrual is recorded as follows:

Dr Expense Account

Cr Accrued Expenses (Liability)

This entry ensures the cost appears in the correct period and that the balance sheet reflects the outstanding obligation.

When the supplier invoice is later received and paid, the accrual should be cleared, not expensed again. This avoids double-counting.

Dr Accrued Expenses

Cr Cash / Accounts Payable

Accrued expense balances should be reviewed regularly. If an accrual remains on the balance sheet for multiple periods without settlement, it often indicates either over-accrual or a breakdown in follow-up.

Accrued Income

Accrued income arises when revenue has been earned but has not yet been billed or collected. The service has been delivered, or a contractual milestone has been met, but cash receipt will occur later.

Examples include professional services completed at month's end, interest income earned but not yet credited, or long-term contracts with periodic billing.

In these cases, revenue belongs to the current period and must be recognised, along with an asset representing the right to receive payment.

Accrued Income Journal Entry

At period end, the entry is recorded as:

Dr Accrued Income (Asset)

Cr Revenue

When the invoice is issued, or payment is received in the subsequent period, the accrual is reversed:

Dr Cash / Accounts Receivable

Cr Accrued Income

As with accrued expenses, accrued income balances should not remain open indefinitely. Persistent balances often point to billing delays or revenue recognition issues rather than timing differences.

From a control standpoint, accruals should always be supported by clear documentation and a defined rationale. Estimates must be reasonable, consistent, and reviewed each period rather than rolled forward mechanically.

Also Read: Accrued Expenses: Definition, Types, and Differences

Accounting For Prepayments: Journal Entries And Treatment

Prepayments are about discipline over time. Unlike accruals, which are often cleared quickly once invoices arrive, prepayments require ongoing attention across multiple periods. Most errors here come not from incorrect initial booking, but from failing to release balances consistently.

This section focuses on how prepayments should be recognised and expensed in practice.

Prepaid Expenses

A prepaid expense arises when cash is paid before the related service or benefit is consumed. At the point of payment, no expense has yet been incurred. The payment represents a future economic benefit and is therefore recorded as an asset on the balance sheet.

Common prepaid expenses include rent paid in advance, insurance premiums, annual software subscriptions, maintenance contracts, and retainers.

Initial Recognition Of A Prepaid Expense

When the upfront payment is made, the journal entry is:

Dr Prepaid Expense (Asset)

Cr Cash / Bank

This entry records the cash outflow without affecting the income statement.

Periodic Expense Recognition

As the benefit is consumed over time, the prepaid balance is released to the income statement. This is typically done monthly on a straight-line basis unless the contract specifies otherwise.

Dr Expense Account

Cr Prepaid Expense

This ensures expenses are matched to the periods in which the benefit is received.

A common control failure is leaving prepaid balances untouched for months after the benefit has ended. Finance teams should review prepaid schedules regularly and close balances promptly once fully amortised.

Unearned Revenue (Deferred Revenue)

Unearned revenue arises when a business receives payment before delivering goods or services. Until performance obligations are met, the amount received represents a liability rather than income.

Examples include advance payments for service contracts, retainers, subscriptions, or long-term engagements billed upfront.

Initial Recognition Of Unearned Revenue

At the time cash is received:

Dr Cash / Bank

Cr Unearned Revenue (Liability)

This reflects the obligation to deliver services in the future.

Revenue Recognition Over Time

As services are provided or milestones are met, revenue is recognised proportionately:

Dr Unearned Revenue

Cr Revenue

This process continues until the full amount has been earned.

From a reporting perspective, unearned revenue balances should align closely with delivery schedules and contractual terms. Large or aging unearned revenue balances often signal delays in service delivery or mismatches between billing and performance.

Also Read: What is Deferral in Accounting: Differences, Revenue, Expenses and Definition

Accruals And Prepayments Journal Entries: Quick Reference

Accruals and prepayments rely on the same underlying principle, but the journal entries differ based on whether the timing mismatch relates to cash arriving too late or too early. Having a clear reference helps reduce posting errors during the month-end and year-end close.

The table below summarises the most common journal entries used when accounting for accruals and prepayments.

Journal Entry Summary

While these entries appear straightforward, most errors arise from poor timing discipline rather than incorrect debit and credit logic. Accruals should reverse promptly. Prepayments should unwind systematically.

As a control check, accrual balances should rarely stay open across multiple periods, while prepayments should steadily reduce according to the underlying contract.

Also Read: Understanding General Ledger in Double-Entry Accounting

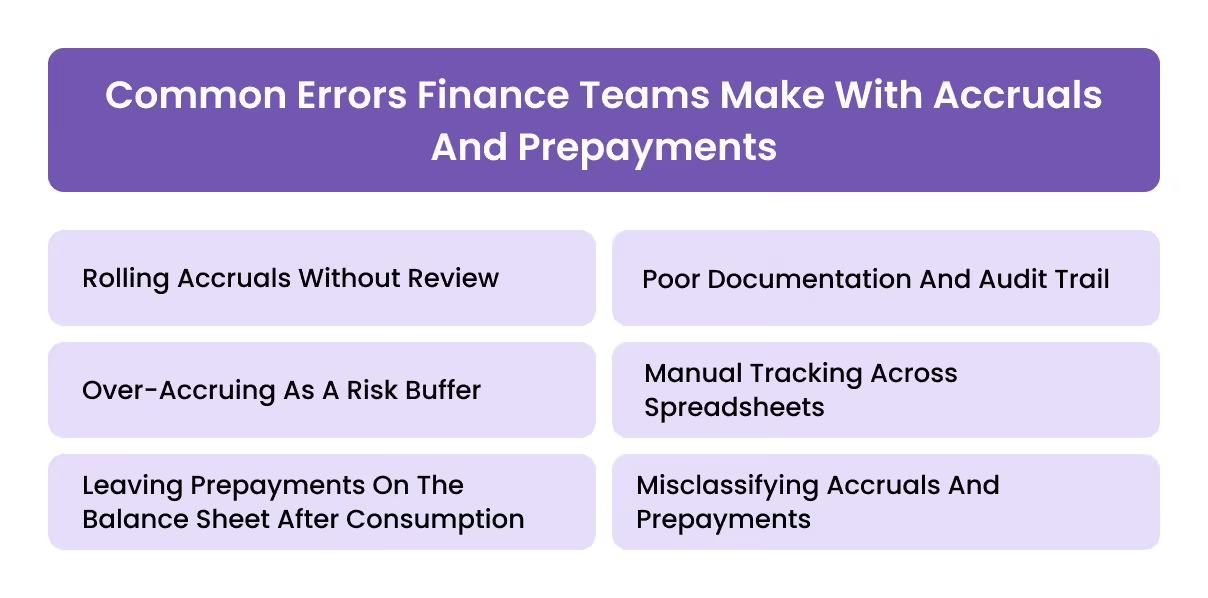

Common Errors Finance Teams Make With Accruals And Prepayments

Most accrual and prepayment issues do not come from a misunderstanding of accounting rules. They come from weak controls, rushed closings, and adjustments being carried forward without proper review. Over time, these small lapses compound and surface as audit findings or unexplained variances.

Below are the most common problem areas seen in practice.

1. Rolling Accruals Without Review

One of the most frequent errors is rolling accruals forward month after month without reassessing whether the obligation still exists. Accruals are estimates, not permanent balances. If they are not reversed or adjusted once invoices arrive, expenses can be overstated or duplicated.

2. Over-Accruing As A Risk Buffer

Some teams intentionally over-accrue to avoid understatements. While conservative intent is understandable, repeated over-accruals distort margins and weaken trust in management reporting. Accruals should be reasonable, evidence-based, and adjusted when new information becomes available.

3. Leaving Prepayments On The Balance Sheet After Consumption

Prepayments are often booked correctly at the start and then forgotten. When the service period ends, but the asset remains on the balance sheet, expenses are understated, and profits are overstated. This is especially common with annual subscriptions and insurance policies.

4. Poor Documentation And Audit Trail

Accruals supported only by rough estimates or verbal assumptions invite audit challenges. Without contracts, usage data, or calculation logic, finance teams struggle to justify balances during reviews or audits.

5. Manual Tracking Across Spreadsheets

Managing accruals and prepayments through disconnected spreadsheets increases the risk of omissions, formula errors, and inconsistent updates. As transaction volume grows, spreadsheet-based tracking becomes unsustainable.

6. Misclassifying Accruals And Prepayments

Confusing an accrual with a prepayment leads to incorrect balance sheet treatment. For example, recording an unpaid expense as a prepaid asset or expensing an advance payment immediately results in timing distortions that affect reported profit.

Addressing these issues requires discipline, documentation, and clear ownership rather than more complex accounting rules.

Also Read: 8 Important Steps in the Accounting Process

Best Practices For Managing Accruals And Prepayments At Close

Strong accrual and prepayment management is less about technical sophistication and more about consistency. Finance teams that close smoothly tend to follow simple, repeatable controls rather than relying on individual judgement at the last minute.

Below are practices that materially reduce errors and rework during close.

1. Maintain Structured Accrual And Prepayment Schedules

Accruals and prepayments should be tracked in dedicated schedules that are updated every period. Each balance should clearly show the nature of the item, calculation basis, expected reversal or amortisation timeline, and supporting documentation.

2. Tie Adjustments To Operational Data

Accruals should be linked to actual consumption or activity, not historical averages alone. Where possible, use usage reports, service delivery confirmations, payroll data, or contractual milestones to support estimates.

3. Reverse Accruals Promptly And Review Variances

Once invoices are received or payments are made, accruals should be reversed immediately. Any difference between the accrued amount and the actual invoice should be analysed and documented, rather than silently absorbed.

4. Review Prepayments Monthly, Not Annually

Prepaid balances should be reviewed at every close to ensure amortisation aligns with service periods. Waiting until year-end increases the risk of material misstatements and late corrections.

5. Assign Clear Ownership And Review Controls

Each accrual or prepayment category should have a defined owner responsible for calculation, review, and clearance. Independent review adds discipline and reduces reliance on assumptions.

6. Automate Where Transaction Volumes Are High

Recurring accruals and amortisation entries should be automated where possible. Automation reduces manual errors and ensures consistency, particularly in high-volume environments.

These practices shift accruals and prepayments from being reactive adjustments to controlled components of the close process.

Also Read: Guide to Preparing Financial Statements Efficiently

How Alaan Supports Better Accrual And Prepayment Management

Accruals and prepayments rely less on complex accounting rules and more on having clean, timely, and well-documented transaction data. While Alaan is not an accounting system, it plays a practical role in strengthening the inputs that finance teams depend on when recording and reviewing these adjustments.

Below are specific ways Alaan supports accrual and prepayment discipline in practice.

1. Real-Time Visibility Into Business Spend

Alaan provides real-time visibility into company spending across cards, reimbursements, and vendor payments. This helps finance teams identify expenses incurred but not yet invoiced, a common trigger for accruals during month-end close.

With up-to-date spend data, teams are less reliant on estimates or delayed reports when identifying accrued expenses.

2. Centralised Documentation For Audit Support

Accruals and prepayments are frequently challenged during audits due to missing or incomplete support. Alaan centralises receipts, invoices, and supporting documents alongside each transaction, making it easier to substantiate balances.

This reduces time spent chasing documentation during close and audit reviews and improves confidence in accrual calculations.

3. Clear Expense Timing And Period Attribution

By capturing transaction dates, merchant details, and spend categories at the point of payment, Alaan helps finance teams determine whether a cost belongs to the current period or should be treated as a prepayment.

This improves consistency in identifying prepaid expenses and ensures costs are allocated to the correct accounting period.

4. Faster Close Through Reduced Manual Follow-Ups

Manual follow-ups for missing receipts or unclear spend slow down accrual reviews and increase close pressure. Alaan’s structured expense workflows reduce back-and-forth by prompting employees to submit complete information upfront.

As a result, finance teams spend less time validating inputs and more time reviewing accrual and prepayment schedules.

5. Better Audit Readiness Without Adding Accounting Complexity

Auditors expect clear trails linking expenses to underlying transactions and documentation. Alaan helps maintain this trail by keeping spend data, approvals, and supporting records in one place.

This makes accruals and prepayments easier to explain and defend during audits, without adding complexity to the accounting process itself.

Conclusion

Accounting for accruals and prepayments is ultimately about discipline at the edges of the reporting period. These adjustments determine whether financial statements reflect economic reality or simply mirror cash movements. When handled poorly, they introduce noise into the close process, weaken audit confidence, and obscure true performance.

The goal for finance teams is not to make accruals and prepayments more complex, but to make them predictable. Clear schedules, documented assumptions, timely reversals, and regular reviews turn these adjustments into routine controls rather than recurring pain points. Over time, this improves close efficiency, reduces audit adjustments, and strengthens confidence in reported numbers.

Alaan supports this discipline by improving the quality of spend data that feeds into accrual and prepayment decisions. With real-time visibility, centralised documentation, and clearer transaction context, finance teams can manage period-end adjustments with greater confidence and less manual effort.

Want to see how better spend visibility can support a faster, cleaner close?

Book a free demo with Alaan to see how finance teams simplify expense control and improve audit readiness.

Frequently Asked Questions (FAQs)

1. How Do You Identify Accruals And Prepayments During Month-End Close?

Finance teams typically identify accruals and prepayments by reviewing expenses and income against service periods rather than payment dates. Common methods include scanning unbilled services, reviewing contracts that span multiple months, analysing prepaid vendor payments, and comparing current-period usage against invoices received. Items where timing does not align usually require accrual or deferral adjustments.

2. What Happens If Accruals Or Prepayments Are Missed In Financial Statements?

If accruals or prepayments are missed, expenses or income may be recognised in the wrong period, leading to misstated profits. This can result in misleading management reports, audit adjustments, compliance issues, and incorrect tax or VAT calculations. Over time, repeated omissions reduce confidence in financial reporting and increase audit scrutiny.

3. How Often Should Accruals And Prepayments Be Reviewed?

Accruals and prepayments should be reviewed at every reporting close, not just at year-end. Monthly reviews help ensure accruals are reversed on time, and prepayments are amortised correctly. In fast-growing or high-volume environments, more frequent reviews reduce the risk of balances becoming stale or misstated.

4. Are Accruals And Prepayments Required Under IFRS And GAAP?

Yes. Both IFRS and GAAP require accrual accounting, which includes recognising accruals and prepayments to ensure income and expenses are matched to the correct period. While specific presentation or disclosure requirements may vary, the underlying principle of timing alignment is mandatory under both standards.

5. How Do Accruals And Prepayments Impact VAT Or Indirect Taxes In The UAE?

In the UAE, accruals and prepayments can affect VAT timing and reporting, particularly where tax invoices are issued before or after service delivery. Incorrect treatment may lead to VAT being claimed or reported in the wrong period. Finance teams must ensure that accounting recognition aligns with VAT rules and supporting documentation.

6. What Documents Are Needed To Support Accruals And Prepayments During Audits?

Auditors typically expect contracts, service agreements, invoices, usage reports, payroll records, calculation workings, and approval evidence. Clear documentation explaining why an accrual or prepayment exists and how the amount was calculated significantly reduces audit challenges and follow-up queries.