Invoice discounting becomes relevant when sales are real but cash has not arrived yet. For businesses that sell on credit, the invoice may be approved, delivered, and recorded, while payroll, rent, inventory purchases, and supplier payments still need to be funded before the customer pays.

This timing gap is a live issue in the UAE. Atradius’ 2025 UAE payment practices report found that overdue invoices affect 58% of B2B sales, and some industries report payment terms of around 40 to 50 days from invoicing. For finance teams, that delay can turn receivables into a working capital constraint even when demand is strong.

Invoice discounting helps bridge this gap by allowing a business to access cash against unpaid invoices. But it should not be treated as free liquidity. The cost, recourse terms, customer quality, documentation requirements, and reporting treatment all determine whether it supports cash flow or simply hides a deeper collections problem.

In this blog, we will explain what invoice discounting means, how it works in practice, how it differs from factoring and bill discounting, and what finance teams should evaluate before using it to manage cash flow.

TL;DR / Key Takeaways

- Invoice discounting helps businesses access cash earlier by using unpaid customer invoices as the basis for financing.

- It improves short-term liquidity, but it does not automatically remove customer payment risk or fix weak collections.

- Finance teams must check advance rates, total fees, recourse terms, customer eligibility, documentation requirements, and repayment obligations.

- Discounted invoice proceeds should be tracked separately so cash flow reporting does not overstate operating performance.

- Invoice discounting works best when receivables are reliable, invoice records are clean, and cash visibility is strong.

What Invoice Discounting Means

Invoice discounting is a form of receivables finance where a business uses its unpaid invoices to access working capital before the customer pays. Instead of waiting for the full payment cycle to complete, the business receives a percentage of the invoice value upfront from a bank or financing provider.

The invoice itself becomes the basis for the financing decision. The financier evaluates the invoice, the customer’s creditworthiness, and the terms of the transaction before releasing funds.

From a practical standpoint, invoice discounting does not change the underlying sale. The customer still owes the full invoice amount. The difference is that the business improves its cash position by bringing forward part of that payment.

Also Read: Understanding Trade Receivables Key Concepts

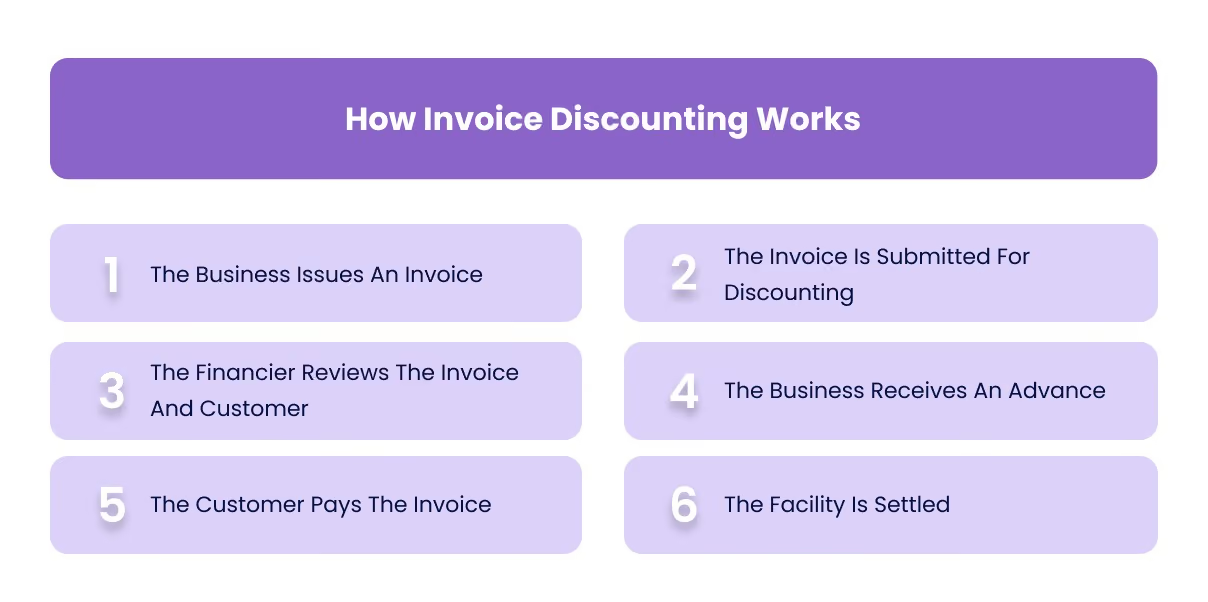

How Invoice Discounting Works

Invoice discounting follows a structured process. While the details vary depending on the provider, the underlying flow remains consistent.

1. The Business Issues An Invoice

The business completes a sale and raises an invoice with agreed payment terms. These terms often range from 30 to 90 days, depending on the industry and customer relationship.

2. The Invoice Is Submitted For Discounting

The business submits the invoice to a bank or financing provider as part of an invoice discounting facility.

3. The Financier Reviews The Invoice And Customer

The financier evaluates the invoice, checks supporting documents, and assesses the customer’s ability to pay. This step determines whether the invoice qualifies for financing and at what advance rate.

4. The Business Receives An Advance

Once approved, the business receives a portion of the invoice value upfront. This provides immediate liquidity to support operations.

5. The Customer Pays The Invoice

The customer pays the invoice according to the original payment terms. Depending on the structure, the payment may go to the business or directly to the financier.

6. The Facility Is Settled

After the invoice is paid, the financier recovers the advance along with applicable fees. The remaining balance, if any, is released to the business.

Invoice Discounting Example

A simple example helps illustrate how invoice discounting affects cash flow.

- Invoice Value: AED 100,000

- Advance Rate: 80 percent

- Cash Received Upfront: AED 80,000

The business receives AED 80,000 immediately instead of waiting for the full payment period. When the customer pays the full AED 100,000, the financier deducts its fees and settles the remaining amount with the business.

This improves short-term cash flow, but the total amount retained by the business is slightly reduced due to financing costs.

Invoice Discounting Vs Factoring

Invoice discounting is often compared with factoring, but the two structures differ in how control and responsibility are handled.