Invoice discounting becomes relevant when sales are real but cash has not arrived yet. For businesses that sell on credit, the invoice may be approved, delivered, and recorded, while payroll, rent, inventory purchases, and supplier payments still need to be funded before the customer pays.

This timing gap is a live issue in the UAE. Atradius’ 2025 UAE payment practices report found that overdue invoices affect 58% of B2B sales, and some industries report payment terms of around 40 to 50 days from invoicing. For finance teams, that delay can turn receivables into a working capital constraint even when demand is strong.

Invoice discounting helps bridge this gap by allowing a business to access cash against unpaid invoices. But it should not be treated as free liquidity. The cost, recourse terms, customer quality, documentation requirements, and reporting treatment all determine whether it supports cash flow or simply hides a deeper collections problem.

In this blog, we will explain what invoice discounting means, how it works in practice, how it differs from factoring and bill discounting, and what finance teams should evaluate before using it to manage cash flow.

TL;DR / Key Takeaways

- Invoice discounting helps businesses access cash earlier by using unpaid customer invoices as the basis for financing.

- It improves short-term liquidity, but it does not automatically remove customer payment risk or fix weak collections.

- Finance teams must check advance rates, total fees, recourse terms, customer eligibility, documentation requirements, and repayment obligations.

- Discounted invoice proceeds should be tracked separately so cash flow reporting does not overstate operating performance.

- Invoice discounting works best when receivables are reliable, invoice records are clean, and cash visibility is strong.

What Invoice Discounting Means

Invoice discounting is a form of receivables finance where a business uses its unpaid invoices to access working capital before the customer pays. Instead of waiting for the full payment cycle to complete, the business receives a percentage of the invoice value upfront from a bank or financing provider.

The invoice itself becomes the basis for the financing decision. The financier evaluates the invoice, the customer’s creditworthiness, and the terms of the transaction before releasing funds.

From a practical standpoint, invoice discounting does not change the underlying sale. The customer still owes the full invoice amount. The difference is that the business improves its cash position by bringing forward part of that payment.

Also Read: Understanding Trade Receivables Key Concepts

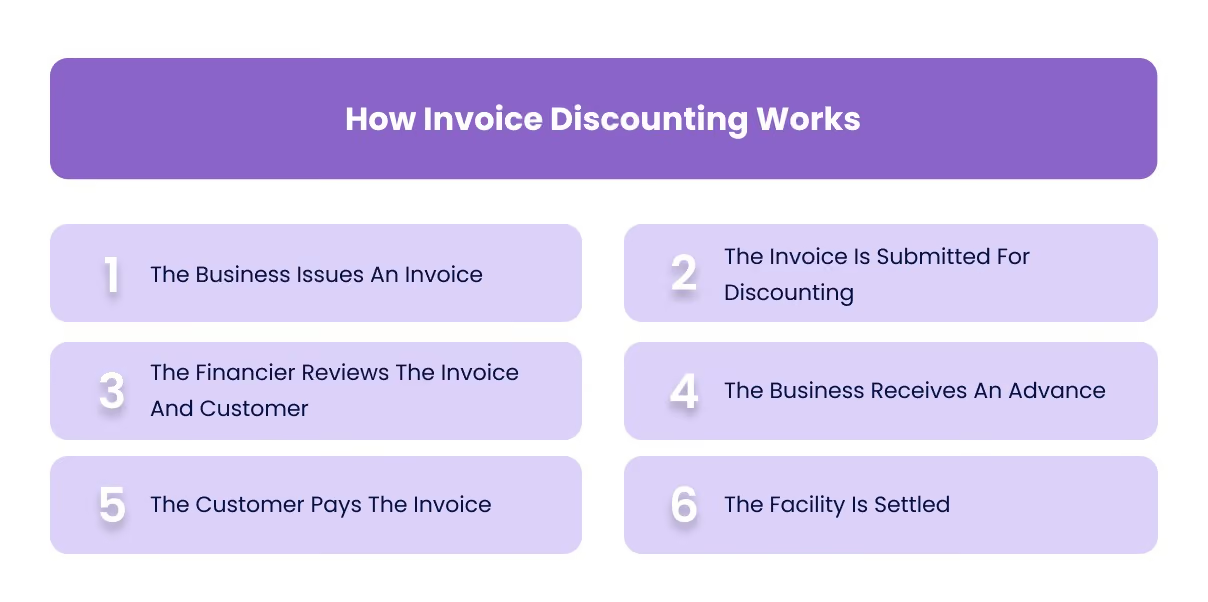

How Invoice Discounting Works

Invoice discounting follows a structured process. While the details vary depending on the provider, the underlying flow remains consistent.

1. The Business Issues An Invoice

The business completes a sale and raises an invoice with agreed payment terms. These terms often range from 30 to 90 days, depending on the industry and customer relationship.

2. The Invoice Is Submitted For Discounting

The business submits the invoice to a bank or financing provider as part of an invoice discounting facility.

3. The Financier Reviews The Invoice And Customer

The financier evaluates the invoice, checks supporting documents, and assesses the customer’s ability to pay. This step determines whether the invoice qualifies for financing and at what advance rate.

4. The Business Receives An Advance

Once approved, the business receives a portion of the invoice value upfront. This provides immediate liquidity to support operations.

5. The Customer Pays The Invoice

The customer pays the invoice according to the original payment terms. Depending on the structure, the payment may go to the business or directly to the financier.

6. The Facility Is Settled

After the invoice is paid, the financier recovers the advance along with applicable fees. The remaining balance, if any, is released to the business.

Invoice Discounting Example

A simple example helps illustrate how invoice discounting affects cash flow.

- Invoice Value: AED 100,000

- Advance Rate: 80 percent

- Cash Received Upfront: AED 80,000

The business receives AED 80,000 immediately instead of waiting for the full payment period. When the customer pays the full AED 100,000, the financier deducts its fees and settles the remaining amount with the business.

This improves short-term cash flow, but the total amount retained by the business is slightly reduced due to financing costs.

Invoice Discounting Vs Factoring

Invoice discounting is often compared with factoring, but the two structures differ in how control and responsibility are handled.

The key distinction is control. Invoice discounting allows businesses to maintain their customer relationships and collection processes, while factoring shifts more responsibility to the financing provider.

OECD’s SME finance methodology notes that factoring turnover can include invoice discounting, recourse factoring, non-recourse factoring, collections, export factoring, import factoring, and export invoice discounting, which is why finance teams should confirm the exact structure of the facility rather than relying only on the product label.

Related: Calculate And Track Bad Debts Expense

Invoice Discounting Vs Bill Discounting

The terms invoice discounting and bill discounting are often used interchangeably, but they can differ slightly depending on the market, bank, or financing structure.

Invoice discounting is typically based on commercial invoices raised against customers under open account terms. The business submits these invoices to a financier to access early payment.

Bill discounting, on the other hand, is often linked to trade instruments such as bills of exchange or formally accepted payment documents. These are more common in structured trade finance transactions where the payment obligation is documented and sometimes accepted by the buyer.

In practice, the distinction matters less than the structure of the facility. Finance teams should focus on:

- What document is being financed

- Who is responsible for repayment

- Whether the buyer has formally accepted the payment obligation

- How the financing is recorded and settled

Understanding these details is more useful than relying on terminology alone.

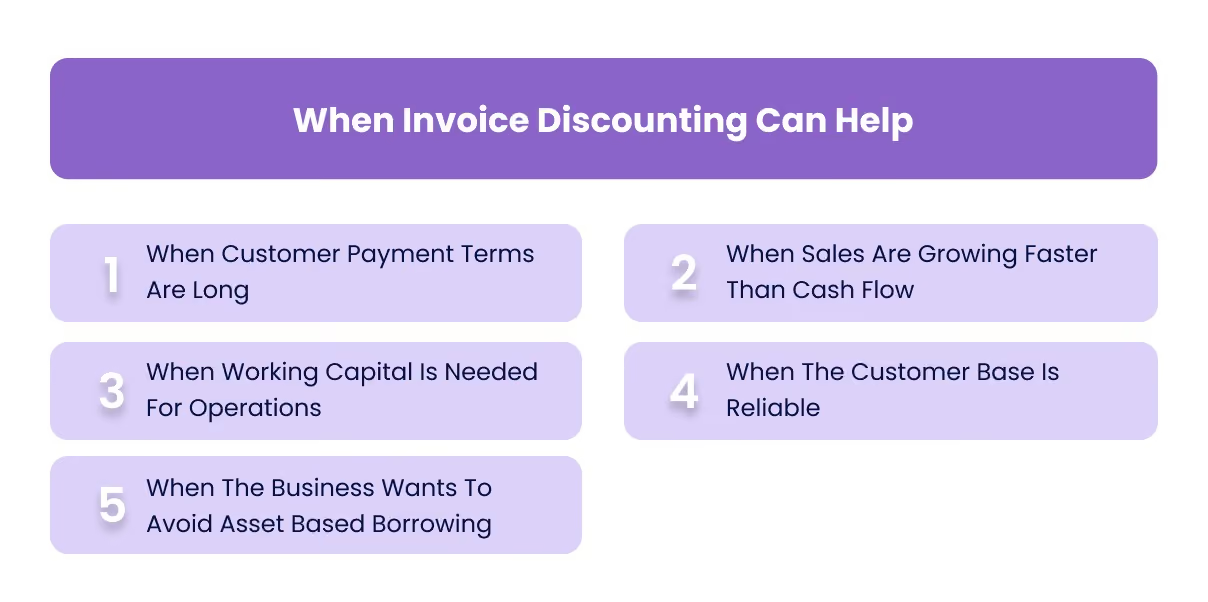

When Invoice Discounting Can Help

Invoice discounting is most effective when it is used to address timing gaps in cash flow rather than as a substitute for strong financial discipline.

1. When Customer Payment Terms Are Long

Businesses operating on 30, 60, or 90-day payment cycles often experience delays between revenue recognition and cash receipt. Invoice discounting helps bridge this gap.

2. When Sales Are Growing Faster Than Cash Flow

Rapid growth can increase receivables faster than cash inflows. Even profitable businesses can face liquidity pressure if collections lag behind sales.

3. When Working Capital Is Needed For Operations

Access to early cash can support payroll, supplier payments, inventory purchases, and other operational expenses without waiting for customer payments.

4. When The Customer Base Is Reliable

Invoice discounting works best when customers have a strong payment track record. The quality of receivables directly affects approval and cost.

5. When The Business Wants To Avoid Asset Based Borrowing

Instead of pledging physical assets, the business uses receivables as the basis for financing.

Related: Cash Flow Operating Activities Guide

Risks And Costs Of Invoice Discounting

While invoice discounting improves liquidity, it introduces financial and operational considerations that need to be understood clearly before use.

1. Financing Costs Reduce Net Cash Received

The business receives cash earlier but pays a discount fee or financing charge. Over time, this reduces overall margins if used frequently.

2. Customer Non Payment May Still Be A Risk

In many structures, the business remains responsible if the customer fails to pay. This is especially relevant in recourse arrangements.

3. Poor Documentation Can Delay Or Block Access

Incomplete invoices, missing delivery confirmations, or unclear customer details can slow down approval or lead to rejection.

4. Over Reliance Can Mask Weak Collections

Invoice discounting can temporarily improve cash flow, but it does not fix underlying issues such as delayed collections or poor credit control.

5. It Can Affect Customer Perception

Depending on how the facility is structured, customers may become aware that invoices are being financed, which can influence relationships.

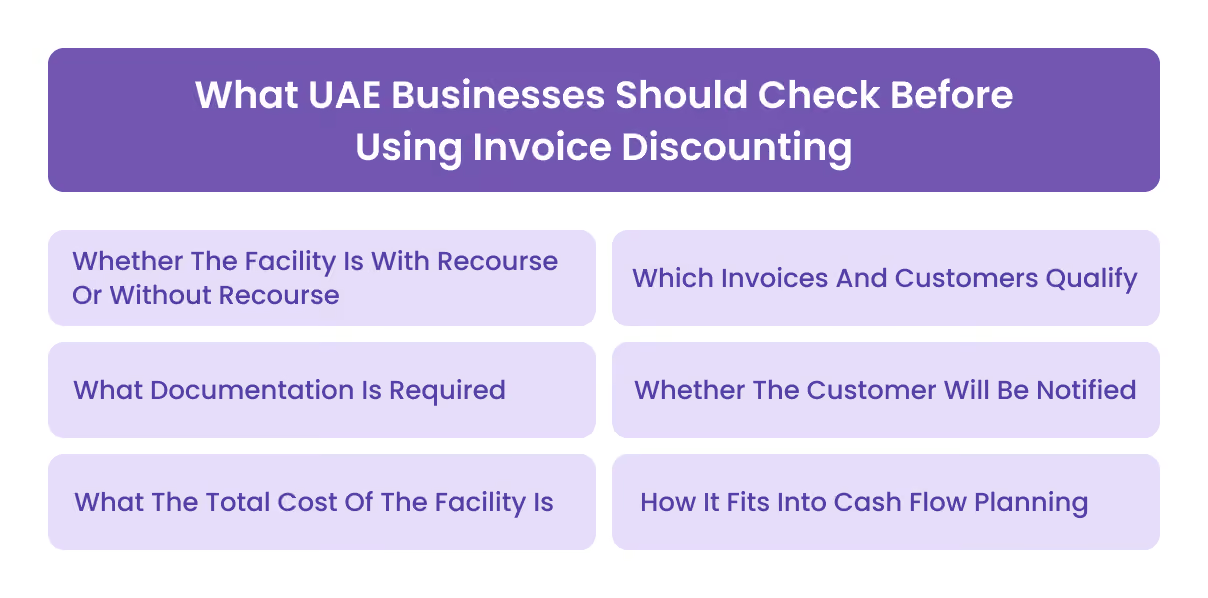

What UAE Businesses Should Check Before Using Invoice Discounting

Before using invoice discounting, finance teams should review the facility carefully to understand both the benefits and obligations involved.

1. Whether The Facility Is With Recourse Or Without Recourse

This determines who bears the risk if the customer does not pay. In many cases, the business remains responsible.

2. Which Invoices And Customers Qualify

Not all invoices may be eligible. Financiers often evaluate customer credit quality, invoice size, and payment history.

3. What Documentation Is Required

Typical requirements include invoices, delivery confirmations, customer details, and supporting trade documents. Incomplete documentation can delay funding.

4. Whether The Customer Will Be Notified

Some arrangements are confidential, while others require customer involvement. This affects how the relationship is managed.

5. What The Total Cost Of The Facility Is

Finance teams should assess all fees, including discount rates, administrative charges, and penalties.

6. How It Fits Into Cash Flow Planning

Invoice discounting improves short-term liquidity but must be aligned with future cash inflows, repayments, and overall working capital strategy.

Also Read: Cash Flow Forecasting

Common Mistakes Businesses Make With Invoice Discounting

Invoice discounting can improve liquidity, but its impact depends on how it is used. Many businesses run into issues not because the tool is flawed, but because it is applied without proper financial discipline.

1. Treating Discounted Cash As Free Cash

The advance received against invoices is still linked to an obligation. Treating it as unrestricted cash without considering repayment and fees can distort financial decisions.

2. Ignoring The True Cost Of Financing

Focusing only on the advance amount without evaluating discount rates, fees, and charges can lead to underestimating the actual cost of using the facility.

3. Discounting Invoices From Weak Customers

If customer payment reliability is low, invoice discounting increases risk. Delayed or defaulted payments can create additional pressure if the business remains liable.

4. Using Invoice Discounting Instead Of Fixing Collections

Invoice discounting should support cash flow, not replace proper receivables management. Weak collection processes can lead to overdependence on financing.

5. Failing To Track Financed Invoices Separately

Without clear tracking, businesses may lose visibility into which invoices are already discounted, creating confusion during reconciliation and reporting.

6. Mixing Discounted Cash With Operating Cash Without Clarity

Combining discounted proceeds with regular cash inflows can make it harder to understand actual business performance and cash generation.

Also Read: Account Reconciliation Importance Steps

How Invoice Discounting Affects Cash Flow Reporting

Invoice discounting changes the timing of cash inflows, which can make cash flow appear stronger in the short term. However, this does not change the underlying economic reality of the business.

The cash received from discounting is an advance against future receipts. The original customer payment is still expected, and the financing cost reduces the final amount retained.

For finance teams, this creates a reporting challenge. If discounted cash is treated as standard operating inflow without proper tracking, it can overstate performance and obscure true cash generation.

To maintain clarity, it is important to:

- Track discounted invoices separately from regular receivables

- Distinguish between operational cash inflow and financing inflow

- Account for fees and repayment obligations clearly

- Align cash flow reporting with actual business activity

This ensures that short-term liquidity improvements do not distort financial analysis.

How Alaan Helps Finance Teams Maintain Better Invoice And Cash Visibility

Invoice discounting relies heavily on the quality of receivables data, supporting documentation, and overall cash visibility. Without structured tracking, finance teams may struggle to understand which invoices are outstanding, which are financed, and how cash is actually moving through the business.

At Alaan, we focus on improving the execution layer that supports these decisions. While invoice discounting provides access to cash, effective spend and documentation control ensures that the underlying financial data remains accurate and usable.

- Corporate Cards With Spend Controls

Businesses can manage operational spending with defined limits and controls, reducing untracked outflows that distort cash visibility. - Structured Approval Workflows

Expenses are reviewed before they occur, helping maintain discipline in how cash is used across the business. - Real Time Visibility Into Expenses

Finance teams can monitor spending as it happens, making it easier to align outflows with incoming cash. - Centralised Invoice And Receipt Capture

All supporting documents are linked to transactions, improving traceability and reducing gaps in records. - Controlled Payment Execution With Full Cost Visibility (Super Pay)

Where businesses rely on invoice-based supplier payments, SuperPay allows finance teams to review the full payment impact before funds are released. This includes visibility into FX rates, transfer fees, and final settlement amounts, helping ensure that improved inflows from tools like invoice discounting are not offset by hidden costs or poorly timed outflows. - Seamless Accounting Integration

Integrations with Xero, QuickBooks, NetSuite, and Microsoft Dynamics ensure that financial data flows cleanly into accounting systems, supporting accurate reporting.

By improving how expenses and documentation are managed, Alaan helps finance teams maintain a clearer view of cash flow, making it easier to evaluate tools like invoice discounting within a broader financial strategy.

Conclusion

Invoice discounting can be a useful tool for improving short-term liquidity, especially for businesses that operate on extended payment terms. It allows companies to access cash tied up in receivables and maintain smoother operations without waiting for customer payments.

However, it is not a substitute for strong financial discipline. The effectiveness of invoice discounting depends on reliable customers, accurate invoice records, clear documentation, and consistent tracking of cash movement.

For finance teams, the focus should be on using invoice discounting as part of a broader cash flow strategy rather than relying on it to solve underlying issues. When supported by better visibility, structured approvals, and accurate reconciliation, businesses can manage both receivables and expenses with greater control.

If you want to improve how your business tracks cash movement and maintains financial visibility, you can explore how Alaan helps finance teams manage expenses, documentation, and reconciliation more effectively. Book a demo to see how better spend control supports stronger cash flow management.

Frequently Asked Questions

1. Does Invoice Discounting Affect Customer Relationships

It depends on the structure. Some invoice discounting arrangements are confidential, while others may involve notifying the customer. Businesses should understand whether customers will know that their invoices are being financed.

2. What Is A Typical Advance Rate In Invoice Discounting

Advance rates vary by financier, customer quality, invoice value, sector, and risk profile. Many facilities advance only a portion of the invoice value upfront, with the balance released after collection minus fees and charges.

3. Can A Business Use Invoice Discounting For Any Customer Invoice

Not always. Financiers may reject invoices linked to disputed work, weak customer credit, related-party transactions, missing documents, or customers with poor payment history. Eligibility depends on the financier’s risk assessment.

4. What Happens If The Customer Does Not Pay The Invoice

In a recourse arrangement, the business may remain responsible for repayment even if the customer does not pay. In a non-recourse structure, the financier may take on more credit risk, usually at a higher cost.

5. Is Invoice Discounting Better Than A Working Capital Loan

It depends on the business’s needs. Invoice discounting is tied to unpaid receivables and can scale with sales, while a working capital loan is a broader borrowing facility. The better option depends on cost, flexibility, risk, and repayment terms.

6. Can Invoice Discounting Hide Poor Collections Performance

Yes. It can bring cash forward, but it does not fix weak receivables management. If customers consistently pay late or invoices are often disputed, invoice discounting may reduce short-term pressure while leaving the underlying problem unresolved.