Deferred payment is not a new concept in finance, but it has taken on renewed importance for businesses in the UAE navigating tighter liquidity and rising compliance demands. Consider a mid-sized construction firm in Abu Dhabi: its suppliers offer 90-day terms on materials, while project revenues may not be collected for 120 days or more. Or take a marketing agency in Dubai subscribing to multiple SaaS platforms and preferring to spread those costs over installments rather than locking up cash upfront. Both examples reflect the same mechanism — a purchase today, a payment obligation tomorrow.

For finance leaders, deferred payment arrangements are neither inherently good nor inherently risky. They can preserve working capital, support project timelines, and provide short-term flexibility. At the same time, hidden fees, deferred interest, and regulatory nuances such as VAT timing can quickly erode any benefit. Mismanaging these obligations not only strains cash flow but also exposes businesses to audit issues and supplier disputes.

This article explains what deferred payment means in a business context, how it is commonly used in the UAE, the advantages and risks involved, and what finance teams should consider before agreeing to such terms.

Key Takeaways

- Deferred payment is a contractual liquidity tool, not an accounting adjustment — misuse blurs cash flow and financials.

- In the UAE, VAT is due at invoice issuance, not at payment — deferred payment doesn’t postpone VAT liability.

- Hidden costs (deferred interest, processing fees) often outpace the benefit of extended terms.

- A well-structured deferral contract demands explicit clauses: grace/cure periods, recourse, penalty triggers, and credit insurance.

- Embedding deferred obligations into forecasting models, ageing reports, and approval controls turns them from hidden liabilities into strategic levers.

Deferred payment explained in business finance

At its simplest, deferred payment refers to a contractual arrangement where a buyer receives goods or services immediately but agrees to pay at a later date. The delay may be a fixed grace period (for example, 30 or 60 days after invoice issuance) or a series of instalments spread across months.

In consumer finance, deferred payment often appears as a “buy now, pay later” (BNPL) option or an instalment plan on a credit card. For businesses, however, the implications are far more strategic. Deferred payment functions as a short-term financing tool that directly affects working capital, supplier relationships, and compliance timelines.

Key characteristics of deferred payment in corporate settings include:

- Timing: Payment is scheduled after delivery, often linked to invoice terms or agreed instalments.

- Cost: Some arrangements are interest-free; others carry interest, fees, or deferred interest clauses that activate if obligations are missed.

- Documentation: Proper invoices, terms, and VAT-compliant details are required under UAE regulations.

- Risk allocation: In B2B BNPL models, suppliers may transfer credit risk to a third-party insurer or financing partner.

For UAE finance leaders, deferred payment is not just a liquidity convenience. It is a decision that must be aligned with overall treasury management, VAT planning, and cash-flow forecasting. A poorly structured deferral may postpone a problem rather than solve it, while a well-negotiated one can provide breathing room to support growth and stability.

Also read: Real-time expense tracking — why it matters in the UAE

Common forms of deferred payment in the UAE

Although the principle of “pay later” is simple, the way it shows up in business transactions varies widely. In the UAE, finance teams most often encounter deferred payment in three forms:

1. Supplier and trade credit

The most traditional and widespread form is supplier credit, where vendors extend payment terms of 30, 60, or 90 days after delivery. This is common in industries like construction, logistics, and wholesale, where projects have long working-capital cycles.

- Example: A construction contractor receives steel shipments in March but is not required to pay until May.

- Benefit: The firm can use those two months to bill clients and generate inflows before settling the payable.

- Risk: Extending payables too far can strain supplier relationships and may invite tighter terms in future contracts.

2. B2B “buy now, pay later” (BNPL) and instalments

What started as a consumer phenomenon has made its way into corporate procurement. Several fintech platforms now offer B2B BNPL in the UAE, where companies can split vendor invoices into multiple instalments.

- Example: A Dubai-based SaaS reseller allows corporate customers to pay for annual licences in quarterly instalments instead of upfront.

- Advantage: Aligns subscription costs with revenue cycles.

- Risk: If not tracked carefully, multiple BNPL arrangements across departments can accumulate into hidden liabilities.

3. Card-based deferrals and instalment plans

Many UAE banks and issuers allow cardholders to convert a transaction into fixed monthly instalments. Some corporates permit this for large purchases; others restrict it through card policy.

- Example: An agency books a large digital advertising campaign on a corporate card and converts the payment into six instalments.

- Benefit: Flexibility for one-off expenses without needing supplier negotiation.

- Risk: Processing fees and deferred interest clauses can make these arrangements more expensive than traditional supplier credit.

Deferred payments may also appear in hybrid models — for example, a supplier offers 60-day credit but outsources collections to a financing partner that charges the buyer a service fee. Finance leaders need to evaluate the total cost of such arrangements, not just the headline term.

Also read: Corporate card policy best practices

Why finance teams use deferred payment to protect liquidity

When structured carefully, deferred payment can be more than a short-term cash buffer. It becomes part of a deliberate working-capital strategy. The main advantages include:

1. Preserving liquidity for core priorities

Delaying outflows frees up cash for payroll, supplier advances, or growth initiatives. For example, a retail chain in Dubai heading into peak season might defer inventory payments until after sales revenue is realised. This allows management to cover staffing and marketing without tapping credit lines.

2. Matching outflows to inflows in project-driven businesses

Industries such as construction, real estate development, and creative agencies often bear costs well before client invoices are paid. Deferred payment enables firms to align supplier settlements with customer receipts, smoothing the cash gap that would otherwise require external financing.

3. Negotiating flexibility with suppliers

Suppliers may be willing to offer early-payment discounts even within deferred arrangements. A 2% discount for paying within 10 days on a 60-day invoice, for instance, can represent a risk-free return that is attractive when cash is available.

4. Expanding procurement options

Deferred terms can make it feasible to invest in technology, equipment, or large service contracts that might otherwise stretch budgets. For example, hospitals procuring medical equipment often use deferred instalments to spread costs while still ensuring timely upgrades.

5. Reducing reliance on short-term borrowing

Well-negotiated deferrals can reduce the need for overdrafts or short-term loans, cutting interest costs and strengthening the balance sheet.

Risks Finance Leaders Must Account For

While deferred payment offers breathing room, the risks can outweigh the benefits if not evaluated carefully.

1. Hidden Interest and Fees

Many card-based deferrals and BNPL products advertise “0%” or “no cost” instalments. In practice, finance teams may encounter processing fees, service charges, or deferred interest clauses that backdate charges if balances are not cleared on time. What appears interest-free can quickly become costlier than short-term credit lines.

2. VAT Timing and Compliance Obligations

Under UAE VAT rules, liability typically arises when the tax invoice is issued, not when the payment is made. A deferred arrangement does not postpone this obligation. For example, if an invoice is issued in April with a 90-day payment term, VAT is due in the April return even if cash will not leave the business until July. Failure to plan for this gap risks penalties or cash-flow mismatches.

3. Supplier Relationship Strain

Stretching payables may damage relationships with critical vendors. Suppliers in construction and logistics often operate on thin margins themselves; delayed settlement can push them to tighten credit or demand upfront payment in the future. For businesses dependent on specialised suppliers, this can introduce operational fragility.

4. Audit and Documentation Gaps

Without clear documentation, deferred arrangements can cause disputes during audits. Missing payment terms, incomplete tax invoices, or unclear responsibilities in a BNPL contract can lead to non-recoverable VAT and compliance breaches.

5. Accumulated Liabilities

When multiple departments enter into deferred arrangements simultaneously, liabilities can pile up out of view. Without centralised monitoring, finance teams risk discovering significant obligations only at month-end or quarter-close — a common cause of reconciliation delays.

Deferred Payment vs Deferred Revenue and Expenses

The word deferred shows up frequently in finance, but its meaning shifts depending on context. Confusing these terms can lead to reporting errors, miscommunication with auditors, and poor cash-flow planning.

Deferred Payment

A contractual arrangement where the buyer receives goods or services now and pays later.

- Example: A logistics company in Dubai purchases fuel and agrees to settle the invoice 60 days after delivery.

- Impact: Creates a short-term liability under accounts payable.

Deferred Revenue

An accounting concept under IFRS and GAAP where payment is collected in advance, but revenue recognition is postponed until goods or services are delivered.

- Example: A SaaS firm in Abu Dhabi bills an annual subscription upfront in January but recognises revenue monthly over the year.

- Impact: Recorded as a liability until the service is provided.

Deferred Expense

An accounting concept where cash is paid in advance, but expense recognition is deferred and spread across the period of benefit.

- Example: A hospital in Sharjah pays for a 12-month insurance policy in January, expensing it gradually each month.

- Impact: Initially recorded as a prepaid asset, reduced over time.

Comparison at a Glance

Key takeaway:

- Deferred payment is a contractual, liquidity-related arrangement.

- Deferred revenue/expenses are accounting treatments for timing of recognition.

Mixing them up risks misstating liabilities, assets, and income, which has implications for both audits and compliance.

Also read: UAE VAT Tax Invoice Format — Checklist for Finance Teams

Structuring Deferred Payment Terms Effectively

A deferred payment arrangement is only as safe as the terms agreed in writing. For finance leaders, the negotiation should go beyond the number of days in the payment window. Key clauses to examine include:

1. Interest and Penalty Clauses

Is the arrangement genuinely interest-free, or are charges applied if deadlines are missed? Some contracts include deferred interest, where interest is applied retroactively from the original transaction date if payment is not made in full by the due date.

2. Grace and Cure Periods

Suppliers may offer a short grace period before penalties are triggered. A cure period allows the buyer additional time to rectify a missed payment without defaulting. These details matter when planning working capital under tight cash cycles.

3. Fee Structures

BNPL providers and banks often charge processing fees for instalment conversions or service fees for extended terms. These should be factored into total cost of capital when comparing against alternatives like credit lines or overdrafts.

4. Recourse and Dispute Resolution

Contracts should clarify what happens if goods are defective or services incomplete. For UAE businesses operating across multiple jurisdictions, ensure that governing law and dispute-resolution mechanisms are clearly stated.

5. Insurance and Third-Party Risk Transfer

Some B2B BNPL arrangements in the UAE are backed by credit insurance, protecting the supplier if the buyer defaults. Finance teams should confirm the insurer’s coverage scope and exclusions. Not all contracts guarantee the same level of protection.

6. VAT-Compliant Documentation

Even with deferred terms, VAT liability is triggered when the invoice is issued. The invoice must include:

- Supplier and buyer Tax Registration Numbers (TRNs)

- Accurate description of goods or services

- Payment terms clearly stated

- VAT amount calculated correctly

Without these details, companies risk non-recoverable VAT and compliance penalties during Federal Tax Authority (FTA) audits.

Also read: Sample Business Expense Policy — Guidelines and Examples

[cta-4]

Incorporating Deferred Payments Into Cash-Flow Planning

Deferred payments may solve an immediate liquidity gap, but they still represent future obligations that must be tracked and planned for. Effective use requires embedding them directly into cash-flow models and finance workflows.

Model Deferred Liabilities in Forecasts

Finance leaders should treat deferred payments as short-term liabilities in cash-flow forecasts, not simply as “delayed expenses.” This means mapping expected outflows by maturity date and integrating them into rolling 13-week or 90-day forecasts.

- Example: A Dubai-based distributor defers AED 1 million in supplier invoices to 90 days. Unless modelled, the sudden cash squeeze in the following quarter can disrupt payroll or tax payments.

Set Approval Thresholds

Not all deferrals should be treated equally.

- Low-value deferrals (e.g., AED 10,000 marketing invoices) may follow departmental workflows.

- High-value deferrals (e.g., AED 500,000+ procurement contracts) should require CFO or board-level approval.

Clear thresholds prevent overuse and ensure senior oversight of material obligations.

Monitor Ageing Schedules

Deferred liabilities should appear in the same ageing reports used for accounts payable. Finance teams should categorise them by 30/60/90 days and reconcile against cash forecasts. This prevents deferred invoices from becoming “invisible” until they are due.

Align With VAT Payment Cycles

Because VAT is due upon invoice issuance in the UAE, companies must ensure the VAT portion of deferred invoices is funded on time — even if the net amount will not be paid until later. Factoring VAT into weekly cash forecasts avoids liquidity mismatches.

Reconcile Early, Not Just at Maturity

Instead of waiting until the due date, finance teams should reconcile deferred invoices continuously. Matching invoices to purchase orders, checking receipt details, and earmarking funds in advance reduce month-end reconciliation stress.

Also read: Cash Flow Forecasting — Best Practices for UAE Businesses

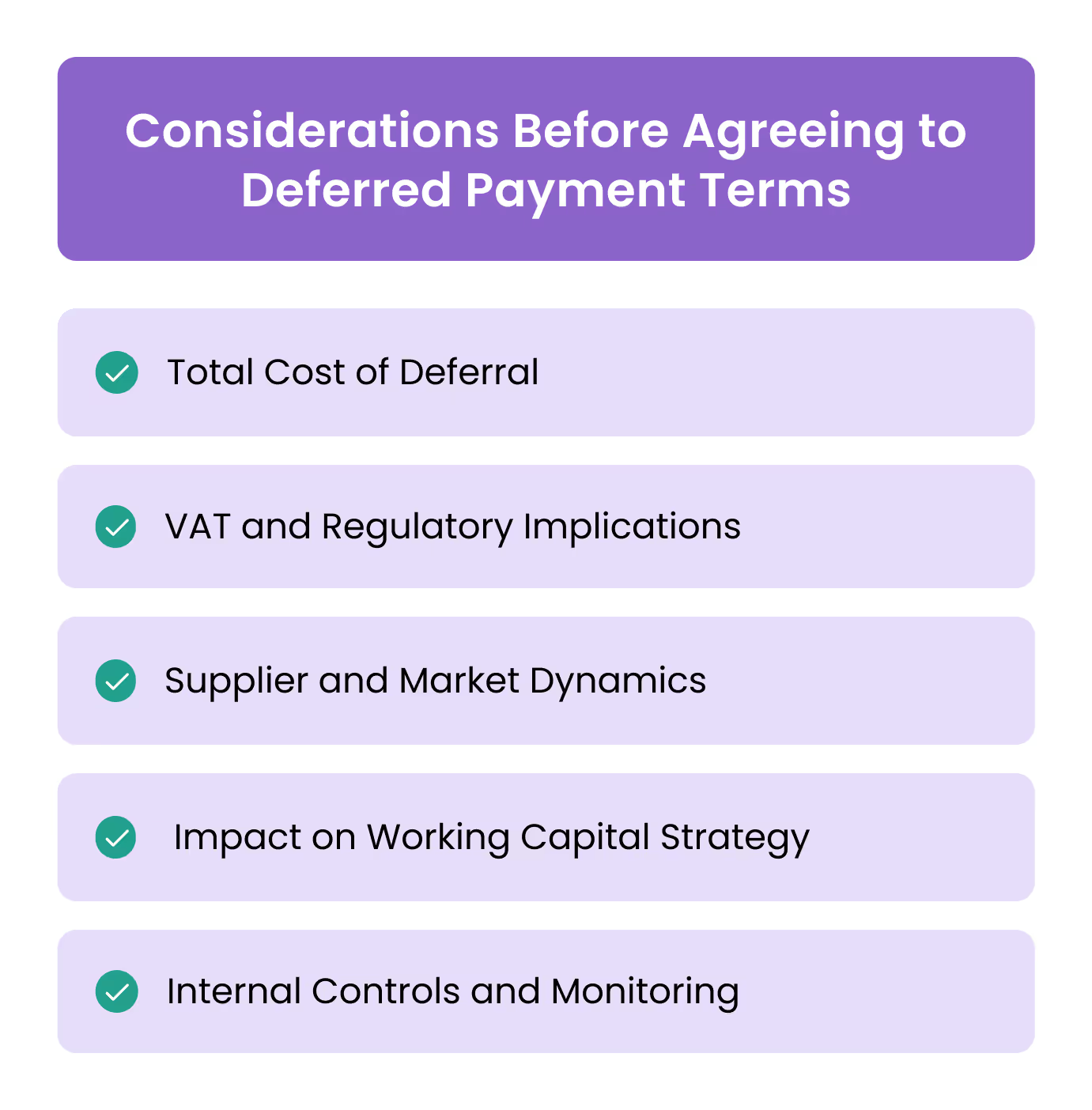

Key Considerations Before Agreeing to Deferred Payment Terms

A deferred payment agreement should never be signed on the strength of headline terms alone. For finance leaders in the UAE, the following considerations determine whether such arrangements strengthen or weaken the organisation’s financial position.

1. Total Cost of Deferral

Look beyond the stated payment window. Processing fees, deferred interest, penalty rates, and opportunity costs (such as lost early-payment discounts) all contribute to the true cost of the arrangement. In some cases, a short-term credit facility may be cheaper than a “0%” instalment plan.

2. VAT and Regulatory Implications

Even if cash settlement is delayed, VAT liability arises when the invoice is issued. Businesses must ensure they can fund VAT obligations on schedule, or risk compliance breaches with the Federal Tax Authority (FTA). VAT rules also require accurate invoice data — without TRN, VAT rates, and correct descriptions, input VAT may be unrecoverable.

3. Supplier and Market Dynamics

Using extended terms may provide short-term relief but could strain supplier relationships. Vendors may respond with tighter conditions, higher prices, or even restrict credit in the future. For businesses dependent on critical suppliers, this can erode supply-chain resilience.

4. Impact on Working Capital Strategy

Deferred obligations should be tested in cash-flow forecasts under different scenarios (e.g., delayed customer receipts, currency fluctuations). Finance leaders must understand whether deferrals align with liquidity strategy or simply postpone a cash crunch.

5. Internal Controls and Monitoring

Without clear approval flows, vendor whitelists, and spend limits, deferred payments can proliferate across departments and create hidden liabilities. Embedding monitoring into spend-management systems ensures visibility and accountability.

At Alaan, we help UAE finance teams enforce these controls in real time — from role-based approvals to invoice capture and reconciliation — so deferred payments become a strategic tool, not an uncontrolled liability.

Also read: Expense Reimbursement Best Practices for UAE Businesses

How Alaan Simplifies Per Diem and Travel Expense Management

At Alaan, we see UAE finance teams managing travel allowances far more efficiently when per diem policies are integrated directly into their spend workflows.

With Alaan’s corporate cards and expense management platform, companies can:

- Issue daily or trip-based allowances instantly—no manual fund transfers or petty cash.

- Apply role-based approval flows that match internal travel policy.

- Set card-level limits for meals, lodging, or international spending to prevent misuse.

- Use real-time dashboards to track active trips, per diem disbursed, and average spend per day.

- Automate reconciliation, VAT checks, and reporting for every trip—without chasing receipts.

This automation gives finance leaders full visibility into allowances while freeing employees from manual claims. It transforms per diem from a static policy into a dynamic, auditable system that scales with business growth.

Book a demo with Alaan to see how leading UAE organisations manage per diem allowances, travel expenses, and reimbursements in one unified platform.

Frequently Asked Questions (FAQs)

1. How does deferred payment differ from EMI or installment payment?

Deferred payment may allow paying the full amount at a later date or splitting into instalments; EMI is typically fixed monthly payments over a period. Deferred plans might include retroactive interest if conditions aren’t met.

2. Does deferred payment affect my cash flow positively or negatively?

When used sparingly and tracked, deferred payment improves short-term cash flow. But if liabilities accumulate without control, it may create cash crunches later.

3. Will deferred payment impact my VAT reporting or audit risk?

Yes. In the UAE, VAT liability arises at invoice issuance, not when payment is made. Incorrect invoices or undocumented deferrals can raise audit flags and non-recoverable VAT.

4. Do suppliers usually charge extra for offering deferred payment?

Often yes. They may embed interest, management fees, or processing costs that reduce the apparent benefit of the extended term.

5. When should a finance team say no to deferred payment offers?

When hidden costs are high, vendor relationships risked, forecasting shows tight liquidity, or internal controls are insufficient to track the obligations.

6. How can technology help manage deferred payments effectively?

Platforms with real-time dashboards, spend tracking, approval workflows, and invoice capture help finance leaders monitor deferred obligations, ensure compliance, and avoid surprise liabilities.