Financial reporting is often described as the backbone of corporate finance — but for today’s CFOs, it is much more than compliance paperwork. Accurate, timely, and transparent reporting shapes investor confidence, enables access to credit, and ensures businesses stay on the right side of regulators.

In the UAE, the stakes are even higher. With the adoption of IFRS as the national standard, the rollout of Corporate Tax at 9%, and existing VAT obligations, financial reporting has shifted from a quarterly task to a strategic discipline. Reports are no longer just filed — they are scrutinised by auditors, investors, banks, and tax authorities. Any weakness in accuracy or timeliness can lead to penalties, lost funding opportunities, or reputational damage.

At the same time, finance leaders are expected to provide boards and investors with forward-looking insights, not just historical accounts. This means reporting must bridge compliance with strategy — a balancing act made possible only through automation and modern fintech infrastructure.

Key Takeaways

- Financial reporting = compliance + strategy. It’s the structured presentation of financial data under IFRS, forming the basis for VAT and corporate tax filings as well as investor confidence.

- UAE businesses face dual pressures. Reports must satisfy both international standards (IFRS) and local obligations (FTA filings, Central Bank oversight), making accuracy and timeliness critical.

- Traditional methods fall short. Manual spreadsheets and fragmented data create risks: errors, delays, and rejected VAT claims.

- Automation is a game-changer. Real-time expense capture, AI-driven reconciliations, and audit-ready trails reduce risk while saving time.

- Best practice = proactive finance. Align reporting calendars with tax deadlines, embed controls, automate reconciliations, and maintain continuous audit readiness.

Why Financial Reporting Matters Beyond Compliance

For experienced finance professionals, financial reporting is the language through which a company communicates with its stakeholders. Its value extends far beyond statutory requirements:

- Investor confidence: Transparent reporting is often the first checkpoint for investors evaluating UAE startups and scale-ups. A single audit exception can delay or derail funding rounds.

- Operational decision-making: Detailed cash flow and margin reporting help CFOs decide whether to expand, restructure, or conserve capital in volatile markets.

- Regulatory compliance: VAT submissions, IFRS-compliant statements, and corporate tax filings all rely on robust reporting frameworks. Late or inaccurate filings risk financial penalties and regulatory red flags.

- Strategic growth: When expanding into Saudi Arabia or wider GCC, reliable financial reporting helps companies align with regional regulations and build credibility with cross-border partners.

In short, financial reporting is not just about documenting the past — it’s about building trust and enabling growth in real time.

Financial Reporting Meaning in Practice

At its core, financial reporting is the structured presentation of a company’s financial position and performance to stakeholders — from boards and investors to regulators and tax authorities. It turns raw financial data into a formalised narrative that demonstrates whether a business is compliant, profitable, and sustainable.

But in practice, “financial reporting” for a CFO in the UAE goes beyond simply producing a balance sheet or income statement. It means:

- Adhering to IFRS: Since 2015, International Financial Reporting Standards (IFRS) have been mandatory for most UAE companies, aligning the country with global practices. Reports must meet IFRS definitions of revenue, expenses, and disclosures — leaving little room for ambiguity.

- Supporting VAT and Corporate Tax filings: Financial reports now form the foundation for tax submissions. For example, VAT returns depend on accurate classification of expenses, while corporate tax filings require clear profit attribution. Weak reporting can directly trigger penalties or disputes with the Federal Tax Authority (FTA).

- Enabling governance and audit: The Central Bank of the UAE requires external audits for licensed entities and financial service providers. This makes reporting not just an internal discipline, but a governance obligation tied to operational licenses.

- Driving strategic conversations: Financial reporting also informs management discussions on growth strategies, capital structure, and risk exposure. The way figures are presented can influence whether a business secures new funding, restructures debt, or proceeds with an expansion.

In other words, financial reporting meaning in a UAE business context = a dual mandate:

- Compliance-first (satisfy IFRS, VAT, CT, and audit requirements).

- Strategy-enabled (turn numbers into board-level decisions and investor-ready insights).

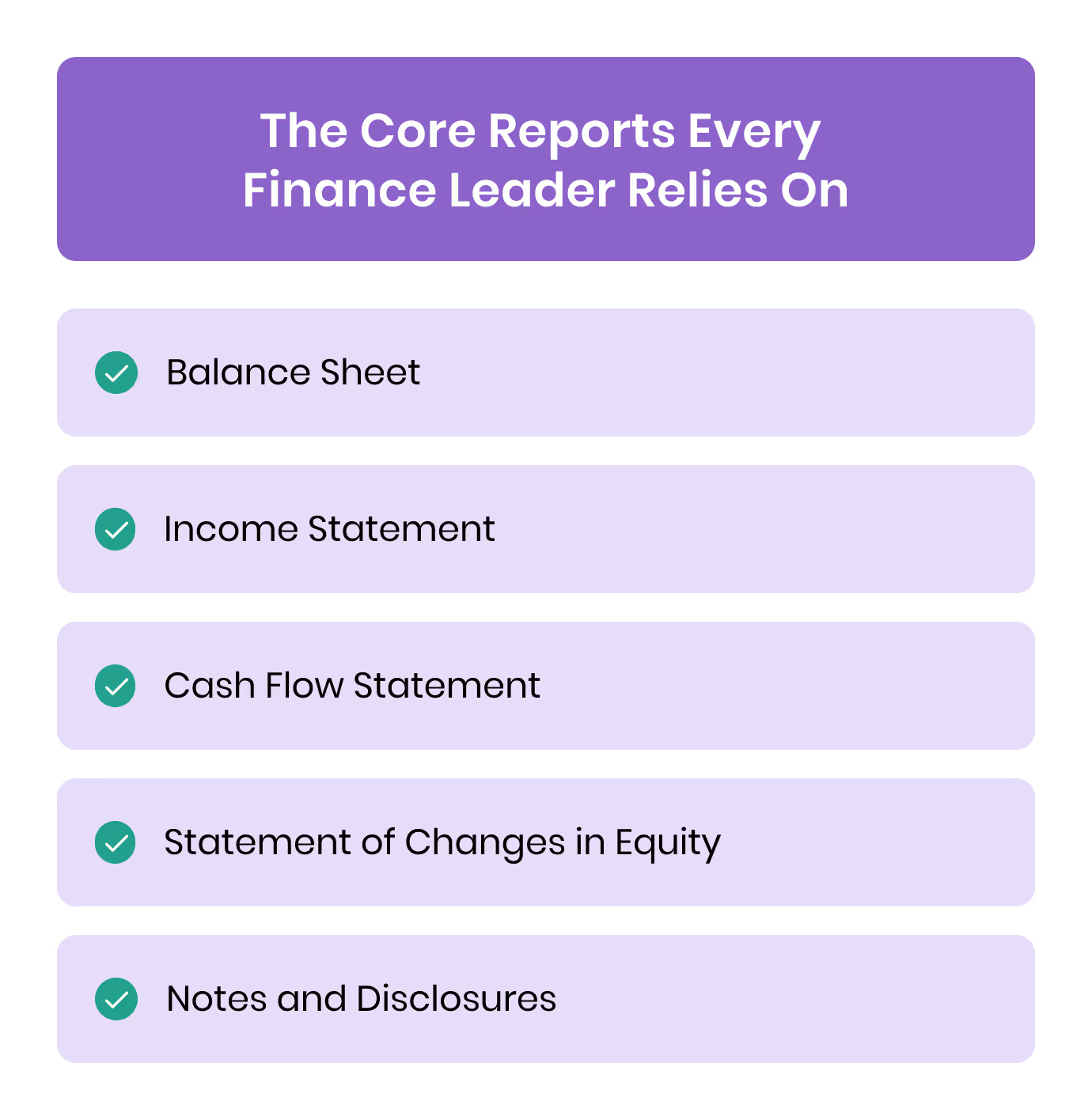

The Core Reports Every Finance Leader Relies On

Financial reporting is built on a set of primary statements. While the formats are standardised under IFRS, the way CFOs interpret them in practice determines whether they serve as compliance documents or strategic decision tools.

1. Balance Sheet: The Business at a Glance

The statement of financial position is more than a snapshot of assets and liabilities — it shows liquidity, leverage, and solvency. For UAE firms, banks and investors scrutinise debt-to-equity ratios closely before approving financing. In regulated sectors, the Central Bank also uses balance sheets to monitor capital adequacy.

2. Income Statement: Profitability and Tax Basis

Beyond showing revenues and expenses, the income statement forms the foundation for corporate tax calculations in the UAE. Misclassification of expenses or revenue recognition errors can trigger disputes with auditors or the FTA. CFOs rely on this report to track margins, set cost-control strategies, and evaluate whether growth is sustainable.

Also read: Understanding Cost Management

3. Cash Flow Statement: Survival and Sustainability

Cash flow is often the most practical indicator of financial health. A company may show profits on paper but still face liquidity crises if receivables are delayed. In the UAE, where seasonal demand and cross-border transactions are common, cash flow statements help CFOs ensure enough liquidity for payroll, VAT payments, and vendor settlements.

4. Statement of Changes in Equity: Investor Confidence

This report details how profits are retained, distributed, or reinvested. For startups in hubs like DIFC or ADGM seeking venture capital, equity statements help demonstrate governance and justify valuations. Investors want to see disciplined capital allocation, not just top-line growth.

5. Notes and Disclosures: Audit Defense

The supporting notes explain policies, assumptions, and risks — everything from lease obligations to related-party transactions. In UAE audits, these disclosures are often where regulators and auditors spot compliance gaps. Well-prepared disclosures build trust and reduce the likelihood of restatements.

Strong reporting isn’t just about producing these documents — it’s about ensuring they are accurate, timely, and aligned with IFRS and UAE tax requirements. At Alaan, we provide finance teams with real-time expense tracking and help with reconciliations, ensuring reports are accurate, audit-ready, and reliable for board reviews.

[cta-4]

Also read: Improving Internal Control in Financial Reporting

Reporting Standards and UAE Compliance Imperatives

For finance leaders in the UAE, “financial reporting” cannot be separated from regulation. The country’s adoption of International Financial Reporting Standards (IFRS), combined with VAT (5%) and Corporate Tax (9%), has made reporting both a compliance obligation and a credibility test.

IFRS as the Baseline

Since 2015, IFRS has been mandatory for most UAE companies, aligning them with international practice. Unlike localised frameworks, IFRS requires detailed disclosures, fair value accounting, and strict treatment of revenue and expenses. For CFOs, this means:

- Reports must be globally comparable — useful for attracting foreign investment.

- Estimates and assumptions must be documented clearly, reducing subjectivity.

- Auditors have a standardised basis to review, reducing scope for disputes.

VAT and Corporate Tax Demands

- VAT filings depend on accurate categorisation of sales and purchases. Misreporting input VAT can trigger penalties or rejected claims.

- Corporate Tax filings rely on precise income statements and reconciliations. Errors in expense treatment or intercompany transactions can draw scrutiny from the Federal Tax Authority (FTA).

- Both VAT and CT deadlines mean reporting calendars must be tightly managed — late filings can erase months of financial progress with penalties.

(Also read: Filing and Making VAT Payments in the UAE)

Central Bank Oversight

Licensed financial institutions — from banks to fintechs — must also comply with the Central Bank of the UAE’s Rulebook on Financial Reporting and External Audit. This elevates the role of reporting to a governance standard, where non-compliance risks regulatory action.

Investor and Market Expectations

For startups in DIFC or ADGM, audited financial reports are often a prerequisite for raising capital. Investors are increasingly demanding IFRS-compliant, transparent reporting before committing funds. A weak reporting process can delay deals or reduce valuations.

In practice, UAE CFOs must manage reporting across three fronts: regulatory filings, investor expectations, and internal decision-making. Modern fintech platforms like Alaan help bridge these by ensuring transactions are recorded in real time, VAT is validated, and reports are always audit-ready.

[cta-6]

Where Traditional Reporting Falls Short

Despite the clear regulatory frameworks, many businesses in the UAE still rely on outdated reporting processes. Manual spreadsheets, fragmented data sources, and retrospective reconciliations create risks that go beyond inefficiency.

1. Slow, Static Reporting Cycles

Traditional month-end or quarter-end closes are too slow for a fast-moving market. By the time reports are produced, CFOs are reacting to outdated information. This delay can mean missed opportunities or compliance surprises, especially with VAT and corporate tax deadlines.

2. High Risk of Human Error

Manual data entry, spreadsheet linking, and late reconciliations introduce errors that ripple through financial statements. In UAE audits, even minor misstatements can trigger penalties or erode investor trust.

3. Poor Expense Data Quality

Expense data often sits at the root of reporting challenges. Missing receipts, non-compliant invoices, and unapproved spending distort the accuracy of VAT claims and profitability calculations. In the UAE context, this can result in rejected VAT recoveries or corporate tax disputes.

4. Lack of Real-Time Visibility

Legacy systems provide historical snapshots, not current insights. Without real-time dashboards, CFOs cannot detect spending anomalies or forecast cash flow accurately. This weakens both compliance and strategic decision-making.

5. Disconnected Teams and Systems

When finance, procurement, and operations rely on separate tools, reports become siloed. Reconciling this data manually wastes time and increases audit risk. For cross-border UAE businesses, fragmented reporting makes it even harder to ensure IFRS alignment.

In our work with UAE companies, we often see that the root cause of reporting failures isn’t IFRS complexity — it’s process inefficiency. By digitising expenses and automating reconciliations, businesses move from error-prone, static reporting to audit-ready visibility in real time.

Also read: Track and Manage Business Expenses

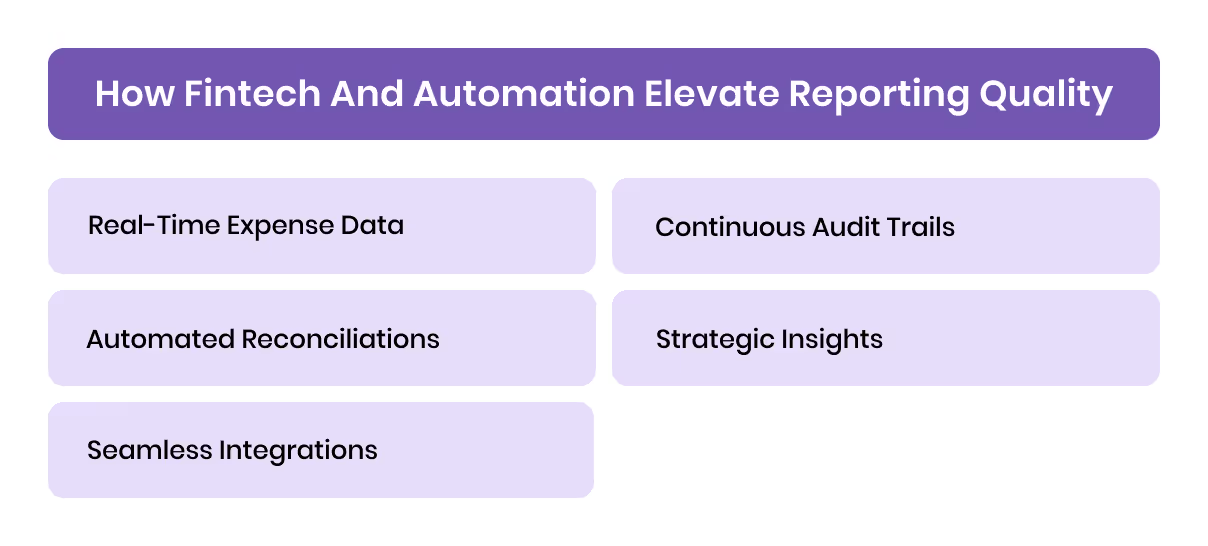

How Fintech and Automation Elevate Reporting Quality

Modern finance leaders cannot afford to treat reporting as a backward-looking task. With regulators, investors, and boards demanding both accuracy and speed, technology has become central to producing high-quality reports.

1. Real-Time Expense Data

Fintech platforms capture every transaction at the point of spend, eliminating the lag between expense and reporting. Instead of waiting weeks for reconciliations, CFOs can monitor cash burn, vendor payments, and VAT positions in real time.

2. Automated Reconciliations

AI-driven systems match receipts with transactions automatically, validate VAT fields, and flag anomalies. This reduces the risk of errors that often slip through manual checks and later cause audit disputes.

3. Seamless Integrations with ERP and Accounting

APIs allow expense platforms to sync directly with systems like Xero, QuickBooks, and Microsoft Dynamics. This ensures that financial data flows smoothly into reporting tools without manual uploads or formatting errors.

4. Continuous Audit Trails

Automation doesn’t just accelerate reporting — it creates built-in audit trails. Every transaction is logged with supporting documents, approval history, and tax validations. For UAE companies facing annual external audits or tax inspections, this readiness is a competitive advantage.

5. Strategic Insights

Beyond compliance, fintech-powered reporting provides forward-looking intelligence. CFOs can analyse spend categories, track working capital, and model tax scenarios — moving reporting from a regulatory exercise to a decision-making engine.

At Alaan, we see businesses move from static, error-prone reporting to audit-ready, insight-driven reporting within months of adoption. By combining corporate cards, AI receipt validation, and automated reconciliations, CFOs gain the assurance that every figure in their reports is accurate, compliant, and investor-ready.

Also read: Modern Expense Management Guide

Best Practices for UAE Businesses

Producing high-quality financial reports is not only about meeting IFRS requirements — it’s about building a finance function that is disciplined, efficient, and audit-ready. For CFOs in the UAE, the following practices create a strong foundation:

1. Align Reporting Calendars with Tax Deadlines

Set financial close and reporting cycles to ensure VAT and Corporate Tax filings are always prepared on time. This reduces last-minute errors and avoids costly penalties from the Federal Tax Authority (FTA).

2. Standardise Templates Under IFRS

Use consistent formats and disclosure structures across all entities and reporting periods. This not only supports IFRS compliance but also makes audits and investor reviews smoother.

3. Automate Reconciliations and Approvals

Replace manual reconciliations with automated tools that match receipts, validate VAT entries, and flag anomalies. Automated approvals ensure transactions are policy-compliant before they hit the books.

4. Strengthen Internal Controls

Implement real-time spend controls such as card limits, vendor locks, and approval flows. Strong internal controls prevent non-compliant spending from distorting reports.

[cta-3]

(Also read: Effective Business Spending Policies)

5. Link Financial Goals to Reporting KPIs

Reporting should not only look backward but also track progress against strategic financial goals (e.g., cash runway, gross margin targets, or debt-to-equity ratios). This keeps reporting relevant to decision-making, not just compliance.

6. Maintain Continuous Audit Readiness

Build audit requirements into everyday workflows. Ensure supporting documents, VAT-compliant invoices, and approval histories are available in one place. This reduces the stress of year-end audits and strengthens investor trust.

Businesses in the UAE that embed these practices find that reporting shifts from a regulatory burden to a strategic advantage. With Alaan, many of these steps — from automated reconciliations to VAT validation — are built into the platform, helping finance teams achieve both compliance and efficiency.

Conclusion

Financial reporting is far more than compliance paperwork. For UAE businesses, it sits at the intersection of IFRS standards, VAT obligations, corporate tax filings, and investor scrutiny. Poor reporting creates risks — from regulatory penalties to lost investor confidence — while strong reporting builds credibility and unlocks strategic decision-making.

By adopting structured processes, embedding automation, and aligning reporting cycles with regulatory deadlines, finance leaders can elevate reporting from a reactive exercise to a proactive advantage.

At Alaan, we help CFOs and finance teams achieve this shift. Our platform integrates corporate cards, AI-driven receipt validation, automated reconciliations, and VAT compliance checks into one seamless system. The result: financial reports that are accurate, timely, and always audit-ready.

Book a demo today to see how Alaan can simplify financial reporting for your business.

FAQs on Financial Reporting Meaning

1. What does financial reporting mean in business?

Financial reporting is the process of preparing statements and disclosures that reflect a company’s financial performance and position. It includes balance sheets, income statements, cash flow statements, and notes prepared under standards such as IFRS.

2. Why is financial reporting important for UAE businesses?

In the UAE, reporting ensures compliance with VAT (5%) and corporate tax (9%) regulations. It also builds trust with auditors, banks, and investors, making it essential for both growth and governance.

3. How often should financial reports be prepared?

Most companies prepare reports monthly, quarterly, and annually. In the UAE, deadlines are also tied to VAT and corporate tax submissions, making regular reporting cycles a necessity.

4. What is the difference between financial reporting and accounting?

Accounting is the process of recording transactions, while financial reporting is the structured presentation of that information in statements and disclosures for regulators, auditors, and stakeholders.

5. What are the risks of poor financial reporting?

Risks include regulatory penalties, rejected VAT claims, delayed audits, reduced investor confidence, and poor internal decision-making. For UAE businesses, the consequences can directly affect both compliance and growth.

6. How can automation improve financial reporting?

Automation ensures that expense data is captured in real time, VAT is validated, reconciliations are accurate, and audit trails are complete. This reduces manual errors, saves time, and makes reporting more reliable.