For many growing companies in the GCC, access to timely funding is one of the toughest hurdles. The region’s SME financing gap is estimated at over $250 billion, leaving finance teams searching for alternatives that don’t involve lengthy bank approvals or heavy collateral requirements.

One option that has gained traction is the Merchant Cash Advance (MCA). Unlike traditional loans, MCAs provide quick access to capital (often within days) with repayments tied directly to sales or revenue streams. For SMBs and mid-market enterprises scaling rapidly, this flexibility can be a lifeline.

But speed comes at a cost. MCAs are often expensive, and repayment amounts fluctuate with revenue, creating potential cash flow strain.

This guide breaks down what finance leaders need to know about MCAs: how they work, the trade-offs involved, checklists for evaluation, and alternative financing routes worth considering in the GCC market.

Key Takeaways

- Benefits of MCA: Businesses gain fast funding, flexible repayment linked to revenue, and freedom to use funds across operations.

- How It Works: An MCA involves an upfront advance, daily or weekly repayment through card sales, and final settlement once the balance is cleared.

- Pros and Cons of MCAs: When MCAs are most effective, and when MCAs pose cash flow risks.

- Checklist for Decision: Evaluate card sales, cash flow, business age, repayment ability, and margin sufficiency to determine if an MCA fits your business.

- Application Process: MCA approval depends on transaction history and revenue patterns, not credit score or collateral, allowing funding in 24–72 hours.

- Alternatives to MCA: Revenue-based financing, term loans, invoice financing, or business lines of credit may offer lower costs and more predictable repayment.

What a Merchant Cash Advance Does for Your Business

Cash flow gaps can slow growth, especially when customer payments or bank approvals take time. A Merchant Cash Advance (MCA) addresses this by providing a lump sum of funding upfront, with repayment automatically tied to your sales or revenue streams.

Instead of fixed monthly instalments, a portion of your daily or weekly card transactions, called a holdback, is collected until the total repayment is complete. Unlike a traditional interest rate, the factor rate is a fixed multiplier that determines the total repayment, regardless of how quickly you repay.

In practice, the cycle is simple: advance → holdback → settlement.

This approach gives businesses fast access to capital without requiring collateral, while aligning repayments with actual revenue. It’s particularly effective for companies with predictable, card-heavy sales, though costs can rise if sales fluctuate unexpectedly.

What People Often Get Wrong About MCAs

At first glance, MCAs look similar to small business loans, but their mechanics and costs differ significantly.

The difference is that MCAs don’t have fixed monthly installments. Instead, costs are calculated with a factor rate, and repayments move up or down with sales. This catches many businesses off guard, especially when cash flow is uneven. A direct comparison makes the distinction clear:

Why does the difference matter? Because companies with strong sales volumes but weaker credit often turn to MCAs when bank loans aren’t an option. The trade-off: while MCAs are more accessible, their effective annual cost can be significantly higher, putting added pressure on cash flow.

How MCAs Differ from Other Funding Options

In the UAE, businesses looking for working capital aren’t limited to MCAs. Alternatives such as loans, credit lines, and invoice factoring each come with different costs and repayment structures, which directly shape how cash flow is managed.

1. Loans vs MCAs (interest vs factor rate)

Traditional loans charge interest over a fixed term. For example, an AED 50,000 loan at 10% annual interest over three years results in approximately AED 8,000 in interest. In contrast, a merchant cash advance with a 1.3 factor rate requires repayment of AED 65,000, regardless of how quickly the business repays.

Loans offer predictable monthly payments, while MCAs adjust automatically to sales volume, giving faster access but potentially higher effective cost.

2. Business lines of credit vs MCAs

A business line of credit works like a revolving facility: you borrow what you need, pay interest only on the drawn amount, and replenish the balance as you repay. For example, a company drawing AED 30,000 for one month at 1% monthly interest would pay AED 300.

MCAs, by contrast, deduct a fixed percentage from card sales daily or weekly, which suits businesses with steady transaction volumes but can strain cash flow if sales fluctuate.

3. Invoice factoring vs MCAs

Invoice factoring converts outstanding invoices into cash by selling them to a provider. For instance, a B2B company with AED 100,000 in receivables might receive AED 95,000 upfront, with the provider collecting directly from customers.

MCAs do not rely on invoices and instead pull directly from card sales, making them more appropriate for retail, hospitality, and other card-heavy businesses.

Though many financing options may appear similar, merchant cash advances offer a distinct set of benefits for businesses with consistent card-based sales.

When an MCA Makes Sense for Your Business

Merchant cash advances provide businesses with immediate access to working capital while aligning repayments with actual revenue. This adaptive structure offers several distinct advantages for companies that rely on consistent card-based sales.

1. Fast Access to Capital

MCAs allow businesses to obtain funds quickly, often within 24 to 72 hours, without the lengthy approval processes of traditional loans.

For example, a retail business in Dubai requiring AED 100,000 for seasonal stock can receive the advance almost immediately, ensuring operations continue without disruption. Repayments adjust automatically to daily or weekly sales, reducing the strain on cash flow during slower periods.

2. Funding for Multiple Operational Needs

Funds from an MCA can be applied flexibly across business requirements, including working capital, equipment purchases, inventory management, or expansion projects.

For instance, a UAE-based café may use an MCA to purchase new coffee machines or remodel a space while covering short-term payroll. The versatility of MCAs makes them suitable for urgent or planned expenditures without waiting for revenue accumulation.

3. Flexible Repayment Structure

Unlike fixed monthly instalments, MCAs link repayment to sales performance. A business experiencing a surge in transactions will clear the advance more quickly, while slower sales naturally extend the repayment period. This ensures that repayments remain proportional to revenue, helping businesses maintain operational stability and avoid overextension.

Once you receive your MCA funds, manage every dirham effortlessly with Alaan’s corporate cards. Set custom spend limits, control vendor payments, and monitor all transactions in real time. Book a demo today to streamline your MCA spending.

[cta-1]

How Merchant Cash Advances Work

The procedure for a merchant cash advance (MCA) differs from other financing options. Unlike traditional loans or lines of credit, MCAs link approval and repayment directly to a business’s card sales. Here is a typical workflow:

1. Application and Approval Flow

Approval for an MCA is generally faster than traditional bank loans due to the criteria underwriters use. Providers primarily review:

- Card processing history: volume and consistency of card sales.

- Point-of-sale (POS) statements: verifying daily or weekly transaction flow.

- Bank statements: confirming overall revenue patterns.

Documentation requirements are typically straightforward, because the underwriting focuses on actual sales performance rather than credit score alone, approval can often be granted within 24 to 72 hours.

2. Funding and Payout Timeline

Once approved, funding is usually disbursed quickly. Typical timelines in the UAE range from one to five business days, depending on factors such as:

- Verification of sales and bank account information.

- The provider’s internal processing speed.

- Seasonal or unusual fluctuations in transaction volumes.

Quick disbursement ensures businesses can address urgent operational needs, such as inventory replenishment or short-term payroll.

3. Repayment Mechanics: Holdback and Settlement

Repayment occurs through a holdback, a fixed percentage of daily or weekly card receipts automatically deducted by the provider. Key points include:

- Sales-dependent repayment: higher sales accelerate repayment; slower periods extend it.

- Cashflow impact: for instance, an AED 50,000 advance with a 15% holdback on daily card receipts of AED 5,000 results in AED 750 daily repayment, adjusting naturally as revenue fluctuates.

- Seasonal considerations: businesses with seasonal peaks may repay faster during high-sales months and slower during low-sales periods, without additional fees.

Next, we’ll break down how to calculate the total cost of an MCA and what repayments could look like for your business.

How to Calculate the Costs of a Merchant Cash Advance

Before committing to a Merchant Cash Advance, it’s crucial to estimate the total cost so you can evaluate if it fits your business’s fast-funding needs. Let’s work through a practical example.

Suppose your business takes an AED 120,000 advance with a factor rate of 1.35. The total repayment would be:

120,000 × 1.35 = AED 162,000

This means your total fee is AED 42,000.

Your daily or monthly repayment depends on your sales volume. Here’s a breakdown for monthly card sales of AED 40,000, AED 70,000, and AED 90,000, assuming a holdback of 12% and a 30-day month:

Key Takeaways for Your Business:

- Slower sales stretch repayment but keep short-term cash flow manageable.

- Faster sales clear the advance sooner but increase the effective cost, impacting short-term profitability.

Are MCAs a Funding Shortcut or Long-Term Strain?

Merchant cash advances can either support growth or create challenges, depending on how your business manages them. This practical assessment helps businesses map whether an MCA aligns with their operational and cash flow realities.

When an MCA Can Boost Your Business

MCAs are best suited for businesses that:

- Have predictable card-based revenue to ensure repayments align naturally with sales.

- Require short-term capital for urgent operational needs or temporary cashflow gaps.

- Value speed and simplified underwriting, with approval based on transaction history rather than credit score.

When MCAs Can Backfire on Cash Flow

Businesses should consider potential downsides and cashflow implications:

- Higher effective cost: Factor rates often exceed traditional loan interest, increasing total repayment.

- Frequent repayment deductions: Daily or weekly holdbacks can reduce liquidity and strain cash flow.

- No reduction for early repayment: Paying off the advance early does not lower the total owed.

- Complex contract terms: Some MCA agreements contain clauses that may be difficult to interpret.

- Revenue volatility risk: Businesses with inconsistent sales may face extended repayment periods, impacting operational stability.

Evaluating the advantages and risks of MCAs naturally raises the question: which types of businesses are best positioned to benefit from this financing model?

Which Businesses Are Suitable Candidates for MCA?

Not all businesses are suited for merchant cash advances. The ideal candidates are companies with predictable, card-based, or digital spend, multiple teams or projects, and operational structures that allow repayments to align with revenue flows.

1. Retail, Hospitality, and Other Card-Heavy Operations

E-commerce, retail, and logistics firms and other card-heavy operations are ideal candidates for MCAs because their revenue largely comes from frequent, card-based transactions.

This predictable cash flow allows providers to calculate holdbacks accurately and ensures repayments are aligned with actual sales.

Key metrics to evaluate suitability in these sectors include:

- Card-sales share percent: A higher proportion of revenue from card payments ensures predictable repayment. Typically, businesses with 60% or more card-based revenue are better positioned.

- Average ticket size: Consistent transaction amounts make it easier for providers to determine appropriate holdback percentages.

- Daily or weekly transaction volume: Regular transaction activity supports timely repayment and reduces cash flow disruption.

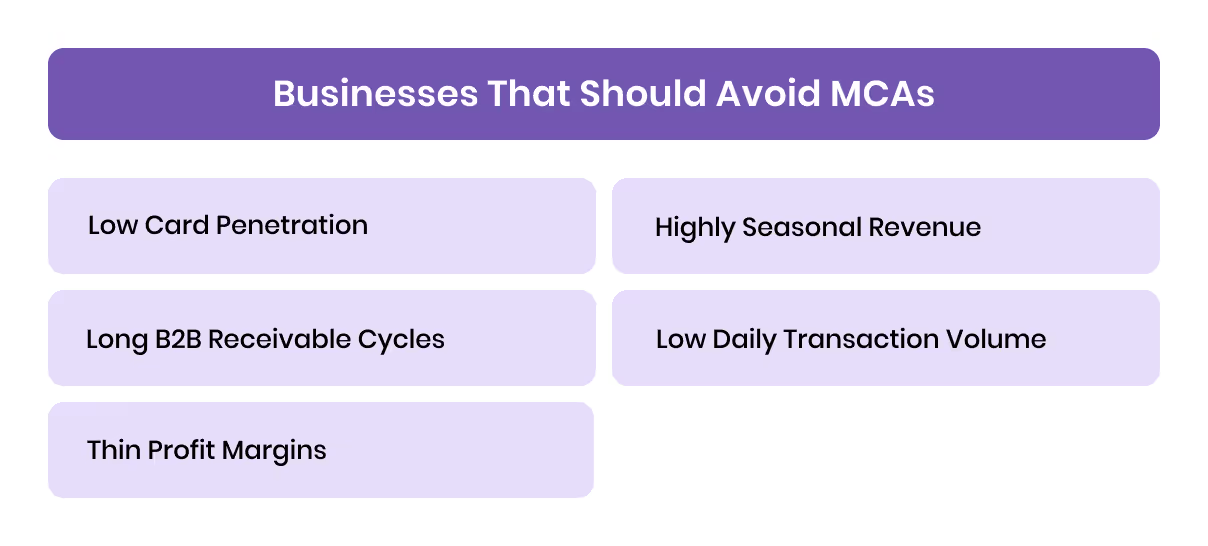

Businesses That Should Avoid MCAs

Certain profiles face a higher risk and may find MCAs unsuitable:

- Low card penetration: Predominantly cash-based operations create unpredictable repayment.

- Long B2B receivable cycles: Businesses dependent on delayed invoices cannot align with daily or weekly holdbacks.

- Thin profit margins: High repayment percentages can strain operations.

- Highly seasonal revenue with extreme peaks and troughs: Repayment can become difficult during low-sales periods.

- Low daily transaction volume: Infrequent card sales limit provider confidence and may increase costs.

MCAs are best suited for corporate spend-heavy, multi-team, or project-focused businesses with consistent card or digital transaction volumes. Evaluating whether your organisation meets these criteria helps ensure that funding will address cashflow needs effectively without creating repayment pressure.

The next step is to review the application process for a Merchant Cash Advance, including eligibility requirements, necessary documentation, and what to expect during underwriting.

How to Apply for a Merchant Cash Advance

The MCA application process is structured around corporate transaction patterns rather than collateral or traditional credit scores. Businesses that maintain predictable card or digital payment volumes can often complete underwriting and receive funding faster than with conventional loans.

Eligibility and Required Documents

Providers typically assess eligibility based on consistent digital or card-based transactions and financial statements. Common documentation includes:

- Corporate card or digital transaction statements: POS, payment gateways, or ERP transaction logs.

- Bank statements: Usually covering the past 3–6 months to verify cash inflows.

- Revenue reports: Demonstrating predictable monthly or project-based sales.

- Business registration and operating license: To confirm compliance with UAE or regional regulations.

- Existing financial obligations: Any active loans, lines of credit, or VAT filings.

What to Expect During Underwriting

Providers focus on cash flow reliability and transaction history rather than credit scores or collateral. Typical checks include:

- Processor statements: Assess daily/weekly card or digital transactions.

- Bank statements: Verify consistent inflows and operational liquidity.

- Chargeback or refund analysis: High dispute rates may affect holdback percentages.

- Revenue stability and seasonality: Determine repayment alignment with actual inflows.

Pro tip: Preparing clean, up-to-date statements and highlighting predictable revenue streams significantly accelerates underwriting and increases approval chances.

Even though the MCA application process is straightforward, these advances carry interest. High interest rates, variable repayment tied to card transactions, and potential cash flow strain mean that MCAs may not suit every business.

Depending on your operations, revenue patterns, and financial priorities, there are other funding options available.

4 Smarter Alternatives to High-Cost Merchant Cash Advances

If an MCA is not ideal for your business, there are several financing methods in the UAE that can provide capital with different risk, cost, and repayment profiles. These options offer more predictable cash flow management and may align better with seasonal or recurring revenue models.

1. Revenue-Based Financing

Revenue-based financing allows businesses to secure funds and repay them as a percentage of ongoing revenue. Repayment adjusts automatically with sales, making it suitable for companies with predictable card-based transactions or recurring revenue. This method aligns funding costs with performance, offering flexibility during slow or seasonal periods.

2. Business Lines of Credit

A business line of credit provides revolving access to funds that can be drawn as needed. Repayments are typically interest-based and flexible within the credit limit. This option is ideal for businesses with recurring working capital requirements, enabling them to manage cash flow gaps without committing to a lump-sum advance.

3. Invoice Financing

Invoice financing enables companies to convert outstanding invoices into immediate cash. This method is particularly useful for businesses with long B2B payment cycles, as it provides liquidity while awaiting client payments.

Funds are typically advanced against approved invoices, allowing operations to continue smoothly without waiting for receivables.

4. Term Loans

Term loans are structured financing solutions with fixed repayment schedules over a predetermined period. These are generally suited for larger, long-term investments, providing predictability and stability for capital-intensive projects.

Repayment amounts and terms are agreed upon upfront, offering businesses a clear path for financial planning.

Choosing the right funding option depends on your business model, cash flow patterns, and operational priorities. While MCAs provide fast, flexible funding, alternatives can deliver better alignment with business needs and transaction structures.

Step-By-Step Checklist: Should You Take an MCA Today?

Deciding whether a Merchant Cash Advance is the right option requires evaluating your business against clear operational and financial criteria. Use this checklist to assess suitability quickly.

- Does your business generate regular credit or debit card sales as a primary revenue source?

- Is your cash flow seasonal or unpredictable, creating short-term funding gaps?

- Have you been operating for at least six months with stable monthly revenue?

- Do you require quick access to capital for urgent operational needs?

- Can your business handle variable repayments tied directly to daily or weekly card transactions?

- Are traditional bank loans or lines of credit unavailable, slow, or unsuitable for your needs?

- Are your profit margins sufficient to absorb the higher costs associated with MCAs?

- Are you prepared for automatic deductions from sales without early repayment benefits?

If you decide that a Merchant Cash Advance is the right move, having total control over how the funds are spent becomes critical. This is where a unified spend management platform can help you track every dirham, enforce limits, and maintain compliance effortlessly.

Optimise Your MCA with Alaan

Merchant Cash Advances provide quick capital, but tracking and controlling the use of these funds can be challenging.

Alaan acts as a central dashboard for MCA spending, combining smart corporate cards, automated expense management, and real-time analytics to ensure businesses maintain visibility, compliance, and control over every dirham spent. At Alaan, we deliver this through our integrated corporate cards and spend management platform.

Key Features for MCA Management:

- Corporate Cards Built for Visibility and Control: Prepaid corporate cards let businesses load MCA funds in advance, eliminating overspending risks and interest charges from traditional credit cards. Finance teams can set custom limits, apply vendor-specific restrictions, and instantly block or freeze cards if required.

- Smart Receipt Automation: Employees can snap receipts, and Alaan’s OCR links them to the correct transaction, simplifying reporting of MCA funds.

- Built-In Spend Controls: Set custom limits, vendor restrictions, and approval workflows to prevent overspending from MCA disbursements.

- Budget Management: Allocate MCA funds to departments, projects, or teams, enforcing limits on where and how the money can be used.

- Smooth ERP Integration: MCA-related expenses automatically flow into accounting systems, like QuickBooks Online, Xero, Oracle NetSuite, Microsoft Dynamics 365, Odoo, SAP, and Zoho Books, maintaining accurate ledgers and VAT documentation.

- Built-In Compliance and Audit Trail: Every MCA transaction includes receipts, notes, and approvals, making audits straightforward and reducing policy violations.

- AI-Powered Insights: Alaan monitors MCA spending patterns, flags unusual activity, and provides actionable analytics to optimise cash flow.

- Spend insights and instant savings: Alaan's dashboards reveal spending trends, vendor costs, and areas for potential savings. Businesses also earn up to 2% cashback on eligible international transactions, turning everyday spending into tangible savings.

Explore Alaan today to manage your MCA funds with full visibility and control. Track expenses, enforce limits, and simplify reconciliation for smarter spending.

Conclusion

Merchant Cash Advances provide businesses with fast, flexible access to capital, but they come with trade-offs that may affect cash flow and repayment. Evaluating your business profile, revenue patterns, and funding needs is essential before opting for an MCA.

At Alaan, we simplify spend management through AI-backed automation, smart corporate cards, and centralised dashboards. Teams gain real-time visibility, reduce errors, and optimise cash flow without relying solely on short-term advances. To see how your business can maintain control while funding operational needs, schedule a free demo.

FAQs

1. What is a Merchant Cash Advance (MCA)?

A Merchant Cash Advance is a financing solution where a business receives a lump sum upfront and repays it through a percentage of future credit or debit card sales. Unlike traditional loans, repayment adjusts to actual sales volume.

2. How fast can a business receive MCA funding?

Funding timelines typically range from a few days to a week, depending on transaction history, underwriting, and provider efficiency. The process is generally faster than bank loans due to minimal collateral requirements.

3. Which businesses are most suitable for MCAs?

MCAs are best for businesses with consistent card-based sales, seasonal or fluctuating revenue, and urgent short-term working capital needs, such as retail stores, restaurants, e-commerce, and service providers.

4. What are the risks of taking an MCA?

MCAs can strain cash flow if sales drop or fluctuate unexpectedly. They often come with higher overall costs compared to traditional loans, and early repayment may not reduce fees. Businesses with thin margins or low card sales may face high repayment pressure.

5. Are MCAs the only option for short-term capital in the UAE?

No. Alternatives include business loans, revenue-based financing, invoice financing, term loans, and modern corporate card solutions with expense management platforms, such as Alaan, which provide real-time control and visibility over operational spending.