If you manage accounts payable, you know that paying too quickly can strain cash flow, while paying too slowly can hurt supplier relationships. Without solid data, you’re flying blind. The accounts payable turnover ratio gives you the metrics to balance cash preservation with strong vendor partnerships.

This metric shows how often a company settles supplier invoices in a given period. It is calculated by dividing total credit purchases (or COGS) by average accounts payable, a simple formula that reveals discipline in payment practices and the health of supplier relationships.

In this blog, we will cover how to calculate the ratio, read benchmarks across industries, and apply practical ways to improve results, especially for businesses in the UAE and wider MENA region seeking tighter financial control.

Key Takeaways

- Calculation Methods of AP Turnover Ratio: The ratio can be calculated using Net Credit Purchases ÷ Average Accounts Payable for accuracy or COGS ÷ Average Accounts Payable when credit purchase data is unavailable.

- Pros and Cons of High Ratio: Signals operational efficiency, automation, and timely payments; risks include cash strain, reduced liquidity, and masking other inefficiencies.

- Pros and Cons of Low Ratio: Indicates slower payments, which may aid liquidity or strategic negotiations; risks include late fees, strained supplier relationships, and operational bottlenecks.

- Limitations and Considerations: Differences in industry norms, accounting practices, timing, and strategic payment decisions can impact the ratio’s relevance.

- How to Increase Accounts Payable Turnover Ratio: Focus on faster payments, prioritise critical suppliers, automate AP workflows, and use analytics to optimise cash flow and strengthen vendor relationships.

- How to Lower Accounts Payable Turnover Ratio: Strategically extend payment terms, consolidate supplier accounts, monitor cash flow, and balance outflows to preserve liquidity while maintaining supplier trust.

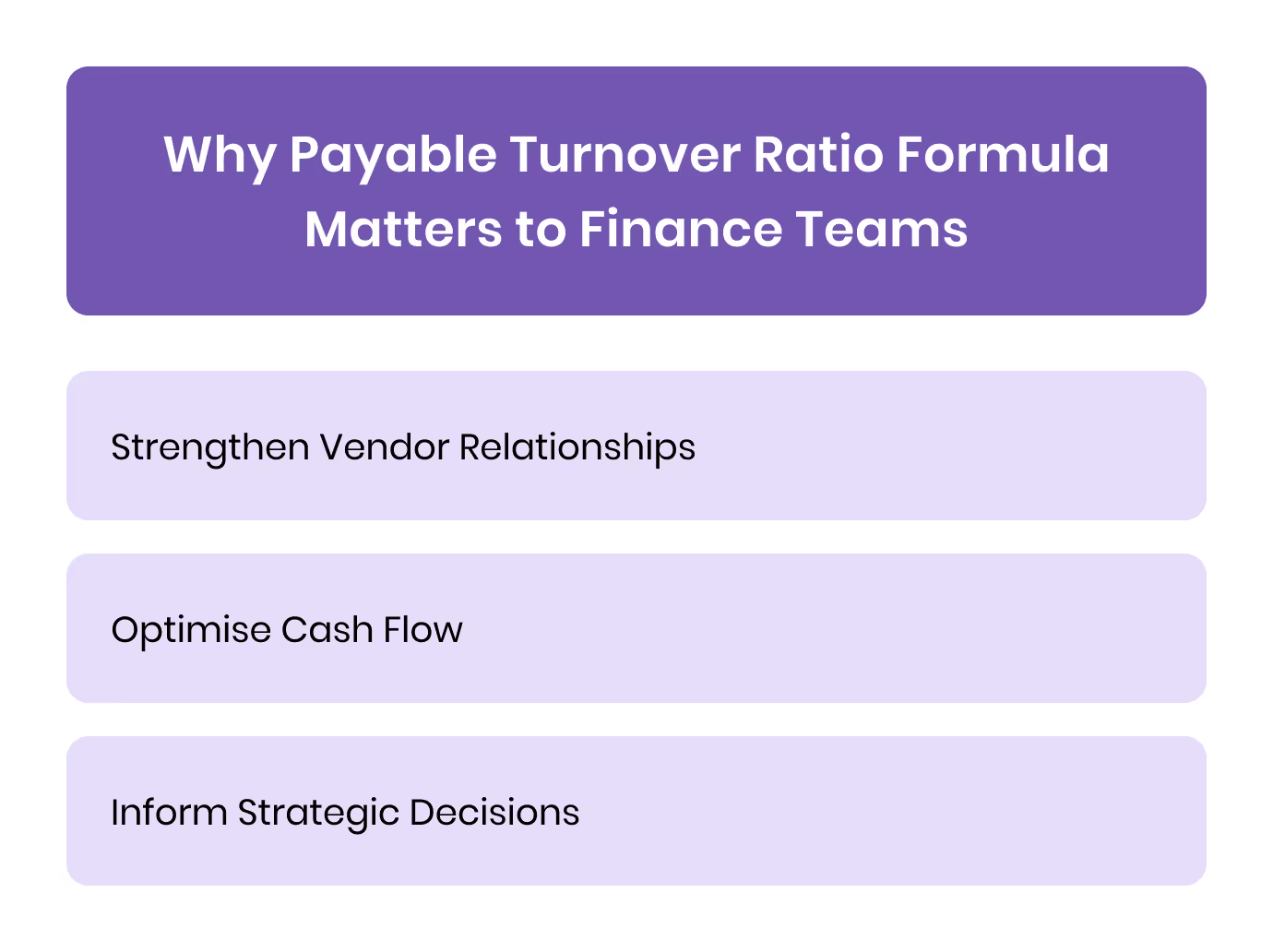

Why Payable Turnover Ratio Formula Matters to Finance Teams

It highlights the speed of payments, reveals cash flow trends, and reflects working capital management. High or low ratios send clear signals about a company’s financial discipline and its ability to maintain strong supplier relationships.

Finance managers and CFOs monitor payable turnover to:

- Strengthen Vendor Relationships: Regular, timely payments build trust and can unlock discounts or priority fulfilment.

- Optimise Cash Flow: Identifying whether outflows are too fast or too slow helps prevent liquidity issues while maintaining cash flow stability.

- Inform Strategic Decisions: Comparing turnover ratios across periods or peers provides insight for negotiating supplier terms or adjusting payment cycles.

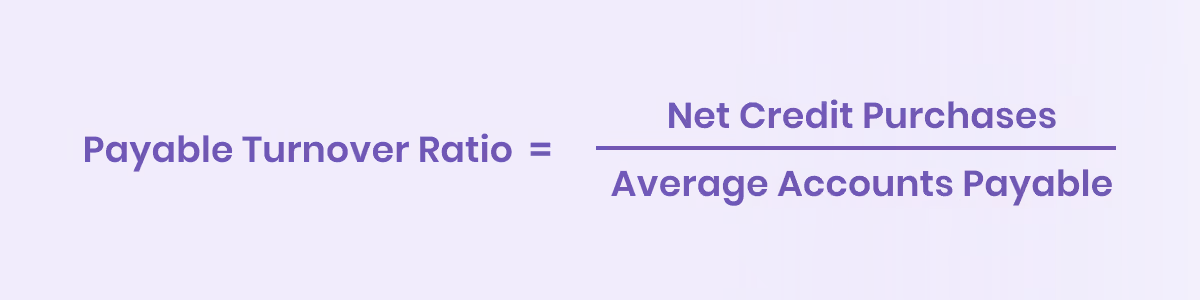

Standard Formula:

- Net Credit Purchases ÷ Average Accounts Payable: Preferred method, aligning with international accounting standards.

- COGS ÷ Average Accounts Payable: Acceptable when credit purchase data is unavailable, though slightly less precise.

How to Calculate Payable Turnover Ratio with Examples

Depending on data availability and reporting standards, there are two accepted methods for calculating the payable turnover ratio.

Method-1

This is the preferred method, as it aligns with international accounting and auditing standards and provides the clearest view of supplier obligations.

There are two components to this formula:

- Net Credit Purchases: The total value of purchases made on credit during the accounting period, excluding cash purchases.

- For SaaS businesses: credit purchases typically include cloud hosting, software subscriptions, and licensing fees.

- For manufacturers, it covers raw materials and production inputs.

- For retailers, it includes inventory purchased for resale.

- Average Accounts Payable: The average balance a company owes to suppliers over the reporting period. It is calculated as:

This figure shows the typical level of unpaid obligations a business carries at any point in time.

Example: If your business reports AED 2,400,000 as the Net Credit Purchases and AED 600,000 as Average Accounts Payable, you can calculate your accounts payable turnover ratio with this formula:

2,400,000 ÷ 600,000 = 4

This means the company pays its suppliers four times per year, roughly once every three months.

Accounts Payable Turnover in Days

The accounts payable turnover in days indicates the average number of days a company takes to pay its suppliers. It is calculated by dividing 365 days by the payable turnover ratio:

Payable Turnover in Days = 365 ÷ Payable Turnover Ratio

Using the earlier example:

Payable Turnover in Days = 365 ÷ 4 = 91.25

This means the company takes approximately 91 days to pay its suppliers, or roughly once every three months.

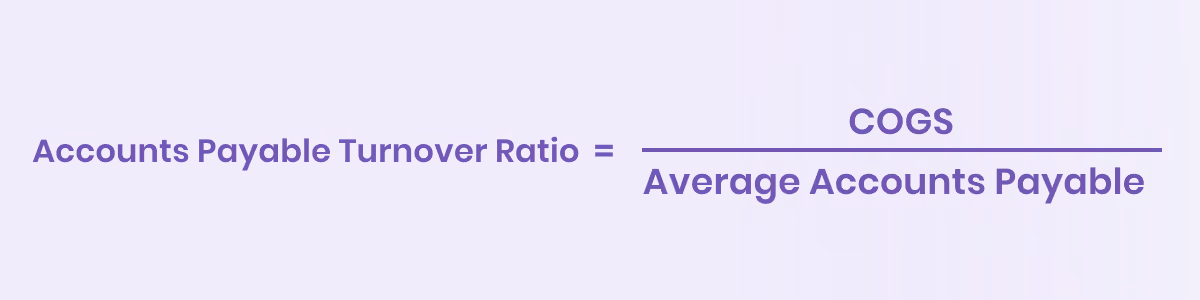

Method-2

This is permissible when net credit purchases are unavailable. While practical, it may provide a slightly less precise picture of actual payables, especially if cash purchases or indirect costs are significant.

COGS represents the direct costs incurred to produce or purchase the goods that a company sells during a specific period. This includes expenses such as raw materials, manufacturing costs, and supplier costs directly tied to products, but excludes indirect overheads like marketing or administrative expenses.

Example:

- COGS: AED 2,500,000

- Average Accounts Payable: AED 625,000

So, as per the accounts payable turnover ratio formula, this is how you calculate:

2,500,000 ÷ 625,000 = 4

The ratio is similar to the net credit purchases method in this case, showing payment frequency, but minor differences may appear in businesses with mixed payment types.

Adjusted Calculations for Accuracy

Finance teams in the UAE and MENA often operate with seasonal spikes or irregular purchasing cycles. To refine the payable turnover ratio for more actionable insights, they can apply the following adjustments:

- Seasonal Adjustments: For businesses with fluctuating expenses (e.g., retail during Ramadan), calculate turnover per active season to avoid skewed annual ratios.

- Incorporating Purchases Instead of COGS: When indirect costs or large cash purchases exist, using total purchases ÷ average AP can provide a more precise reflection of payables cycles.

Example (Seasonal Adjustment):

- Q4 Purchases: AED 1,200,000

- Average AP in Q4: AED 300,000

Adjusted Turnover Ratio: 1,200,000 ÷ 300,000 = 4 for Q4 alone, highlighting faster payments during peak operations.

Key Takeaways:

- Use Net Credit Purchases ÷ AP for accurate, standards-aligned reporting.

- Use COGS ÷ AP when credit purchase data isn’t available, but note potential deviations.

- Apply seasonal or purchase adjustments to gain more actionable insights and informed decision-making.

Once finance teams calculate the payable turnover ratio, the next critical step is interpreting what the number actually means for the business.

Also Read: What are Accounts Payable and Accounts Receivable?

How to Interpret Payable Turnover Ratio?

The payable turnover ratio offers a window into a company’s payment practices and financial health. High, low, or average values can have very different implications depending on the sector, payment terms, and operational dynamics.

There’s no single ‘correct’ accounts payable turnover ratio. A high ratio indicates fast payments and strong controls, while a low ratio reflects slower payments and potential liquidity management. Finance teams should aim for a balance that maintains healthy supplier relationships without unnecessarily tying up cash.

Industry benchmarks can help guide what’s reasonable, for example, technology or SaaS companies often target higher ratios due to predictable cash flows, whereas retail businesses may operate with slightly lower ratios to preserve liquidity

1. High Ratio

A high or rising turnover ratio shows the company is paying suppliers more quickly. A short-term spike could mean excess cash on hand or supplier demands for faster payment. Over time, an increasing ratio may indicate effective management of payables and cash flow, though it could also suggest the company isn’t reinvesting funds into other parts of the business.

Advantages:

- Signals efficient payables management and strong operational discipline.

- May enhance supplier confidence, unlocking early-payment discounts or preferential terms.

- Shows that finance teams have effective control over cash outflows, enabling better strategic planning.

- Often indicates automation or streamlined AP processes, which reduce manual errors and save time.

Risks:

- Rapid payments may tie up funds that could otherwise support operational needs or strategic investments, especially during a high-expense period

- Suppliers may not offer discounts if they see payment speed as excessive, reducing strategic leverage.

- It can limit short-term liquidity for other strategic investments, tying up cash unnecessarily.

- May mask underlying inefficiencies elsewhere, such as slow collections or overstocked inventory, hidden by fast payments.

2. Low Ratio

A low or declining turnover ratio means the company is taking longer to pay its suppliers. A sudden drop could signal cash shortages or disputes with vendors. Over time, a gradual decline might reflect negotiated payment terms or deliberate cash management strategies rather than operational issues.

Implications:

- Indicates slower payment cycles, which may be intentional to retain cash longer.

- Can signal liquidity issues, operational inefficiencies, or delayed invoice processing.

- May serve as a strategic negotiation tool with vendors, but risks straining supplier relationships.

- Highlights potential bottlenecks in AP processes that could be improved with automation.

Risks:

- Slower payments may damage vendor relationships, leading to stricter terms or delays.

- Can signal inefficient internal processes, such as delayed approvals or manual reconciliations.

- It could create a false sense of liquidity, masking the need for better cash flow planning.

- Might reduce supplier confidence in long-term partnerships, affecting procurement flexibility.

High or low payable turnover ratios provide signals, but several contextual factors can affect their accuracy and comparability. Finance teams should consider these factors to make informed decisions, rather than relying solely on the ratio.

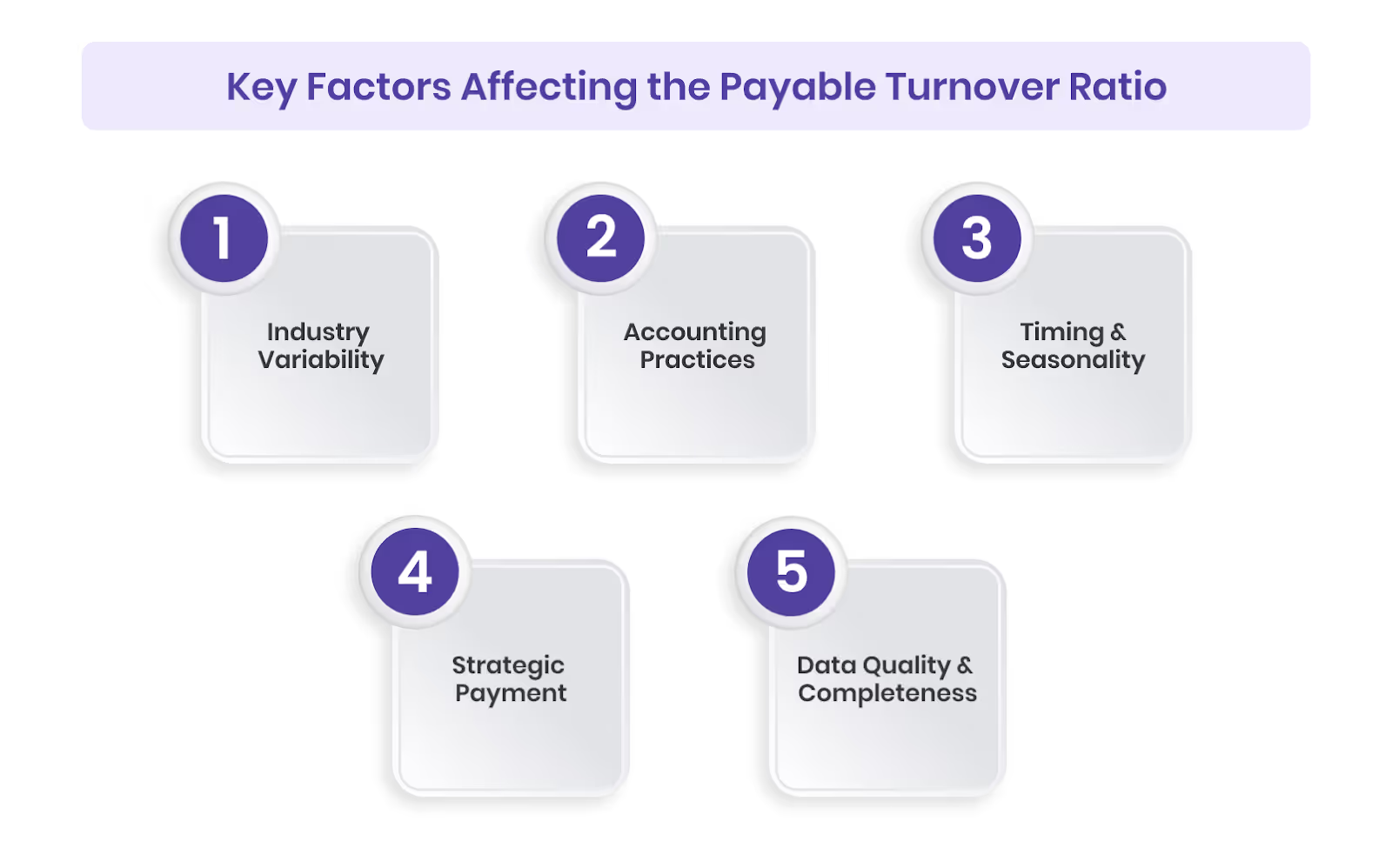

Key Factors Affecting the Payable Turnover Ratio

The payable turnover ratio provides useful insights into supplier payments and cash flow, but several factors can skew its interpretation or limit comparability across businesses. Finance teams should account for these nuances to ensure accurate analysis and informed decisions.

- Industry Variability

- Benchmarks differ across sectors. What is considered healthy for a technology firm may be unusually high for retail or professional services.

- Seasonal businesses, like retail during holiday peaks, may see temporary spikes or dips in payables that distort annual ratios.

- Comparing ratios without considering industry norms can mislead decision-making, potentially prompting unnecessary operational changes.

- Accounting Practices

- Differences in how companies record purchases, COGS, and AP can significantly affect the ratio. For example, some firms include indirect costs or accruals, while others track only direct supplier invoices.

- Manual vs. automated AP processes can also impact average AP calculations, influencing the turnover ratio.

- Finance teams should align calculations and clarify assumptions when benchmarking internally or against peers.

- Timing and Seasonality

- Payment cycles and purchase patterns fluctuate throughout the year. Calculating a ratio over a full year without considering seasonal trends can mask cash flow pressures in specific periods.

- Quarterly or monthly breakdowns can provide a more precise view of operational efficiency and liquidity needs.

- Strategic Payment Decisions

- Companies may intentionally delay payments to manage working capital, which can lower the ratio without indicating inefficiency.

- Conversely, aggressive early payments can inflate the ratio while tying up cash that could be invested elsewhere. Finance teams should interpret the ratio alongside broader cash management strategies.

- Data Quality and Completeness

- Incomplete or inaccurate AP records, missing invoices, or misclassified transactions can distort the ratio.

- Implementing AP automation and real-time dashboards helps ensure reliable calculations, improving the usefulness of the metric.

With these limitations in mind, finance teams can adopt targeted strategies to optimise the payable turnover ratio, improve cash flow, and strengthen supplier relationships.

How to Increase Your Accounts Payable Turnover Ratio

Speeding up your AP turnover ensures timely payments, strengthens supplier relationships, and reflects payment cycle consistency. Finance teams can implement the following strategies:

- Timely Invoice Approvals: Reduce bottlenecks by setting clear approval workflows for faster payment processing.

- Use Automation: Implement automation for the invoice process to reduce errors and ensure consistency.

- Prioritise Critical Suppliers: Pay essential suppliers first to maintain strong relationships and secure favourable terms.

- Leverage Early-Payment Discounts: Take advantage of discounts for faster payments without harming cash flow.

- Corporate Cards for Controlled Payments: Utilise corporate cards offered by Alaan to track transactions and integrate with expense management systems.

- Monitor with Real-Time Dashboards: Track payments and trends to avoid delays and optimise working capital.

[cta-5]

How to Lower Your Accounts Payable Turnover Ratio

Slowing down AP turnover can preserve cash and optimise liquidity without damaging supplier trust. Consider these approaches:

- Negotiate Longer Payment Terms: Extend supplier payment cycles strategically to free up cash.

- Consolidate Supplier Accounts: Reduce multiple accounts to increase leverage and simplify AP management.

- Adjust Vendor Segmentation: Delay payments for less critical suppliers while maintaining timely payments for key vendors.

- Schedule Payments Strategically: Align payments with cash inflows to avoid liquidity pressure.

- Forecast Cash Flow: Plan outgoing payments to safely extend cycles without risking late fees or strained supplier relationships.

While these steps help optimise your payable turnover, using an AI-powered spend management platform such as Alaan can make execution faster, more accurate, and fully automated.

Streamline Accounts Payable and Expense Management with Alaan

Alaan goes beyond traditional AP and invoice tools by providing a unified, AI-powered spend management platform. Finance teams can save time, reduce errors, and gain real-time visibility across all business expenses.

How Alaan Helps:

- Complete Expense Visibility: Track every business expense in one place for accurate, real-time financial oversight.

- AI-Powered Data Capture: Upload receipts or invoices via mobile app or Chrome extension, and let Alaan automatically extract key details like TRN and vendor information.

- Smart Analytics for Spend Control: Gain actionable insights into spending trends to optimise costs.

- Custom Approval Workflows: Set approval flows for teams or individuals, ensuring compliance with company policies.

- Built-in Card Controls: Establish spending limits and restrictions to prevent overspending.

- Time and Cost Savings: Automate invoice processing and approvals, freeing 16+ hours per month and cutting processing costs.

- Error Reduction: Automated checks and validations minimise costly mistakes and ensure accuracy.

[cta-4]

Get started with Alaan and transform your accounts payable, invoice management, and overall expense workflows with a reliable, scalable, and AI-driven solution that adapts to your business needs.

Conclusion

Optimising the payable turnover ratio formula is crucial for businesses looking to maintain healthy cash flow, strengthen supplier relationships, and improve operational efficiency.

Manual accounts payable processes slow down payments, increase errors, and obscure visibility into company expenses. Automation provides a streamlined approach, allowing finance teams to process invoices faster, enforce approval workflows, and gain actionable insights in real time.

With Alaan, businesses can automate their AP processes, control spending, and track every transaction in one unified platform. Book a free demo today and start leveraging AI-powered expense management to save time, reduce errors, and optimise your payable turnover ratio with precision.

FAQ About Payable Turnover Ratio Formula

1. What is the payable turnover ratio formula?

The standard formula is Payable Turnover Ratio = Cost of Goods Sold ÷ Average Accounts Payable, though some firms use Net Credit Purchases ÷ Average Accounts Payable for greater accuracy. It measures how often a company pays its suppliers over a period.

2. Why use Net Credit Purchases instead of COGS?

Net Credit Purchases align with international accounting standards and provide a more precise view of supplier obligations. COGS can be used if credit purchase data is unavailable, but it may slightly under- or overstate payables efficiency.

3. How does the ratio impact cash flow management?

A higher ratio indicates faster supplier payments, which can enhance vendor relationships but reduce cash on hand. A lower ratio may improve liquidity, but risk late fees or strained supplier terms.

4. Are there industry benchmarks for the payable turnover ratio?

Yes. Technology and SaaS companies often have ratios between 6–8, retail or e-commerce around 4–6, and professional services 3–5, reflecting sector-specific payment practices and operational cycles.

5. How can businesses improve their payable turnover ratio?

Strategies include negotiating payment terms, automating AP processes, monitoring cash flow, and implementing approval workflows. Using AI-powered expense management platforms like Alaan can further streamline payables and optimise the ratio.