As per the FTA guidelines, registered businesses can claim an input tax credit against VAT paid on the purchase of eligible products and services. However, there are certain expense categories where claiming input VAT is not possible, and these are classified as Non-Recoverable Input VAT in the UAE.

Understanding this concept is critical for accurate tax filing and avoiding penalties from the Federal Tax Authority (FTA). By recognising different expenses that fall under this category, you can effectively manage your cash flow and optimise your VAT claims.

This blog covers different supplies ineligible for input VAT credit, the process to handle such purchases, and answers important questions related to non-recoverable input VAT in the UAE. Keep reading to know more.

What is non-recoverable input VAT?

In the UAE's VAT system, registered enterprises have the option to recover the VAT paid on purchases used to make taxable supplies. This provision allows you to offset the tax paid for business purchases against the VAT charged for your sales. As a result, your overall tax burden and the amount to be remitted to the government is reduced.

However, there are certain exceptions where the VAT you have paid cannot be claimed. This can happen in two situations:

- The nature of the expense: Some expenses, like entertainment expenses in the UAE, are non-recoverable by nature, regardless of their use in the business.

- The use of the expense: In some cases, the specific use of an otherwise-recoverable expense can result in the VAT becoming non-recoverable. For instance, if you purchase a company car and allow employees to use it for personal reasons, then the VAT on that purchase might be non-recoverable.

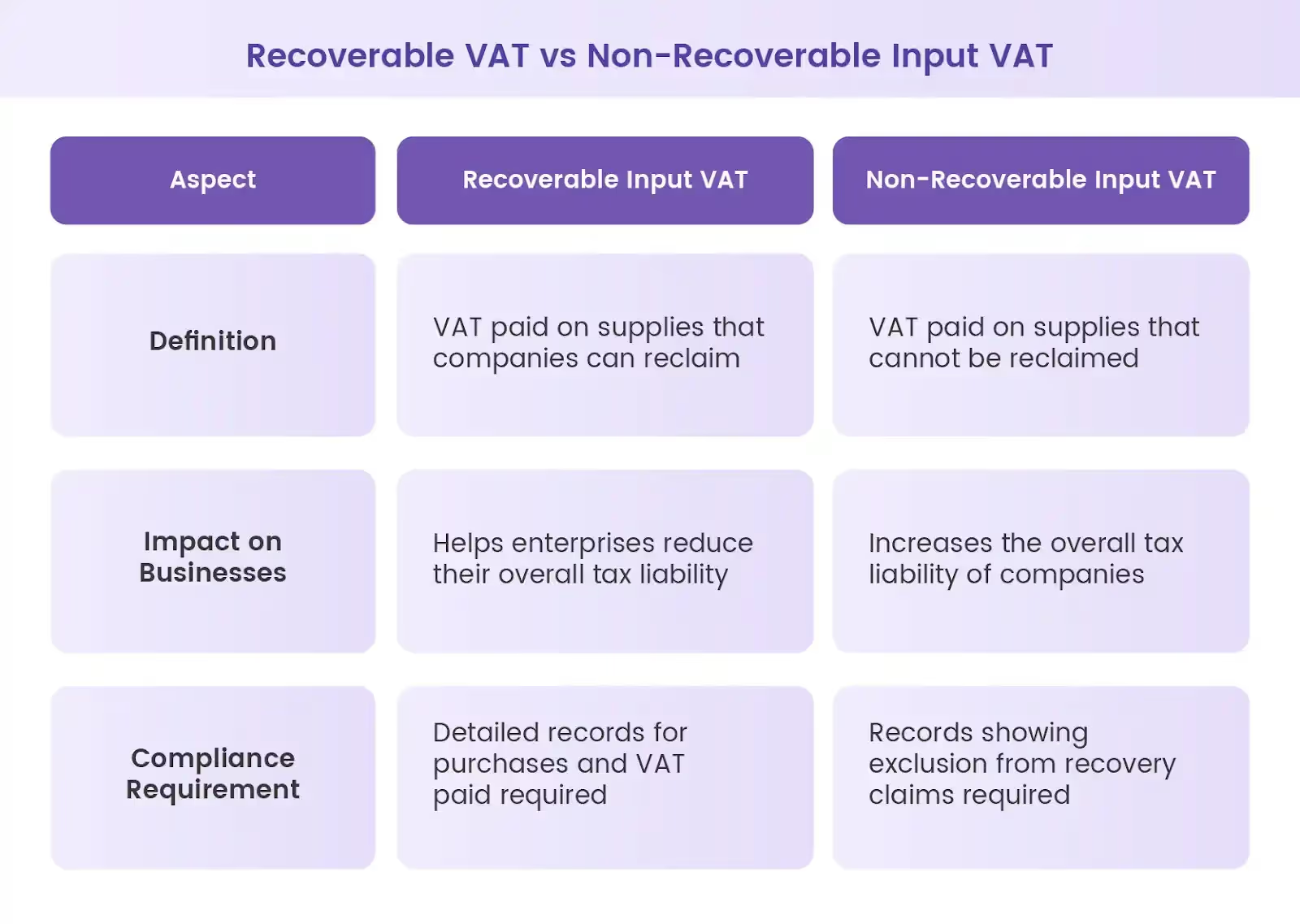

Recoverable vs. non-recoverable VAT

The key difference between recoverable and non-recoverable VAT lies in your ability to claim the input credit.

Recoverable VAT allows you to reduce your tax liability by claiming an input credit on your VAT return. On the other hand, non-recoverable VAT becomes part of your overall business expense and cannot be offset against your output VAT.

What supplies are not eligible for input VAT recovery?

As per the Federal Decree Law No. (8) of 2017, certain supplies are not eligible for recoverable input tax. Here are important details related to such supplies:

1. Entertainment services and VAT

According to the UAE VAT rules, taxes paid on entertainment expenses are non-recoverable. This expenditure could include extravagant meals, tickets to sports events, or fun activities for employees or clients.

The rule is also applicable to the costs linked with offering hotel accommodation services, food, and drinks that are not typically part of a business meeting. However, there are certain exceptions:

- If you offer entertainment services that are part of a contractual obligation, the VAT may be recoverable.

- Any food and drinks that you offer during the normal course of business meetings as a basic courtesy would not be considered entertainment services. For example, if lunch is served to potential customers after the meeting and at the same venue, it would not be considered an entertainment expense. However, as a general rule, the cost of the lunch must be similar to standard employee meal allowances.

2. Personal use of vehicles and VAT

As per the UAE VAT Law, the term motor vehicle refers to a road vehicle meant for the conveyance of 10 or fewer persons, including the driver. This definition excludes vehicles like a truck, forklifts, hoists or other similar vehicles.

The VAT treatment for company vehicles depends on their usage:

- Used for business purposes: If the company car is used exclusively for business purposes, you can claim the VAT on its purchase and maintenance expenses (like fuel and occasional servicing).

- Used for personal tasks: But if the motor vehicle purchased for business purposes is used by employees to run personal errands, VAT paid is not recoverable.

There are a few exceptions where the vehicle used for your company will not be treated as available for personal use:

- Licensed taxis: Taxis licensed by a competent authority within the UAE qualify for full VAT recovery on purchase or lease, even with some personal use.

- Emergency vehicles: Registered emergency vehicles used by police, fire departments, ambulances, or similar services can claim the full VAT on purchase or lease, regardless of minor personal use.

- Rental vehicles: Vehicles used in a car rental business and rented out to customers allow for full VAT recovery on purchase or lease, even if there's some internal company use.

3. Employee Expenses and VAT

According to UAE VAT rules, the tax paid on goods or services purchased for use by employees, for which they have paid no charges, is not recoverable. This means that if you incur expenses for the personal benefit of employees, the VAT paid on these expenditures cannot be claimed. For instance, if you provide complementary gym memberships to your employees for their fitness needs, the VAT paid on these memberships is not recoverable.

There are exceptions to this rule. If the services or goods have been purchased to be used by employees for no charge but are directly related to the business, the VAT may be recoverable, such as:

- Legally mandated benefits: If you have a legal obligation to provide certain goods or services under the UAE or Designated Zone labour laws, the input VAT on these expenses can be recovered.

- Contractual or documented policy: You can claim VAT on expenses mentioned in a contract or documented company policy that helps employees perform their duties.

- Deemed supplies: In some scenarios, the provision of goods or services to employees might be considered a deemed supply under the UAE VAT laws. In such situations, your company can be eligible for input VAT recovery.

How to handle non-recoverable input VAT?

Here are some important tips to handle non-recoverable input VAT in the UAE to ensure compliance with the FTA guidelines:

- Monitor Non-recoverable Expenses: Implement a system to categorise and track non-recoverable expenses. Analyse this data regularly to identify areas where you can potentially reduce these costs. For example, you can explore alternative transportation solutions for employees and avoid personal usage of company vehicles.

- Review VAT Efficiency Regularly: Schedule periodic reviews of your VAT processes, including non-recoverable expenses. This allows you to identify areas for improvement and ensure you are adhering to the VAT laws.

- Automate Processes: Consider implementing a spend management platform like Alaan that offers automated VAT calculations and categorisation features. This can streamline your bookkeeping process and reduce the risk of human error when dealing with non-recoverable VAT.

- Stay Updated on VAT Regulations: VAT rules in the UAE are updated periodically. Subscribe to updates from the FTA to stay notified about any developments that can have an impact on your non-recoverable input VAT calculations.

- Maintain Records for Audits: Always retain proper documentation for all your purchases, including invoices and receipts. This is essential for supporting your VAT claims and avoiding potential penalties during FTA audits.

Enhance VAT reporting with Alaan

Navigating the complexities of VAT reporting and ensuring FTA compliance can be daunting. However, with Alaan's spend management solutions, you can effectively streamline your VAT reporting process, ensuring accuracy and compliance.

1. Automate VAT calculation

One of the key features of Alaan's spend management solution is the ability to automate VAT calculations. The system can be configured to apply the correct VAT rate to each purchase, and it can automatically calculate the VAT owed on each invoice. This lowers the human error risk and ensures consistency in your VAT calculations, reducing the chance of penalties from the FTA.

2. Ensure VAT compliance

Alaan keeps you VAT compliant by categorising your expenses according to their VAT treatment (e.g., exempt, zero-rated, standard). This clear categorisation makes it easy to identify recoverable input VAT and non-recoverable input VAT, simplifying your VAT return preparation.

3. Facilitate VAT reclaims

It also helps you maintain a clear audit trail of all VAT transactions and maximise your VAT reclaim opportunities. With all your invoices stored in a central location, you can easily access them for record-keeping and reclaim purposes. This eliminates the need for maintaining physical copies and simplifies the process of VAT reconciliation.

Want to understand how Alaan can ease your VAT reporting better? Connect with the experts at Alaan to know more!