Accounts receivable sits at the heart of most business balance sheets, yet it remains one of the most misunderstood financial concepts among executives.

A common misconception is treating AR as a cost centre or liability, rather than recognising it as an asset. This misunderstanding leads companies to list AR on their financial statements without fully reflecting its role in the business. As a result, businesses fail to accurately track expected cash inflows, creating a flawed picture of their cash flow.

This blog will clarify why AR is classified as a current asset, rather than a revenue or liability. We also highlight why AR matters beyond the balance sheet and how optimising it can strengthen cash flow and financial decision-making.

Key Takeaways

- Revenue vs. Accounts Receivable: Revenue is recognised at the point of sale, while AR tracks unpaid amounts; understanding this distinction prevents reporting errors.

- Accounts Receivable vs. Liabilities: AR increases liquidity and working capital, whereas liabilities reflect obligations that decrease cash availability.

- Why AR Tells You More Than Just Assets: AR signals cash flow health, customer reliability, and financial risks, providing leaders with actionable insights beyond its balance sheet value.

- Accounting Automation: Automating AR processes reduces errors, improves collections, and provides real-time visibility into cash flow.

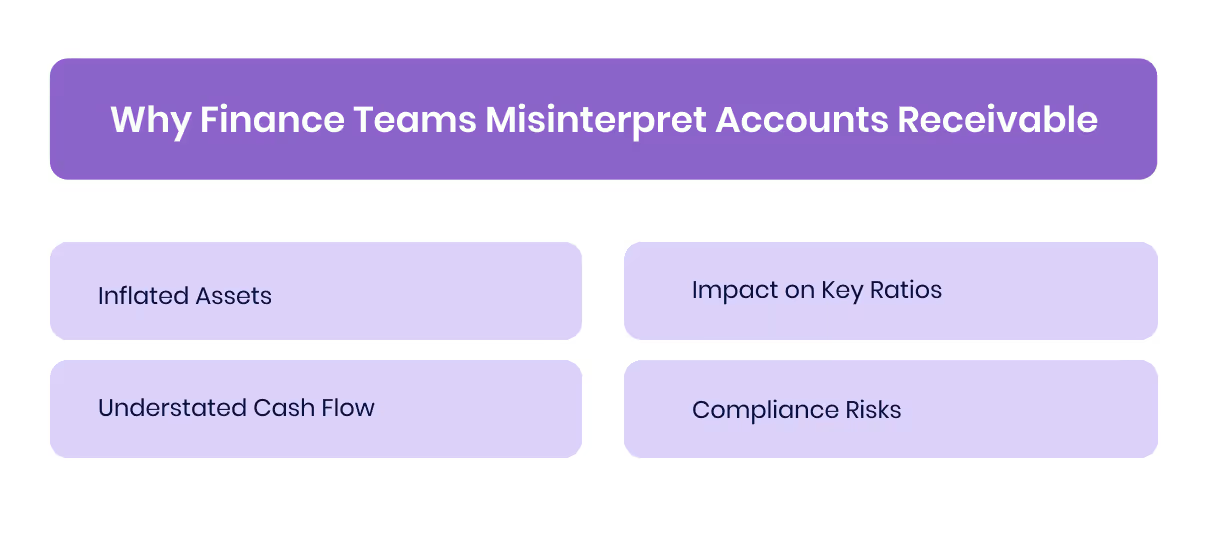

Why Finance Teams Misinterpret Accounts Receivable

Even for experienced finance managers, accounts receivable (AR) can be deceptively complex. Its confusion often stems from its dual nature: AR is directly linked to revenue, yet sits on the balance sheet as a current asset.

This confusion isn’t theoretical, it has real consequences:

- Inflated Assets: Overstating AR can make working capital appear stronger than it is, masking cash shortages and creating poor liquidity planning.

- Understated Cash Flow: If AR is miscalculated or ignored, businesses may misjudge expected cash inflows, leading to delayed payments, missed opportunities, or unnecessary borrowing.

- Impact on Key Ratios: AR miscalculations affect working capital ratios, current ratios, and Days Sales Outstanding (DSO). For example, an overstated AR inflates the current ratio, giving a false sense of liquidity.

- Compliance Risks: Incorrect AR reporting can result in errors in financial statements, triggering audits or regulatory scrutiny.

[cta-6]

So, what exactly is accounts receivable, and how can it be efficiently accounted for? Let’s explore its classification, treatment on financial statements, and practical strategies for managing AR effectively.

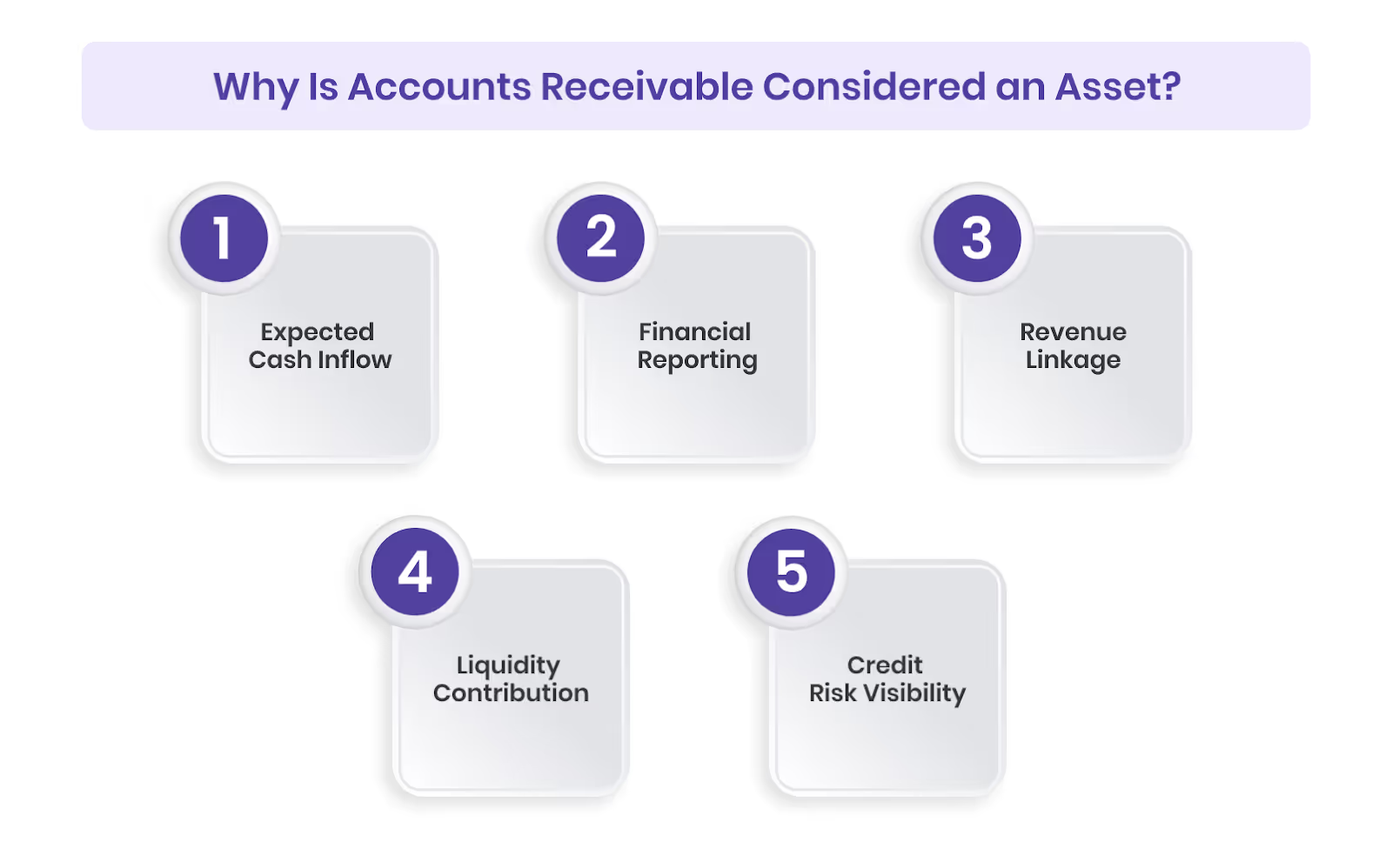

Why Is Accounts Receivable Considered an Asset?

Accounts receivable (AR) is classified as an asset because it represents a claim to future cash from customers for goods or services already delivered, providing measurable economic value to the business. Several factors explain why AR holds this asset status:

- Expected cash inflow: AR is anticipated to convert into cash within the company’s operating cycle, making it a tangible resource.

- Financial reporting relevance: Properly recorded AR ensures the balance sheet reflects the company’s short-term financial position accurately.

- Revenue linkage: AR corresponds to revenue recognised under accrual accounting, keeping revenue and receivables aligned.

- Liquidity contribution: AR provides insight into the company’s cash flow expectations, supporting working capital management.

- Credit risk visibility: Tracking AR allows businesses to monitor customer payment behaviour and assess potential collection challenges.

Classifying AR as an asset explains its place on the balance sheet, but the bigger question is whether it counts as revenue, because that distinction shapes how growth and performance are measured.

Do Accounts Receivable Count as Revenue?

While accounts receivable is linked to revenue, AR itself is not revenue. Under accrual accounting, revenue is recognised at the point of sale, while AR tracks the unpaid portion until payment is received.

When a sale is made on credit, revenue is recorded on the income statement, and AR is recorded on the balance sheet at the same time. This ensures both earned revenue and expected cash inflows are reflected accurately.

To clarify the difference, the following table highlights how accounts receivable and revenue are recorded and treated in financial statements.

Accounts Receivable vs. Liabilities

Accounts receivable (AR) and liabilities represent opposite sides of a company’s finances. While AR is an asset reflecting amounts owed to the business, liabilities are obligations the business owes to others, such as accounts payable (AP).

AR boosts short-term liquidity, whereas liabilities indicate cash obligations that must be planned for to maintain solvency.

Also Read: What are Accounts Payable and Accounts Receivable?

How Receivables Shape Your Balance Sheet and Income Statement

Accounts receivable (AR) plays a crucial role in financial reporting, primarily appearing on the balance sheet and indirectly linked to revenue on the income statement. Understanding its presentation ensures an accurate reflection of liquidity and earned income.

1. AR in Balance Sheet

- Classification: AR is recorded as a current asset because it is expected to convert into cash within the operating cycle, typically within 12 months.

- Impact on liquidity: Including AR in current assets provides a clear picture of the company’s short-term cash inflows and overall working capital.

2. AR in Income Statement

- AR does not appear directly: Only the revenue from sales is recognised on the income statement under accrual accounting. AR represents the portion of that revenue not yet collected in cash.

- Revenue recognition link: When a sale is made on credit, revenue is recognised immediately, and AR tracks the corresponding amount owed until payment is received.

Practical Examples with Journal Entries

Example 1: Sale on Credit (AED 50,000)

Example 2: Customer Payment (AED 50,000)

These journal entries illustrate the dual impact of AR on financial statements: revenue is recorded immediately, while AR reflects the future cash inflow, keeping both the balance sheet and the income statement aligned.

Why Accounts Receivable Tells You More Than Just Assets

Accounts receivable (AR) is more than a line item on your balance sheet; it’s a window into the financial health and strategic performance of your business.

For finance leaders, AR provides insight into cash flow health, customer payment behaviour, and financial risk.

1. AR as an Early Warning System for Cash Flow

Even if revenue looks strong, delayed or ageing receivables can signal potential liquidity pressures. Rising AR balances without corresponding cash inflows reduce operational flexibility, limiting the ability to invest in growth, pay suppliers, or respond to unexpected expenses.

Leaders who monitor AR closely gain foresight into cash shortages and can proactively adjust working capital or financing strategies, avoiding costly last-minute fixes.

2. What AR Ageing Reveals About Customer Health

The composition of AR tells a story about your customers’ reliability and financial stability. Receivables consistently ageing beyond agreed terms may indicate stressed or high-risk clients.

This insight allows leaders to intervene timely: tightening credit policies, renegotiating payment terms, or prioritising collections from at-risk customers to protect the company’s cash position and maintain predictable cash flow.

3. How AR Quality Affects Valuation, Credit, and Investor Trust

Investors, lenders, and board members scrutinise receivables closely. High-quality, collectable AR signals a healthy sales model and effective credit management. Conversely, overstated or uncollectible AR raises red flags, potentially lowering company valuation, complicating fundraising, or increasing borrowing costs.

4. Why Mismanaging AR Distorts the Real Financial Picture

Mismanaged AR can mislead leadership about both liquidity and profitability. Inflated receivables make working capital appear stronger than it is, while underreported AR hides potential cash inflows, skewing forecasts.

Accurate tracking and proactive management of AR provide a true picture of financial health, enabling more precise strategy and risk mitigation.

How to Optimise Accounts Receivable Accounting

A common mistake is assuming that recording accounts receivable (AR) completes the accounting process. In practice, optimising AR requires continuous monitoring, timely follow-ups, and accurate reconciliation. Poorly managed AR can silently inflate books, reduce liquidity, and distort financial decision-making.

Automation corrects this by creating a streamlined, end-to-end process for AR accounting:

- Automated invoicing: Invoices are generated and shared instantly after a credit sale, ensuring no receivable slips through the cracks.

- Smart reminders: Customers receive scheduled alerts for upcoming and overdue payments, reducing manual follow-ups.

- Real-time visibility: Dashboards display the current AR balance, ageing reports, and cash inflow forecasts, giving finance teams a clear view of what’s collectable and when.

- Error reduction: Automated reconciliation minimises mismatches between customer payments and ledger entries, strengthening the accuracy of financial statements.

- Streamlined collections: By flagging overdue accounts and integrating with payment gateways, automation speeds up recovery without adding extra steps.

Instead of operating in the dark with outdated spreadsheets, businesses gain accurate, up-to-date insights into who owes what, how long payments have been pending, and the realistic cash position. This visibility empowers leadership to make informed decisions on working capital, credit policies, and growth investments.

[cta-5]

Wrapping Up

Accounts receivable is often misunderstood. Some mistake it for revenue, while others confuse it with liabilities. In reality, AR represents a current asset, a claim to future cash that strengthens liquidity only when collected. Recognising this distinction is key to accurate accounting and better cash flow management.

But the cycle doesn’t end when customers pay. Once cash hits your account, the next challenge is managing how that money is spent. This is where a spend management solution becomes essential.

Alaan is built for this purpose. As the leading spend management platform in the Middle East, Alaan offers an AI-powered system that complements your AR optimisation. By automating expense processes, providing real-time spend oversight, and integrating seamlessly with accounting systems, finance teams gain full visibility and save significant time on manual reconciliations.

[cta-4]

With corporate cards, Alaan helps companies manage both cash inflows and outflows efficiently, creating a complete approach to cash flow management.

If you’re ready to strengthen your financial control from receivables to expenses, schedule a free demo of Alaan today and see how it can transform your cash flow management.

FAQs About Accounts Receivable

1. What is the difference between accounts receivable and revenue?

Accounts receivable (AR) is the amount a business is owed by customers for goods or services delivered on credit. Revenue is the income recognised at the time of the sale under accrual accounting, regardless of whether cash has been received. AR reflects the unpaid portion of revenue and appears on the balance sheet as a current asset; revenue appears on the income statement.

2. Is accounts receivable a liability or an asset?

Accounts receivable are an asset. It represents a claim to future cash from customers and is listed as a current asset on the balance sheet because it's expected to convert into cash within the normal operating cycle. It is not a liability, which refers to obligations a business owes to others.

3. How are accounts receivable and accrued revenue different?

Accrued revenue refers to income earned for work performed or goods delivered that have not yet been invoiced, while accounts receivable refers to amounts owed once an invoice has been issued. Both are assets, but accrued revenue precedes invoicing, whereas AR follows invoicing. Misclassifying them can lead to timing errors in financial statements.

4. Why doesn’t accounts receivable appear on the income statement directly?

Because accounts receivable is an asset, not income. Revenue (income) is recognised when the sale occurs under accrual accounting; AR is simply the unpaid portion of that revenue, which will convert to cash later. The income statement records revenue and expenses, whereas the balance sheet tracks AR and other assets.

5. Can expenses reduce accounts receivable, or are they separate?

Expenses do not reduce accounts receivable. Accounts receivable is a claim to cash (an asset), while expenses are costs incurred by the business and are reflected on the income statement. Only if a receivable becomes uncollectible (bad debt) will you debit a bad debt expense and reduce AR, but that’s a special case, not a regular expense transaction.