Even a single VAT compliance lapse can saddle a UAE company with fines of AED 1,000–AED 10,000 or more, putting cash flow and profitability under pressure.

Under the UAE’s B2B VAT rules, businesses whose taxable supplies exceed AED 375,000 must register with the Federal Tax Authority (FTA) within 30 days of crossing that threshold or face penalties such as AED 10,000 for late registration.

Once registered, companies must file VAT returns on time, where late submission can trigger fines of AED 1,000 for the first offence and AED 2,000 for repeat offences within 24 months, and ensure invoices meet strict FTA requirements to avoid AED 5,000 penalties per incorrect invoice.

For finance leaders working under the UAE’s tax environment, mastering these rules is essential not only to sidestep penalties but also to protect working capital, maintain supplier trust, and ensure audit readiness.

This blog discusses the core B2B VAT rules in the UAE, explains registration and documentation requirements, highlights common compliance pitfalls, and offers clear guidance to help your team stay compliant with confidence.

Key Takeaways

- B2B VAT compliance in the UAE is invoice-driven; without FTA-compliant tax invoices, input VAT recovery is legally lost.

- Reverse Charge Mechanism errors are among the most common B2B failures, especially for imported services and overseas vendors.

- VAT risk grows with transaction volume; manual processes do not scale with modern procurement or card-based spending.

- Penalties are operational, not theoretical; late returns, missing invoices, and incorrect reporting trigger fixed fines.

- Embedding VAT controls at the point of spend is more effective than correcting errors during month-end reconciliation.

What Are B2B VAT Rules in the UAE?

B2B VAT rules in the UAE govern how VAT applies when one VAT-registered business supplies goods or services to another business. These rules are defined under Federal Decree-Law No. 8 of 2017 on VAT and enforced by the Federal Tax Authority (FTA).

At their core, B2B VAT rules determine when VAT should be charged, who accounts for it, and how it must be reported.

A transaction is treated as B2B for VAT purposes when:

- Both the supplier and the customer are businesses

- The supply is made in the course of business

- The customer is either VAT-registered or required to be VAT-registered in the UAE

In most domestic B2B transactions, VAT is charged at the standard rate of 5 percent, unless a zero-rate or exemption applies.

Not all B2B transactions follow the standard charging model. Special rules apply in cases such as:

Also Read: How To File VAT Returns in the UAE?

Now that the foundation of B2B VAT is clear, the next step is understanding how these rules differ from B2C VAT and why that distinction directly affects pricing, cash flow, and compliance obligations.

How B2B VAT Differs from B2C VAT in the UAE

While both B2B and B2C transactions fall under the UAE VAT framework, the tax treatment, recovery rights, and compliance impact differ significantly. Misunderstanding this distinction is a common source of VAT errors for growing businesses.

- In B2B transactions, VAT is usually recoverable by the buyer as input VAT

- In B2C transactions, VAT is a final cost borne by the consumer

This distinction affects how businesses price their products and services and manage working capital.

One of the most critical differences lies in VAT recovery:

As B2B VAT compliance becomes more digital and tightly regulated, the UAE is moving away from manual processes toward a fully automated tax environment.

UAE VAT in 2026: E-Invoicing and What Changes for B2B

From 2026 onward, the UAE will begin rolling out a mandatory e-invoicing framework for B2B transactions, fundamentally changing how VAT is recorded, reported, and audited. This reform is designed to give the Federal Tax Authority near real-time visibility into business transactions and reduce VAT leakage across the economy.

E-invoicing does not mean sending PDFs by email. It requires invoices to be:

- Created in a structured digital format (such as XML or JSON)

- Transmitted through an approved digital reporting framework

- Validated and stored in a way that allows real-time or near real-time access by tax authorities

With VAT enforcement becoming more real-time and system-driven, registration is no longer a formality; it is the legal gateway to participating in the UAE’s B2B economy.

VAT Registration in the UAE: When and How B2B Rules Apply

Under UAE law, VAT registration determines whether you are legally allowed to charge VAT, recover input VAT, and participate in compliant B2B transactions.

Mandatory registration applies if taxable supplies or imports exceed AED 375,000 over 12 months or the next 30 days; voluntary from AED 187,500. Free zone firms register like the mainland unless designated exempt. Non-residents register without a threshold for UAE supplies. FTA processes online via the EmaraTax portal in 20 working days.

Step-by-step registration:

- Create EmaraTax account at tax.gov.ae with Emirates ID/email.

- Submit Taxable Person Registration Form (TPRF): trade license, passport copies, bank details, and turnover proof.

- Get a 15-digit TRN upon approval, display on all B2B invoices.

Here’s the detailed overview of the registration threshold:

Once your business is registered, compliance moves from theory to execution. Every B2B transaction now carries a legal obligation: issuing a VAT-compliant tax invoice that can withstand FTA scrutiny.

B2B Tax Invoices in the UAE: What the Law Requires

UAE VAT law demands full tax invoices for all B2B supplies over AED 10,000 or to registered buyers. A tax invoice is the legal record that allows your customer to reclaim VAT and enables the FTA to verify your reporting. For B2B transactions, invoices must meet strict content and timing standards under the VAT Executive Regulations.

A valid B2B tax invoice must be issued within 14 days of the date of supply and include specific information.

Required fields on every B2B invoice must show:

- "Tax Invoice" marked at the top in bold

- Supplier full name, address, 15-digit TRN

- Buyer's full name, address, and TRN (if registered)

- Unique sequential invoice number (e.g., INV-2026-0001)

- Invoice issue date + supply date (if different)

- Precise goods/services description per line item

- Quantity, unit price (ex-VAT), line total

- VAT rate (5% standard), VAT amount, total payable

- Any discounts/credits applied pre-VAT

If any of these elements are missing or incorrect, the buyer’s input VAT claim may be rejected, and the supplier may face penalties.

A compliant invoice is only half the equation. The real financial impact of VAT in B2B transactions lies in whether that tax can be recovered.

Recovering Input VAT: What UAE Businesses Can and Cannot Claim

Input VAT is the VAT your business pays on goods and services purchased for commercial use. Under UAE VAT law, VAT-registered businesses can reclaim this amount, provided strict conditions are met. This recovery mechanism is what keeps VAT neutral between businesses when it works correctly.

Input VAT can be recovered only when all three conditions are satisfied:

- The expense is incurred wholly or partly for business purposes

- The supply is taxable (standard-rated or zero-rated)

- A valid tax invoice or import document is held

If any of these are missing, the FTA may deny the claim.

Businesses can usually reclaim VAT on:

- Office rent and utilities

- Professional services (legal, audit, consulting)

- Software and IT tools

- Marketing and advertising

- Business travel directly related to work

These costs are considered directly linked to taxable business activity.

Input VAT recovery assumes that your supplier charges VAT correctly. However, in certain B2B scenarios, UAE law shifts that responsibility to the buyer. This is where many businesses make costly reporting mistakes.

Reverse Charge Mechanism (RCM) in B2B Transactions

The Reverse Charge Mechanism (RCM) applies when the obligation to account for VAT moves from the supplier to the buyer. In B2B transactions, this typically occurs when a UAE business purchases goods or services from a non-UAE supplier that is not VAT-registered in the country.

Instead of paying VAT to the supplier, the UAE buyer must:

- Calculate the VAT due on the transaction

- Declare it as output VAT in their VAT return

- Claim the same amount as input VAT (if eligible)

This results in a net-zero cash impact when handled correctly, but only if it is reported accurately.

The most frequent use case is imported services, for example, paying a foreign SaaS provider, legal firm, or marketing agency.

Once VAT is charged, recovered, or self-accounted under reverse charge, it must be formally reported. This is where many businesses slip, because VAT compliance ultimately lives or fails in the return.

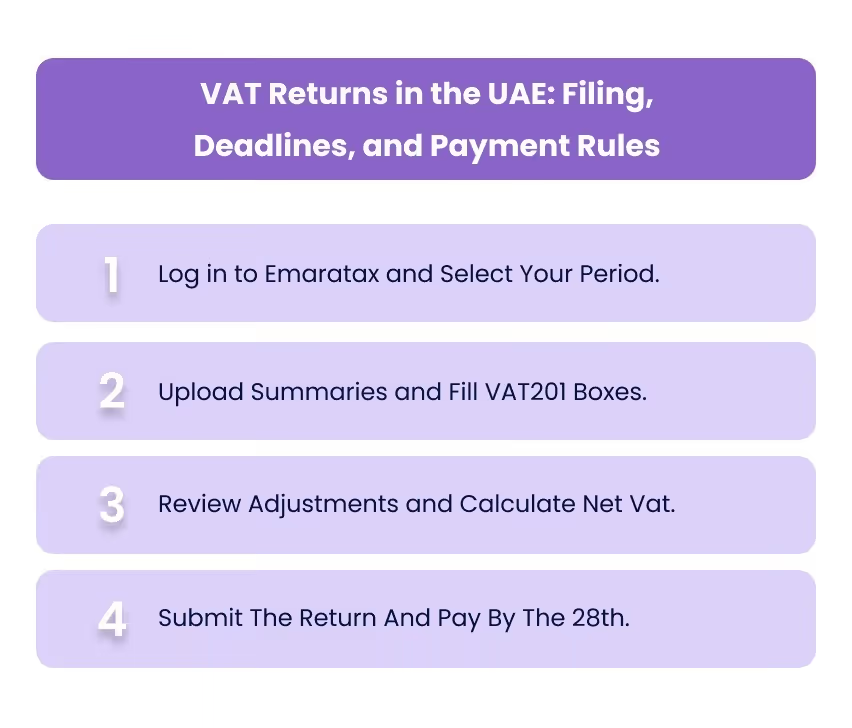

VAT Returns in the UAE: Filing, Deadlines, and Payment Rules

Every VAT-registered business in the UAE is required to submit VAT returns through the Federal Tax Authority portal for each assigned tax period. These returns consolidate all VAT activity, sales, purchases, imports, and reverse-charge transactions into a single legal declaration.

Here's the complete 4-step filing process explained simply:

Step 1: Log in to Emaratax and Select Your Period.

Go to tax.gov.ae, enter your username and password to access EmaraTax. Pick the exact tax period you need to report, like "Q1 2026" if filing for January to March. The system shows your previous filings to avoid mistakes.

Step 2: Upload Summaries and Fill VAT201 Boxes.

Upload your sales and purchase summary reports in Excel or CSV format, which list all invoices with VAT amounts. Then enter key figures: Box 1 holds standard sales VAT at 5%, Box 10 captures Reverse Charge output VAT you owe as buyer, and Box 12 shows recoverable input VAT from valid supplier invoices. Double-check totals match your records.

Step 3: Review Adjustments and Calculate Net Vat.

Scan for FTA debits, prior adjustments, or penalties added automatically. The portal calculates your net VAT due: output tax minus input recovery. If inputs exceed outputs, you get a credit to carry forward or claim as a refund later.

Step 4: Submit The Return And Pay By The 28th.

Click submit to lock the return; FTA reviews within days. Pay any amount owed through bank transfer or debit from your tax account. Keep the payment receipt and confirmation email for 5 years.

Also Read: Advantages of VAT in the UAE for Growth and Cash Flow

Even businesses that understand VAT rules can still incur penalties when controls break down. Most fines in the UAE are not the result of intentional non-compliance; they stem from timing gaps, manual errors, and overlooked obligations.

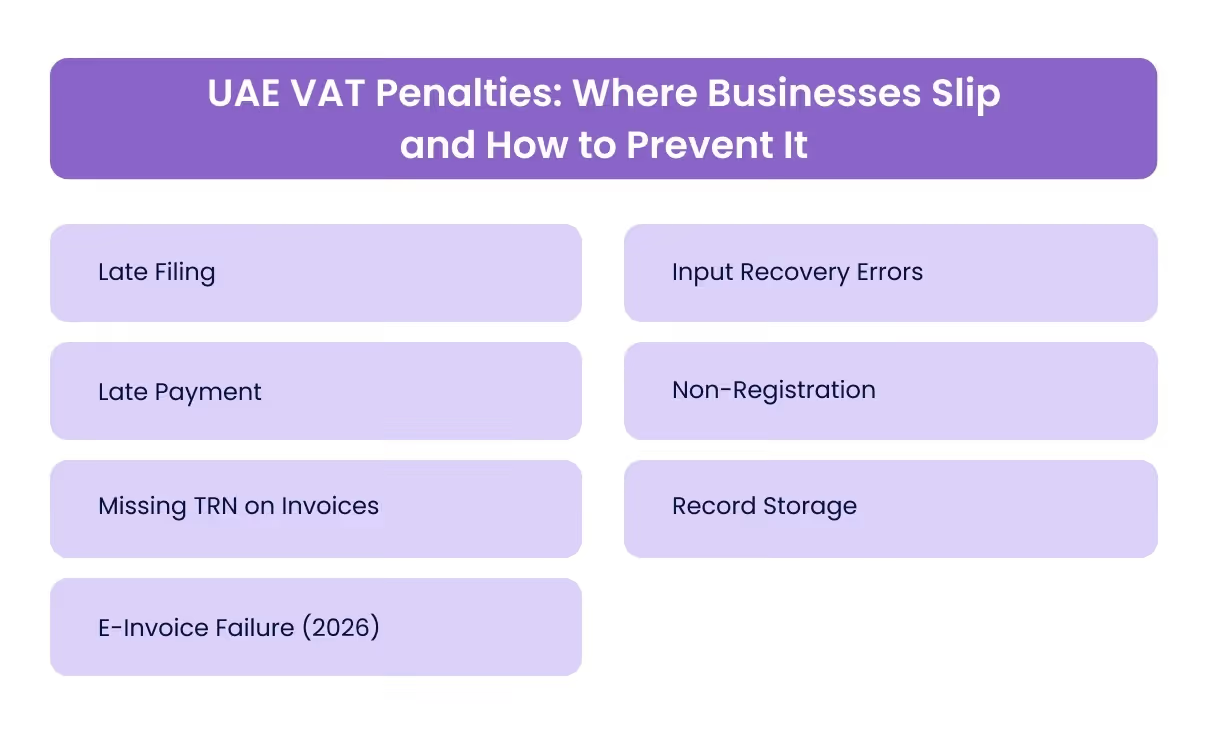

UAE VAT Penalties: Where Businesses Slip and How to Prevent It

The Federal Tax Authority applies fixed and escalating penalties across the VAT lifecycle, from registration to invoicing and return filing. These penalties are triggered automatically through system checks and audits.

Here top 7 penalties and their fixes:

- Late Filing: Pay AED 1,000 for the first offence or AED 2,000 for repeats within 24 months. Set calendar reminders 10 days before the 28th deadline.

- Late Payment: Face 2% monthly interest on unpaid VAT, capped at 100% of the amount due. Authorize automatic debit from your tax account each period.

- Missing TRN on Invoices: Incur AED 1,000–5,000 fine per invoice without Tax Registration Number. Add a template checklist before sending any B2B invoice.

- E-Invoice Failure (2026): Get AED 10,000 for non-issuance or AED 20,000 for validation errors. Test full Peppol integration during the Q1 2026 pilot phase.

- Input Recovery Errors: Lose 100% of the claim plus 50% penalty on incorrect amounts. Match every input invoice to bank payment records monthly before filing.

- Non-Registration: Owe AED 10,000 plus all back VAT when turnover exceeds AED 375K unregistered. Track weekly turnover through ERP dashboard alerts.

- Record Storage: Pay an AED 5,000 fine for each missing year of documents during audit. Set cloud backups with an automatic 5-year retention policy active now.

After understanding edge cases, cross-border rules, and penalty-heavy scenarios, one reality becomes clear: B2B VAT compliance in the UAE is not a once-a-month task. It is a continuous operational discipline.

How Alaan Simplifies B2B VAT Compliance

Alaan is the #1 spend management platform in the Middle East. It helps businesses issue corporate cards, control spending, and automate receipts through a single AI-powered system. For VAT, Alaan moves compliance out of spreadsheets and after-the-fact reconciliation, and into the moment a transaction happens.

Instead of fixing VAT errors at month-end, Alaan prevents them at source.

Alaan is designed around the realities of UAE VAT rules and FTA expectations:

- Every transaction is captured in real time, with merchant data and spend category automatically attached

- VAT-relevant details are structured at the point of purchase, not reconstructed later

- Receipts are enforced, digitized, and linked to each transaction, reducing missing-document risk.

- Audit-ready records are centralized, searchable, and exportable for FTA reviews.

By embedding VAT discipline into everyday spending, Alaan shifts compliance from reactive correction to proactive control. Finance teams gain clarity, speed, and confidence, without increasing operational burden on employees.

If VAT accuracy impacts your cash flow, audit exposure, and leadership credibility, it should not depend on memory or manual checks.

Book a demo to see how Alaan turns VAT compliance into a built-in business advantage.

Summing Up,

B2B VAT in the UAE is operational; it affects every invoice, payment, and cross-border transaction you process. Small lapses can trigger fines, blocked input tax recovery, and audit exposure.

Clear rules exist, but manual tracking, delayed receipts, and fragmented data make compliance fragile. You reduce risk when VAT controls move closer to the point of spend. Real-time visibility, structured records, and automated enforcement turn VAT from a liability into a managed process.

Alaan addresses this at the source of spend by issuing corporate cards that capture VAT-ready receipts in real time, enforce compliant expense categories, and structure every transaction with the data required for recovery and reporting. Your finance team gains a clean, audit-ready VAT trail without chasing documents or correcting errors after the fact. Book a demo to see how Alaan simplifies B2B VAT compliance across your organization.

FAQs

1. What qualifies as a B2B transaction under UAE VAT?

A B2B transaction occurs when both the supplier and buyer are VAT-registered businesses in the UAE. These transactions require compliant tax invoices and allow input VAT recovery, subject to FTA rules.

2. Can a business recover VAT without a valid tax invoice?

No. The FTA allows input VAT recovery only when a valid tax invoice is held. Missing TRN, VAT amount, or supplier details can invalidate the claim and trigger penalties.

3. Does VAT apply to cross-border B2B services?

Often through the Reverse Charge Mechanism. The UAE business must self-account for VAT on imported services and report it in the VAT return, even if no VAT is charged by the supplier.

4. How often must B2B businesses file VAT returns?

Most UAE businesses file quarterly, though some are assigned monthly periods. Returns and payments must be submitted within 28 days after the tax period ends.

5. What happens if input VAT is overclaimed?

Overclaims can lead to assessments, penalties, and interest by the FTA. Repeated errors also increase audit risk and can impact future refund approvals.