UAE businesses are structurally exposed to FX risk because cross-border trade is not an edge case. The UAE’s non-oil foreign trade reached ~AED 3.8 trillion in 2025, according to the Emirates News Agency (WAM).

The Bank for International Settlements (BIS) reports that global FX turnover averaged USD 9.5 trillion per day (≈ AED 34.89 trillion) in April 2025, based on the final results of its latest Triennial Survey released in December 2025.

That combination is why building a budget for FX risk management is not about predicting the perfect exchange rate. It is about setting clear rules for planning rates, buffers, hedging, approvals, and execution so volatility does not turn into avoidable variance.

This guide explains how to build a budget for FX risk management in 2026, including exposure mapping, planning-rate policy, scenario buffers, hedging guardrails, and variance reporting for UAE finance teams.

TL;DR

- An FX Budget Controls Decisions, Not Markets, by standardising planning assumptions and defining guardrails.

- Exposure Mapping Is The Foundation, because hidden recurring FX flows create the most avoidable variance.

- Planning Rates And Hedging Serve Different Purposes, and mixing them usually weakens both.

- Scenario Buffers Reduce Budget Fragility, especially when volatility increases or payment timing shifts.

- Variance Reporting Works Best When Split By Driver, separating market movement from spread, fees, and timing.

- Process Controls Prevent Unplanned Exposure, particularly through renewals, ad hoc purchasing, and inconsistent approvals.

- A Connected Payments Workflow Improves Predictability, especially when invoices, approvals, FX visibility, and reconciliation stay in one system.

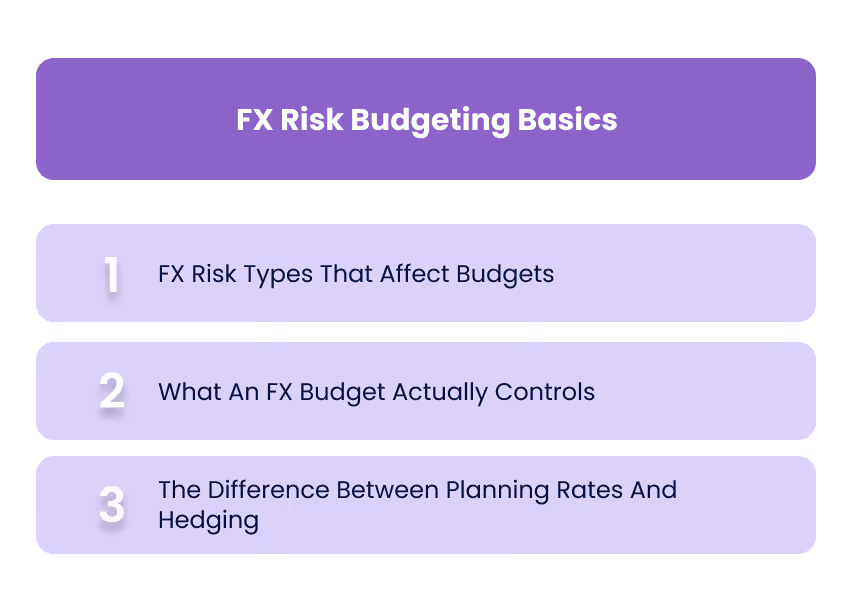

FX Risk Budgeting Basics

Before you build an FX budget, it helps to separate three things that often get mixed together: the types of FX exposure you have, what your budget is actually controlling, and where “planning” ends and “hedging” begins. When these are clear, the rest of the process becomes easier to standardise across teams.

1. FX Risk Types That Affect Budgets

Most budgeting issues show up in transaction FX risk (future cash flows in foreign currency), but it is still useful to recognise the other categories so you do not over-engineer the wrong problem.

- Transaction Risk: Occurs when exchange rates move between pricing/approval and settlement. This is the most common budget pain point for supplier payments and foreign-currency costs.

- Translation Risk: Arises when you revalue foreign-currency balances or consolidate entities across currencies. This is usually a reporting issue, but it can still create variance headlines.

- Economic Risk: Reflects long-term currency shifts that affect competitiveness and pricing power. This matters more in strategy than in month-to-month budgeting.

2. What An FX Budget Actually Controls

An FX budget does not control the market. It controls your internal decisions and the conditions under which you take FX risk. Practically, your FX budget should define:

- Which exposures are in scope (Supplier payments, subscriptions, foreign payroll, receivables, debt service).

- How you will plan rates (A defined budget rate approach, not ad hoc “today’s rate”).

- What variance you will tolerate (Thresholds that trigger action or escalation).

- Where buffers sit (Which cost lines carry contingency, and under what rules).

- Who owns what (Finance vs procurement vs sales, with a clear approval matrix).

3. The Difference Between Planning Rates And Hedging

A clean budgeting model separates assumptions from actions.

- Planning rate: The rate you use to translate expected foreign-currency cash flows into your budget currency for forecasting and performance measurement. This creates consistency across plans and teams.

- Hedging: The action you take to reduce uncertainty (for example, locking a rate for a future payment). Hedging is optional and policy-driven; planning is mandatory if you want a stable budget baseline.

A useful way to think about it is: budgeting sets the “expected path” and the guardrails; hedging is one of the tools you may use when an exposure is large enough or sensitive enough to justify protection.

Also Read: Understanding What is Financial Planning and Analysis (FP&A)

Step-By-Step Budget For FX Risk Management

A reliable FX budget works as a repeatable decision framework. It starts with mapping exposure, then sets planning-rate rules, defines tolerances, and adds buffers and review cycles so decisions stay consistent across the year. The steps below are designed to produce concrete outputs you can reuse: an exposure register, a planning-rate policy, a variance playbook, and a review cadence.

1. Map Your FX Exposure

Budgeting fails when teams only model the “obvious” exposures and miss the recurring ones that quietly accumulate variance. Start by mapping every foreign-currency flow that can materially affect cash flow, cost of goods, or margins, then assign ownership so it does not become a spreadsheet that nobody maintains.

At a minimum, capture:

- Currency (USD, EUR, GBP, INR, etc.).

- Flow type (Payables, receivables, subscriptions, payroll, debt service).

- Timing (Weekly, monthly, quarterly, ad hoc).

- Volume and seasonality (Average amounts and peak periods).

- Business owner (Who initiates and who approves).

- Sensitivity (What happens if the rate moves 1–3% before settlement).

The output of this step is an “FX exposure register” that becomes the source of truth for your budget. It also makes it easier to spot where you can reduce risk without financial instruments, such as matching inflows and outflows in the same currency.

2. Select Your Planning Rate Approach

Once you know your exposures, you need a consistent way to translate them into your budget currency. The goal is not to find the perfect rate. The goal is to use a method that is stable enough for planning, defensible in reviews, and easy to apply consistently.

Most finance teams choose one of these planning approaches:

- Budget-Date Spot Rate: Set the budget using the prevailing rate at the time of budget finalisation. This is simple, but it can create large variance if rates move early in the year.

- Rolling Average Rate: Use an average over a defined window (for example, three or six months). This smooths short-term swings and often produces more stable budgets.

- Policy Rate With Bands: Set a standard internal planning rate and define acceptable variance bands. If the market moves outside the band, you re-forecast or adjust buffers based on pre-agreed rules.

Choosing the approach is about fit. For highly predictable, high-value payables, many teams prefer a method that avoids sharp swings in reported variance. For smaller, frequent payments, simplicity matters more than precision.

The output of this step is a documented planning-rate policy so every team uses the same assumptions and nobody quietly “updates rates” to make their numbers look better.

3. Set Risk Appetite And Guardrails

FX risk appetite is the line between normal variance and variance that requires action. Without explicit guardrails, the default behaviour becomes reactive: teams escalate only after the budget is already off track.

A practical guardrail framework defines:

- Tolerance thresholds by currency or exposure type (for example, a variance percentage that triggers review).

- Approval rules for when hedging is permitted or required.

- Escalation paths so procurement and finance do not debate “who owns the problem” during a supplier deadline.

- Measurement rules so variance is calculated consistently (rate movement vs spread vs fees).

This is also where you decide whether you manage FX centrally (finance/treasury owns all exposure decisions) or in a hybrid model (business teams own exposure, finance owns policy and oversight). The right model depends on transaction volume and team maturity, but the budget must reflect whichever model you choose.

4. Build Scenario Buffers Into The Budget

Even with a planning rate, you need a structured way to handle adverse moves without rewriting the budget every month. Scenario buffers do that. They let you separate “expected cost” from “protection capacity.”

A workable scenario setup includes:

- Base case: The planning-rate assumptions you will measure performance against.

- Adverse case: A realistic downside move based on your exposure sensitivity.

- Severe case: A stress scenario used to test liquidity and supplier payment resilience.

Buffers should sit where they will actually be used. Some teams hold a central contingency line in finance; others allocate buffers into the cost lines that carry the exposure. What matters is that the release and reallocation rules are defined in advance, so buffers do not become an informal slush fund.

5. Define Your Review Cadence

FX budgets break when monitoring is irregular. A budget for FX risk management needs a cadence that matches how quickly your exposures change and how much capacity your team has.

Most teams adopt a simple rhythm:

- Monthly review for high-volume payables and subscriptions.

- Quarterly review for longer-dated contracts and strategic exposures.

- Event-based reviews when large supplier contracts are signed, pricing changes, or currencies move outside your tolerance bands.

The output of this step is a review calendar and a variance playbook: what you check, how you explain variance, and what actions are permitted at each threshold.

Also Read: Difference between Budgeting and Financial Forecasting

Hedging Tools To Protect Your FX Budget

Once your budget for FX risk management has a clear exposure register, planning-rate approach, and variance guardrails, hedging becomes easier to use responsibly. The point is not to hedge everything. The point is to use the right instrument for the exposures that can meaningfully disrupt cash flow, margins, or supplier commitments.

This section covers the most common hedging tools finance teams use and how they fit into an FX budgeting framework.

1. Natural Hedging

Natural hedging reduces FX exposure by structuring operations so currency inflows and outflows offset each other. It is often the lowest-friction approach because it does not rely on financial contracts.

Natural hedging can work when:

- You have both revenue and costs in the same currency (for example, EUR receivables and EUR supplier payments).

- You can invoice in the currency you pay in, reducing conversion frequency.

- You can time conversions, holding foreign currency for upcoming payments rather than converting immediately.

The budgeting benefit is straightforward: fewer conversions mean fewer opportunities for spread, fees, and timing variance to hit your cost base.

2. Forward Contracts

A forward contract lets you lock an exchange rate for a future date. It is most useful for large, predictable payments where the “cost of uncertainty” is higher than the cost of locking a rate.

Forward contracts tend to fit well when:

- Supplier payments are fixed and scheduled, such as quarterly inventory purchases.

- Your margin is sensitive to rate moves, and a small shift changes profitability materially.

- You need delivery certainty, because a delayed payment or cost surprise risks fulfilment.

In budgeting terms, forwards work best when your policy defines clear thresholds, such as a minimum payment size or a maximum variance tolerance that triggers a hedge decision. That keeps hedging consistent and reduces the chance of “hedge-by-opinion.”

3. Options

Currency options provide the right but not the obligation to exchange at a specific rate. They can be useful when you want protection against adverse moves without losing upside if rates move in your favour.

Options are typically considered when:

- Cash flows are uncertain, such as a forecasted purchase that may shift in timing or size.

- You want downside protection with flexibility, rather than locking a single rate.

- The exposure is meaningful, and the premium cost is justified versus budget risk.

For most mid-market businesses, options are not the first tool used. They are more appropriate when exposure uncertainty is high and forward contracts feel too rigid.

4. Multi-Currency Accounts

Multi-currency accounts allow businesses to hold balances in multiple currencies and decide when to convert. This can reduce unnecessary conversions and give finance teams more control over timing.

They can be useful when:

- You pay suppliers regularly in the same foreign currency, making it sensible to maintain a working balance.

- You want to reduce conversion frequency, especially when payments are frequent and operational.

- You want better cash planning, holding currency in advance of known obligations.

The budgeting advantage is that multi-currency balances reduce last-minute conversions driven by supplier deadlines, which is often when spreads and timing variance become most painful.

When Not To Hedge

Hedging is not automatically “best practice.” It adds operational overhead, requires governance, and can create confusion if it is not linked to your budgeting process.

Hedging may not be appropriate when:

- Exposures are small or irregular, and the administrative cost outweighs the risk.

- Your business can naturally offset flows, making financial hedges redundant.

- You do not have clear policy controls, which increases the chance of inconsistent decisions and messy reporting.

A disciplined approach is to start with exposure mapping and guardrails, then hedge only what is both material and manageable.

Also Read: Cost Management in UAE: Key Steps, Benefits & Proven Strategies for 2026

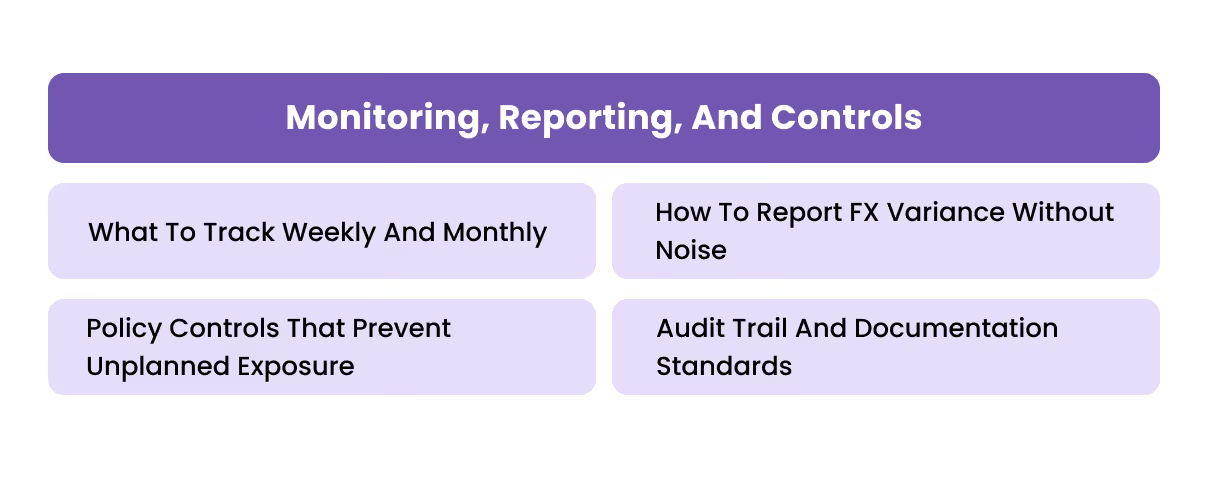

Monitoring, Reporting, And Controls

A budget for FX risk management only works if it is monitored with a repeatable cadence and reported in a way that drives action, not noise. The objective is to spot meaningful drift early, explain variance consistently, and prevent unplanned exposure from entering the business through ad hoc purchasing or inconsistent assumptions.

What To Track Weekly And Monthly

You do not need a complex treasury dashboard to stay in control. You need a small set of metrics that connect exposure to budget impact.

Track the following on a consistent schedule:

- Net Exposure By Currency (Outstanding payables and receivables, netted where appropriate).

- Planning Rate Versus Current Rate (To quantify drift in budget terms).

- Coverage Ratio (What percentage of material exposures are hedged or naturally offset).

- FX Variance Split (Rate movement versus spread/fees versus timing).

Weekly tracking is useful when you have frequent supplier payments, while monthly tracking works when payments cluster around specific cycles.

How To Report FX Variance Without Noise

FX variance becomes unmanageable when it is reported as one number with no explanation. A clearer approach is to split variance into components, so stakeholders know what changed and what can be controlled.

A practical split is:

- Market Movement Variance (Changes driven by the underlying rate).

- Pricing Variance (Spread, markups, and fee effects).

- Timing Variance (Differences between approval date and execution date).

This also makes it easier to keep the conversation honest. Market movement may be unavoidable. Spread, fees, and timing discipline are operationally controllable.

3. Policy Controls That Prevent Unplanned Exposure

Many FX surprises come from decisions that bypass budgeting discipline, such as last-minute vendor purchases, subscription renewals in a different currency, or supplier payments executed outside the usual approval workflow.

Controls that reduce unplanned exposure include:

- Currency Rules By Vendor Type (Which currencies are approved for which categories).

- Approval Thresholds (Higher scrutiny for larger foreign-currency commitments).

- Purchase And Renewal Controls (Especially for recurring SaaS and overseas service contracts).

- Standardised Payment References (To avoid reconciliation gaps and compliance queries).

4. Audit Trail And Documentation Standards

FX budgeting improves when the documentation around currency decisions is consistent. This is not just for audits. It is for month-end speed and variance explainability.

The minimum standard is that you can trace:

- The exposure source (Invoice, contract, subscription).

- The planning assumption (Budget rate method and date).

- The execution outcome (Rate applied, fees, settlement confirmation).

- The approval record (Who approved, under what rule).

How Alaan Helps You Streamline FX Budgeting And Control

FX budgeting becomes significantly easier when your foreign-currency spend is visible, approvals follow a consistent process, and payment records stay linked to invoices and accounting entries. At Alaan, we help finance teams do that by connecting spend controls, accounts payable workflows, and international supplier payments in one system.

- Upfront FX Visibility For Supplier Payments With SuperPay

SuperPay is built for paying international suppliers with clearer cost predictability. It brings cross-border transfers into a structured workflow and emphasises lower FX rates and reduced fee friction, which helps finance teams plan supplier costs with less variance. - Invoice And Approval Workflows Before Funds Move

A recurring budgeting failure is executing payments before capturing the full context. SuperPay is designed to keep invoices and approvals connected to transfer execution, which reduces last-minute exceptions and helps enforce consistent budget assumptions across teams. - Centralised Records That Support Budgeting And Reconciliation

Budget control is not only about rate assumptions. It is also about whether you can explain what happened after the payment executes. Keeping payment context, approvals, and supporting documents connected reduces manual reconstruction during close and makes FX variance easier to attribute. - Accounting Integrations For Cleaner FX Entries

Accurate budgeting depends on clean books. Alaan supports accounting integrations with major systems, including QuickBooks, Xero, and NetSuite, which helps teams reduce manual entry and maintain consistent categorisation and reconciliation.

Related: Procure-to-Pay Systems: Defining Process and Steps

Conclusion

A strong budget for FX risk management is built on visibility and discipline, not prediction. When you map exposure clearly, set a defensible planning-rate policy, define variance thresholds, and add scenario buffers and review cadence, currency volatility stops being a surprise and becomes a managed variable.

Hedging tools can strengthen the budget, but only after the budgeting spine is clear. The teams that consistently reduce FX variance are the ones that standardise data, enforce approvals, monitor drift early, and keep payment and accounting records connected.

At Alaan, we built SuperPay to help UAE finance teams manage international supplier payments with upfront FX visibility, structured approvals, and cleaner reconciliation. Book a demo to see how SuperPay fits your supplier payment workflow.

FAQs

1. How Should A Business Choose A Source For Its Budget FX Rate

A defensible budget rate source is one that is consistent, documented, and repeatable. Many teams define a standard source and time window, then apply it across all budgeting models to avoid department-level rate “adjustments.” The best choice depends on exposure frequency, but the governance matters more than the exact source.

2. What Is A Practical Hedge Threshold For SMEs

A common approach is to hedge only when the exposure is both material and time-bound, such as large supplier payments due within a defined window. Rather than using one rule for everything, many teams set thresholds by currency, payment size, and margin sensitivity, then align approval levels to those thresholds.

3. How Should Finance Teams Report Realised And Unrealised FX Differences

Realised differences typically arise when a foreign-currency payable or receivable is settled at a different rate than the one used at recognition. Unrealised differences arise when foreign-currency balances are revalued at period end. A useful management report separates them so operational teams focus on controllable drivers, while finance retains clean reporting logic.

4. How Can Procurement And Finance Stay Aligned On FX Assumptions

The simplest mechanism is a shared planning-rate policy and a standard approval workflow for foreign-currency commitments. When procurement knows the rate basis and the variance tolerance in advance, supplier negotiations and payment timing decisions become more consistent.

5. What Should A Finance Team Look For In A Provider To Reduce FX Budget Variance

Beyond headline rates, look for upfront visibility into total cost, a clear approval process, and records that stay linked to invoices and accounting. Those elements reduce timing variance, fee surprises, and reconciliation gaps, which are often the true drivers of budget drift.