Cash flow capital is tested when a business has enough sales activity but not enough liquidity moving through the operating cycle. Revenue may be growing, yet cash can still be trapped in receivables, inventory, supplier commitments, payroll, and recurring operating expenses.

This is especially relevant for UAE SMEs. The Central Bank of the UAE’s MSME Business Survey found that only 17% of MSMEs applied for bank credit in 2020, and only 9% secured the finance needed. The report also identified inadequate liquidity, cash flow constraints, and lack of collateral as reasons why MSMEs struggled to secure bank financing.

Cash flow capital, therefore, should not be reduced to a funding question. Before borrowing more, finance teams need to understand where capital is trapped, how quickly receivables convert, when suppliers must be paid, how much inventory is being held, and whether operating spend is quietly increasing the baseline cash requirement.

In this blog, we will explain what cash flow capital means in practical terms, how it connects with working capital, and how businesses can protect liquidity by managing the cash cycle more effectively.

TL;DR / Key Takeaways

- Cash flow capital refers to the practical liquidity available to support day-to-day operations while cash moves through the business.

- It is closely linked to working capital, but it focuses more on timing gaps between collections, supplier payments, inventory, payroll, and operating spend.

- Revenue growth can increase pressure on cash flow capital when costs rise before customer cash is collected.

- Receivables, inventory, supplier terms, fixed costs, and recurring spend are the main areas where liquidity gets trapped.

- Businesses can protect cash flow capital by improving collections, aligning payments, controlling inventory, and keeping operating spend visible.

What Cash Flow Capital Means In Practice

Cash flow capital is not a formal accounting term found in financial statements. Instead, it is used in a practical sense to describe the capital available to support the movement of cash through a business.

It represents the liquidity required to:

- pay suppliers

- manage payroll

- fund inventory

- cover operating expenses

- handle timing gaps between inflows and outflows

Unlike profit or revenue, which are measured on an accounting basis, cash flow capital reflects the real availability of funds at any point in time. A business may appear strong on paper but still face pressure if cash is tied up in receivables or inventory.

This is why understanding cash flow capital requires looking beyond balances and focusing on how quickly cash moves through the operating cycle.

How Cash Flow And Working Capital Are Connected

Cash flow and working capital are closely related, but they are not the same. Understanding the distinction is essential for managing liquidity effectively.

Cash flow tracks how money moves in and out of the business over time. Working capital reflects the difference between current assets and current liabilities, indicating whether the business can meet short-term obligations.

A simple way to view the relationship is:

A business can have positive working capital but still experience cash flow pressure if inflows are delayed. Similarly, strong cash flow can temporarily mask weak working capital if driven by financing or delayed payments.

Also Read: Manage Business Cash Flow Effectively

Where Capital Gets Trapped Inside The Cash Cycle

Cash flow capital is often reduced not by one large issue, but by multiple smaller inefficiencies across the operating cycle. These areas are where liquidity tends to get trapped.

1. Receivables That Convert Too Slowly

When customers take longer to pay, cash remains locked in outstanding invoices. This creates a gap between revenue recognition and actual cash availability. Atradius’ 2025 UAE payment practices report found that overdue invoices affect 58% of B2B sales, showing how delayed receivables can reduce available cash flow capital even when revenue has already been recorded.

2. Inventory That Moves Slower Than Expected

Inventory ties up cash until it is sold. Excess stock or slow-moving items increase the capital required to maintain operations.

3. Supplier Payments That Come Due Before Customer Cash Arrives

When suppliers require early payment while customers pay later, the business must bridge the gap using its own cash or external capital.

4. Fixed Costs That Continue Regardless Of Revenue Timing

Expenses such as salaries, rent, subscriptions, and logistics continue even when inflows are delayed.

5. Growth Spending Before Returns Are Realised

Investments in hiring, marketing, or expansion often happen before revenue converts into cash, increasing short-term pressure.

Why Revenue Growth Can Increase The Need For Cash Flow Capital

Growth is often assumed to improve financial stability, but it can also increase pressure on cash flow capital.

As a business grows, it typically:

- sells more but collects later

- holds more inventory

- hires more staff

- increases operating expenses

This means cash outflows rise before inflows fully catch up. Without careful planning, growth can widen the gap between spending and cash availability.

For example, a company may double its monthly sales, but if customers pay in 60 days and suppliers require faster payment, the business needs additional capital to sustain that growth.

Also Read: Cash Flow Optimisation Strategies Techniques

How To Know If A Business Needs More Cash Flow Capital

Cash flow pressure does not always appear suddenly. In most cases, there are early indicators that capital available for operations is becoming insufficient.

These signals are usually operational, not accounting-based.

1. Collections Are Slowing While Payments Remain Fixed

If customer payments are delayed but supplier obligations continue on schedule, the business starts funding the gap internally. Over time, this reduces available liquidity.

2. Inventory Purchases Are Increasing Faster Than Sales Conversion

When inventory builds up faster than it is sold, more cash gets tied up in stock. This reduces the capital available for other operating needs.

3. Short Term Borrowing Becomes Routine

Occasional borrowing to manage timing gaps can be normal. However, when it becomes a recurring requirement, it indicates a structural cash flow capital issue.

4. Forecasted Cash Gaps Keep Reappearing

If cash flow forecasts consistently show shortfalls, it suggests that the underlying operating cycle is not aligned with actual inflows and outflows.

Also Read: Cash Flow Forecasting

5. Teams Delay Payments Or Spending Decisions

When departments begin postponing payments or reducing necessary spend due to uncertainty, it often reflects underlying liquidity pressure.

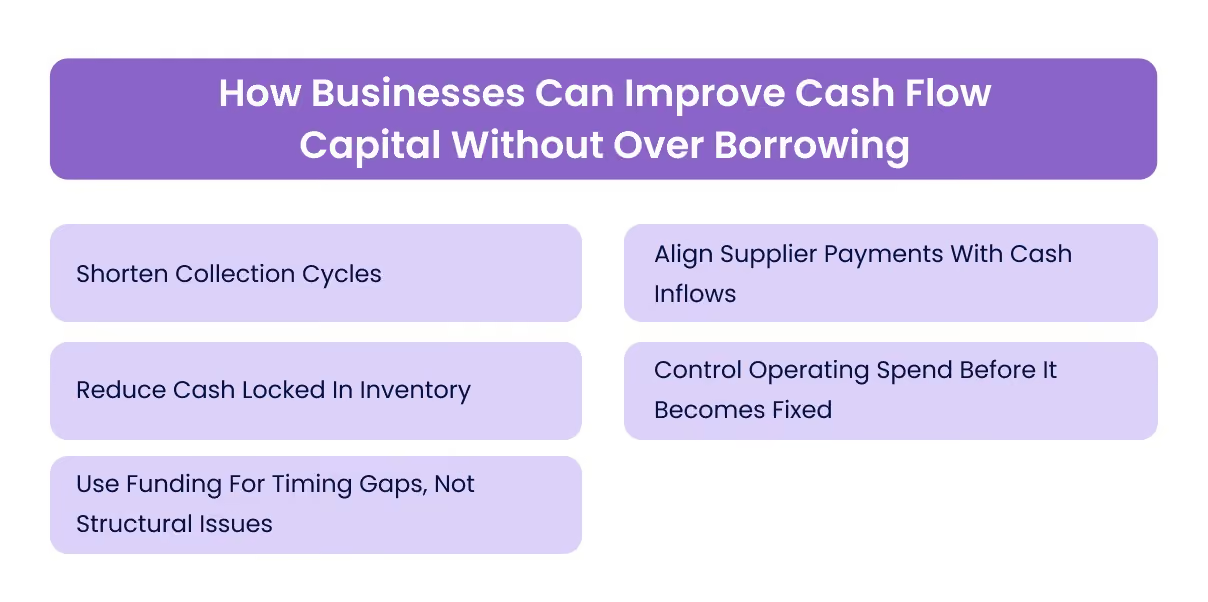

How Businesses Can Improve Cash Flow Capital Without Over Borrowing

Increasing cash flow capital is not always about raising funds. In many cases, improving the efficiency of the operating cycle can release cash that is already within the business.

1. Shorten Collection Cycles

Improving invoicing accuracy, follow-ups, and payment terms can reduce the time it takes for revenue to convert into cash.

Even small improvements in collection timing can significantly improve liquidity.

2. Align Supplier Payments With Cash Inflows

Negotiating better payment terms or aligning payment schedules with expected inflows helps reduce timing gaps.

The goal is not to delay payments arbitrarily, but to match outflows more closely with inflows.

3. Reduce Cash Locked In Inventory

Better demand planning and inventory management can prevent excess stock from tying up capital.

Focusing on turnover rather than volume helps maintain balance.

4. Control Operating Spend Before It Becomes Fixed

Small recurring costs and distributed team expenses often increase gradually. Without control, they raise the baseline cash requirement of the business.

Related: Guide To Manage Overall Business Spending

5. Use Funding For Timing Gaps, Not Structural Issues

External capital should support temporary mismatches between inflows and outflows. If funding is used to cover ongoing inefficiencies, it increases long-term risk.

When External Capital Makes Sense

While improving internal processes is essential, there are situations where external capital is appropriate.

External funding can be useful when:

- the business has predictable demand but faces timing gaps between inflows and outflows

- growth opportunities require upfront investment before returns are realised

- supplier or inventory cycles require additional liquidity support

However, relying on external capital without addressing underlying inefficiencies can create recurring pressure.

The key is to distinguish between short-term liquidity needs and structural issues in the operating cycle.

What Finance Teams Should Review Before Raising Or Allocating Capital

Before deciding to raise or allocate additional capital, finance teams should evaluate how cash is currently moving through the business.

A structured review helps identify whether the issue is timing, inefficiency, or genuine funding need.