Finance teams rarely question whether an investment looks promising. The real challenge comes when assumptions enter the model. Small changes in growth forecasts, operating costs, or discount rates can have a big impact on valuation results.

This is especially true in the UAE, where companies in logistics, real estate, and technology continue investing heavily in expansion and infrastructure. In the first half of 2025, the UAE attracted 613 greenfield FDI projects worth $5.42 billion (AED 19.90 billion), with Dubai accounting for $3.03 billion (AED 11.13 billion).

When capital deployment reaches this scale, investment decisions need structured valuation models. Discounted cash flow analysis helps finance teams estimate the present value of future cash flows and assess whether an investment is likely to generate real financial value.

In this article, you’ll explore how finance teams build DCF models, the assumptions that influence results, and how these models guide capital decisions in UAE businesses.

TL;DR Key Takeaways:

- Discounted Cash Flow Supports Major Capital Decisions: UAE finance teams rely on DCF models to evaluate acquisitions, infrastructure expansion, technology investments, and regional growth initiatives.

- DCF Models Depend on Operating Drivers: Free cash flow projections are built from operating profit, working capital changes, capital expenditure, and tax assumptions, not just revenue forecasts.

- Discount Rate Selection Shapes Valuation: Finance teams construct WACCs based on equity expectations, borrowing costs, capital structure, and sector-specific risk adjustments.

- Terminal Value Drives Most Valuations: Terminal value often represents 60–70% of total DCF valuation, making long-term growth assumptions critical.

- Reliable Financial Data Improves Forecast Accuracy: Platforms like Alaan help finance teams track operational spending in real time, improving the cost visibility and financial inputs used in DCF models.

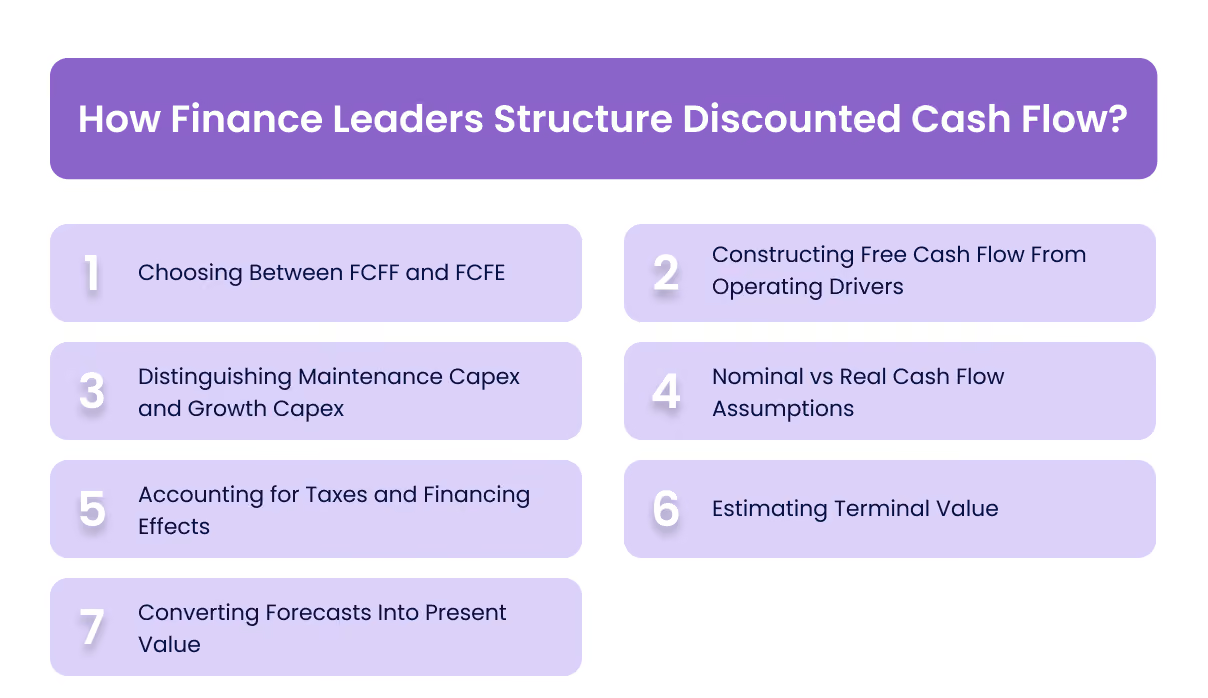

How Finance Leaders Structure Discounted Cash Flow?

Across the UAE, DCF models guide evaluations of logistics, real estate, technology, and GCC market-entry projects. These capital-intensive investments demand close scrutiny of free cash flow, discount rates, and assumptions.

Investment committees focus on revenue growth, working capital, and terminal value, while finance teams run sensitivity analysis to see how small changes affect valuations.

Below are the core modelling decisions finance teams address when structuring a DCF model.

- Choosing Between FCFF and FCFE

Finance teams start by deciding whether to model Free Cash Flow to the Firm (FCFF) or Free Cash Flow to Equity (FCFE).

- FCFF: It measures cash flows available to all capital providers and is commonly used to estimate enterprise value, especially for acquisitions, infrastructure projects, or strategic expansions.

- FCFE: It focuses on cash flows available to shareholders after debt obligations and is often used to assess equity returns or shareholder value creation.

In capital-intensive sectors like logistics infrastructure and real estate development in the UAE, finance teams often model FCFF first to understand enterprise value before factoring in financing decisions.

- Constructing Free Cash Flow From Operating Drivers

DCF models are built from operating forecasts, not just revenue projections. Finance teams typically construct free cash flow using key financial components:

- Operating profit after tax

- Capital expenditure requirements

- Depreciation adjustments

- Changes in working capital

Working capital assumptions are especially important in industries with large receivables or inventory cycles. Logistics operators, retail distributors, and e-commerce businesses in the UAE often experience significant expansion of working capital during growth phases.

As a result, a project may look profitable on an accounting basis but generate lower free cash flow if receivables increase quickly or inventory requirements grow alongside revenue.

- Distinguishing Maintenance Capex and Growth Capex

Capital expenditure assumptions are another area where judgement matters. Finance teams usually separate:

- Maintenance capex: Sustains current operations

- Growth capex: Supports expansion initiatives

Example:

In 2025, ADNOC Gas allocated $1.22 billion to growth projects and $217 million to sustaining assets and turnaround activities, showing how phased investments in infrastructure require careful planning to manage cash flow and financing.

This distinction is especially important for infrastructure and property development projects, where capital spending occurs in phases. Real estate and infrastructure projects in the UAE are often financed through project-based debt, meaning capex timing can significantly influence cash flow projections.

- Nominal vs Real Cash Flow Assumptions

Another key decision is whether to forecast cash flows in nominal or real terms.

- Nominal models include expected inflation in revenue, operating costs, and capex.

- Real models exclude inflation and apply inflation-adjusted discount rates instead.

In sectors like construction, healthcare infrastructure, and logistics in the UAE, inflation assumptions can significantly affect long-term project valuations. Finance teams ensure discount rates and cash flow projections remain consistent within the chosen approach.

- Accounting for Taxes and Financing Effects

Tax policy also affects free cash flow modelling. With the introduction of the UAE corporate tax, finance teams now include tax impacts when projecting operating profit and financing costs.

Interest payments may create tax shields that increase cash flow available to investors. When these effects aren’t modelled carefully, the estimated investment value can change significantly.

- Estimating Terminal Value

Most investments generate value beyond the forecast period, so finance leaders calculate terminal value to capture the business value after the projection window.

Two common methods:

- Perpetual growth method: It assumes long-term cash flow growth at a stable rate

- Exit multiple method: It applies a valuation multiple based on comparable market transactions

Research shows that terminal value often accounts for 60–70% of total DCF valuation, so finance teams scrutinise long-term growth assumptions carefully.

- Converting Forecasts Into Present Value

Once free cash flows and discount rates are defined, finance teams discount projected cash flows to estimate present value.

The standard formula is:

DCF = CF ÷ (1 + r)ᵗ

Where:

- CF is the projected cash flow

- r is the discount rate

- t is a time period

Each projected cash flow is discounted to today’s value, then combined with the discounted terminal value to estimate the overall investment or business value.

Why Reliable Cost Data Matters in DCF Models?

DCF outcomes are highly sensitive to operating assumptions. Even small inaccuracies in cost projections, working capital estimates, or operating expenses can materially affect valuations.

At Alaan, we help finance teams maintain real-time visibility into operational spending through corporate cards and automated expense tracking. Reliable cost data improves operating expense forecasts and working capital assumptions that feed directly into the free cash flow projections used in valuation models.

Once the DCF structure is in place, selecting the appropriate discount rate is a key step in achieving an accurate valuation.

How Do UAE Finance Teams Choose a Discount Rate in DCF Models?

Selecting the discount rate is often the most debated step in a DCF model. It captures both the true cost of capital and the project’s risk profile.

Even small changes can significantly alter valuation outcomes, which is why investment committees review the rate construction before approving major capital projects.

Most businesses calculate the discount rate using the Weighted Average Cost of Capital (WACC).

- Building WACC in Practice

In theory, WACC combines the cost of equity and the cost of debt based on the company’s capital structure.

In practice, finance teams spend most of their time validating the assumptions behind these inputs, including:

- Risk-free rate benchmarks

- Equity return expectations

- Borrowing costs across financing structures

- Capital structure assumptions

For UAE companies with access to international capital markets, teams often benchmark the risk-free rate against US Treasury yields and adjust return expectations to account for regional market risk.

Another key decision is whether to use:

- Corporate WACC, reflecting the company’s overall cost of capital

- Project-specific discount rates, used for new infrastructure projects, real estate developments, or international expansion

Project-specific rates are common when a project's risk profile differs significantly from the company’s existing operations.

- Estimating Equity Return Expectations

The cost of equity reflects the return investors expect for taking on business risk. Finance teams typically estimate this using the Capital Asset Pricing Model (CAPM).

The critical decisions lie in selecting inputs for the model. Teams evaluate factors such as:

- Whether beta should be adjusted for private or high-growth companies

- How to estimate the market risk premium

- Whether additional country risk should be incorporated for cross-border expansion

These adjustments are particularly relevant when UAE businesses evaluate investments in the GCC or emerging markets, where economic and regulatory conditions differ from those in the domestic market.

- Evaluating Debt Costs in Regional Financing Structures

The cost of debt reflects interest paid on borrowed capital, but financing structures vary widely across UAE industries.

Typical patterns include:

- Real estate and infrastructure projects financed through project-based debt structures

- Logistics infrastructure investments funded through long-term financing tied to asset cash flows

- Technology companies are relying more heavily on equity funding during early growth phases

Because these structures differ, finance teams often adjust discount rates to reflect the expected funding mix over the investment’s life.

- Accounting for Country and Market Risk

When evaluating regional expansion, finance teams often add country risk premiums to the discount rate.

Adjustments may consider factors such as:

- Regulatory stability

- Economic volatility

- Currency exposure

- Differences in market maturity

These ensure the valuation model reflects the true investment environment rather than assuming identical risk conditions across markets.

- Applying Sector-Specific Risk Premiums

Industry dynamics also influence assumptions about the discount rate. For example:

- Infrastructure and real estate projects involve long investment horizons and higher leverage

- Logistics businesses require significant upfront capital but may generate stable long-term cash flows

- Technology companies face lower capital intensity but higher uncertainty in revenue growth

Finance teams adjust discount rates to reflect the capital needs and operational risks of each sector.

Selecting the right discount rate is just one part of the process; finance teams also need to verify the key assumptions that ensure the DCF model’s reliability.

Key Assumptions to Check in Discounted Cash Flow Models

Discounted cash flow models help finance teams assess major investments and capital allocation decisions. However, the accuracy of a DCF model depends heavily on the assumptions used to project future cash flows.

Experienced finance teams review these assumptions carefully before presenting valuation models for investment approval. Even small changes to margins, capital expenditure, or terminal growth rates can significantly affect valuation outcomes.

Below are the key assumptions finance leaders typically stress-test when building DCF models.