A capital structure decision can seem simple in leadership discussions, but it quickly becomes complex when interest payments strain cash flow, loan conditions tighten, and refinancing becomes urgent.

This pressure is increasing in the UAE, where the debt capital market is projected to exceed $350 billion (AED 1285.38 billion) by 2026, reflecting a rising reliance on debt to fund expansion.

As a result, the debt-to-equity ratio becomes a critical indicator. It shapes borrowing costs, influences investor confidence, affects credit ratings, and ultimately determines how much financial flexibility a business can retain.

Its impact also varies by sector. In real estate and logistics, leverage can support expansion, while in tech and SaaS, excessive debt can impact recurring revenues and limit strategic choices.

So, in this blog, you’ll explore how the debt-to-equity ratio influences risk, outline sector benchmarks in the UAE, and highlight a long-term capital strategy.

TL;DR

- Debt to Equity Ratio Impacts Financial Strategy: The ratio directly shapes borrowing costs, covenant strength, credit access, and investor confidence.

- Industry Benchmarks in the UAE: Real estate and construction often operate at 2.0–3.0, while technology and SaaS typically remain between 0.5–1.5 to preserve flexibility.

- Implications of a High Ratio: Higher leverage increases repayment pressure, refinancing exposure, and borrowing costs, limiting flexibility during slowdowns.

- Implications of a Low Ratio: Lower leverage reduces risk but may reflect unused borrowing capacity and slower capital deployment.

- Strategies to Adjust the Ratio: Rebalance through equity infusion, disciplined debt use for revenue-generating assets, refinancing costly loans, stronger retained earnings, and regular cash flow stress testing.

How Finance Leaders Calculate the Debt-to-Equity Ratio?

Calculating the debt-to-equity (D/E) ratio is an important step for finance leaders and CFOs in the UAE and MENA region, especially when making decisions about capital structure, investment plans, and borrowing.

This ratio shows how much debt a company uses relative to its equity, which plays a key role in its financial stability and growth potential.

What Debt Should Be Included in the D/E Ratio?

To calculate the D/E ratio accurately, it’s important to include both short-term and long-term liabilities:

- Short-term debt (e.g., working capital loans and accounts payable) helps you manage day-to-day operational needs, particularly in sectors such as e-commerce and logistics.

- Long-term debt (e.g., loans, bonds, long-term obligations) is especially relevant in industries such as real estate, where projects require significant upfront investment and long repayment periods.

For healthcare companies, this may include financing for medical equipment or facility expansion, while tech startups may use venture debt or convertible notes that affect their capital structure without immediately diluting equity.

How to Calculate the D/E Ratio: A Practical Example

Here is a simple example of a real estate company operating in the UAE:

Total Debt:

- Short-term debt: AED 300,000

- Long-term debt: AED 1,200,000

- Total Debt = AED 1,500,000

Shareholder's Equity = AED 2,500,000

To calculate the D/E ratio, apply the formula:

D/E Ratio = Total Debt ÷ Shareholder’s Equity

D/E Ratio = 1,500,000 ÷ 2,500,000 = 0.6

This means the company has AED 0.6 of debt for every AED 1 of equity. For real estate businesses, a ratio at this level is considered balanced, supporting growth while maintaining financial stability.

Why It Matters: Understanding the Impact of D/E Ratios

- For CFOs in capital-intensive sectors like real estate, a moderate to high D/E ratio can be a deliberate strategy. It allows you to use debt to fund large projects while still keeping financial risk manageable.

- For tech startups or SaaS companies, a lower D/E ratio is usually more suitable, as these businesses often depend more on equity funding and predictable recurring revenue.

Maintaining the right balance between debt and equity helps you choose the most effective funding approach for growth and stability. At the same time, it is important to avoid excessive reliance on debt, as this can affect creditworthiness and increase future borrowing costs.

Knowing how to calculate the debt-to-equity ratio makes it easier to compare it with other key financial ratios.

Suggested Read: Calculating and Tracking Bad Debt Expense

Debt to Equity Ratio vs. Other Key Financial Ratios: What You Should Know

The D/E ratio helps you understand how much debt your company uses and the level of financial risk it carries. But you should not rely on it alone.

When you look at the D/E ratio along with other key ratios, you get a clearer picture of your company’s overall financial health. Below is a comparison of the Debt-to-Equity Ratio with other key financial ratios.

Comparing the debt-to-equity ratio with other financial ratios also helps you understand what it means when the ratio is too high or too low.

What Happens if Your Debt-to-Equity Ratio Is Too High or Too Low?

The debt-to-equity (D/E) ratio shows how a company structures its finances and how much risk it takes to support growth. Keeping this ratio at the right level is crucial.

If it goes too high or too low, it can affect financial flexibility, growth plans, and even the cost of capital.

1. Consequences of a High Debt-to-Equity Ratio

When the D/E ratio is high, the company relies heavily on debt rather than equity to run and expand the business. Debt can help drive growth, but it also increases financial pressure.

Key Issues:

- Increased Risk of Default: Higher debt means fixed repayments. During slow periods or when profits drop, those repayments can put real pressure on cash flow.

- Higher Borrowing Costs: Lenders often see a high D/E ratio as risky. They may charge higher interest rates or impose stricter loan terms.

- Creditworthiness Impact: A high ratio can affect your credit rating and make it harder to secure favourable financing later.

Impact on Decision-Making: Finance leaders need to closely monitor a high D/E ratio to avoid overloading the business with debt, especially in industries with volatility or uneven cash flow.

2. Consequences of a Low Debt-to-Equity Ratio

When the D/E ratio is low, the company takes a cautious approach, relying more on equity than on debt. This lowers financial risk, but it can also create limitations.

Key Issues:

- Missed Growth Opportunities: Low leverage can slow expansion, especially in sectors such as technology and real estate, where companies often need large capital investments.

- Underutilised Debt Capacity: A company with a low D/E ratio may not use available debt options that could help it scale faster or strengthen operations.

- Impact on Profitability: In some cases, finance teams may miss opportunities to improve returns on equity by avoiding debt to support expansion.

Impact on Decision-Making: CFOs and finance leaders must ask whether the business uses debt wisely to support growth. A low D/E ratio may indicate stability, but it can also signal that the company is not fully leveraging its financial position.

3. Finding the Right Balance

For startups, SMBs, and large enterprises, the goal is to strike the right balance between debt and equity. The right D/E ratio enables the business to grow without compromising financial stability.

Key Considerations:

- Industry Standards: Every industry has different expectations. Real estate and other capital-intensive sectors often operate with higher D/E ratios because they generate steady returns. Technology startups may prefer lower ratios in the early stages to limit risk.

- Business Cycle: The company’s growth stage also matters. A startup might accept a higher D/E ratio to grow quickly. An established company may choose a more conservative approach to protect stability.

Actionable Insight: Review your D/E ratio regularly and connect it to your business goals. Adjust debt levels based on market conditions and industry trends so you avoid taking on too much risk or missing growth opportunities.

At Alaan, we give finance teams real-time visibility into company-wide spend, approvals, and budget utilisation from a single dashboard. This enables tighter spend control, improves cash flow visibility, and supports more informed financial and capital planning decisions.

4. Impact on Investment and Financing Decisions

Investors and lenders closely monitor the D/E ratio when deciding whether to provide capital. If the ratio is too high, they may worry about the company’s ability to repay debt. If it is too low, they may question the company’s growth potential and expected returns.

Key Insight: Investors look for a D/E ratio that shows the company uses leverage wisely while managing risk. Lenders also prefer a balanced ratio that shows the business can comfortably handle its debt obligations.

Understanding what a high or low debt-to-equity ratio means also helps you compare it against industry benchmarks.

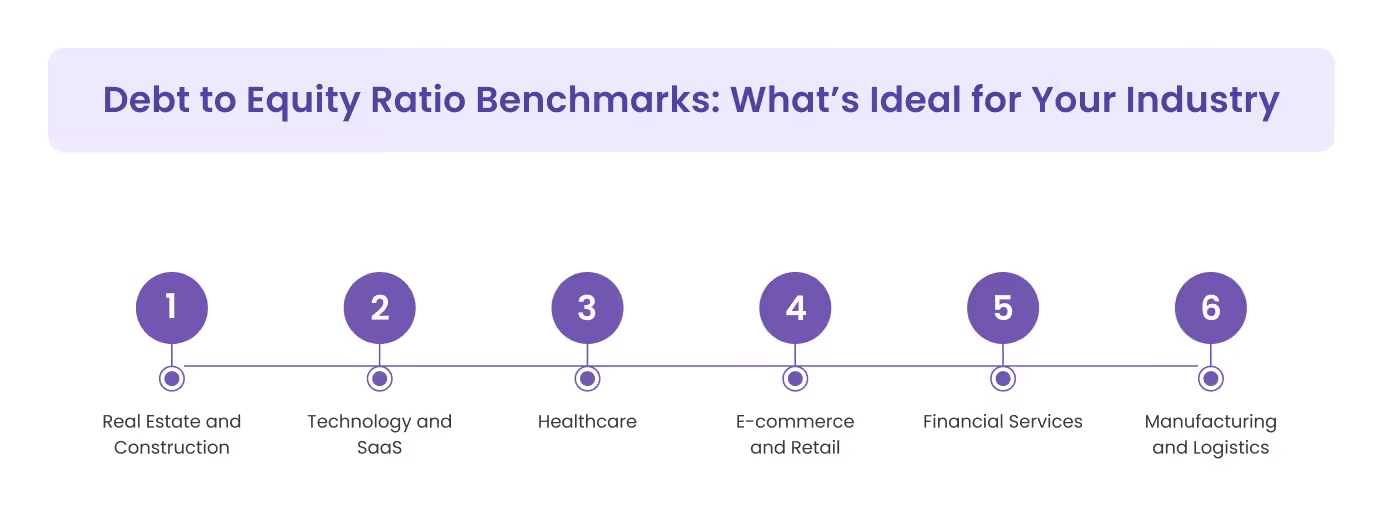

Debt to Equity Ratio Benchmarks: What’s Ideal for Your Industry

Knowing the right debt-to-equity (D/E) ratio benchmark helps you judge your company’s financial health, manage risk, and make smarter strategic calls. The D/E ratio applies to every business, but the ideal number looks very different from one industry to another.

When you compare your ratio to the right industry benchmark, you can see whether you are using debt wisely to support growth while keeping financial stability intact.

1. Real Estate and Construction

Real estate and construction businesses usually need heavy capital to fund projects. Because of this, these industries often operate with higher D/E ratios than most other sectors.

Typical Range: 2.0 to 3.0 (high leverage)

Why It Works: Real estate companies often generate steady cash flow from long-term property assets, which enables them to take on more debt. Construction firms also need large upfront funding for projects, so a higher D/E ratio often makes practical sense.

Key Insight: A higher D/E ratio can work in real estate, but companies still need to stay careful. Project delays or market slowdowns can quickly affect cash flow, making over-leveraging risky.

2. Technology and SaaS

Technology and SaaS companies typically require less physical capital and often generate predictable, recurring revenue. Many of them, especially in early stages, prefer equity over debt.

Typical Range: 0.5 to 1.5 (moderately low leverage)

Why It Works: SaaS companies with recurring revenue and strong margins often keep debt levels lower. Too much debt can create pressure on cash flow and reduce flexibility when scaling.

Key Insight: A lower D/E ratio often suits tech firms. However, when expansion opportunities arise, moderate debt can support growth without giving up too much equity.

3. Healthcare

Healthcare companies invest heavily in infrastructure, equipment, research, and development. Even though they face regulatory pressures, demand for healthcare services remains steady.

Typical Range: 1.0 to 2.0 (balanced leverage)

Why It Works: Hospitals and clinics often benefit from consistent revenue streams, which support moderate debt usage. At the same time, regulations require avoiding excessive borrowing.

Key Insight: Finance teams should use debt for investments that generate strong returns, such as expansion or advanced equipment, while keeping the D/E ratio at a manageable level.

Also Read: Hospital Accounts Receivable: A Practical Guide For Healthcare Finance Leaders

4. E-commerce and Retail

E-commerce and retail businesses operate in fast-changing markets. They deal with shifting demand, seasonal trends, and inventory costs, which affect their capital structure.

Typical Range: 0.7 to 2.0 (moderate leverage)

Why It Works: Many e-commerce companies grow quickly and use debt to finance inventory. At the same time, they must protect liquidity and maintain healthy margins, which keeps the ratio from going too high.

Key Insight: Retailers with strong customer demand and fast inventory turnover can handle more debt. But in volatile markets, too much leverage can create serious pressure.

5. Financial Services

Financial services companies operate under strict regulations. They must carefully balance capital strength and risk management.

Typical Range: 1.0 to 2.5 (varies by sub-sector)

Why It Works: Banks and insurance companies often access lower-cost capital, but they also face high credit risk and regulatory scrutiny. This makes careful monitoring of the D/E ratio essential.

Key Insight: Even though financial institutions can raise funds more easily, they must maintain a solid equity base to stay stable during market fluctuations.

6. Manufacturing and Logistics

Manufacturing companies often invest in heavy machinery and production facilities. Logistics companies spend significantly on fleets, warehouses, and infrastructure.

Typical Range: 1.5 to 2.5 (higher leverage)

Why It Works: These industries often work with long-term contracts or steady revenue streams, which support higher debt levels. Still, they operate in cyclical markets, so financial discipline remains important.

Key Insight: A higher D/E ratio can work in manufacturing and logistics, but companies must track cash flow closely to avoid stretching their finances too far.

Knowing the right benchmark for your industry makes it easier to plan strategies to adjust your debt-to-equity ratio for growth.

6 Strategies to Adjust Your Debt-to-Equity Ratio for Business Growth

The D/E ratio gives you a snapshot of your company’s financial health and risk level. But you can also use it as a practical tool to support growth and manage your capital structure more effectively.

Here are some strategies you can use to adjust your D/E ratio to support your growth plans while keeping your finances under control.

1. Increase Equity Financing to Reduce Risk

If your D/E ratio is too high, you can lower risk by reducing debt and increasing equity. Raising equity, either by issuing shares or bringing in venture capital, helps ease financial pressure and strengthens your credit profile.

How to Implement:

- Review your current capital structure and understand the breakdown of debt versus equity.

- Issue new shares or approach venture capital investors to raise equity.

- In high-risk sectors like real estate, consider relying more on equity to maintain financial stability.

2. Use Debt Financing to Support Expansion

If you want to scale faster, debt can give you the capital you need. It allows you to fund growth while keeping ownership intact and avoiding equity dilution.

How to Implement:

- Study your future cash flows to confirm you can comfortably repay the debt.

- Use borrowed funds for high-return areas such as expansion, research and development, or new product launches.

- Link debt directly to projects that generate revenue and cover interest costs.

Must Read: Top 8 Steps to Master Cash Flow Management for Your Business

3. Refinance Existing Debt on Better Terms

If expensive or restrictive loans push your D/E ratio higher, refinancing can help. Replacing high-interest debt with better terms can lower costs and improve cash flow.

How to Implement:

- Review your current loan agreements and identify refinancing options.

- Negotiate lower interest rates or longer repayment schedules.

- Use the money you save to support growth or invest in priority initiatives.

4. Improve Profitability to Strengthen Equity

You can also improve your D/E ratio by increasing profits. Higher profits increase retained earnings, strengthening your equity base and reducing the need for additional borrowing.

How to Implement:

- Cut unnecessary costs and improve operational efficiency.

- Adopt technologies that automate tasks and reduce manual effort.

- Shift the focus to higher-margin products or services.

At Alaan, we centralise expense management and automate categorisation to improve cost accuracy and reduce the risk of uncontrolled or untracked spend. Cleaner cost data helps finance teams protect retained earnings by improving cost control and financial accuracy over time.

5. Set Clear Debt Limits Based on Cash Flow

Always connect new borrowing to realistic cash flow projections. This keeps debt manageable and protects liquidity.

How to Implement:

- Build detailed cash flow forecasts that map future income and expenses.

- Regularly track cash flow and adjust borrowing as needed.

- Limit debt to amounts you can comfortably repay within projected timelines.

6. Take Advantage of Tax Benefits from Debt

Interest payments on debt are usually tax-deductible. This makes debt attractive when your business generates strong operating profits.

How to Implement:

- Review your tax position and see how debt can reduce overall tax liability.

- Consider low-interest borrowing to maximise tax efficiency.

- Use debt strategically for capital investments and growth-focused spending.

How Alaan Helps Finance Teams Protect the Debt-to-Equity Ratio?

Many finance teams in the UAE manage capital structure at the top, but operational spending stays fragmented across cards, invoices, and systems. This reduces visibility, weakens cash flow planning, and can delay the identification of liabilities, increasing financial risk.

At Alaan, we bring corporate cards, invoice management, approvals, payments, and accounting integrations into one unified spend management platform. This gives finance teams real-time visibility and control over operational spend, helping finance teams protect retained earnings through better cost control, manage liabilities with greater visibility, and maintain capital discipline.

What Alaan Covers Across the Operational Spend Lifecycle

Capital discipline depends not only on financing decisions but also on how effectively daily operational spend is controlled, approved, and recorded. At Alaan, we strengthen each stage of the spend lifecycle so you can make financial decisions based on accurate, real-time operational spend data.

1. Corporate Cards With Built-In Spend Controls

We provide corporate cards with configurable limits and policy controls, allowing you to manage spending before it happens. Admins can:

- Set spend limits by employee, team, or project

- Restrict merchant categories

- Issue virtual or physical cards instantly

- Freeze or block cards in real time

This ensures operational spending stays within approved budgets and helps prevent uncontrolled expenses that could negatively impact cash reserves and retained earnings.

2. Centralised Invoice Capture and Early Validation

We centralise invoice collection through uploads, email forwarding, and integrated workflows. Invoice data, vendor details, and tax fields are captured and validated early.

This helps finance teams:

- Reduce duplicate payments

- Identify errors before approval

- Maintain accurate records of liabilities

Capturing liabilities early improves financial visibility and reduces surprises during close or cash planning.

3. Policy-Driven Approvals Before Financial Commitments Are Finalised

Invoices and payments move through structured approval workflows in accordance with company policies.

This ensures:

- Spend aligns with budgets

- Proper authorisation happens before payment

- Exceptions are flagged early

By strengthening approval controls upstream, finance teams can prevent unnecessary or unplanned liabilities.

4. Integrated Payment Workflows With Full Visibility

Once approved, payments can be executed within controlled workflows, including domestic and supported international supplier payments across selected corridors through Super Pay.

This keeps approvals, payments, and records connected, reducing the risk of off-system transactions and improving cash flow oversight.

5. Automated Sync With Accounting and ERP Systems

We integrate with accounting systems such as:

- NetSuite

- QuickBooks

- Xero

- Microsoft Dynamics

- Zoho Books

- Odoo

Approved transactions sync automatically, ensuring accurate financial records, proper coding, and up-to-date reporting. Accurate books help finance teams monitor retained earnings, liabilities, and overall capital position with confidence.

6. Real-Time Visibility Into Operational Commitments

We provide live dashboards showing:

- Outstanding invoices

- Approved but unpaid spend

- Card transactions

- Department-level spending

This improves forecasting and helps finance teams anticipate cash requirements early, reducing the risk of sudden working capital pressure.

What Alaan Is (And Is Not)

Alaan is a spend management platform that strengthens operational financial control.

It helps finance teams:

- Enforce spending policies

- Improve visibility into operational commitments

- Maintain accurate financial records

Alaan does not replace your ERP or accounting system. Instead, it integrates with your existing systems to improve upstream control and data accuracy.

Final Thoughts

The debt-to-equity ratio reflects your business’s true financial flexibility. For finance leaders in the UAE, its value lies in actively managing it as conditions change, whether to fund growth, handle tighter credit, or protect cash flow.

This requires clear, real-time visibility into obligations and how financial decisions affect leverage. When capital allocation, spending, and reporting stay aligned, you can act faster and reduce unnecessary risk.

At Alaan, we help finance teams maintain real-time visibility by bringing together spend, approvals, and expense data into a unified workflow. This helps you understand how operational spending is tracking against budgets, improve expense reporting accuracy, and enforce control and compliance across your organisation.

Book a free demo to see how Alaan helps UAE businesses strengthen financial control, improve spend visibility, and make more informed financial decisions.

FAQs

Q1. What is the difference between the debt-to-equity ratio and gearing ratio?

A1. The debt-to-equity ratio compares total debt to shareholder equity, showing how much your business relies on borrowed funds versus owned capital. The gearing ratio measures debt as a share of total capital, including both debt and equity. This provides a broader view of the financial structure and is useful in capital-intensive sectors.

Q2. What are the limitations of the D/E Ratio?

A2. The D/E ratio shows financial leverage but does not reflect industry differences or cash flow strength. For example, tech or SaaS companies often keep lower debt to reduce risk, but too little debt can also slow growth. This is why CFOs must balance debt and equity based on growth plans, risk tolerance, and strategy.

Q3. How to determine the right level of debt for the UAE business?

A3. The right level depends on your growth stage, industry, and goals. Capital-intensive sectors like real estate often need higher debt to fund projects, while tech companies prefer lower debt for flexibility. The key is finding a balance that supports growth without increasing financial risk.

Q4. How to adjust the debt-to-equity ratio as the business grows or faces market changes?

A4. CFOs should review the D/E ratio regularly to keep it aligned with business needs. During expansion, debt can help fund growth without diluting ownership. During slowdowns, reducing debt helps protect cash flow and maintain stability.

Q5. What role does the debt-to-equity ratio play in the long-term sustainability of a UAE business?

A5. The D/E ratio helps businesses balance growth and stability. Managing it well supports expansion, controls financial risk, and builds investor confidence. It also helps businesses stay resilient during market changes.