From paying utility bills on a smartphone to applying for credit online, fintech has moved from the margins of finance to the centre of daily life. Juniper Research forecasts that the value of recurring payments alone will exceed USD 15.4 trillion globally by 2027.

For finance leaders in the UAE, fintech is not just a matter of convenience. It is the foundation for managing corporate spend, ensuring VAT and Corporate Tax compliance, and competing in a digital-first economy. Companies that fail to modernise risk inefficiencies, audit penalties, and reduced competitiveness in a market where regulators and investors increasingly expect digital readiness.

This article defines fintech technology, traces its history, unpacks the key technologies powering it, and explores modern use cases — from digital wallets to AI-driven expense management platforms.

What Is Fintech Technology?

Fintech — short for “financial technology” — refers to the use of digital tools to transform financial services. Unlike traditional systems reliant on legacy IT and paper-heavy workflows, fintech platforms are cloud-native, API-driven, and customer-centric.

Core elements of fintech technology include:

- APIs and Open Banking – Secure data exchange between banks and third-party platforms.

- Cloud Infrastructure – Scalable, cost-efficient systems with faster deployment cycles.

- Data Analytics and AI – Fraud detection, credit scoring, and real-time expense categorisation.

- Blockchain and Distributed Ledgers – Transparent, decentralised records for payments and settlements.

- Security and Authentication – Encryption, tokenisation, and biometric verification to protect users.

For UAE businesses, these capabilities go beyond speed and convenience. They enable compliance with local regulations, real-time spend visibility, and stronger investor confidence.

At Alaan, we leverage fintech technology through our corporate expense cards and spend management platform. By integrating AI-powered receipt validation, automated VAT checks, and accounting integrations, we help finance leaders gain full control over expenses while remaining audit-ready.

Also read: AI Use Cases in Finance

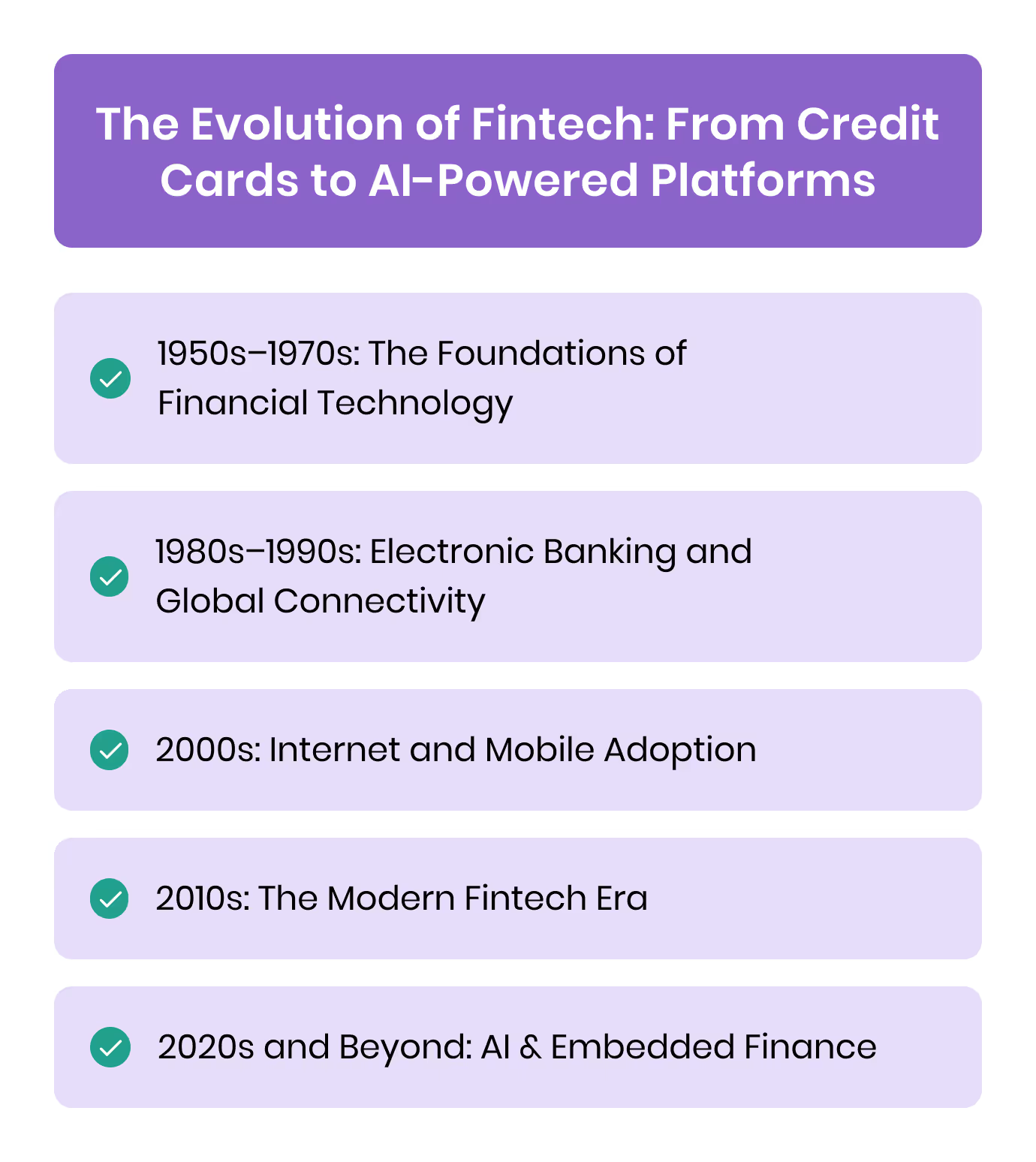

The Evolution of Fintech: From Credit Cards to AI-Powered Platforms

While the word “fintech” only entered popular usage in the 2010s, the idea of applying technology to financial services goes back decades. Each major wave of innovation mirrored advances in computing, communications, and evolving customer expectations.

1950s–1970s: The Foundations of Financial Technology

- The first major consumer-facing innovation was the credit card. In 1950, the Diners Club introduced one of the first universal charge cards, which allowed users to defer payments.

- In 1967, Barclays installed what is widely considered the world’s first robotic cash dispenser (ATM) in London.

- During the 1970s, financial institutions began adopting mainframe computing systems, electronic securities trading, and early interbank messaging protocols. The establishment of SWIFT in 1973 was a watershed for cross-border banking communication.

1980s–1990s: Electronic Banking and Global Connectivity

- In the 1980s, banks expanded electronic banking: ATMs and telephone banking matured, databases and networked systems enabled more seamless internal operations.

- At the same time, SWIFT expanded its network, enabling banks globally to exchange standardized financial messages.

- By the 1990s, the rise of the internet enabled retail customers to log in to bank portals, view balances, initiate transfers, and manage accounts online — shifting many financial services into homes and offices.

2000s: Internet and Mobile Adoption

- The dot-com boom drove growth in online payments — PayPal began operations in 1998 (initially as Confinity).

- When smartphones became widespread mid-2000s, mobile banking apps and digital wallets took off, reshaping both consumer finance and small/medium enterprise (SME) banking.

2010s: The Modern Fintech Era

This decade saw the crystallization of fintech as a discrete sector:

- Open Banking frameworks (e.g. via APIs) pushed legacy banks to open data access channels to third parties (e.g. in Europe under PSD2).

- Digital-only/neobanks emerged, offering streamlined, lower-cost banking services.

- Blockchain and cryptocurrencies spurred decentralized financial models and tokenized assets.

- Fintech startups scaled quickly, disrupting lending, wealth management, and insurance vertically.

- In the UAE, regulators such as the Central Bank, DIFC, and ADGM launched fintech sandboxes and licensing frameworks to catalyze innovation.

For instance, the UAE’s Central Bank has signed MOUs with DIFC and ADGM for a co-sandboxing programme. (Central Bank of the UAE)

ADGM’s “RegLab” is a regulatory sandbox that allows fintech firms to pilot solutions in a controlled environment without full regulatory burdens.

DIFC offers an ‘Innovation Testing Licence’ (ITL) for early-stage firms to test regulated products.

2020s and Beyond: AI and Embedded Finance

Currently, fintech is increasingly powered by artificial intelligence, real-time payments, and embedded finance — where financial services (payments, lending, insurance) are seamlessly integrated into non-financial apps.

In the Middle East, this evolution is accelerated by digitally native populations, high smartphone penetration, and proactive regulatory reform. The UAE, in particular, holds nearly half of the region’s fintech activity.

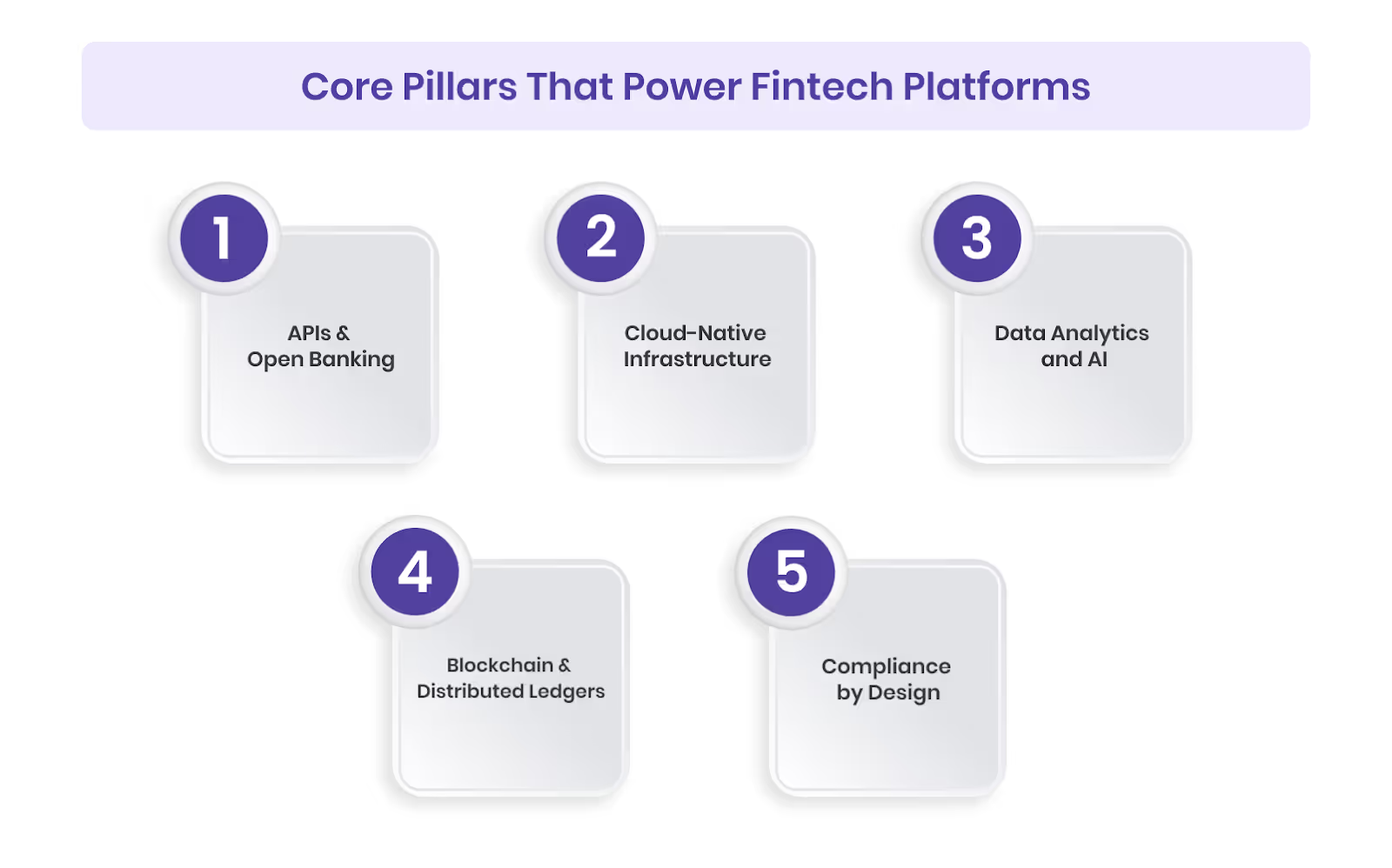

Core Pillars That Power Fintech Platforms

Behind every mobile wallet, lending app, or expense management solution is a set of technologies that make fintech scalable, secure, and compliant. For CFOs and finance leaders, understanding these pillars is essential to evaluating solutions in the UAE market.

1. APIs and Open Banking

APIs are the foundation of fintech. They enable secure data exchange between banks, platforms, and third parties. Open banking regulations in Europe and the Middle East have accelerated this trend, requiring banks to provide access to account data.

For UAE businesses, APIs are more than technical plumbing — they are what allow expense platforms to connect directly with accounting systems, VAT compliance tools, and banking providers, reducing manual effort and error.

2. Cloud-Native Infrastructure

Fintech solutions are typically cloud-based rather than tied to expensive on-premise servers. Cloud offers scalability, faster rollouts, and lower IT overheads. It also ensures platforms can handle rapid spikes in demand, whether during payroll processing or VAT filing deadlines.

3. Data Analytics and AI

Modern fintech platforms run on real-time analytics and machine learning models. Applications include:

- Fraud detection through pattern recognition.

- Automated categorisation of expenses.

- Credit scoring for SMEs without long credit histories.

For UAE CFOs, this means faster reporting cycles, better decision-making, and fewer missed compliance risks.

4. Blockchain and Distributed Ledgers

While not essential for every fintech platform, blockchain enables transparent and tamper-proof records for payments, smart contracts, and settlements. Cross-border businesses in the GCC use distributed ledgers to speed up remittances and reduce costs.

5. Security and Compliance by Design

Cybersecurity is non-negotiable in fintech. Biometric authentication, encryption, and tokenisation protect data integrity, while regulatory features such as AML (Anti-Money Laundering) and KYC (Know Your Customer) ensure compliance.

In the UAE, compliance extends to VAT and Corporate Tax record-keeping, making security and audit-ready documentation a dual priority for fintech adoption.

At Alaan, these same pillars form the backbone of our platform. We combine Visa’s global payment network with cloud-native infrastructure, AI-powered receipt validation, and VAT checks to give finance teams a secure, compliant, and scalable foundation for expense management.

[cta-4]

Also read: Understanding Business Spend Management Tools

Major Use Cases of Fintech in Modern Finance

Fintech is no longer limited to payments. It is embedded across nearly every area of financial services, reshaping how individuals and businesses manage money. For UAE companies, fintech adoption often links directly to compliance, efficiency, and investor expectations.

1. Digital Payments and Wallets

Mobile wallets and contactless payments are now mainstream, with more than half of UAE consumers using them regularly.

- Platforms such as Apple Pay and Google Pay rely on fintech APIs, tokenisation, and encryption.

- The shift away from cash improves accountability, a critical factor for companies that need accurate VAT reporting.

Also read: Understanding Cost Management

2. Lending and SME Credit Access

Fintech lenders use AI-driven credit scoring to assess borrowers quickly, even where traditional credit history is limited.

- Peer-to-peer (P2P) lending platforms offer alternatives to banks.

- For UAE SMEs, this expands access to working capital, often with faster approvals and flexible repayment terms.

3. Insurtech and Regtech

- Insurtech applies AI to underwriting, claims, and customer onboarding, cutting processing times.

- Regtech supports compliance by automating AML checks, KYC verification, and VAT-related documentation.

These technologies are particularly relevant in the UAE, where regulatory fines for non-compliance can significantly impact profitability.

4. Wealth Management and Robo-Advisors

Algorithms now build and rebalance portfolios in real time. Robo-advisors have opened wealth management to individuals and SMEs at lower cost. Increasingly, they also integrate ESG investing.

For UAE-based investors, robo-advisors provide access to global markets while maintaining transparency around fees and performance.

5. Corporate Spend and Expense Automation

Fintech has transformed how companies manage business expenses. Modern expense management platforms integrate corporate cards, automated receipt scanning, and AI-driven categorisation.

This provides real-time visibility into spending, critical for CFOs navigating VAT and Corporate Tax obligations in the UAE.

6. Open Banking and Account Aggregation

Open banking regulations are expanding across the Middle East, including initiatives in the UAE. Businesses can consolidate multiple accounts in one platform, improving cash flow forecasting.

For CFOs, this reduces manual reconciliation work and provides a clearer view of liquidity across entities.

Also read: Improving Internal Control in Financial Reporting

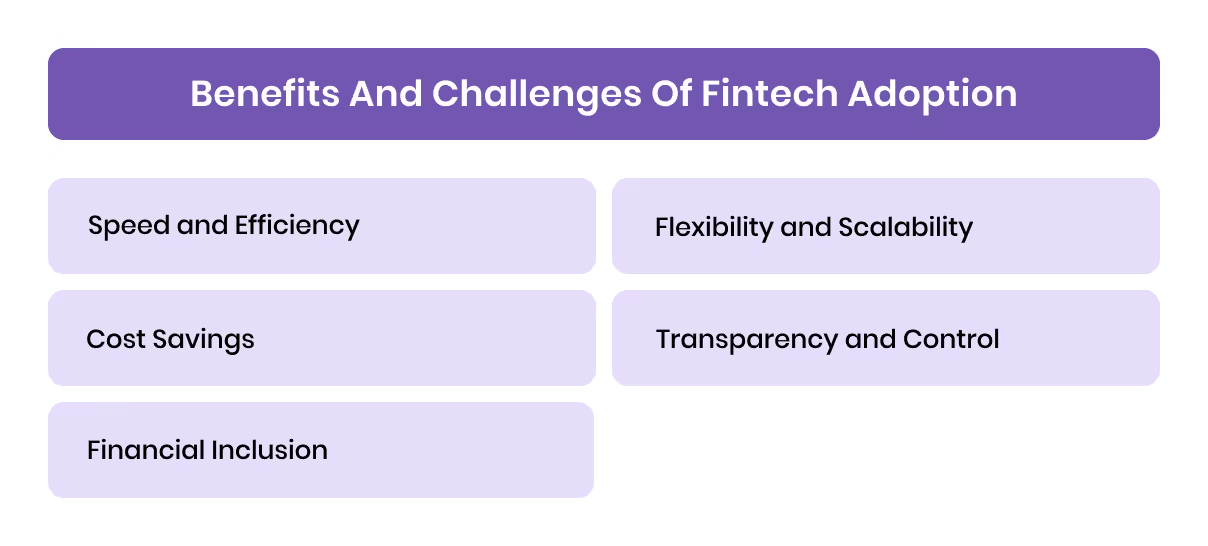

Benefits and Challenges of Fintech Adoption

Like any major shift, fintech adoption delivers both opportunities and risks. For CFOs in the UAE, the key is to capture the efficiency gains while ensuring compliance and security remain intact.

Benefits of Fintech Technology

- Speed and Efficiency

Digital-first infrastructure enables instant payments, faster reconciliations, and real-time reporting. For finance teams dealing with VAT filings or month-end close, this speed directly reduces compliance risks.

- Cost Savings

Automating expense tracking, approvals, and reconciliations reduces manual workload. Cloud-native fintech platforms also cut IT overheads by removing the need for expensive on-premise servers.

- Financial Inclusion

Fintech platforms extend access to credit, savings, and insurance for underbanked SMEs. In the UAE, this is particularly relevant for small businesses and startups that may not qualify for traditional loans.

- Flexibility and Scalability

Cloud systems allow fintech tools to scale with the business — from startups to regional enterprises — without costly infrastructure upgrades.

- Transparency and Control

Real-time dashboards provide audit-ready visibility into spending, helping CFOs prevent budget overruns and maintain investor confidence.

At Alaan, companies adopt our corporate cards not only to cut costs but to gain real-time visibility into every expense, ensuring VAT readiness at all times.

[cta-5]

Challenges of Fintech Technology

- Regulatory Complexity

Fintech often operates across borders, meaning businesses must meet AML, KYC, VAT, and Corporate Tax requirements. For UAE entities, aligning fintech adoption with local compliance frameworks is critical. - Cybersecurity Risks

With data moving across APIs and mobile apps, risks such as phishing, fraud, and identity theft require continuous monitoring and advanced security protocols. - Integration with Legacy Systems

Large enterprises often rely on older ERP or banking systems. Without robust APIs, connecting fintech tools to existing workflows can slow adoption. - Data Privacy and Governance

Finance leaders must ensure platforms comply with GDPR, UAE Central Bank rules, and data residency laws. Mishandling sensitive financial data risks both penalties and reputational damage.

Also read: VAT Compliance Health Check in the UAE

Fintech in the UAE and MENA: Local Context and Trends

The Middle East has rapidly become one of the world’s most dynamic fintech regions, with the UAE leading the charge. A combination of progressive regulation, strong banking infrastructure, and digital-savvy consumers is fuelling adoption at scale.

Regulatory Support Driving Innovation

- Central Bank of the UAE (CBUAE): Introduced regulatory sandboxes to test emerging fintech solutions in a controlled environment.

- Free Zones: The Dubai International Financial Centre (DIFC) and Abu Dhabi Global Market (ADGM) have built fintech hubs that attract startups and global players with flexible licensing and supportive policies.

- Open Banking Frameworks: Regulators in the GCC are mandating secure data-sharing between banks and third-party fintech platforms, paving the way for account aggregation, faster lending, and more integrated spend management.

Rapid Adoption Across Consumers and Businesses

- Over 50% of UAE consumers use digital wallets regularly, according to market studies — a figure expected to climb as contactless payments expand.

- Businesses are digitising core finance functions, moving away from cash-heavy processes such as petty cash funds, which often cause reconciliation delays and compliance risks.

(Also read: Effective Petty Cash Management for UAE Businesses)

UAE-Specific Business Needs

- VAT and Corporate Tax Compliance: With VAT at 5% and Corporate Tax at 9%, finance teams require fintech tools that not only simplify transactions but also validate invoices, extract VAT details, and keep records audit-ready.

- Investor Readiness: Startups in DIFC or ADGM aiming to raise capital face intense scrutiny on financial discipline. Fintech platforms that track burn rates, automate expense approvals, and maintain audit trails improve investor confidence.

- Regional Expansion: Many UAE companies look to expand into Saudi Arabia and the wider GCC. Fintech solutions provide the infrastructure to handle cross-border payments, tax differences, and local compliance rules.

At Alaan, we help UAE companies turning compliance into a competitive edge. By combining corporate cards, VAT validation, and automated reconciliation, finance teams meet regulatory requirements while improving efficiency and visibility.

Also read: Corporate Tax Registration in the UAE

How Businesses Can Adopt Fintech Technology Wisely

Fintech adoption is no longer a “nice to have” for UAE businesses—it is a necessity. But many projects fail when organisations rush into tools without considering compliance, integrations, or cultural readiness. A phased approach reduces risk and ensures maximum value.

1. Assess Business Needs First

Start by identifying the real gaps in your financial processes.

- Are expense claims frequently delayed or rejected?

- Do you struggle to maintain VAT-compliant receipts?

- Are employees frustrated with manual reimbursement cycles?

Mapping these pain points ensures fintech adoption solves practical finance problems instead of becoming another system to manage.

(Also read: Understanding Business Spend Management Tools)

2. Run a Pilot Before Scaling

Instead of a full rollout, test fintech solutions with one department or cost centre. For example, issue digital cards to the sales team for travel and entertainment, then evaluate policy compliance, reporting accuracy, and user adoption.

This pilot approach helps uncover gaps early and build internal champions for broader adoption.

3. Prioritise Compliance and Security

Fintech is only valuable if it passes the compliance test. Businesses in the UAE must ensure any platform can handle:

- AML/KYC checks for onboarding

- VAT validation on receipts and invoices

- Corporate Tax readiness with clean, audit-friendly records

- Data privacy standards in line with UAE Central Bank rules

At Alaan, our spend management platform is designed with these requirements built in—ensuring finance teams remain audit-ready without extra effort.

[cta-6]

(Also read: VAT Compliance Health Check in the UAE)

4. Plan Integrations Early

Fintech delivers maximum impact when connected to the systems you already use. Look for providers with robust APIs and pre-built integrations into:

- ERP systems such as Microsoft Dynamics, Xero, QuickBooks, or NetSuite

- HR and payroll tools for benefits and reimbursement management

- Procurement software for automated vendor payments

This ensures real-time data flows instead of manual uploads.

5. Train Employees and Update Policies

Adoption is not just technical—it’s cultural. Employees need clear guidance on:

- How corporate cards can be used (spend categories, limits)

- Approval workflows for expense submission

- Consequences of policy breaches

Updating internal spend policies alongside fintech rollout helps embed discipline into daily workflows.

(Also read: Effective Business Spending Policies)

6. Monitor and Refine Continuously

Use dashboards to track adoption, spend patterns, and compliance metrics. If a department regularly breaches limits, tighten approval workflows. If VAT filing errors persist, adjust receipt validation rules. Continuous monitoring ensures fintech stays aligned with business goals.

Conclusion

Fintech technology has evolved from credit cards and ATMs in the 1950s to today’s AI-driven, API-first platforms. What started as banking automation has become the foundation of digital payments, expense management, lending, and compliance tools worldwide.

For UAE businesses, fintech adoption is not just about convenience or cost savings. With VAT at 5% and Corporate Tax at 9%, finance teams must maintain precise, audit-ready records. Fintech platforms that combine corporate cards, automated reconciliation, and AI-powered receipt validation are critical to meeting these standards.

At Alaan, we bring fintech innovation directly into corporate finance. Our platform enables companies to issue expense cards instantly, control spending in real time, and stay compliant with UAE tax regulations—while saving hours of manual work every month.

Book a demo today and see how Alaan helps finance leaders simplify spend management and stay ahead in the digital-first economy.

FAQs on Fintech Technology

1. What technologies power fintech?

Fintech is built on APIs, cloud computing, AI/ML, data analytics, and in some cases blockchain. These technologies enable real-time insights, faster payments, and seamless integrations with accounting or ERP systems.

2. When did fintech start?

The concept dates back to the 1950s with credit cards and ATMs. The modern term “fintech” gained traction in the 2010s with open banking, mobile wallets, and AI-powered platforms.

3. Is blockchain essential for fintech?

Not always. While blockchain is valuable for transparent payments and cross-border settlements, many fintech tools—like corporate expense platforms or mobile wallets—operate effectively without it.

4. How is fintech different from traditional banking technology?

Traditional banking relies on legacy IT systems and manual processes. Fintech platforms are modular, API-driven, and cloud-native, designed for speed, scalability, and customer-centric workflows.

5. What are the risks of adopting fintech?

The main risks are cybersecurity threats, regulatory complexity, and integration challenges with legacy systems. UAE companies must also ensure compliance with VAT, Corporate Tax, AML, and data privacy regulations.

6. How can UAE businesses adopt fintech effectively?

Adopt a phased approach: assess business needs, run a pilot, ensure compliance, plan integrations, update spend policies, and monitor results continuously. Partnering with providers like Alaan ensures both compliance and efficiency from day one.