An international payment often seems simple until the final amount does not match the approved figure, vendors start asking questions, and reconciliation stretches into month-end.

For finance teams in the UAE, managing these payments means coordinating approvals, FX exposure, settlement timelines, documentation, and compliance. As organisations expand globally, even small process gaps can quickly turn into major pressure points.

This challenge is especially relevant in a market where 95 % of UAE residents send money internationally at least once a year. It highlights the scale and frequency of cross-border transactions that you are expected to manage with precision.

So, in this blog, you'll take a closer look at how international payment processing works within UAE finance teams. You’ll learn about the key cost drivers, compliance, best practices, and how modern teams are redesigning processes to scale efficiently while maintaining clarity and control.

TL;DR

- Key Cost Factors in International Payments: FX fluctuations, intermediary bank fees, delayed settlements, internal processing, and compliance documentation often push costs beyond transfer fees.

- Payment Methods Used in the UAE: Bank transfers for high-value suppliers, corporate cards for recurring SaaS and digital spend, FX providers for specific corridors, and platform-led transfers for better workflow control.

- Choosing the Right Payment Method: Teams consider vendor type, payment value and frequency, approval requirements, settlement reliability, reconciliation impact, and documentation readiness.

- Best Practices at Scale: Enforce controls before execution, standardise approvals, design for reconciliation, plan for settlement variability, and review workflows regularly.

- Rethinking International Payments in the UAE: Organisations are shifting to control-led workflows with early visibility, fewer manual follow-ups, and stronger alignment with VAT and reporting requirements.

4 True Cost Drivers Behind International Payments

The cost of an international payment rarely matches what appears on the invoice. What gets approved internally and what finally leaves the bank account often don’t line up.

The difference usually hides in small details that are easy to overlook, until payment volumes rise and the impact becomes harder to ignore. Here’s where those hidden costs usually come from.

1. FX Rates and Timing Risk

Foreign exchange often drives the highest cost, yet teams control it the least. Many teams approve payments using indicative FX rates. But by the time they execute the payment, banks may apply a different final rate.

This quickly turns into a budgeting headache where:

- Cash forecasts lose accuracy

- You lose sight of true spending

- Small FX changes add up over time

This hits hardest for businesses that pay overseas vendors regularly or manage subscription payments, where even small rate shifts can create noticeable differences month after month.

Suggested Read: Cash Forecasting Methods CFOs Trust for Accurate Liquidity

2. Intermediary and Correspondent Bank Fees

Most international payments don’t travel straight from sender to recipient. They usually pass through several intermediary banks. Each bank may take a fee, and teams don’t always see these charges upfront.

The fees appear after the payment has gone out, and this makes it harder to:

- Explain payment differences

- Reconcile final amounts

- Understand the real cost of working with certain vendors or regions

Over time, this lack of clarity makes financial planning tougher.

3. Processing Costs Inside the Finance Team

Some of the highest costs never appear on a bank statement. They show up in your team’s day-to-day workload.

Manual reviews, follow-ups, and reconciliations quietly consume hours every week. Some of the common tasks include:

- Checking payment status across multiple systems

- Matching bank confirmations to invoices

- Fixing accounting entries after settlement

These tasks grow with payment volume. As the business expands, the operational effort around international payments grows even faster.

4. Compliance and Documentation Overhead

Cross-border payments usually bring extra compliance requirements. Missing documents, incorrect tax treatment, or incomplete records often lead to rework later. For teams operating in the UAE and across the wider MENA region, this also means ensuring records align with VAT rules where required.

When teams run compliance checks after they send payments, finance pays the price during audits and month-end close through extra reviews, corrections, and delays.

Once you see what drives the true cost of international payments, it becomes easier to understand the different processing methods used in the UAE.

5 Types of International Payment Processing Methods in the UAE

Finance teams in the UAE don’t choose international payment methods solely based on availability. They look at control, cost visibility, settlement reliability, and how easily each payment fits into existing finance workflows.

Below are the main international payment methods used by UAE businesses.

1. Bank Transfers via Correspondent Banking Networks

This remains the most common way to pay international suppliers, especially for high-value or contract-based payments.

Most cross-border bank transfers from the UAE move through the SWIFT network. While SWIFT itself does not settle funds, it enables global communication between banks.

From a finance perspective, bank transfers feel familiar and work almost everywhere. But they also bring challenges that matter as volumes grow:

- FX rates and intermediary fees often get confirmed late

- Settlement timelines change based on corridor and cut-off times

- Payment tracking usually turns manual once funds leave the account

You can use this method when vendors don’t accept cards, but it requires strong internal controls to maintain visibility and reconciliation.

2. Card-Based Payments for International Vendors

Corporate cards are popular for recurring international spend, such as software subscriptions, digital services, and advertising platforms.

For finance leaders, cards offer:

- Faster execution

- Clear transaction records

- Easier reconciliation for smaller, repeat payments

That said, cards don’t work for every vendor. Acceptance limits, transaction caps, and higher charges on large payments mean teams usually reserve cards for specific spend categories rather than core supplier payments.

3. FX and Exchange House Transfers

Some businesses use exchange houses or FX-focused providers to access better rates or specific currency corridors.

While this can help manage FX exposure, it often adds complexity as:

- Approvals and payment execution sit outside core finance systems

- Teams reconcile documentation separately

- Visibility across total spend becomes harder to maintain

Teams using this option need to balance potential FX savings against the extra operational effort.

4. Letters of Credit

For import-export, manufacturing, or commodity-driven businesses in the UAE, Letters of Credit (LCs) are sometimes used to reduce counterparty risk in high-value cross-border transactions.

Under this structure, a bank guarantees payment to the supplier once predefined documentation and shipment conditions are met.

Finance teams typically rely on LCs when:

- Transaction values are large

- Vendor relationships are new

- Shipment or delivery risks require mitigation

While LCs provide stronger payment security, they also introduce:

- Additional bank charges

- Documentation complexity

- Longer processing timelines

- Increased administrative workload

For most modern, service-based UAE businesses, LCs are used selectively rather than for routine international supplier payments.

5. Platform-Led Cross-Border Transfers

Newer platforms bring together payment execution, spend controls, approvals, and record-keeping.

The value isn’t just in moving money but in the ability to:

- Review the total cost before approval

- Keep approvals, invoices, and payment data connected

- Reduce manual reconciliation later

This approach works well for teams that want international payments to stay close to their existing spend workflows rather than treating them as isolated banking tasks.

Choosing the right international payment method usually comes down to payment value and frequency, vendor acceptance and urgency, required approval levels, and impact on reconciliation and reporting.

At Alaan, we enable international transfers alongside approvals, spend controls, and reconciliation in one connected workflow, so finance teams can manage cross-border payments with greater visibility and accountability. This allows teams to manage cross-border payments without treating them as isolated banking tasks.

Understanding the various international payment methods in the UAE also helps clarify the compliance requirements you must follow.

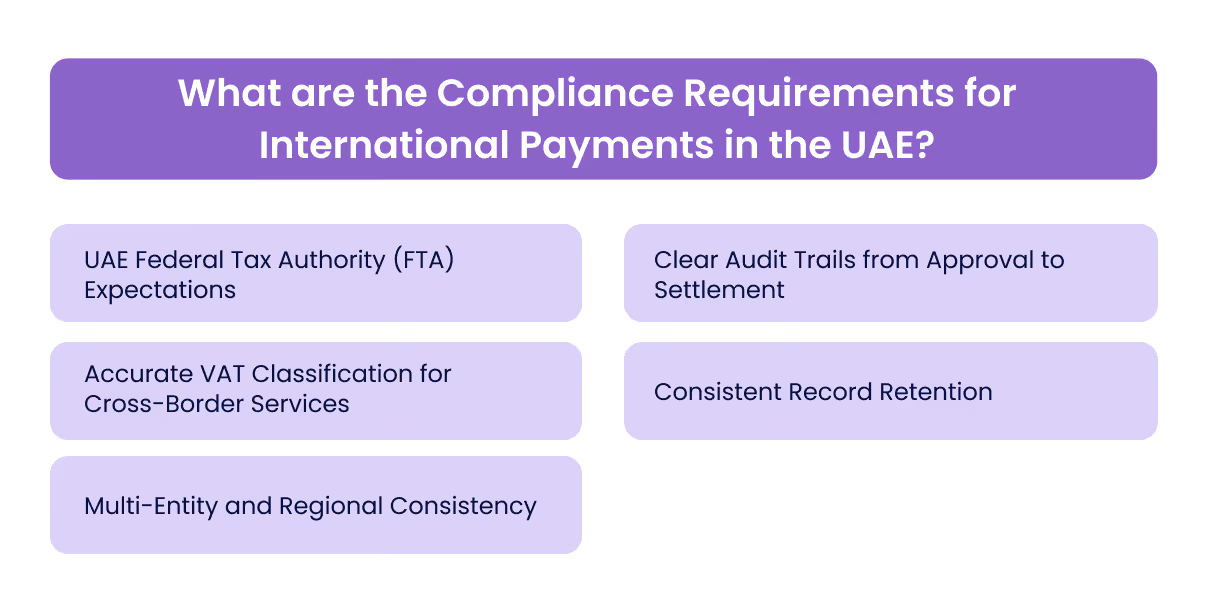

What are the Compliance Requirements for International Payments in the UAE?

International payments carry a higher compliance burden than domestic transactions for UAE finance teams. The risk comes from incomplete documentation, weak traceability, and gaps between execution and record-keeping.

As cross-border volumes grow, processes need to withstand regulatory review without relying on manual reconstruction later. Below are the compliance requirements for international payment processes in the UAE.

1. UAE Federal Tax Authority (FTA) Expectations

The FTA requires businesses to retain sufficient records to support VAT treatment, even when VAT is not charged on a cross-border payment. This includes invoices, contracts, and payment confirmations that clearly explain the nature of the transaction and the place of supply.

2. Clear Audit Trails from Approval to Settlement

You must show how each payment was approved, executed, and recorded. When approvals, invoices, and bank confirmations exist in separate systems, audit preparation becomes time-consuming and error-prone.

3. Accurate VAT Classification for Cross-Border Services

International payments often relate to services that may be zero-rated, out of scope, or taxable, depending on the type of service and jurisdiction. Correct classification at the time of payment helps avoid corrections during VAT reviews.

Also Read: Filing and Making VAT Payments in UAE

4. Consistent Record Retention

UAE regulations require financial records to be retained for several years; a commonly cited baseline is 5 years. Fragmented storage of invoices and payment evidence increases audit effort and risk, especially as staff or systems change.

5. Multi-Entity and Regional Consistency

For organisations operating across multiple UAE entities or the wider MENA region, documentation standards must stay consistent. Inconsistent practices complicate consolidated reporting and raise questions during audits.

Knowing the compliance requirements for international payments in the UAE lays the groundwork for implementing best practices to manage the process efficiently at scale.

8 Best Practices for Managing the International Payment Process at Scale

As international payment volumes grow, small inefficiencies turn into repeat problems. What worked when payments were occasional stopped working once cross-border spending became routine.

So, here are some of the best practices for managing the international payment process at scale:

1. Tailor Payment Approaches to Vendor Relationships

Adjust your payment method based on how you work with each vendor. Recurring international vendors need consistent, predictable payments, while one-off or project-based vendors require speed and full documentation.

Tip: Separate recurring and ad hoc payments to match risk profiles and avoid applying a single approach to very different vendor types.

2. Apply Control Measures Before Funds Move

Focus on pre-spend controls rather than post-payment corrections. Strong processes ensure:

- Approvals are completed before execution

- Payable amounts are verified in advance

- Limits, policies, and restrictions are applied upfront

Tip: Shift from reactive reconciliation to proactive control to avoid month-end cleanup.

3. Gain Full Cost Visibility Beyond Fees

Evaluate payment methods based on total cost, including FX handling, intermediary charges, and rate timing.

Tip: Surface all costs before approval to improve budgeting and reduce reconciliation friction.

4. Monitor Settlement Timing and Operational Impact

Settlement speed affects vendor relationships and internal operations. You need to track:

- Typical settlement timelines by corridor

- Variability across currencies

- Likelihood of follow-ups or exceptions

Tip: Prioritise predictable settlement to reduce operational noise and improve vendor confidence.

Must Read: 10 Proven Vendor Management Strategies for UAE Companies

5. Integrate International Payments Into Core Workflows

Separate systems for approvals, execution, and reconciliation reduce visibility into the process. High-performing teams:

- Own the process end-to-end

- Set clear checkpoints before funds move

- Keep approvals, payment data, and documentation connected

Tip: Embed international payments into your core finance workflows to reduce handoffs and maintain accountability.

6. Standardise Requests and Approval Logic

Ad hoc requests create delays at scale. Consistency ensures smooth operations:

- Include required documentation with every payment request

- Follow the same approval paths across departments

- Make exceptions easy to identify and review

Tip: Implement standard templates and workflows to reduce friction and errors.

7. Design Reconciliation From the Start

Reconciliation is where most teams lose time. Best practices include:

- Matching payments cleanly to invoices

- Ensuring reference data flows into accounting records

- Keeping documentation ready before the month-end

Tip: Build reconciliation into the payment workflow to reduce closing pressure and manual effort.

At Alaan, we keep international payment data, documents, and approvals connected to each transaction. This reduces manual effort and helps simplify the closing process.

8. Adapt Processes as Volumes Grow

Growth introduces new vendors, regions, and regulations. Finance leaders who stay proactive:

- Spot bottlenecks early

- Adjust approval thresholds as risk evolves

- Remove manual steps before they become structural issues

Tip: Continuously review workflows to maintain predictability, control, and visibility as the business scales.

Applying best practices at scale is also shaping how finance teams in the UAE are rethinking their international payments approach.

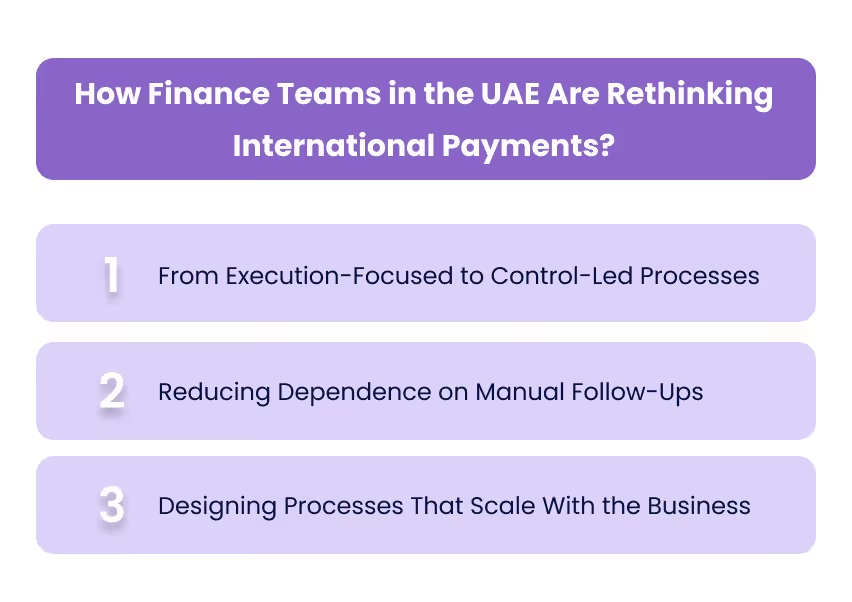

How Finance Teams in the UAE Are Rethinking International Payments?

Finance teams in the UAE are feeling pressure from both sides. Businesses are expanding globally, while regulatory and reporting expectations continue to tighten. International payments, once handled as routine bank transfers, now sit at the center of financial operations.

Here’s how finance teams are rethinking international payments:

1. From Execution-Focused to Control-Led Processes

In the past, teams measured success by whether they sent payments on time. Today, finance leaders care just as much about what happens before and after execution.

Teams now focus on:

- Clear approvals before funds move

- Visibility into total cost before confirmation

- Documentation readiness at the point of payment

This shift reflects a broader move toward stronger governance without slowing the business.

2. Reducing Dependence on Manual Follow-Ups

As international payment volumes grow, manual tracking no longer works. Finance teams in the UAE are cutting back on emails, spreadsheets, and ad hoc status checks.

Instead, they are reshaping workflows so that:

- Teams can see payment status without chasing banks

- Vendors get timely confirmation

- Finance spends less time handling escalations

The goal is to make international payments quieter and easier to manage day to day.

3. Designing Processes That Scale With the Business

Many organisations are expanding across regions, entities, and vendor networks. Finance teams now realise international payment processes must scale without adding headcount.

That means prioritising:

- Consistent approval structures

- Predictable settlement handling

- Clean handoff to reconciliation and reporting

Processes that worked at low volume are giving way to ones built for long-term growth.

How Alaan Simplifies International Payments for UAE Finance Teams?

Many finance teams in the UAE handle international payments outside their main spend systems. Corporate cards usually cover SaaS, advertising, and employee expenses.

But international suppliers, imports, and bulk vendor payments often go through separate bank transfers, exchange houses, or standalone FX tools. This breaks visibility and makes control harder as volumes grow.

Super Pay brings international payments into the same platform teams already use to manage business spend, approvals, and reconciliation. It works alongside existing banks and payment providers and does not replace them.

What Alaan Covers Beyond Just the Transfer

Alaan goes beyond cross-border payments. It combines international transfers with spend and finance controls that support the payment process before and after funds move.

1. Cross-Border Transfers With Upfront Cost Visibility

You can see FX rates and the expected total payable amount before approving a transfer. This lets teams review costs earlier in the approval flow, rather than only spotting differences after settlement.

Cross-border payments are currently available on selected corridors in Phase 1, with additional corridors expected over time.

2. Two-Level Approval Workflows

Separate invoice and payment approval workflows help you review and approve payments before authorising the transfer. This structure works especially well for higher-value or higher-risk international payments where teams need extra oversight.

3. Centralised Vendor and Beneficiary Management

Alaan stores supplier and beneficiary details, supporting documents, and payment history in one place. Teams can reuse verified details across payments and maintain consistent records.

This central setup reduces friction during first-time payments and supports more consistent payment execution for repeat vendors.

4. Integrated Spend

Unlike FX-only tools, Alaan also supports:

- Corporate cards for SaaS, advertising, and employee spend

- Expense tracking and receipt capture

- Email invoice forwarding

- Automated checks, such as identifying duplicates and capturing tax invoice details

This lets you manage local spend and international payments in a single system, rather than stitching together multiple tools.

5. Cleaner Reconciliation and Accounting Sync

Payment data, FX details, invoices, and approvals stay connected and sync with accounting systems. This creates a cleaner handoff to accounting and helps simplify reconciliation during month-end close.

By keeping payment context tied to each transaction, you can spend less time rebuilding information or explaining FX and fee differences later.

What Alaan Is (And Is Not)

Alaan is not a bank and does not replace existing banking relationships.

Super Pay works alongside banks and payment providers to give finance teams better visibility and structure across the international payment process, especially for payments where cards don’t fit.

Final Thoughts

International payment processing is critical for UAE businesses, but it doesn’t have to be unpredictable. Most issues, like unexpected FX differences, delayed settlements, reconciliation gaps, and vendor follow-ups, arise from fragmented workflows and late-stage visibility.

Finance teams that bring structure to approvals, understand the true cost before execution, and keep documentation linked to each transaction gain more than just efficiency. They protect cash flow forecasts, reduce operational noise, and maintain control as international spend grows across currencies and regions.

At Alaan, we support this shift by bringing international payment processing into a single, connected workflow. From upfront cost visibility and structured approvals to smoother reconciliation, we help finance teams manage cross-border payments with greater clarity, without replacing existing banks or adding complexity.

Schedule a free demo to see how Alaan helps finance teams in the UAE simplify international payment workflows and improve cost visibility.

FAQs

Q1. What risks do finance teams face when international payments are handled outside core finance systems?

A1. When international payments happen outside core workflows, finance teams lose early visibility into costs, approvals, and documentation. This leads to heavier reconciliation work, weaker audit trails, and a higher chance of issues surfacing late during month-end close or compliance reviews.

Q2. How is international payment processing different from domestic payment processing?

A2. International payment processing involves multiple currencies, cross-border settlement networks, and intermediary banks, all of which affect cost visibility and settlement timelines. Domestic payments typically move faster, with clearer fees and simpler reconciliation, since they stay within a single banking system.

Q3. How do international payment processes impact vendor negotiations and contracts?

A3. Payment predictability builds vendor trust. However, delays, unexpected deductions, or inconsistent settlement timelines can influence contract terms and service levels. Teams that manage payments more closely often gain greater leverage in vendor discussions over pricing, timelines, and penalties.

Q4. When should finance teams review or redesign their international payment process?

A4. A review usually makes sense when payment volumes grow, new regions or currencies are added, or month-end reconciliation starts taking longer than expected. Regular vendor follow-ups, FX variances, or compliance exceptions are also clear signs that the current process is no longer scaling.

Q5. How does VAT consideration change for international payments in the UAE?

A5. Not all cross-border payments are subject to VAT, but finance teams still need clear documentation and accurate classification to support the VAT treatment, where applicable. Gaps in records or delayed checks can complicate VAT reviews and audits, especially when payments span multiple jurisdictions.