Moving funds between the UAE and the UK is routine across both personal and commercial contexts, from vendor settlements and property commitments to education payments and treasury flows. This corridor sits within a much larger ecosystem of outbound transfers: personal remittances from the UAE alone reached roughly AED 183 billion in 2024, underscoring the scale and frequency with which money moves across borders from the region.

At a structural level, the UAE’s cross-border remittance market is valued at about $39 billion (AED 143 billion), driven by a predominantly expatriate population and extensive international business connectivity. These dynamics make transfer execution not just a financial routine, but an operational capability that organisations and individuals rely on daily.

While the mechanics of sending money are straightforward, outcomes vary significantly depending on preparation quality, routing choice, and cost awareness. Transfers commonly settle within one to three working days through standard bank channels, yet timing and total cost depend on cut-off windows, intermediary handling, and exchange-rate treatment.

This guide focuses on execution discipline, outlining required information, behavioural differences across transfer routes, and the financial considerations UAE-based senders should evaluate before initiating payments.

TL;DR (Key Takeaways)

- Cross-border payments are a workflow problem disguised as a transaction. Cost, delays, and reconciliation issues usually originate upstream in data accuracy, documentation discipline, and approval structure, not in the transfer mechanism itself.

- Provider comparison should model outcomes, not features. Evaluating transfers by “speed” or “fees” misses the economic reality; modelling landed value, FX exposure, and audit traceability yields materially better decision-making.

- Execution rails segment by organisational maturity. As transaction complexity rises, organisations naturally shift from convenience-driven channels to those optimised for governance, capital efficiency, and reporting continuity.

- Settlement variability is systemic, not exceptional. Routing dependencies, screening logic, and banking cycles make timing probabilistic rather than deterministic; operational resilience comes from expectation management and process standardisation.

- Payment performance improves when embedded in spend governance. Embedding transfers within invoice capture, structured approvals, and accounting linkage, as enabled by platforms like Alaan, reduces friction across the full payment lifecycle rather than optimising a single transaction event.

Information You Need Before Initiating A Transfer

Preparation prevents delays more reliably than provider choice. Most outward transfers fail or stall because beneficiary or compliance inputs are incomplete rather than because of payment-rail limitations.

Recipient Banking Details

You should collect and verify:

- Recipient full legal name

- UK bank account details or IBAN

- Bank identifier where required

UK IBANs consist of 22 alphanumeric characters encoding country code, bank identifier, and account routing data, enabling accurate cross-border settlement.

Sender Identification And Purpose

Typical onboarding and transaction checks require:

- Valid ID such as Emirates ID or passport

- Proof of address

- Transfer purpose description

For larger transactions, institutions may request documentation validating the source of funds or the commercial nature of the payment.

Operational Inputs

Before submitting the payment:

- Ensure funds are available

- Confirm routing codes if applicable

- Add the beneficiary in advance within online banking

International transfer workflows require beneficiary setup before execution, after which recurring or scheduled payments can be configured.

Main Methods Used To Send Money From UAE To UK

Payment rails differ in pricing structure, execution speed, and operational suitability. Selection should reflect transaction size, urgency, and governance requirements.

1. Traditional Bank Transfers

This remains the default option for structured or high-value payments. Transfers initiated through UAE banks typically reach UK accounts within two to three working days depending on receiving-bank processing and submission timing.

Banks may charge telegraphic transfer fees alongside foreign-exchange spreads, and exchange rate markups can materially increase the total cost of larger transfers.

Typical use cases include:

- Supplier or payroll settlements

- Intercompany transfers

- Transactions requiring audit traceability

Initiating transfers before cut-off windows can enable same-day processing on the sending side, while delays may occur if requests are submitted later in the day or around weekends and holidays.

Also Read: Building a Robust Cash Management Control System for UAE Businesses

2. Exchange And Specialist Currency Providers

Currency specialists focus primarily on exchange optimisation rather than banking services. As a result, they often deliver tighter spreads and lower fees than traditional banks, particularly for larger transactions.

Advantages typically include:

- Exchange rates closer to market levels

- Minimal or zero transfer fees

- Advisory support on timing and rate locking

Transfers usually settle within one to two working days depending on provider routing arrangements.

This route is commonly selected for:

- Property-related payments

- Treasury or capital transfers

- High-value one-off remittances

Also Read: Cash Flow Optimisation Strategies for UAE Businesses in 2025

3. Digital Platforms And App Based Transfers

Digital transfer platforms are increasingly used for routine international payments where visibility into fees and exchange rates matters more than branch support. These services operate under regulatory oversight in the UAE payments ecosystem and follow customer-verification and monitoring requirements similar to banks and exchange houses.

Execution is generally simple: create an account, complete identity verification, add a recipient, and fund the transfer from a bank account or balance wallet. Identification checks typically require a passport or Emirates ID to confirm customer identity before transactions proceed.

Transfer behaviour varies by provider and routing model:

- Some digital rails deliver near-instant settlement when liquidity is pre-positioned in the destination market.

- Others follow standard international clearing timelines comparable to SWIFT routing.

- Most show the final amount received before execution, allowing users to evaluate landed cost rather than just fees.

Digital transfers are commonly used for:

- Regular personal remittances

- Freelancer or contractor payments

- SME vendor settlements where accounting integration is not critical

Also Read: Guide to Modern Expense Management Practices

4. Money Transfer Operators And Cash Access Options

Licensed exchange houses and remittance operators remain heavily used in the UAE due to branch accessibility and familiarity. These providers are regulated by the Central Bank, which licenses and supervises institutions to ensure operational and governance standards are met before they serve customers.

Transfers through this channel usually require basic due-diligence verification:

- Emirates ID or passport

- Visa copy where applicable

- Transaction purpose and source-of-funds validation

Such checks align with AML and customer-due-diligence obligations designed to ensure the legitimacy of funds and reduce misuse of the financial system.

Operationally, these operators provide flexibility:

- Bank account credit in the UK

- Physical branch initiation support

- Cash-based settlement alternatives where required

They are often selected for convenience or familiarity rather than workflow integration, especially for lower-value personal transfers.

Also Read: Why and How to Separate Personal and Business Finances

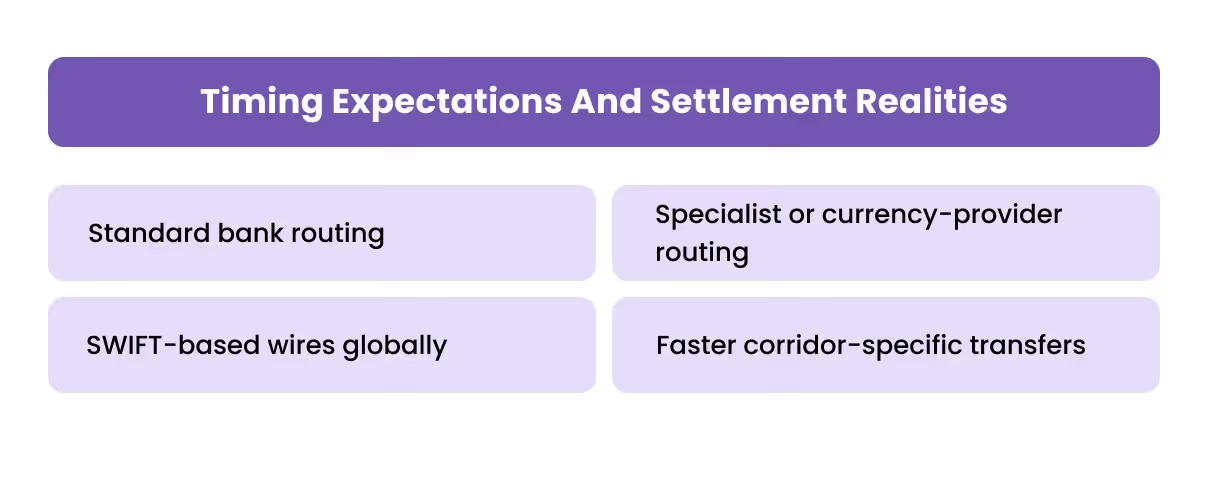

Timing Expectations And Settlement Realities

Understanding realistic timelines prevents unnecessary escalation when funds are in transit. International payments move through multiple clearing stages, so arrival time depends on routing path, cut-off timing, and receiving-bank handling.

Typical patterns across the UAE→UK corridor include:

- Standard bank routing:

- Around 2–3 working days in many cases

- Sometimes 3–5 working days depending on currency path or intermediaries

- SWIFT-based wires globally:

- Often between 1–5 working days end-to-end

- Specialist or currency-provider routing:

- Settlement frequently within 1–2 working days after funding

- Faster corridor-specific transfers:

- Some services estimate arrival in 1–3 working days depending on the receiving country and bank scrutiny levels

Timing variability is driven primarily by:

- Submission cut-off windows

- Currency conversion steps

- Compliance screening

- Receiving-bank processing

International wires generally fall into the one-to-five-day envelope across markets.

Also Read: Cash Flow Forecasting: Best Practices and Key Methods

Cost Comparison And FX Evaluation Framework

Transfer cost rarely comes from the line item labelled “fee.” In cross-border payments, exchange-rate margin and routing deductions typically outweigh visible charges. Evaluating cost correctly requires separating these components rather than focusing on the advertised headline price.

1. Visible Transfer Fees

Banks often charge a fixed outward remittance fee that can range roughly between £5 and £25 depending on institution and corridor.

Within the UAE market, comparable bank-style outward transfers are frequently priced around AED 75–150 per transaction.

These costs are predictable and appear clearly before execution, making them easy to compare but rarely the largest cost driver.

2. Exchange Rate Margin

Providers typically apply a markup to the mid-market exchange rate rather than passing the market rate directly to the customer. Bank spreads commonly sit in the 3–5 % range, while specialist providers or fintech rails may narrow spreads closer to 0.5–1.5 %.

Because the spread scales with transfer value, it becomes the dominant cost component. Even modest percentage differences materially affect high-value transfers.

3. Intermediary And Receiving Charges

Payments routed through correspondent banking networks may incur deductions from intermediary institutions, typically between £5–10 each, alongside possible receiving-bank processing fees.

These deductions are often not visible upfront and may only appear after settlement, creating reconciliation gaps for finance teams.

4. Practical Evaluation Approach

Before execution:

- Compare provider rate vs mid-market reference

- Calculate spread impact on total value

- Confirm visible fees

- Check potential routing deductions

This produces a truer landed-value comparison than a fee-only evaluation.

Also Read: Cost Management in UAE: Key Steps, Benefits & Proven Strategies for 2025

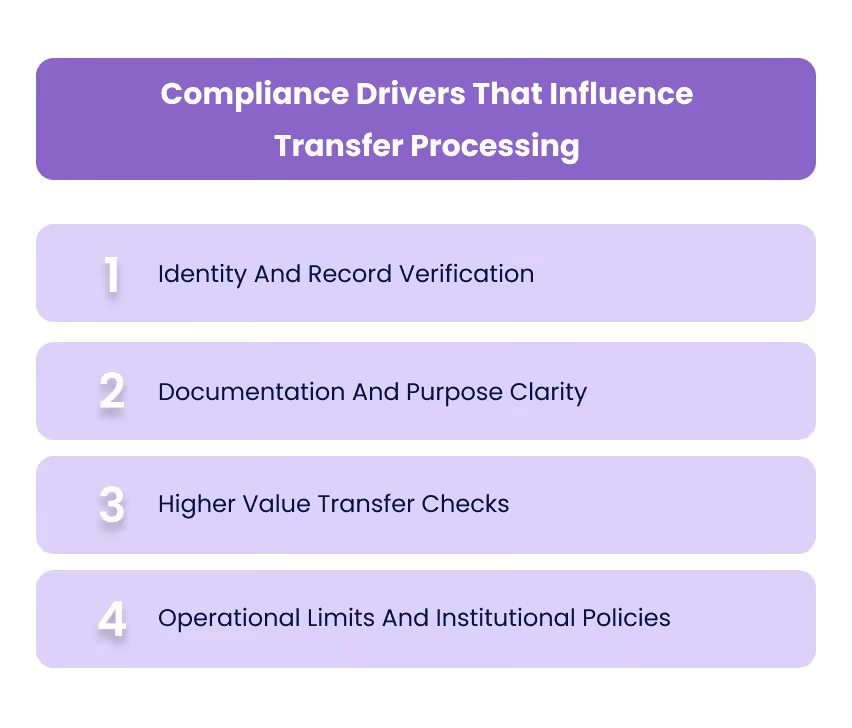

Compliance Drivers That Influence Transfer Processing

Cross-border transfers operate within regulatory frameworks designed to prevent misuse of the financial system. These checks influence both documentation requirements and processing behaviour.

Identity And Record Verification

Financial institutions must verify sender identity once transaction thresholds are reached, around AED 2,000 equivalent for exchange houses and AED 3,500 for banks, and maintain transaction monitoring processes.

For larger or unusual transfers, enhanced due diligence may include documentation confirming income source, transaction purpose, or beneficiary relationship.

Documentation And Purpose Clarity

Incomplete beneficiary details or vague transfer descriptions can cause rejections or holds, since payment data must align with the sender’s activity profile and declared purpose.

Maintaining standard templates and copying official legal entity names directly from contracts reduces rejection risk.

Higher Value Transfer Checks

Outward transfers above certain thresholds may trigger additional source-of-funds verification and record-keeping obligations, particularly for cash-originated funds or aggregated activity.

Operational Limits And Institutional Policies

Although UAE regulation generally does not impose a strict cap on legitimate outward remittances, exchange houses and providers frequently set operational limits and documentation thresholds internally.

These compliance checks are routine and should be treated as workflow expectations rather than exceptions.

Also Read: Spending Policy for Businesses: A Complete Compliance Guide

Common Causes Of Payment Delays Or Exceptions

Transfer delays usually result from input or workflow issues rather than infrastructure failure.

1. Incorrect Beneficiary Data

Missing IBANs, partial legal names, or inconsistent addresses can cause receiving banks to reject or return payments for clarification.

2. Documentation Mismatch

Transfers where invoices, purpose descriptions, or sender details do not align with institutional expectations may pause while clarification is requested.

3. Compliance Screening

Large or irregular payments frequently undergo additional verification checks involving source-of-fund confirmation or beneficiary validation.

4. Routing Deductions And Investigations

Intermediary bank deductions or amendment requests can extend settlement timelines and introduce extra costs if payment instructions require correction.

Finance teams that standardise payment templates and documentation typically experience fewer exceptions across recurring transfers.

Also Read: Importance and Steps in Account Reconciliation

How Alaan Fits Into UAE To UK Business Payments

For many organisations, sending funds to the UK is not technically difficult. The friction tends to arise around preparation and follow-through invoices arriving across channels, approvals handled outside payment systems, and reconciliation rebuilt later from bank references. This fragmentation introduces delays, duplicated work, and avoidable exceptions.

At Alaan, through Super Pay, we support UAE finance teams by connecting the steps around cross-border supplier payments so governance and documentation remain intact across the workflow.

- Invoice Capture And Validation Before Scheduling

Invoices can be captured centrally and reviewed before any transfer is scheduled. Validating supplier details, amounts, and documentation at this stage reduces routing errors and compliance queries when payments are sent to UK accounts. - Approval Separation For Spend And Timing Decisions

Approval workflows distinguish between validating the legitimacy of a cost and deciding when funds should be released. This structure allows finance teams to align GBP settlements with liquidity planning rather than approving execution under time pressure. - Transfers Executed Through Super Pay Within Supported Corridors

For supplier or vendor payments requiring bank-account settlement, transfers to supported corridors, including the United Kingdom, can be executed within the same governed environment where approvals occur. Keeping execution within this context preserves audit trails and reduces switching between disconnected tools. - Visibility Into Expected Cost Before Execution

Before approving supported international transfers, finance teams can review cost implications. This allows decisions to be made with clearer information and supports more predictable planning of cross-currency outflows. - Linked Records For Reconciliation And Reporting

Invoice records, approvals, and payment references remain connected and synchronise with accounting integrations. This continuity reduces manual tracing and supports faster response to supplier queries, internal reviews, or audit checks.

By embedding transfer execution within structured approvals and record continuity, we help organisations send international supplier payments while maintaining visibility and documentation discipline across the payment lifecycle.

Also Read: Understanding the Procure-to-Pay (P2P) Process

Conclusion

Sending money from the UAE to the UK is operationally straightforward when approached as a structured process. Preparation of beneficiary details, understanding cost drivers, and selecting the correct execution rail all materially affect outcomes. Most transfers reach UK accounts within one to four working days depending on routing and verification factors, though faster rails can complete within minutes or hours under supported conditions.

For businesses, the priority extends beyond execution speed, visibility, documentation consistency, and reconciliation readiness shape long-term financial efficiency. Connecting invoices, approvals, execution, and accounting records reduces exception handling and supports predictable financial reporting.

At Alaan, we help UAE finance teams govern cross-border payments within a unified workflow so international transfers align with approval structures and accounting outcomes from the outset. To evaluate how your current payment process compares, schedule a demo with our team and review practical benchmarks tailored to your organisation.

FAQs

1. How Much Money Can I Legally Send From UAE To UK?

Electronic transfers generally face no legal cap between the two countries, as both operate without exchange controls. However, individual banks may impose their own daily transaction limits.

2. Do I Need An IBAN To Send Money To The UK?

Yes. UK transfers commonly require the beneficiary’s IBAN or equivalent banking identifiers to ensure routing accuracy and prevent settlement failure.

3. How Fast Is The Fastest Possible Transfer?

Depending on service and corridor configuration, transfers can arrive within minutes or hours, while standard bank wires typically take several business days.

4. Will I Be Taxed In The UK For Sending Savings Home?

Tax exposure depends on residency status and source of earnings rather than the act of transferring funds itself. UK tax treatment is assessed based on where the income was earned and residency classification.

5. What Documents Might Be Requested For Large Transfers?

Institutions may request source-of-fund documentation, such as bank statements, contracts, or income records, when transfers exceed typical thresholds or trigger verification checks.

6. Why Do Exchange Rates Matter More Than Fees?

Exchange-rate markups can represent the largest component of total transfer cost, often exceeding fixed transaction fees and significantly affecting received value.