Cash flow problems are rarely caused by a single “bad month”. More often, they come from a timing gap: you pay suppliers, payroll, rent, and tax on schedule, but customer cash arrives late, unpredictably, or after disputes.

In the UAE, this timing risk is not theoretical. Surveys of UAE businesses show late payments affect about 56% of B2B invoices, with typical payment terms sitting around 40–50 days from invoicing, meaning a large share of revenue is structurally slower to convert into cash.

That matters even more because SMEs make up roughly 94% of UAE businesses, so liquidity pressure is widespread, not niche.

The goal of improving cash flow is not aggressive cost-cutting. It is shortening the time between cash leaving the business and cash returning by tightening receivables discipline, managing payables intentionally, reducing cash tied up in inventory and operational leakage, and forecasting early enough to make decisions before pressure hits.

TL;DR

- Cash flow strength comes from timing discipline, not just profitability. Liquidity improves when businesses shorten collection cycles, schedule payments intentionally, and avoid capital being trapped in working assets.

- Receivables are usually the fastest lever. Prompt invoicing, clear terms, dispute prevention, and structured follow-ups reduce unpredictability without pressuring customers.

- Payables should be managed strategically, not delayed blindly. Using agreed credit periods fully, aligning payment cycles, and separating approval from payment timing preserves liquidity while maintaining supplier trust.

- Inventory and spend visibility release tied-up capital. Faster turnover, demand-aligned purchasing, and tighter procurement governance free cash otherwise locked in stock or leakage.

- With tools like Alaan providing real-time spend monitoring, structured approvals, and documentation capture, finance teams can align commitments with cash position before funds exit the business.

What Improving Cash Flow Actually Means

Improving cash flow means improving liquidity. Practically, that comes down to managing how quickly you turn operating activity into cash, and how predictably you can meet short-term obligations.

Profit Is Not Cash

Profit is affected by accounting timing (revenue recognition, accruals), while cash flow reflects when money actually moves. If customers pay late, inventory builds, or spend is committed without visibility, cash can tighten even when reported profit looks stable.

The Working Capital Lens

A useful way to frame this is the cash conversion cycle, which measures how long cash is tied up between paying suppliers and collecting from customers. A common expression uses inventory days, receivables days, and payables days.

In most businesses, cash flow improvement comes from tightening a small set of levers:

- Collect Faster (reduce receivables delay)

- Pay Smarter (use payables terms intentionally)

- Tie Up Less Cash (reduce inventory and prevent leakage)

Also Read: Building a Robust Cash Management Control System for UAE Businesses

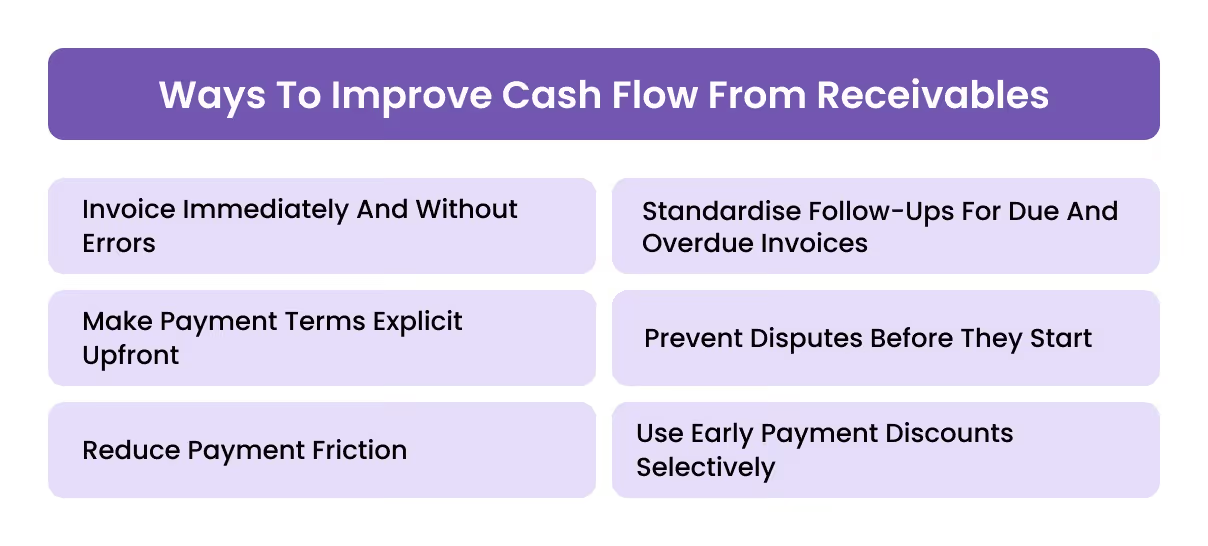

Ways To Improve Cash Flow From Receivables

Receivables are often the fastest place to improve cash flow because small process fixes can reduce delays, disputes, and “lost invoice” friction. The aim is not to pressure customers. It is to remove avoidable reasons for late payment and make collections predictable.

1. Invoice Immediately And Without Errors

Late invoicing and incorrect details create delays that compound. The longer an invoice takes to raise, the later it gets paid.

2. Make Payment Terms Explicit Upfront

Terms need to be unambiguous: due date logic, accepted payment methods, and what happens when the invoice is disputed.

3. Reduce Payment Friction

If paying is inconvenient, it becomes procrastinated. Enable simple payment routes appropriate to the customer relationship and value.

4. Standardise Follow-Ups For Due And Overdue Invoices

A consistent cadence reduces “surprise chasing” and prevents receivables ageing silently.

5. Prevent Disputes Before They Start

Many delays are not refusal to pay; they are mismatches in purchase order references, delivery confirmation, or service scope. Build a checklist for what must be present on every invoice for your typical customer type.

6. Use Early Payment Discounts Selectively

Discounts can improve cash timing, but only when the economics work. If the discount costs more than your realistic financing cost or gross margin trade-off, it is not a win.

Also Read: Step-by-Step Automated Invoice Processing and its Benefits

Ways To Improve Cash Flow From Payables

Improving cash flow through payables is not about delaying suppliers indiscriminately. It is about managing timing intentionally so liquidity is preserved without damaging supplier relationships or pricing power. Payables are one of the core components of working capital, alongside receivables and inventory, and their interaction directly affects a firm’s ability to meet obligations and maintain operations.

1. Negotiate Payment Terms That Reflect Business Volume

Suppliers often adjust credit periods based on reliability and purchase scale. Extending terms by even a few days meaningfully affects liquidity without altering operating activity.

2. Use The Full Agreed Credit Period

Paying earlier than required provides no liquidity benefit unless a financial incentive exists. Working capital trade-offs arise when cash leaves the business earlier than necessary.

3. Evaluate Early Payment Discounts Rationally

Discounts should be accepted only when the effective return exceeds the business’s financing cost or opportunity cost of cash.

4. Structure Payment Cycles For Visibility

Consolidating payments into planned cycles improves forecasting clarity and avoids fragmented outflows that distort liquidity planning.

5. Separate Approval From Payment Timing

Validating spend immediately while scheduling payments later preserves control and flexibility, a practical working capital discipline.

Also Read: Accounts Payable Automation and Invoice Management Software

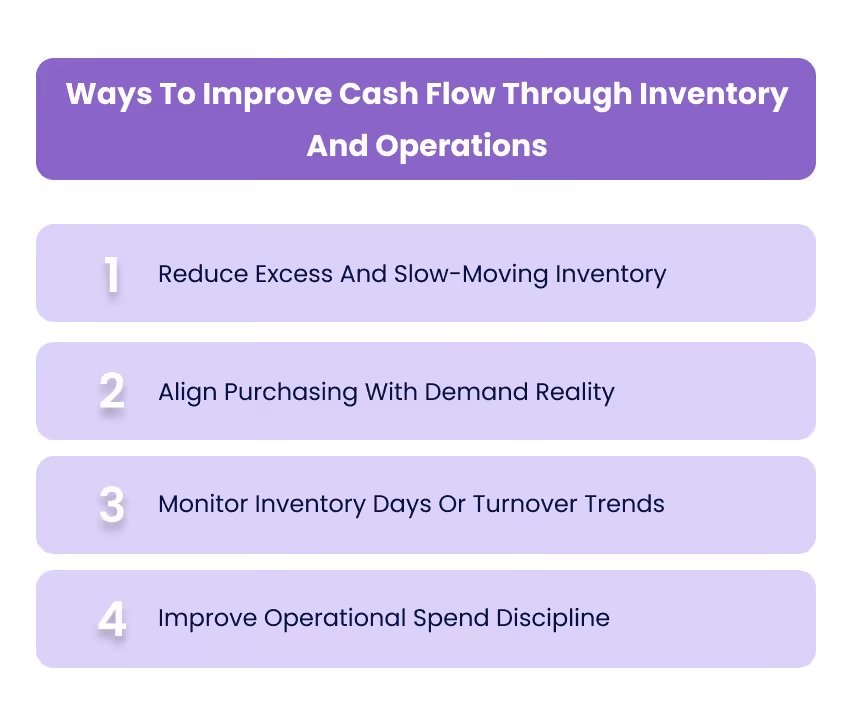

Ways To Improve Cash Flow Through Inventory And Operations

Inventory frequently ties up more cash than owners realise. Capital invested in stock generates little return while sitting unsold, and excess working capital can reduce overall profitability.

Inventory efficiency is commonly assessed using turnover, a measure of how often stock is sold and replaced during a period. Low turnover signals excess stock and tied-up capital, while higher turnover indicates faster movement and more efficient use of cash.

1. Reduce Excess And Slow-Moving Inventory

Overstocking locks liquidity into assets that earn no return. Faster turnover frees capital for operations or growth initiatives.

2. Align Purchasing With Demand Reality

Inventory turnover calculations based on cost of goods sold and average inventory help inform purchasing decisions and pricing strategy.

3. Monitor Inventory Days Or Turnover Trends

Tracking movement across periods reveals whether the stock is becoming inefficiently held. Holding costs and obsolescence risks increase when turnover declines.

4. Improve Operational Spend Discipline

Untracked or uncontrolled operational purchases indirectly inflate inventory-related cash commitments. Visibility and governance over procurement help reduce leakage.

Also Read: Cost Management in UAE: Key Steps, Benefits & Proven Strategies for 2025

Forecasting And Controls That Prevent Cash Flow Problems

Cash flow improvement is sustainable only when supported by forward visibility. Working capital management focuses on balancing current assets and liabilities and deciding the appropriate investment level in short-term resources.

1. Build A Short-Term Cash Forecast

A rolling weekly forecast provides early warning of liquidity pressure and enables scenario planning. Businesses that appear profitable can fail when obligations fall due because liquidity was not anticipated in advance.

2. Establish Decision Rules For Spending

Controls around approval thresholds, vendor access, and discretionary expenditure ensure cash commitments align with forecast capacity rather than reacting after funds are spent.

3. Monitor Working Capital Interaction

Receivables, payables, and inventory influence each other. Extending customer credit may increase sales but reduce liquidity, potentially forcing external financing.

Also Read: Cash Flow Optimisation Strategies for UAE Businesses in 2025

UAE Realities That Affect Business Cash Flow

Cash flow management in the UAE is shaped by payment behaviour across the market. Improving liquidity, therefore, requires understanding operating realities, not just internal process improvements.

Delayed B2B payments remain a structural pressure point. Recent reporting shows that 56% of business-to-business payments are late, with average delays of around 70 days and overdue periods sometimes extending months beyond agreed terms.

Across surveys, more than half of invoices are overdue, and bad debts continue to place pressure on working capital planning.

Payment behaviour fragmentation adds further complexity. Administrative inefficiencies and weak credit enforcement frequently contribute to overdue invoices, while inconsistent settlement patterns can signal underlying liquidity stress within customer organisations.

For SMEs, the macro impact is tangible. They represent roughly 94% of UAE companies, and slower settlement cycles can directly strain operations as teams spend time chasing payments instead of executing core work.

Contract discipline and credit vetting, therefore, become essential. Informal agreements and lack of structured follow-up are common drivers of delayed payment outcomes.

From a practical standpoint, improving cash flow in this environment typically means:

- Setting enforceable terms before delivery

- Monitoring customer payment behaviour

- Diversifying customer exposure

- Building collection processes that operate consistently

Also Read: How to Solve Cash Flow Issues in Business: Practical Strategies in UAE Businesses

How Alaan Tools Support Cash Flow Control

Improving cash flow is not limited to receivables and payment timing. Liquidity is also affected by how operational spending is authorised, tracked, and reconciled. Alaan provides spend and payment controls that help finance teams manage cash commitments before funds exit the business.

1. Corporate Cards With Limits Help Prevent Unplanned Cash Outflow

Alaan corporate cards allow finance teams to set spending caps, merchant controls, and usage rules. This reduces uncontrolled purchasing and keeps discretionary outflows aligned with available liquidity.

2. Real-Time Spend Platform Improves Cash Position Visibility

All card transactions and expense activity appear immediately in a central dashboard. This allows finance teams to monitor spending as it happens and detect potential cash pressure earlier in the cycle.

3. Approval Workflows Ensure Spend Matches Liquidity Capacity

Configurable approval routing validates purchases before commitment. Separating spend validation from payment timing helps preserve working capital flexibility without sacrificing governance.

4. Receipt Capture And Data Extraction Reduce Reconciliation Lag

Supporting documents are attached at the point of spend, with key data extracted automatically. This improves traceability and prevents end-period backlog that obscures true cash position visibility.

5. Accounting Integration Keeps Cash Records Current

Transaction data syncs into accounting systems with categorisation context preserved, improving reporting accuracy and reducing delays in understanding liquidity movement.

Cash flow resilience depends not only on collections and payment terms but also on disciplined visibility over outgoing commitments. By giving finance teams control over operational spending, approvals, and documentation, Alaan helps organisations maintain a clearer awareness of liquidity before cash leaves the business.

Also Read: Spending Policy for Businesses: A Complete Compliance Guide

Conclusion

Improving cash flow is rarely about one tactic. It comes from coordinating receivables discipline, payables strategy, inventory efficiency, and forward visibility. Businesses that focus on shortening collection cycles, managing payment timing, reducing tied-up capital, and forecasting proactively build resilience against liquidity shocks.

Operating realities in the UAE reinforce this approach. Payment delays, credit exposure, and fragmented settlement behaviour are common enough to make structured financial control a necessity rather than optimisation.

At Alaan, we help finance teams strengthen liquidity discipline through controlled spending, real-time visibility, and integrated workflows that align purchasing, approvals, and accounting outcomes before cash leaves the organisation. Book a Demo Today!

Frequently Asked Questions (FAQs)

1. How Do You Improve Cash Flow Without Borrowing

Focus on working capital: collect faster, reduce cash tied up in inventory, and use supplier terms properly. Borrowing can support liquidity, but it does not fix the underlying timing cycle.

2. How Much Cash Reserve Should A Business Keep

There is no single correct number. Many businesses set a minimum reserve based on fixed obligations (payroll, rent, debt, tax) and revenue volatility. The more unpredictable the collections are, the higher the reserve requirement tends to be.

3. What Should You Do When Customers Consistently Pay Late

Treat it as a credit risk signal. Tighten terms for that customer, confirm acceptance criteria before delivery, reduce dispute triggers, and consider staged billing or partial upfront payment where commercially feasible.

4. Is Offering Early Payment Discounts A Good Cash Flow Strategy

Only when the economics work. If the discount costs more than the value of receiving cash earlier, it weakens margins without meaningfully improving long-term cash strength.

5. What Is A 13-Week Cash Forecast And Why Use It

A 13-week forecast is a short-term rolling view of expected cash inflows and outflows, updated weekly. It is useful when cash is tight, growth is accelerating, collections are volatile, or commitments are increasing faster than visibility.

6. How Can Businesses Improve Cash Flow In Seasonal Industries

Seasonal businesses benefit from forecasting that reflects peak and off-peak cycles, inventory discipline during demand drops, and contract structures that reduce cash strain during slow periods (such as deposits, staged billing, or minimum commitments).