Financial decisions inside a business ultimately revolve around one question: what resources does the organisation control today that can create value tomorrow? Those resources, cash balances, receivables, investments, or contractual financial claims, underpin liquidity, planning, and capital allocation. Their importance is reflected at a global scale: total financial assets worldwide amount to roughly $255 trillion (≈ AED 936 trillion), illustrating how economic activity is anchored in financial rights and obligations rather than physical resources alone.

For finance teams, however, managing these assets rarely feels abstract. Liquidity pressures, reconciliation gaps, credit exposure, and reporting deadlines turn asset classification and measurement into practical challenges rather than conceptual ones.

In finance and accounting language, these resources are classified as assets. Understanding how financial assets are defined and measured is not simply technical bookkeeping; it influences lending decisions, liquidity forecasting, and reporting credibility. This guide breaks down what financial assets are, how they differ from other asset types, and how finance teams work with them in practice.

TL;DR

- Financial assets represent resources that can be converted into liquidity or deployed for return. Their management directly affects cash planning, solvency analysis, and capital allocation choices.

- Classification shapes how assets are managed. Separating assets by liquidity horizon, substance, and financial nature helps align reporting accuracy with strategic allocation decisions.

- Measurement choices affect financial results. IFRS 9 classification influences valuation stability, impairment recognition, and earnings volatility, which changes how performance is interpreted.

- Strong oversight improves forecasting and risk visibility. Monitoring receivables quality, credit exposure, and classification consistency strengthens solvency analysis and funding readiness.

- Accurate reporting starts with structured financial data flows. When approvals, spend tracking, and reconciliations are governed as enabled through Alaan, the data supporting financial asset balances stays reliable and audit-ready.

What Are Financial Assets

At the broadest level, an asset is a resource controlled by an entity because of past events and expected to provide future economic benefits. This principle underpins global accounting frameworks and defines why an item appears on a balance sheet in the first place.

A key nuance often missed: an asset does not need physical form. The defining characteristic is the right to future benefit, such as the ability to generate cash inflow or settle obligations.

A financial asset is a specific subset of assets. Unlike machinery or property, its value comes from a contractual claim, for example:

- Bank deposits

- Bonds

- Equity shares

- Receivables owed by customers

These are intangible by nature and usually more liquid than physical assets because their worth is tied to financial rights rather than operational use.

From a practical standpoint, finance teams treat financial assets as the most directly measurable drivers of liquidity and capital deployment, while non-financial assets typically support operations instead.

Also Read: Understanding Types and Definition of Asset in Business Accounting

Assets In Finance vs Assets In Accounting

The term “asset” is used slightly differently depending on context, and mixing those meanings leads to confusion in reporting discussions.

Assets From A Finance Perspective

In finance conversations, assets are viewed as resources that contribute to economic well-being or wealth generation. They include both operational resources and investment holdings, from real estate to intellectual property and securities.

This perspective is forward-looking, concerned with return potential, liquidity, and strategic value.

Assets From An Accounting Perspective

Accounting frames assets within the structure of the balance sheet. The central relationship is the accounting equation:

Assets = Liabilities + Equity

This equation shows that all resources controlled by a business are financed either by creditors or by owners.

Assets represent the resource side of the equation, while liabilities and equity represent claims against those resources.

This view emphasises measurement, recognition criteria, and reporting consistency rather than return potential.

The distinction matters in practise. Finance leaders may evaluate assets for strategic deployment, while accountants ensure those same assets meet recognition and valuation rules that keep financial statements credible.

Also Read: Understanding Financial Statements for Beginners Guide

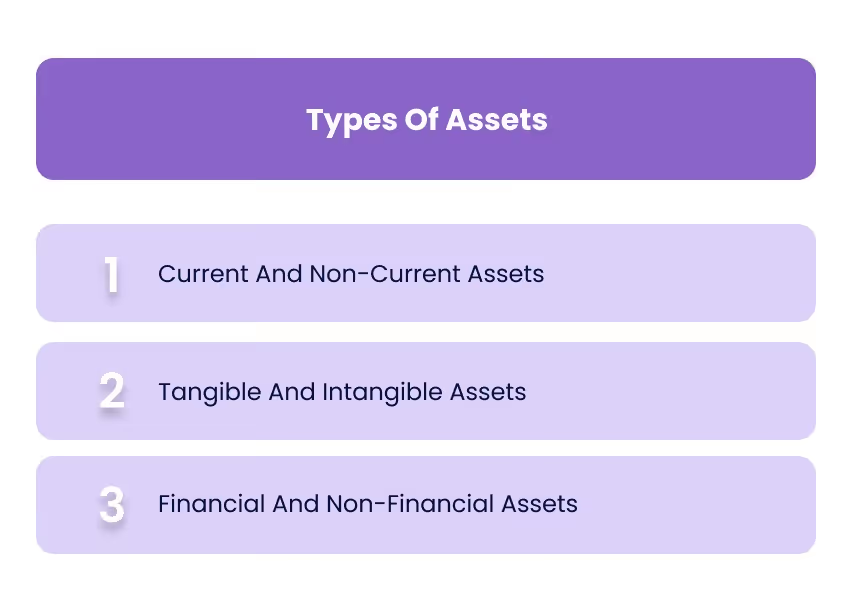

Types Of Assets

Finance teams rarely use a single classification lens. Assets are grouped differently depending on what decision is being made: liquidity planning, reporting, or operational investment. Three classifications appear most often in practise.

Current And Non-Current Assets

This distinction centres on time horizon and convertibility to cash.

Current assets typically include items such as cash balances, receivables, and inventory, resources expected to be used or realised within the operating cycle. By contrast, non-current assets are held for longer-term use and are not intended for liquidation within the current period, such as equipment, buildings, or infrastructure.

This separation matters operationally because liquidity analysis, working capital management, and lender assessments all depend on it.

Tangible And Intangible Assets

Assets may also be classified by physical substance.

Tangible assets have physical form and support operations directly, such as plant, machinery, vehicles, and similar resources. Intangible assets represent value without physical form, such as intellectual property or licences. Both are capable of delivering economic benefit and therefore qualify as assets when recognition criteria are met.

This classification is less about liquidity and more about measurement, depreciation/amortisation, and impairment considerations.

Financial And Non-Financial Assets

This distinction is especially important for finance leaders.

- Financial assets derive value from contractual rights to receive cash or another financial instrument

- Non-financial assets derive value from operational usage or ownership

Separating these helps finance teams focus liquidity and risk analysis on items that directly influence capital deployment and solvency.

Also Read: Understanding Components of a Corporate Balance Sheet

What Counts As A Financial Asset (With Examples)

Financial assets are best understood through practical balance-sheet examples rather than definitions alone. The common thread across them is contractual entitlement rather than operational utility.

Typical Examples Seen In Businesses

- Cash And Bank Deposits

The most liquid financial asset, forming the baseline of solvency assessment. - Trade Receivables

Customer payment obligations resulting from credit sales are often one of the largest working capital drivers. - Loans And Intercompany Balances

Amounts owed to the entity under lending arrangements. - Debt Investments

Holdings that generate fixed or structured cash flows are often maintained for liquidity or yield management. - Equity Investments

Ownership interests in other entities that provide return potential rather than contractual repayment.

What Typically Does Not Qualify

Understanding exclusions prevents classification errors:

- Inventory

- Property or equipment

- Prepaid expenses

These generate economic benefit but do not represent financial claims and therefore fall outside the financial asset category.

Also Read: Chart of Accounts: A Practical Guide for UAE Businesses

Financial Assets Classification For Reporting

Once recognised, financial assets are classified according to international reporting standards based on how they are managed and the nature of their cash flows. This classification affects measurement, earnings volatility, and disclosure requirements.

Under IFRS 9, classification is driven by two tests:

- The business model for managing the asset

- Whether contractual cash flows consist solely of principal and interest

Together, these determine placement into one of three categories.

Amortised Cost

Used when assets are held to collect contractual cash flows and those flows meet the principal-and-interest test.

Typical examples include receivables or loans.

This approach emphasises stability; valuation changes generally do not introduce earnings volatility.

Fair Value Through Other Comprehensive Income (FVOCI)

Applied when assets are managed both to collect cash flows and to sell when needed, provided cash flows meet the required characteristics.

Debt investments held for liquidity management commonly fall into this category.

Here, certain valuation changes bypass profit and loss and appear in comprehensive income instead, affecting how performance is presented.

Fair Value Through Profit Or Loss (FVTPL)

The default classification when other conditions are not met.

Equity investments and derivatives often fall into this bucket, with valuation changes recognised directly in earnings.

This category introduces the greatest income statement sensitivity because market movements flow through reported results.

Classification is not arbitrary. It depends on the entity’s operating model and the contractual design of the asset. IFRS 9 explicitly states that financial assets are initially classified into amortised cost, FVOCI, or FVTPL based on these factors.

Also Read: Understanding General Ledger in Double-Entry Accounting

Measuring Financial Assets In Practise

Recognising a financial asset is only the starting point. Measurement determines how that asset influences reported performance and decision-making. Two realities shape this stage: valuation approach and impairment treatment.

Cost And Fair Value Perspectives

Financial assets may be measured using amortised cost or fair value, depending on their classification and purpose.

Cost-based measurement emphasises stability because values change gradually as cash flows are collected. Fair value measurement, by contrast, reflects market conditions and can introduce volatility into reported results when asset prices fluctuate.

The choice is not arbitrary; it stems from IFRS classification rules and how the asset is managed operationally, which directly affects earnings presentation and stakeholder interpretation.

Impairment And Expected Credit Loss

Under IFRS 9, entities must recognise expected credit losses on many financial assets, such as receivables or debt instruments, rather than waiting for an actual default. The impairment allowance initially reflects expected losses from possible defaults over the next 12 months, expanding to lifetime expected losses when credit risk increases significantly.

This forward-looking approach is designed to ensure that financial statements reflect risk exposure earlier rather than after deterioration becomes visible. In practise, this makes receivable monitoring and ageing discipline central to financial asset management.

Digital Assets And Financial Asset Boundaries

A frequent misconception is that all assets tied to financial markets qualify as financial assets under reporting standards. Digital assets illustrate the boundary clearly.

IFRS guidance indicates that many cryptocurrencies do not meet the definition of financial assets because they do not create contractual rights to receive cash or another financial instrument. Instead, they are generally treated as intangible assets under IAS 38 unless held for sale in the ordinary course of business, in which case inventory rules may apply.

This distinction matters operationally because classification determines measurement approach, impairment treatment, and disclosure expectations. Misclassification can materially distort reporting.

Also Read: Understanding Types and Definition of Asset in Business Accounting

How Alaan Helps Maintain Reliable Financial Asset Data

Financial asset reporting depends on the quality of transactional data feeding balance-sheet positions. Cash balances, receivables, and liquidity indicators are shaped by approvals, payments, and reconciliations happening across the business.

Alaan supports finance teams by structuring these operational flows so asset data remains accurate and audit-ready.

- Corporate Cards And Spend Platform Improve Cash Visibility

Alaan corporate cards and centralised spend tracking capture business expenses in real time. This reduces delayed recognition of cash movements and gives finance teams clearer visibility into liquid financial asset positions throughout the period. - Approval Workflows Strengthen Transaction Governance

Configurable approval flows ensure transactions impacting cash and working capital are validated before execution. This improves traceability and reduces adjustments that can weaken confidence in reported asset balances. - Real-Time Transaction Tracking Reduces Reconciliation Gaps

Transactions, receipts, and metadata are captured as activity occurs, minimising timing mismatches that typically surface during month-end close and affect financial asset reporting. - Accounting Integrations Support Accurate Ledger Classification

Alaan synchronises structured expense and payment data into accounting systems with context preserved. This helps finance teams classify, measure, and review financial asset positions consistently under reporting standards.

Financial assets are defined by accounting frameworks, but their reliability depends on disciplined operational data. By improving visibility over spend, approvals, and reconciliation inputs, Alaan helps finance teams maintain confidence in the numbers underpinning liquidity and reporting decisions.

Why Asset Discipline Matters For UAE Finance Teams

Asset classification is not just about compliance. It directly shapes financial control and strategic decision-making.

Well-structured asset tracking enables finance leaders to:

- Maintain credible liquidity forecasts

- Detect credit deterioration early

- Support audit readiness

- Improve capital allocation decisions

Modern performance analysis increasingly depends on balance sheet-driven metrics, where financial ratios derived from asset and income statement data help evaluate organisational strength and risk exposure.

In practical operating environments, asset visibility influences budgeting, vendor negotiations, funding discussions, and expansion planning. The discipline applied to financial assets, therefore, contributes to both reporting integrity and strategic agility.

Also Read: Guide to Preparing Financial Statements Efficiently

Conclusion

Financial assets sit at the centre of financial decision-making because they represent the most direct claims to liquidity, capital deployment, and return potential. Understanding their definition, classification, and measurement allows finance teams to interpret financial statements accurately and make more informed operational and strategic decisions.

From distinguishing financial assets from operational resources to navigating IFRS classification and impairment expectations, the practical takeaway is consistent: asset discipline improves reporting credibility, forecasting quality, and risk visibility.

At Alaan, we help finance teams maintain clear visibility over spend and financial activity so the data feeding asset balances, approvals, transactions, and reconciliations remains structured and audit-ready. If you’re evaluating how your current processes support financial clarity and reporting confidence, book a walkthrough with our team. Book a Demo Today!

FAQs

1. How do financial assets affect borrowing capacity?

Lenders often evaluate liquidity and collateral quality based on financial asset strength, particularly cash balances and receivable reliability, when assessing creditworthiness.

2. Are financial assets always liquid?

Not necessarily. While many are liquid, liquidity depends on marketability, maturity horizon, and contractual terms rather than classification alone.

3. How often should financial assets be reviewed internally?

Many organisations perform monthly reviews aligned with close cycles, with deeper quarterly assessments focused on impairment risk and valuation sensitivity.

4. Can poor receivable management distort asset quality?

Yes. Slow collections or credit deterioration reduce realisable value and increase expected credit loss exposure, affecting the reported financial position.

5. Do financial assets carry operational risk?

Indirectly. Market volatility, counterparty default, and valuation sensitivity introduce risk that influences treasury strategy and capital planning.

6. How do financial assets support strategic flexibility?

Strong liquid financial asset positions allow faster response to investment opportunities, downturns, or funding constraints.