Are gaps in your bank reconciliation process putting your company’s financial accuracy at risk? According to recent studies, approximately 30% of companies have errors in their financial records due to inadequate bank reconciliation processes. These discrepancies often lead to cash flow mismanagement, compliance issues, or unnoticed fraud, all of which can severely impact operational decisions, particularly in the UAE markets.

A bank reconciliation statement provides a structured way to validate your cash balance. It helps identify missed transactions, unauthorised charges, or delays in posting, ensuring your books match the actual bank data. When performed regularly, it becomes a critical control mechanism for protecting your financial integrity.

This blog offers a complete guide on how to prepare a bank reconciliation statement. You’ll learn the essential steps, common pitfalls to avoid, and why automation is increasingly becoming the smarter option for finance teams in the UAE.

[cta-1]

What Is a Bank Reconciliation Statement?

A bank reconciliation statement (BRS) is a financial document that compares your internal accounting records with your bank statement to ensure accuracy. The goal is to ensure both balances match and explain any differences, such as unrecorded payments, bank fees, or errors.

In the UAE, many businesses use post-dated cheques, deal in multiple currencies, and make regular cross-border payments. Without reconciliation, these transactions can easily result in duplicate entries, missed deposits, or bounced checks, which can affect cash flow and erode supplier trust.

A BRS helps prevent such issues. It ensures your cash position is accurate, detects fraud or bank errors early, and keeps your financial records ready for audits, VAT filings, and tax submissions. When done regularly, it provides clarity and control over your working capital, giving you confidence in every dirham you report or spend.

Why Bank Reconciliation Matters & How to Get It Right

For UAE businesses, especially those subject to VAT, corporate tax, and audit requirements, bank reconciliation is far more than a routine financial task — it’s a strategic control mechanism. Done right, it ensures your cash position is accurate, your compliance risks are minimized, and your operational decisions are based on real numbers.

Why It Matters

- Fraud Prevention: With the widespread use of post-dated cheques, multi-currency transfers, and digital payments in the UAE, it’s easy for unauthorised charges or duplicate payments to slip through. Regular reconciliation surfaces red flags early, before they impact cash flow or supplier relationships.

- Audit & VAT Readiness: Under UAE Federal Tax Authority (FTA) regulations, accurate financial reporting is mandatory. Reconciliation validates your general ledger and helps support clean VAT filings, especially when dealing with cross-border transactions and multi-currency accounts.

- Cash Flow Clarity: Outstanding cheques, unrecorded charges, or missed deposits distort cash visibility. Timely reconciliation gives an updated view of available funds, helping you avoid overdrafts, missed vendor payments, or poor investment timing.

- Regulatory Compliance: Whether you operate in the mainland, the DIFC, or ADGM, maintaining clean, up-to-date bank records is essential to avoid fines, delays in tax returns, or audit failures.

Also Read: UAE Corporate Tax Glossary: Essential Terms for Businesses

Documents Required Before You Start

Before preparing a bank reconciliation statement, it is important to gather all relevant documents to ensure a complete and accurate reconciliation process. Here’s what you will need:

- Your company’s general ledger or cash book for the specific reconciliation period. This serves as your internal financial record and will be matched against your bank statement.

- Bank statement for the same period (daily, weekly, or monthly). The frequency depends on your business cycle and transaction volume.

- List of outstanding cheques, if applicable. This is particularly important in the UAE, where post-dated cheques (PDCs) are commonly used in business agreements.

- Details of direct deposits, standing instructions, and bank charges. These can often be missed in internal records but are typically recorded by the bank.

For UAE-based businesses, ensure you reconcile all AED and foreign currency accounts. This becomes especially important if your company operates across multiple jurisdictions, such as the Dubai International Financial Centre (DIFC) or Abu Dhabi Global Market (ADGM).

These free zones operate under independent regulatory frameworks, and bank accounts maintained within them may have different reporting requirements. Maintaining clear records across jurisdictions not only improves financial accuracy but also supports compliance during audits and tax filings.

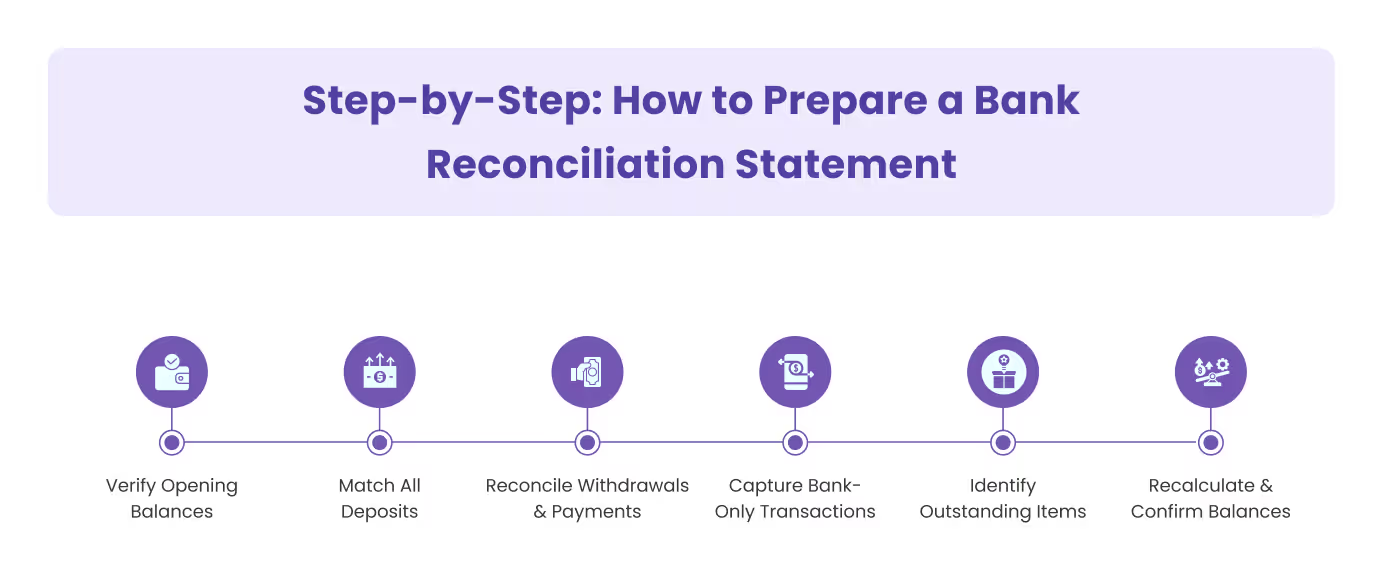

Step-by-Step: How to Prepare a Bank Reconciliation Statement

Manual reconciliation requires a disciplined process to ensure accuracy and compliance, particularly for businesses operating in regulated financial zones such as the DIFC and ADGM. Here is a comprehensive breakdown of each step:

Step 1: Verify Opening Balances

Begin by checking that the opening balance in your cash book matches the opening balance on your bank statement for the period under review. If there’s a mismatch, revisit the closing balances from the previous reconciliation and investigate if adjustments were missed or incorrectly recorded.

For UAE-based companies, ensure the balances include all active AED and foreign currency accounts, particularly if you're operating cross-border or dealing with multicurrency payrolls.

Step 2: Match All Deposits

Go through each deposit recorded in your cash book and confirm that it appears on your bank statement. Common discrepancies may arise from:

- Deposits made at the end of the month that appear in the next statement,

- International remittances, especially from Europe or Asia, which may take 1–3 business days to clear,

- Currency exchange differences in USD, EUR, or GBP accounts.

Ensure that unidentified credits are not VAT refunds, interest income, or customer transfers incorrectly categorised.

Step 3: Reconcile Withdrawals and Payments

Next, match all payments recorded in your cash book, including cheques, online transfers, and standing orders, with corresponding debits in your bank statement. Look out for:

- Outstanding cheques: These are common in the UAE, where B2B post-dated cheques are still widely used.

- Wage transfers via WPS: These may reflect on your bank statement before being recorded in your books.

- Recurring payments: Ensure standing instructions for rent, utilities, and supplier dues are properly captured.

Record any bounced cheques or duplicate payments immediately, and keep copies for audit readiness.

Step 4: Capture Bank-Only Transactions

Certain transactions will only appear on your bank statement, not in your cash book. These must be manually added or imported via your accounting software. They typically include:

- Bank service charges, SMS fees, and minimum balance penalties (common with UAE banks),

- Interest earned on business savings accounts,

- WPS-related salary file rejection penalties,

- Charges for international SWIFT transactions or local fund transfers (e.g. UAEFTS, IBAN errors).

Update your ledger with these transactions using appropriate journal entries to avoid misstatements during VAT filing.

Step 5: Identify Outstanding Items

Now, compile a list of all items that remain unreconciled. These include:

- Outstanding cheques: Issued but not yet presented for payment.

- Deposits in transit: Recorded in your books but not cleared by the bank.

- Bank errors: Though rare, incorrect postings can occur, especially during weekends or public holidays.

Document each item with transaction details and supporting evidence. This is especially important for UAE entities undergoing audits by the Federal Tax Authority (FTA) or preparing annual reports for regulators.

Step 6: Recalculate and Confirm Adjusted Balances

Once all differences are accounted for, compute your adjusted balances as follows:

- Adjusted Bank Balance = Closing Bank Statement Balance ± Outstanding Items

- Adjusted Cash Book Balance = Closing Cash Book Balance ± Manual Adjustments

Both figures should match. If not, review each step again to identify missed entries or calculation errors.

A well-executed bank reconciliation process ensures your financial records reflect reality, helping you prevent errors, detect fraud, and maintain compliance with UAE regulatory standards. Consistency is key to maintaining trust and operational efficiency.

Example of a Bank Reconciliation Statement in the UAE

Let’s consider an example to understand how a UAE-based SME can reconcile its bank statement effectively.

Scenario:

Al Noor Trading LLC maintains a corporate account with a local UAE bank. As of 31 May 2025, their cash book reflects a closing balance of AED 48,000. However, the bank statement shows a closing balance of AED 45,500. The discrepancy is due to the following:

- A deposit of AED 5,000 made on 31 May has not yet been processed by the bank.

- A cheque worth AED 2,500 issued to a supplier is still outstanding.

- The bank has charged a monthly fee of AED 1,000 for account maintenance, which is yet to be recorded in the cash book.

Reconciliation Steps:

- Adjust the bank statement:

- Add the unprocessed deposit: AED 45,500 + AED 5,000 = AED 50,500

- Subtract the outstanding cheque: AED 50,500 − AED 2,500 = AED 48,000

- Adjust the cash book:

- Subtract the unrecorded bank fee: AED 48,000 − AED 1,000 = AED 47,000

At this stage, a mismatch still exists. This signals the need for further investigation, maybe a duplicate transaction or an unposted entry.

Takeaway:

Even a minor delay in recording deposits or bank fees can lead to confusion. Using tools like Alaan’s real-time spend tracking and automated reconciliation features helps UAE businesses, such as Al Noor Trading LLC, maintain financial accuracy without the need for manual back-and-forth.

[cta-3]

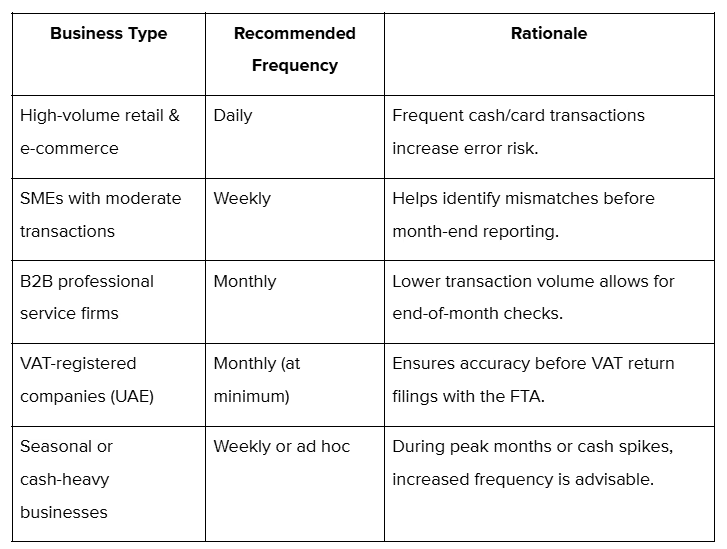

How Often Should UAE Businesses Reconcile Bank Statements?

The ideal reconciliation frequency depends on your transaction volume, business model, and risk exposure. While monthly reconciliation is standard for many small to medium-sized enterprises (SMEs), some UAE businesses may require more frequent checks to maintain financial accuracy and avoid compliance risks.

Recommended Reconciliation Frequencies by Business Type

Note: UAE businesses filing VAT returns should reconcile at least once per month to avoid penalties due to reporting errors. Errors in bank balances could lead to incorrect input tax claims or delayed refunds from the Federal Tax Authority.

When is More Frequent Reconciliation Necessary?

Even if your regular schedule is monthly, additional reconciliations should be performed in the following situations:

- Before submitting VAT returns or financial reports.

- After a period of high transaction activity, such as seasonal promotions or supplier payments.

- If fraud or suspicious activity is suspected.

- When multiple departments or users access bank-linked platforms, it increases the risk of duplicated or missed entries.

Digital Banking Enables Smarter Reconciliation

With digital platforms like Alaan, reconciliation no longer needs to wait until the end of the month. You can monitor transactions in real time, flag discrepancies instantly, and match bank feeds with spend data without manual spreadsheets. This level of visibility and automation enables UAE finance teams to reconcile more frequently, even on a daily basis, without consuming excessive time.

Your reconciliation schedule should reflect the financial rhythm of your business. But consistency is crucial. UAE firms that reconcile regularly and adopt real-time finance tools are better prepared for audits, VAT filings, and business decision-making.

Also Read: UAE VAT Glossary: Essential Terms for Businesses

Common Bank Reconciliation Mistakes to Avoid in UAE Businesses

Even experienced finance teams can fall into reconciliation traps, especially when processes are manual, fragmented, or rushed in the lead-up to VAT filing deadlines. Below are some frequent errors UAE businesses should actively prevent:

- Overlooking Bank-Only Transactions

Many UAE businesses overlook recording bank charges, standing instructions, and interest income or deductions that do not originate from the ERP or cash book. Failing to reflect these in your books leads to mismatched balances and VAT reporting discrepancies.

- Reconciliation Without Updating the Cash Book

Reconciling before posting all transactions, such as petty cash withdrawals or corporate card expenses, leads to inaccurate matching. Your cash book must be fully updated before comparing it against the bank statement.

- Starting with an Incorrect Opening Balance

If your previous reconciliation contained unresolved discrepancies or manual adjustments, the current period will begin with an incorrect balance. This confuses the detection of new issues and affects downstream financial statements.

- Misclassifying Returned or Voided Cheques

Returned cheques, especially from cross-border or post-dated payments, must be reclassified correctly. Many UAE firms misreport these in accounts receivable, leading to duplicated income entries or overstated cash flows.

- Failing to Reconcile Multi-Currency Accounts

Multi-currency accounts, common among UAE firms that deal with suppliers in USD, EUR, or INR, can introduce variations in exchange rates. Reconciliation must account for forex differences, especially when settling invoices through SWIFT or correspondent banks.

- Relying Solely on Excel Without Audit Trails

Spreadsheets lack version control, audit logs, and real-time collaboration. This makes it difficult to track reconciliation history or identify who modified which entry, creating compliance risks, especially during external audits or VAT inspections.

- Skipping Review of Reconciliation Reports

Even after reconciliation is “complete,” unreviewed reports often hide anomalies, like unposted items or duplicated entries. Skipping this step means leaving money (or risk) on the table.

Avoiding these common mistakes ensures your bank reconciliation is accurate, timely, and compliant, helping your UAE business maintain strong financial control and VAT readiness.

Best Practices for UAE Businesses to Streamline Bank Reconciliation

To avoid costly mistakes and ensure full compliance with UAE tax and audit requirements, companies must adopt a disciplined, modern approach to reconciliation. Here’s how to build a bank reconciliation process that’s accurate, efficient, and audit-ready:

- Set a Clear Reconciliation Schedule

Consistency is key. Most UAE businesses benefit from monthly reconciliations aligned with bank statement cycles. However, companies with high transaction volumes should consider reconciling their accounts on a weekly or even daily basis. These would include retail outlets in Dubai’s busy shopping districts or e-commerce platforms serving the GCC.

This helps identify discrepancies and cash flow issues early, allowing timely resolution and reducing the risk of VAT reporting errors.

- Automate the Reconciliation Process

Manual reconciliation is time-consuming and prone to mistakes, especially as your business grows. Many UAE companies now use automated tools that integrate with local banks and accounting software.

Automation accelerates matching transactions, flags anomalies instantly, and maintains a clear audit trail, which is critical for meeting UAE Federal Tax Authority (FTA) compliance and facilitating smoother VAT audits.

- Reconcile all Bank and Cash Accounts Regularly

Even accounts with low activity, such as company savings accounts or foreign currency accounts used for transactions in the GCC, must be reconciled. Dormant or rarely used accounts can go unnoticed, allowing for hidden fees or fraudulent transactions.

In the UAE’s multi-currency environment, don’t forget to reconcile accounts in AED, USD, EUR, or other currencies separately, ensuring foreign exchange impacts are accurately recorded.

- Train Your Finance and Accounting Teams on UAE-Specific Compliance and Workflow

The UAE’s evolving tax laws and financial regulations require your team to be well-versed in local requirements, including VAT documentation, digital invoicing mandates, and record-keeping periods (at least five years as mandated by the FTA).

Regular training reduces compliance risks and empowers your team to handle exceptions, such as returned cheques or bank fees unique to UAE banks.

- Maintain Detailed and Accessible Documentation

UAE tax authorities require businesses to maintain digital records of all bank statements, reconciliation reports, and related financial documents for a minimum of five years. Storing these securely, ideally in cloud-based systems compliant with UAE data protection laws, ensures quick retrieval during audits and supports transparent reporting.

Additional Tips to Enhance Your Reconciliation Process:

- Utilise real-time banking data: UAE banks increasingly offer APIs and online portals that provide near real-time transaction updates. Use these to perform interim checks and catch issues before month-end.

- Standardise workflows with checklists: A step-by-step reconciliation checklist adapted to your business size and complexity helps maintain accuracy and ensures no step is overlooked.

- Regularly review reconciliation reports: These reports highlight unmatched transactions or unusual activity, enabling early intervention and preventing costly errors.

UAE businesses should adopt these practices to achieve smoother bank reconciliations, enhance financial accuracy, and confidently meet local compliance requirements, thereby building a resilient and trustworthy financial foundation.

How Alaan Simplifies Expense Management for UAE Businesses?

Alaan is designed to give UAE businesses full control and transparency over company spending. Here’s how it helps:

- Complete Visibility: Track every dirham spent across your organisation in one central dashboard.

- AI-powered Data Capture: Upload receipts and let Alaan automatically extract VAT, TRN, vendor details, and more.

- UAE Tax Compliance: Ensure all expenses are recorded accurately with tax codes and categories tailored to the UAE Federal Tax Authority rules.

- Automated Accounting: Sync Alaan with your accounting software to update your books in real time, speeding up your monthly financial close.

- Custom Approval Flows: Set spending limits and approval processes by team or individual to easily control budgets.

- Built-in Spend Controls: Reduce overspending risks without micromanagement through card-level restrictions.

Alaan helps you save time, improve accuracy, and stay compliant, all while giving you complete control over your business expenses in the UAE.

Join over 1,000 companies across Dubai, Abu Dhabi, and beyond that rely on Alaan to simplify their finance operations.

Also Read: What is finance automation?

Final Thoughts

Accurate and timely bank reconciliation is crucial for UAE businesses seeking to maintain financial health and comply with local regulations. Avoiding common reconciliation mistakes, adopting best practices, and leveraging automation can save your finance team valuable time and reduce costly errors. As transaction volumes grow, relying on manual processes becomes increasingly risky and inefficient.

To stay ahead, UAE companies must adopt smart solutions that simplify expense management, improve visibility, and ensure regulatory compliance.

Take control of your business finances with Alaan. Our AI-powered platform automates reconciliation, provides real-time spend insights, and supports UAE tax compliance, allowing your team to focus on what matters most: growing your business.

Schedule a demo with Alaan today and experience seamless, error-free bank reconciliation.

FAQs

Q. How often should small businesses in the UAE perform bank reconciliation?

A. Small businesses should reconcile their bank accounts at least once a month to catch discrepancies early. However, companies with high transaction volumes may benefit from weekly or even daily reconciliations.

Q. Can bank reconciliation help detect fraud in UAE companies?

A. Yes, regular reconciliation helps identify unusual or unauthorised transactions quickly. This early detection reduces the risk of fraud and financial loss.

Q. What documents are essential for efficient bank reconciliation?

A. Key documents include bank statements, cash books, payment vouchers, receipts, and invoices. Keeping these organised and digitised streamlines the reconciliation process.

Q. How does multi-currency reconciliation affect UAE businesses?

A. UAE businesses dealing with multiple currencies must carefully track exchange rates and conversion differences during reconciliation to ensure accurate financial records.

Q. Is manual bank reconciliation still relevant with automation tools available?

A. While manual reconciliation can work for very small businesses with limited transactions, automation is recommended for most UAE companies to reduce errors, save time, and ensure compliance with VAT and audit requirements.