Managing vendor payments is a core operational function for businesses in the UAE, yet it is also one of the most common sources of inefficiency, delays and compliance risk. As companies scale, supplier volumes increase, payment methods diversify, and regulatory expectations around documentation and VAT become stricter.

For finance teams, vendor payments are no longer just about settling invoices on time. They directly affect cash flow visibility, supplier relationships, audit readiness and overall financial control.

This guide breaks down how the process typically works, common challenges companies face, and how modern spend and payment platforms help finance teams manage vendor payments at scale.

Key Takeaways:

- Vendor payments are a core finance control, not just a payout task. They directly affect cash flow, VAT compliance, supplier relationships, and the accuracy of financial reporting in the UAE.

- Manual and fragmented processes don’t scale. Email approvals, scattered invoices, and multiple payment channels lead to late payments, reconciliation errors, and poor visibility as vendor volumes grow.

- Lack of visibility is the biggest operational risk. When teams can’t clearly see what’s approved, pending, or overdue, cash flow planning weakens, and supplier disputes increase.

- Payment execution alone is not enough. Effective vendor payment platforms must support invoice capture, approval workflows, VAT validation, and clean accounting sync before money moves.

- Successful adoption depends on process discipline. Clear ownership, standardised vendor data, defined approvals, and early accounting integration are what make vendor payment platforms deliver long-term control and scalability

What Are Vendor Payments and How Do They Work?

Vendor payments refer to payments a business makes to its suppliers for goods or services received. These suppliers may include service providers, product vendors, contractors, logistics partners, landlords or professional firms.

In the UAE, vendor payments are typically invoice-driven. This means payments are released only after a valid invoice is received, reviewed and approved, often with VAT compliance checks in place.

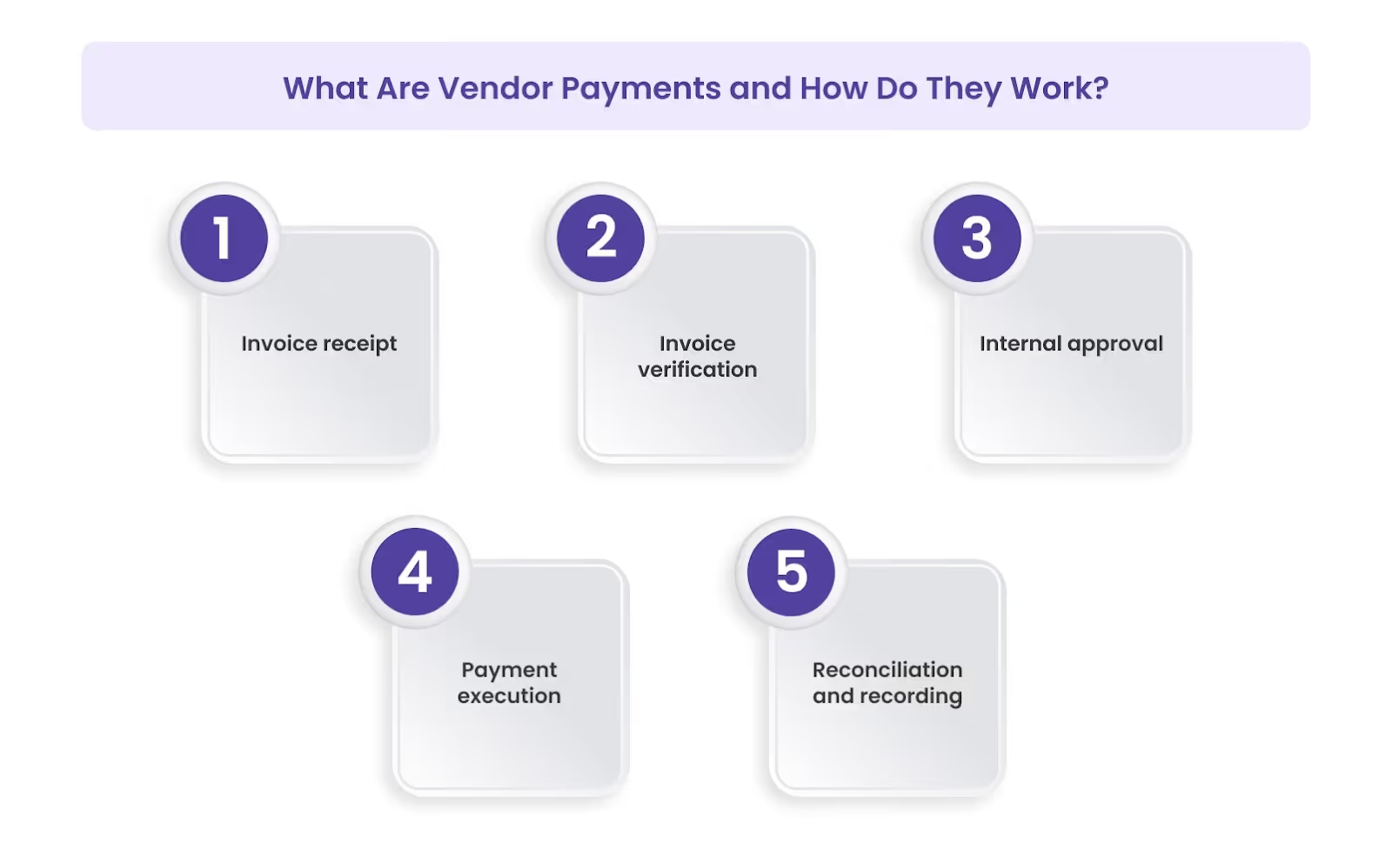

How the Vendor Payment Process Works?

While workflows vary by company size and industry, a typical vendor payment process in the UAE follows these steps:

- Invoice receipt: The vendor submits an invoice through email, a portal or a shared inbox. The invoice includes supplier details, amounts, VAT breakdown and payment terms.

- Invoice verification: Finance teams verify invoice accuracy, confirm VAT compliance, and check alignment with purchase agreements or contracts.

- Internal approval: Invoices are routed to the relevant approvers based on value, department or entity. Approval confirms that the expense is valid and authorised.

- Payment execution: Once approved, the payment is processed through a bank transfer, corporate card, cheque or international transfer, depending on the vendor and payment type.

- Reconciliation and recording: The payment is matched back to the invoice and recorded in the accounting system. This step ensures payable balances are accurate and financial records remain clean.

When managed well, this process ensures vendors are paid on time, cash flow is controlled, and compliance requirements are met. When managed manually, however, it often becomes slow, fragmented and difficult to scale.

Common Vendor Payment Methods Used in the UAE

Businesses in the UAE use a mix of payment methods depending on vendor type, transaction value, location and internal controls. Most finance teams rely on more than one method, which is often where complexity begins.

1. Bank Transfers (Local and International)

The most common method for vendor payments. Local transfers are used for domestic suppliers, while international transfers support overseas vendors and imports. Reliable but often manual, slow and hard to track end-to-end.

2. Corporate Cards

Used for SaaS, advertising, professional services and low to mid-value vendors. Fast and convenient, but not suitable for invoice-based settlements, bulk payments or many international suppliers.

3. Cheques

Still used in some industries, particularly real estate and construction. However, cheques create delays, reconciliation challenges and limited payment visibility.

4. Exchange Houses and FX Providers

Chosen for international payments due to competitive FX rates. These solutions are usually manual and sit outside core finance systems, increasing reconciliation effort.

5. Online Payment Platforms

Used for select international or digital vendors. While convenient, they often lack approval controls, invoice linkage and accounting integration.

As vendor volumes grow, managing payments across these channels makes visibility, control and reconciliation increasingly difficult without a centralised system.

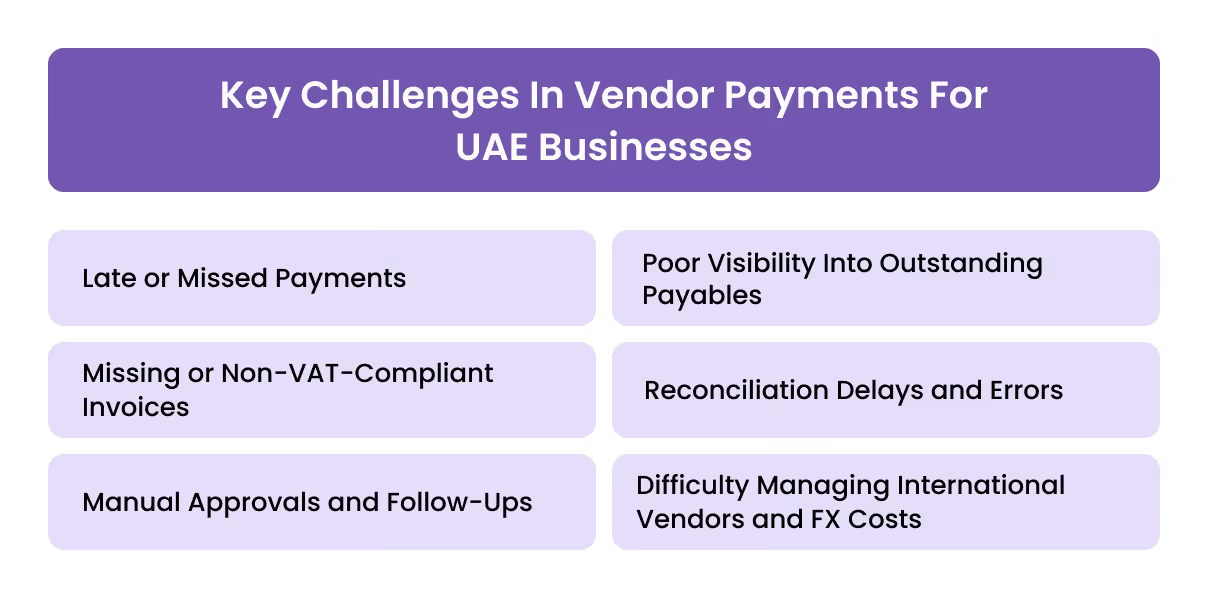

Key Challenges in Vendor Payments for UAE Businesses

As businesses grow, vendor payment processes often struggle to keep up. What starts as a manageable workflow quickly becomes fragmented, manual and difficult to control. In the UAE, these challenges are amplified by VAT requirements and cross-border payments.

1. Late or Missed Payments

Manual approvals, scattered invoices and unclear ownership frequently lead to delayed payments. This strains supplier relationships and can disrupt operations.

2. Missing or Non-VAT-Compliant Invoices

Invoices without proper VAT details or supporting documentation stall payments and create compliance risk. Chasing corrected invoices adds unnecessary back-and-forth.

3. Manual Approvals and Follow-Ups

Email-based approvals and spreadsheets slow down decision-making. Finance teams spend significant time following up instead of focusing on higher-value work.

4. Poor Visibility Into Outstanding Payables

Without a central view, it is difficult to track what has been approved, what is pending and what is overdue. This weakens cash flow planning and prioritisation.

5. Reconciliation Delays and Errors

Matching payments to invoices across bank statements, emails and spreadsheets is time-consuming and prone to mistakes, especially at month-end.

6. Difficulty Managing International Vendors and FX Costs

Cross-border payments often involve hidden fees, FX spreads and delayed settlement. Explaining landed costs and variances becomes challenging for finance leaders.

Together, these challenges show why manual vendor payment processes do not scale for modern UAE businesses.

Top Vendor Payment Platforms You Can Use

As vendor volumes grow and payment complexity increases, many UAE businesses turn to specialised platforms to centralise approvals, payments and reconciliation. Below are some of the commonly used vendor payment platforms in the UAE, each serving different business needs.

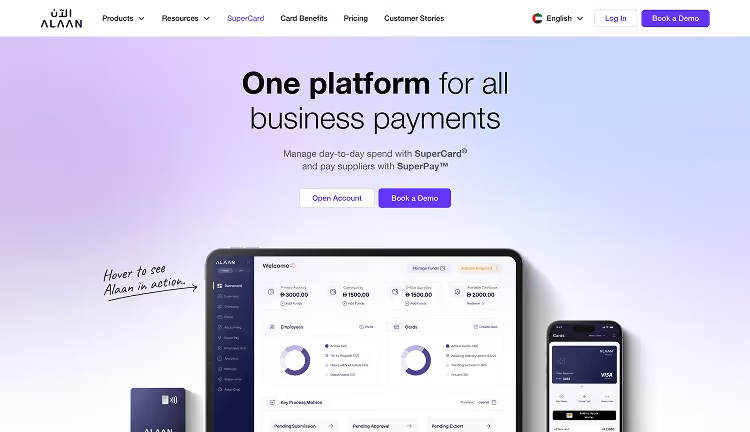

1. Alaan

Alaan is an AI-powered spend management platform built for UAE businesses to manage vendor payments, corporate cards and expenses in one unified system. It focuses on control, visibility and accounting readiness, not just payment execution.

Key features:

- Centralised vendor spend visibility: All vendor-related payments and expenses are visible in one dashboard, improving oversight and control.

- Invoice-linked approvals: Vendor payments follow structured approval workflows before funds are released.

- Corporate cards for eligible vendors: Card-based payments for SaaS, services and recurring vendors with built-in spend controls.

- Automated receipt and VAT capture: Invoices and receipts are captured digitally and checked for VAT compliance.

- Seamless accounting integration: Payments sync with tools like Xero, QuickBooks, NetSuite and Microsoft Dynamics.

- Real-time spend insights: Alaan Intelligence highlights vendor spend patterns and anomalies for better decision-making.

Best suited for: UAE businesses that want to manage vendor payments, expenses and accounting workflows together with strong controls and real-time visibility.

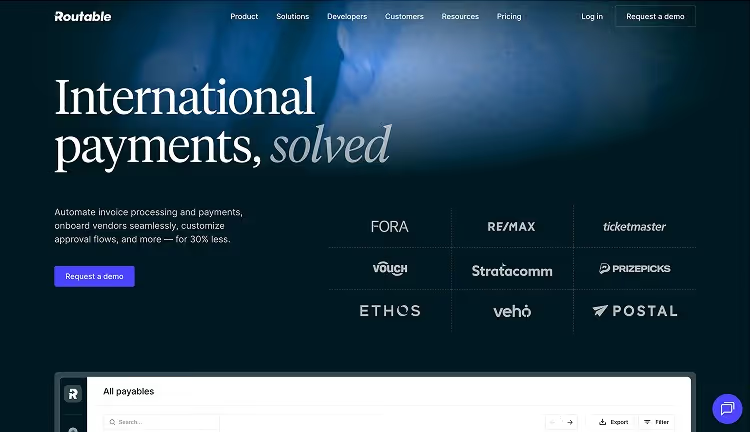

2. Routable

Routable is a global vendor payments platform that helps businesses pay suppliers and contractors across multiple countries, including the UAE.

Key features:

- Vendor onboarding and data collection: Centralised capture of vendor details and documentation.

- Approval-driven payouts: Role-based approvals to control when and how vendors are paid.

- Local and international payments: Supports vendor payouts across multiple countries.

- Payment status tracking: Visibility into scheduled, completed and failed payments.

Best suited for: Companies with international vendor bases that need structured payout and compliance workflows.

3. Qashio

Qashio is a UAE-based spend management platform focused on corporate cards and expense controls.

Key features:

- Corporate card issuance: Cards with predefined limits and usage controls.

- Spend visibility: Track card-based vendor and operational spending in real time.

- Approval controls: Basic approval workflows for managing spend.

- Local market focus: Built with UAE business requirements in mind.

Best suited for: Businesses managing card-based vendor spend and employee expenses primarily within the UAE.

4. Mamo

Mamo provides payment and payout solutions that allow businesses to send funds to vendors and partners through a simple interface.

Key features:

- Business payouts: Send payments to vendors and partners locally.

- Simple payment flows: Quick setup for executing transfers.

- API integrations: Programmatic access for payment automation.

- Payment tracking: Basic visibility into transaction status.

Best suited for: Businesses that need straightforward payout capabilities without complex approval or accounting requirements.

5. Tap Payments

Tap provides payment infrastructure across the MENA region, supporting business payouts and settlement services.

Key features:

- Regional payment coverage: Support for payments across multiple MENA markets.

- Payout and settlement tools: Infrastructure for sending and receiving business payments.

- API-driven platform: Designed for developer-led integrations.

- Multi-country scalability: Enables regional payment operations.

Best suited for: Companies looking for payment infrastructure or payout rails across multiple MENA countries.

How to Choose the Right Vendor Payment Platform in the UAE

Not all vendor payment platforms solve the same problem. Some focus purely on payment execution, while others support approvals, compliance and reconciliation. Choosing the right platform depends on where your biggest gaps exist today and how your business plans to scale.

1. Understand What You Are Trying to Fix

Start by identifying the main source of friction in your current process. For some teams, it is late payments and approval delays. For others, it is poor visibility, VAT compliance risk or reconciliation effort. The right platform should address these pain points directly rather than add another tool to manage.

2. Look Beyond Payment Execution

Sending money is only one part of vendor payments. A strong platform should also support invoice tracking, approvals and documentation so payments are controlled before they happen, not cleaned up after.

3. Evaluate VAT and Compliance Support

In the UAE, vendor payments must be backed by VAT-compliant invoices and clear audit trails. Platforms that do not support invoice capture, tax details and documentation increase compliance risk and manual work.

4. Assess Visibility Into Payables

Finance teams need a real-time view of what is approved, pending and outstanding. Without this visibility, cash flow planning becomes reactive, and payment prioritisation is difficult.

5. Consider Local and International Vendor Coverage

If your business works with overseas suppliers, assess how the platform handles international payments, FX transparency and landed costs. Limited coverage or opaque pricing often creates more issues than it solves.

6. Check Accounting and ERP Integration

Vendor payments should flow cleanly into your accounting system. Platforms that integrate with tools like Xero, QuickBooks or NetSuite reduce reconciliation effort and keep books accurate.

7. Think About Scalability and Control

A solution that works today should still work as invoice volumes, vendors, and entities increase. Look for platforms that support role-based approvals, standardised processes and automation without adding operational overhead.

Choosing the right vendor payment platform is all about finding the right level of control, visibility and integration for your finance team.

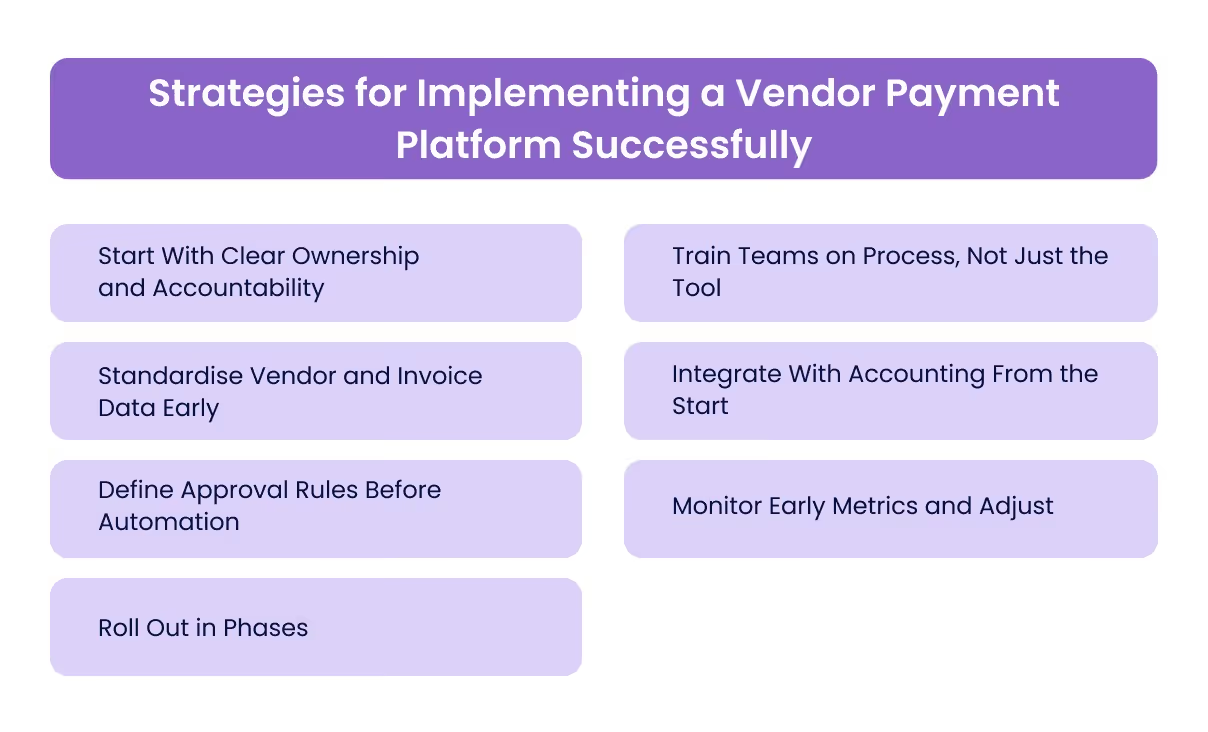

Strategies for Implementing a Vendor Payment Platform Successfully

Implementing a vendor payment platform is not just a systems change. It is a process and behaviour change across finance, procurement and operations. The following strategies help businesses get value quickly while avoiding disruption.

1. Start With Clear Ownership and Accountability

Assign clear ownership for vendor payments, approvals and system configuration from day one. When roles are ambiguous, invoices stall and controls weaken. Define who owns invoice intake, who approves payments and who oversees reconciliation.

2. Standardise Vendor and Invoice Data Early

Clean vendor records and consistent invoice formats make implementation smoother. Before going live, review supplier details, payment terms and tax information to reduce errors and rework later.

3. Define Approval Rules Before Automation

Approval workflows should reflect real business rules, not just system defaults. Set approval thresholds by value, department or entity so payments move quickly without compromising control.

4. Roll Out in Phases

Avoid switching everything at once. Start with a specific vendor group, entity or payment type, then expand gradually. A phased rollout allows teams to adapt without overwhelming operations.

5. Train Teams on Process, Not Just the Tool

Adoption improves when teams understand why processes exist, not just how to click buttons. Focus training on invoice discipline, approvals and documentation expectations, not only system navigation.

6. Integrate With Accounting From the Start

Vendor payment platforms deliver the most value when accounting integration is live from day one. This ensures payables, VAT and cash flow data stay aligned and reduces reconciliation effort immediately.

7. Monitor Early Metrics and Adjust

Track early indicators such as approval turnaround time, overdue invoices and reconciliation effort. These metrics highlight gaps quickly and help refine workflows before issues scale.

Successful implementation is about building consistent, repeatable processes that hold up as vendor volumes grow. When done right, the platform becomes a foundation for long-term financial control rather than another system to manage.

Key Strategies for Implementing a Vendor Payment Platform Successfully

Implementing a vendor payment platform is not just a systems change. It is a process and behaviour change across finance, procurement and operations. The following strategies help businesses get value quickly while avoiding disruption.

1. Start With Clear Ownership and Accountability

Assign clear ownership for vendor payments, approvals and system configuration from day one. When roles are ambiguous, invoices stall and controls weaken. Define who owns invoice intake, who approves payments and who oversees reconciliation.

2. Standardise Vendor and Invoice Data Early

Clean vendor records and consistent invoice formats make implementation smoother. Before going live, review supplier details, payment terms and tax information to reduce errors and rework later.

3. Define Approval Rules Before Automation

Approval workflows should reflect real business rules, not just system defaults. Set approval thresholds by value, department or entity so payments move quickly without compromising control.

4. Roll Out in Phases

Avoid switching everything at once. Start with a specific vendor group, entity or payment type, then expand gradually. A phased rollout allows teams to adapt without overwhelming operations.

5. Train Teams on Process, Not Just the Tool

Adoption improves when teams understand why processes exist, not just how to click buttons. Focus training on invoice discipline, approvals and documentation expectations, not only system navigation.

6. Integrate With Accounting From the Start

Vendor payment platforms deliver the most value when accounting integration is live from day one. This ensures payables, VAT and cash flow data stay aligned and reduces reconciliation effort immediately.

7. Monitor Early Metrics and Adjust

Track early indicators such as approval turnaround time, overdue invoices and reconciliation effort. These metrics highlight gaps quickly and help refine workflows before issues scale.

Successful implementation is about building consistent, repeatable processes that hold up as vendor volumes grow. When done right, the platform becomes a foundation for long-term financial control rather than another system to manage.

Wrapping Up

Vendor payments play a critical role in cash flow control, compliance and supplier relationships for UAE businesses. As organisations scale, managing invoices, approvals and payments through manual processes or disconnected systems creates delays, errors and visibility gaps.

A structured vendor payment platform helps finance teams bring consistency to approvals, maintain VAT-compliant documentation and track payables in real time. This not only improves operational efficiency but also strengthens financial discipline and audit readiness.

At Alaan, we help UAE businesses simplify vendor payments by unifying corporate cards, expense management and accounting automation in one platform. Finance teams gain clearer visibility, cleaner reconciliation and better control as they grow.

See how Alaan can support smarter vendor payment management. Book a demo to get started.

FAQs

1. What is meant by vendor payment?

A vendor payment refers to the payment a business makes to a supplier for goods or services received. It is usually processed against an invoice and recorded under accounts payable in the company’s financial records.

2. What payment methods are used in the UAE?

Common vendor payment methods in the UAE include bank transfers (local and international), corporate cards, cheques, exchange houses for foreign currency payments and online payment platforms. The method used depends on the vendor and transaction type.

3. How does a vendor get paid?

A vendor is typically paid after submitting a valid invoice. The invoice is verified, approved internally and then settled using the agreed payment method. The payment is later reconciled in the accounting system.

4. How can businesses pay vendor payments efficiently?

Businesses can pay vendor payments efficiently by using structured approval workflows, invoice-level tracking and automation tools that centralise payments, support VAT compliance and simplify reconciliation.