The UAE has been a global financial center and a prominent business hub in the Middle East that offers multiple benefits to businesses and foreign investors. One of the biggest incentives included the ‘nil’ tax on profits earned in the country, with only a few exceptions. In December 2022, the UAE government announced the introduction of a Federal Corporate Tax (CT law) that came into effect on June 1, 2023.

As per the new framework of UAE Corporate Tax, a 9% taxation rate has been set for annual taxable income of above AED 375,000 for companies that do not meet the conditions for Qualifying Free Zone Persons (QFZPs). Businesses operating within Free Zones, i.e., QFZPs, can still enjoy a 0% tax rate on qualifying income. However, to be eligible for this benefit, they must meet the relevant conditions set by the tax authorities. Any non-qualifying income of QFZPs is taxable at 9%.

If you are a business owner operating in a Free Zone and want information on how these new changes in the Corporate Tax affect your business, then this guide is for you. Read on!

Background of New Corporate Tax Law

Before we dig deep into the Corporate Tax structure for the Free Zone based companies, let’s have a look at the key aspect of the new Federal Corporate Tax system:

For licensed businesses operating on the UAE mainland, the corporate tax structure is as follows:

- A taxable person is subject to a 0% tax rate on taxable income up to AED 375,000.

- A 9% corporate tax applies to taxable income above AED 375,000.

On the other hand, businesses operating in Free Zones face a different tax structure:

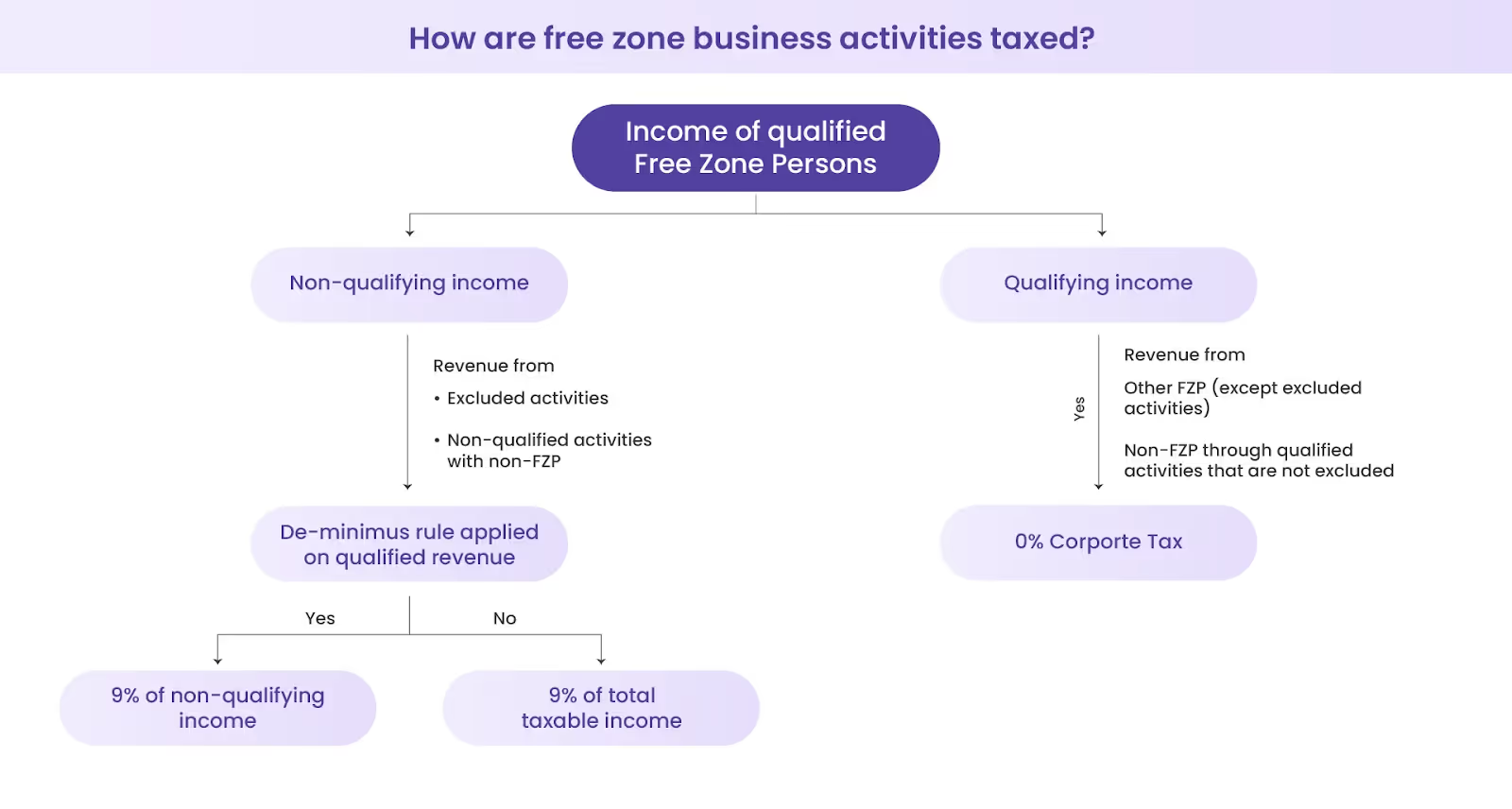

- A 0% corporate tax applies to the qualifying income of businesses recognized as a Qualifying Free Zone Person (QFZP).

- Non-qualifying income in the Free Zone is subjected to a 9% corporate tax, although other exceptions or relief may apply.

This new tax structure affects all businesses operating in the UAE, including foreign businesses with offices here.

The impact of the corporate tax varies depending on your location, i.e., Free Zone or Mainland, during the tax period. Understanding these changes will help you ensure compliance and avoid tax penalties like fines and interest charges.

Understanding the Context Of 'Person' in The UAE Tax Law

To understand the impact of corporate tax on businesses in Free Zones, you need to first understand the context of ‘Person’ defined in the UAE Tax Law:

- Natural Person: If you are a freelancer, a sole proprietor, or part of a civil company, you are considered a 'Natural Person' as per the law. While you might enjoy some Free Zone benefits, your income will still be subject to Corporate Tax. The corporate tax rules applicable here will be the same as those for individuals and businesses outside the Free Zones.

- Juridical Person: If your business is a corporation or a partnership, it is recognized as a 'Juridical Person' for corporate tax purposes. These businesses are eligible for the 0% CT rate on qualifying income if they meet the criteria set out in the UAE tax laws.

In short, while both natural and juridical persons can operate within Free Zones, only Juridical Persons meeting specific qualifying criteria can be classified as "Qualifying Free Zone Persons" (QFZPs) for tax benefits. Such businesses can enjoy a 0% corporate tax rate on their qualifying income.

Remember, obtaining the “Free Zone Person” status isn’t enough. You must also fulfill the qualifying income requirement for tax benefits. More on this later in our blog.

For now, let’s understand who qualifies as QFZP in the UAE.

Who Can be a Qualifying Free Zone Person?

If you are running a business in a Free Zone, here are the criteria you must fulfill to qualify as a QFZP under the new UAE Corporate Tax regime, these are:

- Maintain adequate substance in the UAE: Your business should have a significant presence in the UAE, including physical premises and employees.

- Generate qualifying income: Your income should primarily come from compliant business activities conducted within the Free Zone or with international clients.

- Do not elect to be part of normal CT rates: You should not choose to be taxed under the standard corporate tax rates applicable to non-Free Zone businesses.

- Non-qualifying revenue does not exceed the de minimis threshold: Your non-qualifying income should be below 5% of total revenue or AED 5 million, whichever is lower.

- Have audited financial statements in accordance with IFRS: You should maintain accurate financial records and have them audited in line with the International Financial Reporting Standards (IFRS).

- Meet any other specific conditions prescribed by the Free Zone authority: You should comply with any additional requirements set by the respective Free Zone authority.

While the definition of a Free Zone is established, the Cabinet Decision listing the designated Free Zones is still pending. This means that more clarity is awaited on the Free Zones eligible for corporate tax relief in the UAE. Until the decision is announced, you may contact the Free Zone authority to confirm whether your Free Zone is eligible for Corporate Tax relief.

What is Qualifying Activity?

As per Cabinet Decision No 265, business activities for Corporate Tax purposes can be divided into three categories: Qualifying activities, Excluded activities, and Other activities. Each category has different tax implications and is subject to the regulatory oversight of the competent authority. Only qualifying activities are considered for the Free Zone Tax Relief.

Qualifying activities are specific business operations, as defined by the UAE Ministry of Finance, that are eligible for tax relief under the UAE Corporate Tax Laws. These activities, according to the Ministerial Decision No. (265) of 2023, include:

- Manufacturing of goods or materials

- Processing of goods or materials

- Trading of Qualifying Commodities

- Holding of shares and other securities for investment purposes

- Ownership, management, and operation of Ships

- Reinsurance services

- Fund management services

- Wealth and investment management services

- Headquarter services to Related Parties

- Treasury and financing services to Related Parties

- Financing and leasing of Aircraft

- Distribution of goods or materials in or from a Designated Zone

- Logistics services.

- Any activities that are ancillary to the above Qualifying Activities

Apart from these, the Cabinet Decision also outlines seven activities under Excluded Activities. Free Zone businesses involved in these activities may not be eligible for the 0% Tax rate benefits. You can check out the excluded activities in the official document here.

What is Qualifying Income?

Qualifying Income refers to the income that is considered for 0% corporate tax relief in Free Zone entities across the United Arab Emirates. The determination of qualifying income depends on the nature of transactions and the parties involved. Let's look at three scenarios as per the current provisions of the UAE Corporate Tax for Free Zone:

- Transaction with another Free Zone person: If your business transactions are with another business entity within the same Free Zone, the income generated from these transactions can be considered as qualifying income.

- Transaction with a non-Free Zone person: If your business transactions are with an entity outside the Free Zone, the income from these transactions may not be considered as qualifying income.

- Income from all other transactions: All other income, provided they satisfy the de minimis requirements, can be considered as qualifying income.

However, qualifying income does not include income generated from domestic (mainland) or foreign permanent establishments, immovable property outside the Free Zone, and certain other activities like income from non-commercial properties.

Understanding De Minimis Tax Rule

The De Minimis Rule is an important part of the new UAE Corporate Tax for Free Zone regulations. This rule says that if you are a Qualifying Free Zone Person (QFZP) and your non-qualifying income is less than 5% of the total revenue or less than AED 5 million, whichever is lower, you can still enjoy a 0% tax rate. Let's explain this with an example.

Suppose your total revenue is AED 10 million, and your non-qualifying income is AED 400,000, which is 4% of your total revenue. In this case, your business can still benefit from the 0% tax rate because your non-qualifying income is below the 5% limit of the De Minimis requirements.

It is important to know that certain types of income are not included in these calculations. This includes revenue related to immovable property within the Free Zone and income from Domestic or Foreign Permanent Establishments. For example, if you own a building in the Free Zone and earn rental income from it, this income would not be considered qualifying income under the De Minimis Rule.

Likewise, if you have a branch in the mainland UAE or in a foreign country that generates income, it would also not be considered as qualifying income under this rule. This exclusion is important as it ensures that the 0% tax rate benefit is aimed at the operational income of Free Zone companies rather than passive income or revenue generated from a place of business located outside the Free Zone.

As a business operating in a Free Zone, you should not assume that your income is automatically eligible for the 0% tax rate in the UAE. It is essential to consider the nature of your activities, your customer base, and the types of assets you own to calculate your corporate tax for the financial year.

How does Corporate Tax for Free Zone Impact Businesses?

The introduction of the UAE Corporate Tax for Free Zone has significant implications for businesses operating in these zones. If you are no longer eligible for a 0% tax rate, your financial growth could face significant challenges due to the additional tax burden. Therefore, it is crucial for businesses operating in the UAE to take every possible step to prevent unnecessary cash leakages.

One effective way to stop these cash leakages and manage your business expenses effectively is by automating your expense management. With a robust spend management solution like Alaan, you can

- Identify tax-deductible expenses: Alaan allows you to manage your cash flow in real-time and ensure that you are making the most of the tax deductions available to your business.

- Save time and money: With automated expense management, Alaan helps reduce potential errors in tax filing, saving you both time and money.

- Get valuable insights: As a centralized solution, Alaan provides valuable insights into where your company spends its money. This information is useful to plan strategic measures to control costs.

Ready to take control of your expenses and navigate the new tax landscape with ease? Get started with Alaan today.