Understanding how taxes work is a vital part of running any business — and in the UAE, that’s become more important than ever. While business taxes are a certainty, the actual tax rates and systems vary by country. In recent years, the UAE has introduced a federal Corporate Tax (CT) to align with international standards of tax transparency and reduce harmful tax practices. Introduced by the UAE Ministry of Finance, the Corporate Tax law applies to financial years starting on or after June 1, 2023, with a standard rate of 9% on taxable profits.

Whether you're a startup founder, small business owner, or managing finance for a growing company, knowing when to register, how much tax to pay, and how to stay compliant is key to avoiding penalties and building long-term financial stability. This beginner-friendly guide walks you through the essential aspects of business taxation in the UAE — from corporate tax basics and registration requirements to payment deadlines and available exemptions. Let’s break down what you need to know to stay compliant and confident as you manage your business finances.

What is Corporate Tax?

Corporate tax, also known as corporate income tax, is a type of business tax applied to the net income or profit of organisations operating in the UAE, including foreign and local businesses.

Corporate tax is a relatively new concept in the UAE. Historically, the country has had a tax-friendly environment with little to no corporate tax on most businesses. However, recent developments, especially following the UAE’s commitment to global tax standards, have established a corporate tax.

Introducing a corporate tax is part of the UAE's efforts to diversify its economy, reduce its reliance on oil, and comply with international tax transparency standards.

[cta-6]

Corporate Tax in the UAE

Under the new UAE tax regulations, most UAE businesses are subject to corporate tax. Some of the important aspects of tax regulations are:

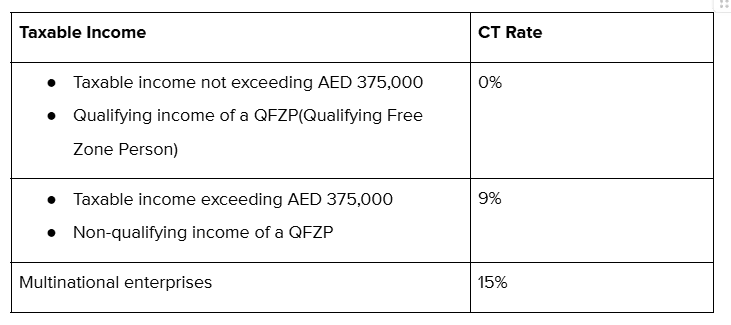

- Tax Rate: The standard corporate tax rate is 9% on profits above AED 375,000 per year. Businesses with annual profits below this amount do not have to pay corporate tax.

- Taxable Profits: The tax is calculated on a company’s net profit, which is the total income after deducting allowable expenses, such as salaries, rent, and other operational costs.

- Tax Filing and Payments: Businesses must file their tax returns yearly to report their profits and expenses and determine their tax liabilities. Once the annual filing is completed, corporate tax must be paid.

Other Taxes Relevant to UAE Businesses

Other than corporate tax, businesses are subjected to several other types of taxes in the UAE, such as:

- VAT (Value Added Tax): VAT is an indirect tax applied to the value added at each production stage or distribution of goods and services. In the UAE, VAT was introduced in 2018 at a rate of 5%. Unlike corporate tax, VAT is not applied to profits but to sales transactions.

- Excise Tax: Applied to certain goods such as tobacco, energy drinks, and sugary beverages, designed to discourage harmful consumption.

- Customs Duties: Taxes applied on imported goods. These duties are typically a percentage of the value of goods entering the UAE.

- DMTT (Domestic Minimum Top-up Tax): The UAE has recently introduced the Domestic Minimum Top-up Tax (DMTT) to align with the OECD/G20's global minimum tax framework under Pillar Two. It will be implemented starting January 1, 2025, per Federal Decree Law No. 60 of 2023. This is introduced to make sure that large multinational companies pay a minimum corporate tax rate of 15% on global profits. The DMTT applies to MNE groups operating in the UAE with consolidated annual revenues of AED 3.1 billion or more in at least two of the last four financial years.

Corporate tax in the UAE

Also Read: UAE Corporate Tax 2024: A Comprehensive Guide For Businesses

Who Should Register for UAE Corporate Tax?

Understanding business taxes is important for businesses operating in the UAE to know who should register for corporate tax. The following entities are mandated to register for corporate tax and get a corporate tax registration number:

Resident Persons

The entities settled in UAE are resident people, including those in offshore jurisdictions, free zones, or on the mainland. This category also includes foreign entities that are managed and controlled in the UAE, as well as individuals operating business within the country.

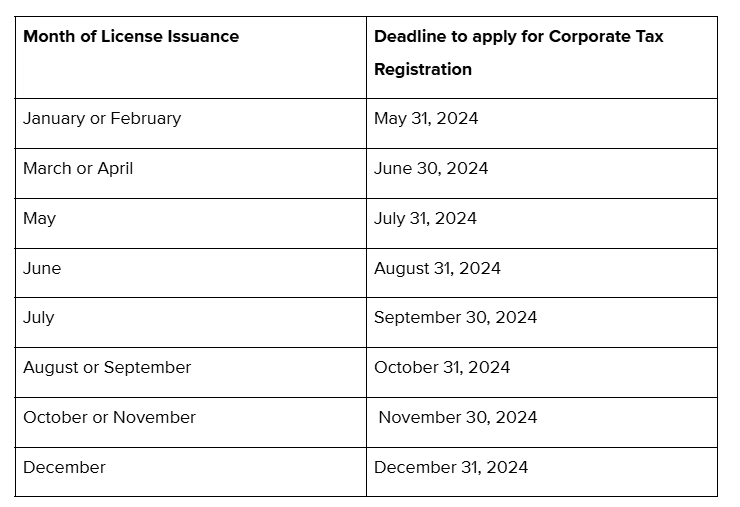

These resident businesses are subject to taxation based on their global income. Moreover, resident taxpayers must register by deadlines determined by the month of their trade license issuance. For instance, if a license was issued in March or April, registration should be completed by June 30, 2024.

Corporate tax registration deadlines for resident persons

Non-Resident Persons

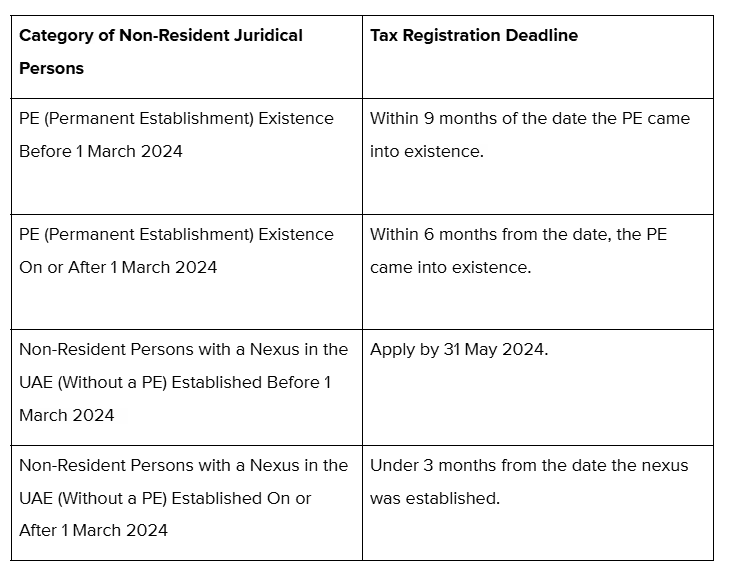

Non-resident persons are the entities having a permanent establishment (PE) or affiliation in the UAE. This involves businesses with considerable economic activity or a physical presence in the UAE. However, they are taxed based only on the income generated from their permanent UAE-based establishments or connections.

The tax registration deadlines for non-residents are:

Who is Exempt From UAE Corporate Tax?

In the United Arab Emirates (UAE), certain entities are exempt from corporate tax under specific conditions. That means they are not liable to pay any corporate tax. These exemptions are designed to promote investment and support various sectors of the economy.

Below is the list of exempt entities:

- Small Businesses

Small businesses with revenue below AED 3 million can claim small business relief. They will be considered as having no taxable income during the relevant tax period and may be subject to simplified compliance obligations. In addition to the threshold revenue, the small business should be a resident of the UAE. Small business relief is not applied to financial institutions or holding companies.

Criteria to apply for small business relief:

- Be a resident person for Corporate Tax purposes in the UAE.

- Have a Revenue of a minimum AED 3,000,000 in the relevant and all previous Tax Periods.

- Not be a member of a Multinational Enterprise (MNE) group or a Qualifying Free Zone Person (QFZP).

- Even if your business has some non-qualifying income, you may still be eligible for SBR if the non-qualifying revenue remains below AED 3 million.

An election to the FTA is required to claim small business relief. This relief will be available for tax periods that end before or on 31 December 2026.

- Free Zone Businesses

The UAE is home to various free zones designed to offer significant advantages, such as 100% foreign ownership, tax exemptions, and full repatriation of profits. Under certain conditions, free zone-based businesses in the UAE are generally exempt from corporate tax. The exemption typically applies if the business operates solely within the free zone and does not conduct business with the UAE mainland.

The other eligibility criteria include:

- Keep a good content level in an Emirates free zone.

- Generate qualified income

- Adhere to the transfer pricing rules and documentation requirements

- Prepare audited financial statements under the International Financial Reporting Standards (IFRS)

- Have non-qualifying income below the minimum threshold.

Here, Qualifying Income for free zone businesses includes transactions with other free zone residents and non-free zone residents in qualifying activities.

The list of qualified activities includes;

- Manufacturing and processing goods

- Holding shares and securities

- Owning and managing ships

- Providing reinsurance and fund management services under UAE regulation

- Offering wealth, investment management, and treasury services

- Headquarters services to related parties

- Financing and leasing aircraft

- Distributing goods within designated zones

- Providing logistics and ancillary services supporting qualifying activities

Aside from small businesses and free zone businesses, the following entities are also exempt from corporate tax in the UAE:

- Government entity;

- Government-controlled entity;

- person engaged in a certain extractive business;

- person involved in a certain non-extractive natural resource business;

- certain qualifying investment funds;

- qualifying public benefit entity;

- pension or social security fund; and

- any other persons as may be specified in a decision issued by the Cabinet.

Key Corporate Tax Obligations for UAE-Based Businesses

With the introduction of corporate tax in the UAE, understanding business taxes and complying with the tax regulations is necessary to avoid penalties and ensure smooth operations. Some of the major corporate tax compliances for UAE-based companies are:

- Registration With The Federal Tax Authority (FTA)

All businesses operating in the UAE — including those with profits below the AED 375,000 threshold — are required to register for corporate tax with the Federal Tax Authority (FTA). Businesses operating in free zones must also register, regardless of whether they qualify for a 0% rate, particularly if they engage in non-qualifying activities or conduct business with the UAE mainland.

Small businesses with revenue of AED 3 million or less may apply for Small Business Relief (SBR), but registration remains mandatory to avail the relief.

A standard penalty of AED 10,000 applies for late corporate tax registration. However, under Cabinet Decision No. 10 of 2024, the FTA has introduced a one-time waiver. To benefit from the waiver, businesses must file their first corporate tax return or annual statement within seven months from the end of their first tax period.

- Filing Corporate Tax Returns

UAE companies have to file an annual corporate tax return to the FTA. This return is important for reporting income, expenses, and tax liabilities. The return has to be filed nine months after the end of the company's fiscal year. Businesses also must ensure that their tax returns are correct and backed by appropriate evidence, including, in some cases, audited financial statements. Failure to submit the tax return within the allowed time may cause penalties.

- Maintaining Proper Financial Records

To comply with UAE corporate tax laws, businesses must maintain accurate accounting records that capture all income, expenses, assets, and liabilities. These records are essential for filing tax returns and ensuring transparency. In some cases, particularly for businesses in free zones, companies may be required to prepare audited financial statements in accordance with International Financial Reporting Standards (IFRS), providing an added layer of compliance and assurance for tax authorities.

- Annual Tax Audits and Assessments

The FTA may conduct audits to ensure that businesses comply with corporate tax regulations. During these audits, businesses are required to cooperate with tax authorities and provide necessary documentation. After reviewing the tax return, the FTA will issue a tax assessment. If discrepancies are found during an audit, the business may be required to pay additional taxes, face penalties, or incur interest charges. Businesses need to maintain accurate records to facilitate these audits and avoid potential issues.

- Compliance with Tax Incentives and Exemptions

Free zone businesses that meet certain conditions, such as generating qualifying income and adhering to transfer pricing rules, may benefit from corporate tax exemptions. Similarly, small businesses meeting the revenue threshold for small business relief are exempt from corporate tax, but they still need to comply with simplified reporting requirements. These exemptions are part of the UAE's broader effort to support business growth, particularly for small and medium-sized enterprises (SMEs) and businesses in specialised zones.

How Businesses in the UAE Pay Taxes

Once a business is registered with the Federal Tax Authority (FTA) and has filed its corporate tax return, the next step is fulfilling its tax payment obligation. Understanding the process and deadlines is essential to ensure compliance and avoid penalties.

1. Tax Payment Deadline

Businesses must pay their corporate tax liability within nine months from the end of their financial year.

For example, if your business’s financial year ends on December 31, 2024, your corporate tax payment must be made by September 30, 2025.

This deadline applies to both filing the return and settling any tax due. Delays beyond this period may trigger penalties or interest charges.

2. Accepted Payment Methods

Tax payments are made through the FTA’s official e-Services portal (EmaraTax). The platform allows various payment options, including:

- Bank transfers

- e-Dirham cards

- Debit or credit cards

Once the payment is completed, a payment receipt is issued by the FTA, which should be saved for recordkeeping and audit purposes.

3. Late Payment Penalties

Failing to pay the tax liability on time can result in:

- A fixed administrative penalty for late registration: AED 10,000 for the first offense and AED 20,000 for repeat offenses.

- Late payment penalties: Typically, interest accrues at a rate of 4% per annum on the unpaid amount.

- Late filing fines: These range from AED 500 to AED 50,000, depending on the extent of the delay and company size.

To avoid these penalties, it’s important to plan ahead and ensure all documents and funds are ready well before the deadline.

4. Tax Return vs. Tax Payment

It’s worth noting that filing a tax return and paying the tax are two distinct actions, though they share the same deadline. Filing the return involves declaring the company’s income, expenses, and tax liability, while payment involves settling the owed tax amount.

Being timely with both steps ensures a clean compliance record with the FTA.

How Alaan Helps with Tax Compliance in the UAE

Managing business taxes in the UAE goes beyond just filing returns — it requires continuous control over spending, accurate expense categorisation, and audit-ready documentation. While Alaan isn’t a tax filing platform, it plays a vital supporting role in helping businesses maintain financial accuracy and simplify compliance.

Here’s how:

- Real-Time Expense Visibility: Alaan provides a centralised view of all business spending, helping finance teams monitor and reconcile transactions with minimal delays or errors.

- Automated Expense Categorisation: With AI-powered tagging and customisable rules, businesses can ensure that expenses are properly classified, improving VAT recovery and CT reporting accuracy.

- Digital Recordkeeping: Every transaction made via Alaan is stored with receipts and contextual data, reducing the burden of manual documentation during FTA audits.

- Custom Spend Controls: Set card limits, vendor restrictions, and approval workflows to prevent out-of-policy or unbudgeted spending, aligning operational behaviour with financial plans.

[cta-8]

- Data Export & ERP Integration: Easily export or sync data to accounting software for streamlined reporting and reconciliation.

By enabling accurate and efficient expense management, Alaan empowers UAE businesses to stay compliant while keeping operations lean and accountable.

Conclusion

Navigating business taxes in the UAE can be overwhelming, especially for companies adjusting to new corporate tax regulations. From understanding who needs to register and what counts as taxable income, to staying on top of FTA deadlines and recordkeeping requirements, compliance demands proactive financial management.

Fortunately, businesses that stay informed, organised, and well-documented can avoid penalties and maximise their tax efficiency. Whether you're a small business owner, finance lead, or founder, taking a structured approach to managing tax obligations is key to long-term financial resilience.

At Alaan, we understand how complex and time-consuming tax compliance can be — especially when you're scaling a business in a dynamic market like the UAE.

That’s why our spend management platform is designed to give you the visibility, control, and efficiency your finance team needs to stay compliant and agile. From real-time tracking to smart policy controls, we help you keep your finances clean, clear, and audit-ready — without adding overhead.

Want to simplify your corporate tax prep and take control of your business spend?

We’d love to show you how.