At month end, finance teams often face a familiar situation. A cost clearly belongs to the current period, but the supplier invoice has not yet arrived. At the same time, there are other expenses already sitting in the system with invoices awaiting approval and payment. Both represent obligations, but they cannot be recorded in the same way.

This is where the distinction between accrued expenses and accounts payable becomes important. The difference is not just technical. It affects how accurately expenses are recorded, how liabilities are reported, and how clean the close process remains.

In this blog, we will explain the difference between accrued expenses and accounts payable, how each is recorded, when one moves into the other, and why the distinction matters for accurate month-end reporting.

TL;DR

- Accrued expenses are costs incurred but not yet invoiced.

- Accounts payable are liabilities based on received supplier invoices.

- Accrued expenses often involve estimates, while accounts payable reflects confirmed amounts.

- Some accrued expenses move into accounts payable once invoices are received.

- Clean invoice capture and reconciliation reduce errors across both categories.

What Accrued Expenses Mean

Accrued expenses are liabilities for costs that a business has already incurred but has not yet been billed for or paid. These expenses are recorded to ensure that financial statements reflect the correct period, even when invoices have not been received.

This approach follows accrual accounting, where expenses are recognised when they are incurred rather than when cash is paid. Without accruals, expenses may be delayed into a later period, which can distort financial reporting.

Common examples include:

- Salaries earned by employees but not yet paid

- Utility usage for the month where the invoice arrives later

- Interest that has accumulated but not yet been charged

- Services received from vendors before billing

- Month-end estimates for recurring expenses

In most cases, accrued expenses rely on internal data such as contracts, usage patterns, or historical trends to estimate the correct amount.

Also Read: Accrued Expenses Definition Types Differences

What Accounts Payable Mean

Accounts payable refers to amounts a business owes to suppliers after receiving an invoice for goods or services. Unlike accrued expenses, these liabilities are supported by formal documentation and clearly defined payment terms.

Accounts payable is typically more structured because each entry is linked to a supplier invoice. This includes details such as invoice number, amount, due date, and applicable taxes.

Common examples include:

- Vendor invoices for software subscriptions

- Supplier invoices for inventory or goods delivered

- Contractor invoices awaiting approval

- Utility bills that have already been received

- Professional service invoices

Accounts payable forms a key part of the payment process. Once invoices are verified and approved, they are scheduled for payment based on agreed terms.

Related: Accounts Payable Examples Explained

Accrued Expense Vs Accounts Payable

While both accrued expenses and accounts payable represent liabilities, they differ in timing, certainty, and documentation. Understanding these differences helps finance teams record expenses accurately and avoid duplication.

The key distinction is simple but critical. Accrued expenses ensure that costs are recorded in the correct period, while accounts payable ensures that invoiced obligations are tracked and paid correctly.

Why The Difference Matters At Month End

The difference between accrued expenses and accounts payable becomes most important during the month-end close. Misclassification can lead to inaccurate financial statements and operational issues.

In fact, finance teams already spend a significant amount of time on reconciliation, with PwC-linked research estimating that around 30-40% of finance effort goes to manual matching and reconciliation.

If expenses are not accrued when required, costs may be understated in the current period and overstated in the next. If items are incorrectly recorded as accounts payable without an invoice, liabilities may be misrepresented or duplicated later when the invoice arrives.

Maintaining a clear distinction helps finance teams:

- Ensure expenses are recorded in the correct period

- Present accurate current liabilities on the balance sheet

- Avoid duplicate entries when invoices arrive

- Improve the speed and accuracy of the close process

- Maintain a cleaner audit trail

This distinction also supports better cash flow planning, as finance teams can separate estimated obligations from confirmed payables with due dates.

Also Read:

Accounting Process Important Steps

Related:

GL In Accounting Double Entry

How Accrued Expenses Are Recorded

Accrued expenses are recorded through adjusting entries at the end of an accounting period. The goal is to recognise costs that belong to the current period, even if the invoice has not yet been received.

1. Identify The Expense Incurred

Finance teams first identify costs that relate to the current period but have not yet been billed. This often comes from contracts, usage data, timesheets, or recurring expense patterns.

2. Estimate The Amount

Since no invoice exists yet, the amount is estimated based on available information. The accuracy of this estimate depends on the quality of internal data and historical trends.

3. Record The Accrual Entry

A journal entry is recorded to recognise the expense and corresponding liability:

- Debit the relevant expense account

- Credit accrued expenses

This ensures the expense is reflected in the correct accounting period.

4. Reverse The Accrual When Needed

In the next period, the accrual may be reversed to avoid duplication once the actual invoice is recorded.

5. Record The Actual Invoice In Accounts Payable

When the supplier invoice arrives, it is recorded in accounts payable using the actual amount, replacing the earlier estimate.

How Accounts Payable Is Recorded

Accounts payable entries are based on supplier invoices and follow a more structured process compared to accruals.

1. Receive The Supplier Invoice

The invoice enters the accounts payable workflow, either through manual entry or automated systems.

2. Verify Invoice Details

Finance teams review key details such as supplier name, invoice amount, due date, tax information, and supporting documentation. Matching against purchase orders or contracts may also be required.

3. Record The Liability

The invoice is recorded using a journal entry:

- Debit the relevant expense or asset account

- Credit accounts payable

This creates a confirmed liability with a defined payment obligation.

4. Route For Approval

Invoices are typically sent through approval workflows before payment is authorised. This step ensures that spending aligns with budgets and policies.

5. Settle The Payable

Once approved, the invoice is paid based on agreed terms. The entry is cleared by debiting accounts payable and crediting cash or bank.

Also Read: Accounts Payable Automation Invoice Management Software

When Accrued Expenses Become Accounts Payable

In many cases, an expense moves from an accrual to accounts payable as part of the normal accounting cycle.

This typically happens when the business has already recognised an expense through an accrual, and the supplier invoice is received in a later period.

A simple example illustrates this flow:

- In March, a business incurs AED 12,000 in marketing services, but no invoice is received

- The finance team records an accrued expense in March to reflect the cost

- In April, the supplier sends the invoice for AED 12,000

- The March accrual is reversed, and the invoice is recorded in accounts payable

This process ensures that the expense is not recorded twice and that both periods remain accurate.

Understanding this transition is important for maintaining a clean close process and avoiding duplication or misstatement of liabilities.

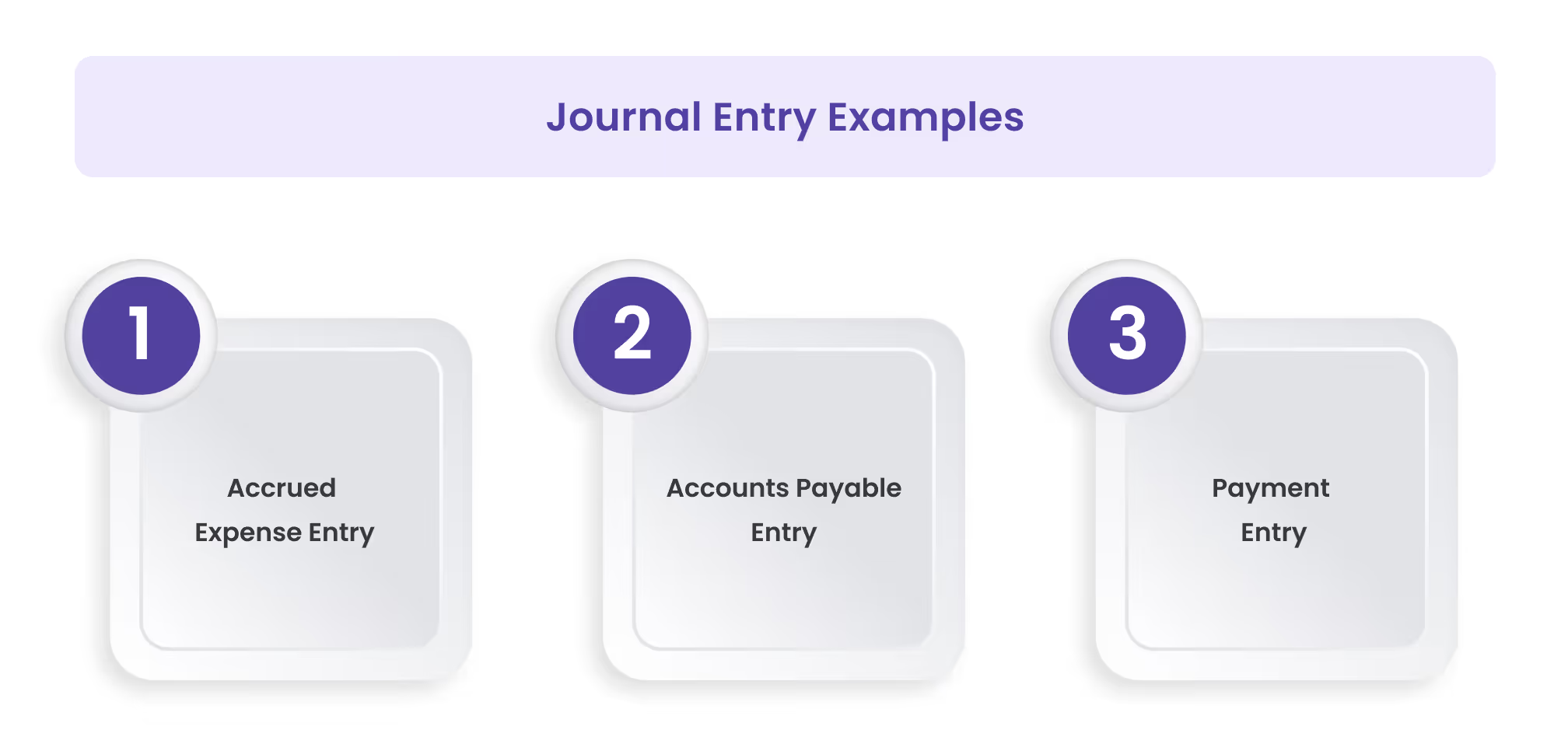

Journal Entry Examples

Clear journal entries help reinforce how accrued expenses and accounts payable are treated in practice.

1. Accrued Expense Entry

A business incurs AED 8,000 in utility costs in March, but the invoice has not been received.

- Debit Utilities Expense AED 8,000

- Credit Accrued Expenses AED 8,000

This recognises the expense in the correct period.

2. Accounts Payable Entry

In April, the utility invoice for AED 8,000 is received.

- Debit Utilities Expense AED 8,000

- Credit Accounts Payable AED 8,000

If the accrual was reversed first, this ensures the expense is not duplicated.

3. Payment Entry

The business pays the supplier AED 8,000.

- Debit Accounts Payable AED 8,000

- Credit Bank AED 8,000

This clears the liability.

Common Mistakes Businesses Make

Even when the definitions are clear, errors often happen during execution. These mistakes usually show up during month-end close, reconciliation, or audit review.

1. Recording Unbilled Costs Directly As Accounts Payable

Some businesses record expenses in accounts payable even when no invoice has been received. This creates confusion later when the actual invoice arrives and can lead to duplication.

2. Forgetting To Reverse Accruals

Accruals are often temporary entries. If they are not reversed when the actual invoice is recorded, the same expense may be counted twice.

3. Recording The Same Expense Twice

This typically happens when an accrual is recorded in one period and the invoice is recorded in the next period without adjusting the original entry.

4. Treating All Unpaid Costs The Same Way

Not all unpaid expenses are accounts payable. Some belong in accrued expenses, depending on whether an invoice exists. Mixing the two reduces reporting accuracy.

5. Missing Corporate Card Or Employee Expense Accruals

Expenses incurred through corporate cards or employee reimbursements may not always have invoices at month end. If these are not accrued, expenses can be understated.

6. Closing The Month Without Reconciling Liabilities

Skipping reconciliation between accrued expenses, accounts payable, and actual supporting documents can leave gaps in financial records and create issues later.

This remains a major operational challenge because reconciliation processes are still highly manual for many finance teams, often with limited visibility into completion status and unresolved discrepancies.

Also Read:

Account Reconciliation Importance Steps

Related:

Corporate Card Reconciliation Guide

How The Difference Affects Cash Flow

Accrued expenses and accounts payable both represent obligations, but they affect cash flow visibility in different ways.

Accounts payable usually comes with defined payment terms. This makes it easier to plan cash outflows because due dates are known and can be scheduled.

Accrued expenses, on the other hand, are often estimates without a confirmed invoice or due date. While they reflect expected obligations, they may not provide precise timing for when cash will leave the business.

For finance teams, this distinction is important for cash planning. Separating estimated liabilities from confirmed payables helps in building more accurate cash flow forecasts and avoiding liquidity surprises.

Related: Manage Business Cash Flow Effectively

How Alaan Helps Finance Teams Improve Expense Accuracy

The difference between accrued expenses and accounts payable depends heavily on the quality of underlying data. Without clear visibility into expenses, invoices, and approvals, it becomes harder to classify liabilities correctly and maintain a clean close process.

At Alaan, we help finance teams improve the execution layer that supports these decisions. While accounting judgement still determines how entries are classified, better data makes those decisions more accurate and consistent.

- Corporate Cards With Spend Controls

Businesses can manage spending with defined limits and policies, reducing untracked or late-recorded expenses. - Real Time Visibility Into Expenses

Finance teams can see transactions as they happen, making it easier to identify costs that need to be accrued before month end. - Centralised Receipt And Invoice Capture

All supporting documents are linked to transactions, improving traceability and reducing missing information. - Structured Approval Workflows

Expenses are reviewed before payment, ensuring that liabilities are properly documented and validated. - Payment Execution With Upfront Financial Clarity (SuperPay)

When accounts payable balances move into actual payments, SuperPay enables finance teams to review FX rates, fees, and final payment cost before execution. This ensures that liabilities recorded in the books translate into payments that are accurate, transparent, and aligned with expected cash outflows. - Seamless Accounting Integration

Integrations with systems like Xero, QuickBooks, NetSuite, and Microsoft Dynamics help ensure that expense data flows cleanly into accounting records.

By improving how expenses are captured and tracked, Alaan helps finance teams reduce errors in both accrued expenses and accounts payable, leading to a more accurate and efficient close process.

Also Read:

Invoice Automation Benefits

Related:

Modern Expense Management Guide

Conclusion

Accrued expenses and accounts payable are both essential parts of financial reporting, but they serve different purposes. Accrued expenses ensure that costs are recorded in the correct period before invoices arrive, while accounts payable tracks confirmed obligations based on supplier invoices.

For finance teams, the distinction is not just technical. It directly affects reporting accuracy, liability tracking, and the efficiency of the month-end close. Misclassification can lead to duplicate entries, misstated expenses, and reconciliation challenges.

The most effective approach is to combine clear accounting practices with strong operational controls. When expenses are captured early, supported by proper documentation, and tracked consistently, it becomes easier to classify liabilities correctly and maintain accurate financial records.

If you want to improve how your business captures and manages expense data, you can explore how Alaan helps finance teams maintain visibility, streamline approvals, and keep reconciliation cleaner at month end. Book a demo to see how better spend control supports more accurate financial reporting.

Frequently Asked Questions

1. Can A Business Record An Accrued Expense Without An Invoice

Yes. Accrued expenses are specifically used when a cost has been incurred but the invoice has not yet arrived. The amount is usually based on a contract, usage data, prior billing pattern, or a reasonable estimate.

2. What Happens When The Invoice Arrives After An Accrual Is Recorded

The accrual is usually reversed, and the actual invoice is recorded in accounts payable. This prevents the same expense from being counted twice and ensures the final liability reflects the confirmed invoice amount.

3. Why Do Accrued Expenses Matter During Audit

Accrued expenses show whether the business recorded costs in the correct accounting period. Auditors may review accruals to check whether expenses were understated, overstated, duplicated, or unsupported by reasonable evidence.

4. Can Accounts Payable Exist Without An Expense Entry

Yes, in some cases. Accounts payable may relate to asset purchases, inventory, prepaid expenses, or capital expenditure rather than a direct expense. The payable records the obligation, while the debit side depends on the nature of the purchase.

5. Are Accrued Expenses Always Estimated

Most accrued expenses involve some level of estimation because the invoice has not yet arrived. However, some estimates can be highly reliable if based on fixed contracts, payroll schedules, loan interest calculations, or predictable recurring costs.

6. How Can Finance Teams Reduce Accrual And AP Errors

Errors reduce when invoices, receipts, approvals, contracts, and payment records are captured early and reconciled consistently. The biggest risks usually come from missing invoices, unreversed accruals, duplicate entries, and unclear ownership during month-end close.