Cash flow problems rarely show up first in the profit line. They show up when collections slow, supplier payments remain due, and finance teams cannot clearly explain why the bank balance moved differently from reported performance.

That gap is visible in the UAE. Atradius’ 2025 UAE payment practices report found that overdue invoices affect 58% of B2B sales, with delays largely driven by administrative inefficiencies in customer payment processes. That kind of timing pressure makes the cash flow statement more than a reporting formality. It becomes the clearest way to see whether cash is coming from operations, financing, or one-off movements.

A cash flow statement helps finance teams read liquidity properly. It shows how money moved through operating, investing, and financing activities, so a business can distinguish healthy operating cash generation from temporary increases caused by borrowing, asset sales, or delayed payments.

In this blog, we will break down what a cash flow statement means, how it is structured, and how finance teams use it as a practical tool for cash flow analysis and financial management.

TL;DR

- A cash flow statement shows how money actually moved through the business during a specific period.

- It separates cash movement into operating, investing, and financing activities, which helps finance teams understand the source of liquidity changes.

- Profit and cash flow can move differently because revenue, expenses, depreciation, receivables, and payables are treated differently in accounting.

- The headline increase or decrease in cash is not enough; the source of that movement determines whether the position is healthy or temporary.

- A reliable cash flow statement depends on timely reconciliation, accurate categorisation, complete documentation, and clear spend controls.

What A Cash Flow Statement Means In Practice

A cash flow statement is a financial report that tracks the inflow and outflow of cash within a business over a specific period. It provides a clear view of how cash is generated and how it is used.

Unlike the income statement, which includes non-cash items, the cash flow statement focuses only on actual cash movement. This makes it one of the most reliable ways to understand liquidity and financial flexibility.

In practical terms, it answers key questions such as whether the business is generating enough cash from its operations, whether it is investing heavily in assets, and how it is funding its activities.

Why The Cash Flow Statement Matters In Financial Management

The cash flow statement plays a central role in financial management because it connects operational performance with actual liquidity. It helps businesses understand not just whether they are profitable, but whether they have the cash required to meet obligations and support growth.

For finance teams, this report is often used to:

- Assess Liquidity Position

It shows whether the business has enough cash to cover short-term commitments. - Evaluate Operating Strength

Consistent positive operating cash flow indicates that core activities are generating real cash. - Understand Funding Structure

Financing activities reveal how much the business depends on external capital. - Support Planning And Decision Making

Cash flow insights help guide budgeting, forecasting, and investment decisions.

Because of this, the cash flow statement is not just a reporting requirement. It is a key management tool used to monitor financial health and guide strategy.

The Three Sections Of A Cash Flow Statement

A cash flow statement is structured into three main sections. Each section represents a different type of activity and provides insight into how cash is moving through the business. IFRS IAS 7 also requires cash flows to be classified into operating, investing, and financing activities, which is why this structure is the standard way to understand the source of cash movement rather than only the final cash balance.

1. Operating Cash Flows

Operating cash flows reflect the cash generated or used by the core business activities. This includes cash received from customers and cash paid for expenses such as suppliers, salaries, and operating costs.

This section is often considered the most important because it shows whether the business model itself is generating sustainable cash.

Also Read: Cash Flow Operating Activities Guide

2. Investing Cash Flows

Investing cash flows relate to the purchase or sale of long-term assets such as equipment, systems, or investments.

These flows can vary significantly from period to period and often reflect strategic decisions rather than day-to-day operations.

3. Financing Cash Flows

Financing cash flows include activities related to funding the business, such as taking loans, repaying debt, or receiving investment.

This section helps explain how the business is managing its capital structure.

What The Cash Flow Statement Does Not Tell You On Its Own

While the cash flow statement is highly useful, it does not provide a complete picture on its own. The report shows how cash has moved, but it does not always explain whether those movements are sustainable or desirable.

For example, a business may show strong positive cash flow because it has taken on new debt. Another may show negative cash flow because it is investing in long-term growth.

Without understanding the context behind these movements, it is easy to misinterpret the data.

Why A Cash Flow Statement Is Not The Same As Profit

Profit is based on accounting principles, while the cash flow statement reflects actual cash movement. This difference can create significant gaps between reported profit and available cash.

Revenue may be recorded before cash is received, and expenses may be recognised before payment is made. Additionally, non-cash items such as depreciation affect profit but do not impact cash.

This is why businesses that appear profitable on paper can still face liquidity challenges.

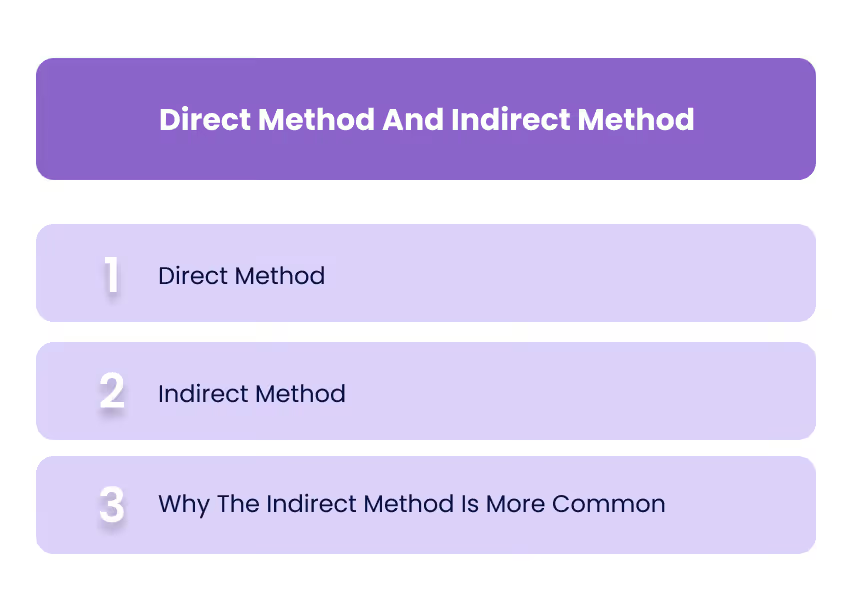

Direct Method And Indirect Method

Cash flow statements can be prepared using two different methods. Both lead to the same final result, but they present operating cash flows differently.

1. Direct Method

The direct method shows actual cash inflows and outflows from operating activities. It lists items such as cash received from customers and cash paid to suppliers.

This method provides a clearer view of cash movement but is less commonly used in practice.

2. Indirect Method

The indirect method starts with net income and adjusts it for non-cash items and changes in working capital to arrive at operating cash flow.

This method is more widely used because it aligns closely with existing accounting records.

3. Why The Indirect Method Is More Common

Most businesses use the indirect method because it is easier to prepare and integrates with financial reporting systems. However, both methods provide the same overall cash flow result.

Example Of A Cash Flow Statement

A cash flow statement becomes easier to understand when the structure is viewed in one place. The format below is a simplified example for a business reviewing one reporting period. It is not a statutory template, but it shows how operating, investing, and financing activities usually come together.

In this example, the business generated AED 170,000 from operations, used AED 60,000 for investing activities, and received a net AED 60,000 from financing activities. The final net increase in cash is AED 170,000.

The important point is not only that cash increased. The source matters. Here, operating cash flow is positive, which suggests the core business generated cash during the period. If the same AED 170,000 increase had come mainly from borrowing, the interpretation would be different.

How Finance Teams Use A Cash Flow Statement As A Management Report

A cash flow statement becomes significantly more valuable when it is used as a management report rather than treated as a compliance document. Finance teams do not just prepare it for reporting purposes. They use it to explain how cash is actually behaving inside the business.

This is where cash flow analysis and cash flow management accounting come into play. The statement helps connect inflow and outflow patterns to operational decisions, making it easier to identify where pressure or strength is coming from.

1. Tracking The Quality Of Operating Cash Flow

Finance teams look beyond whether operating cash flow is positive. They assess whether it is consistent, improving, or dependent on temporary factors such as delayed payments or short-term adjustments.

A business with stable operating cash flow is generally more resilient than one that relies heavily on financing inflows.

Also Read: Cash Flow Operating Activities Guide

2. Identifying Working Capital Pressure Early

Changes in receivables, payables, and inventory directly affect cash movement. A buildup in receivables or inventory can reduce available cash even when revenue is growing.

The cash flow statement helps highlight these shifts, allowing teams to act before liquidity becomes a problem.

Related: Understanding Trade Receivables Key Concepts

3. Explaining Large Cash Movements To Management

Significant inflows or outflows often need explanation, especially during board reviews or internal reporting.

The statement helps break down these movements into operating, investing, and financing categories, making it easier to communicate what changed and why.

4. Supporting Forecasting And Short Term Planning

Historical cash flow data feeds directly into forecasting models. By analysing patterns in inflows and outflows, finance teams can build more accurate projections.

This supports planning around payments, investments, and funding requirements.

Also Read:

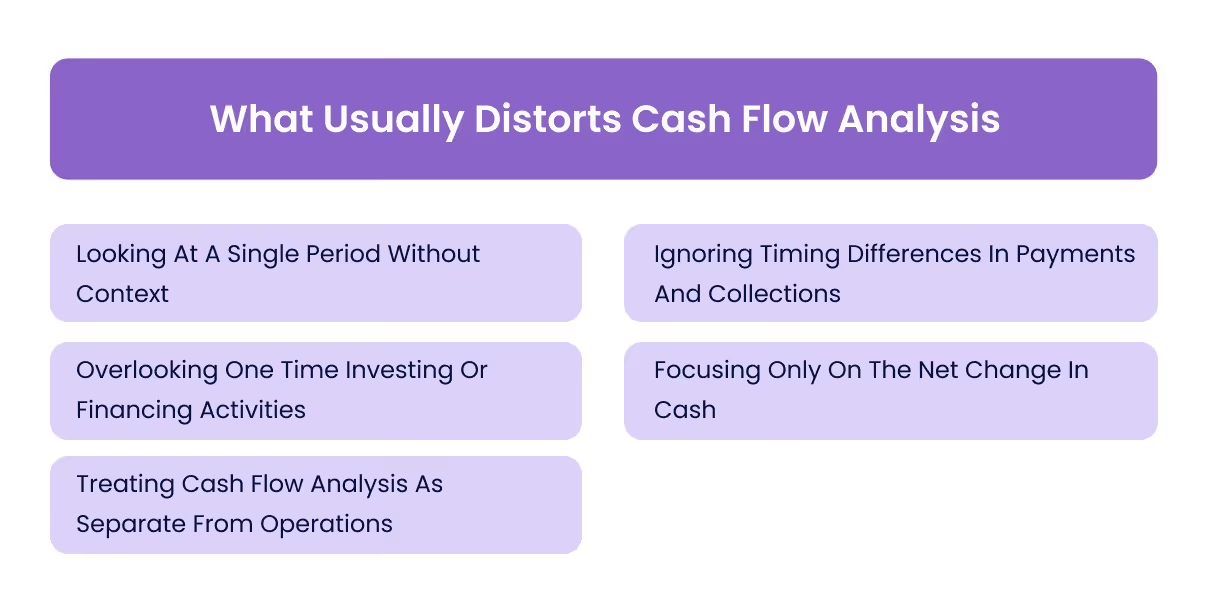

What Usually Distorts Cash Flow Analysis

While the cash flow statement provides clarity, it can still be misinterpreted if certain factors are not considered. Distortions often come from timing differences, one-off events, or incomplete analysis.

1. Looking At A Single Period Without Context

Cash flow can fluctuate due to seasonality, large transactions, or timing differences. Analysing one period in isolation can lead to incorrect conclusions.

A trend across multiple periods provides a more reliable view.

2. Ignoring Timing Differences In Payments And Collections

Cash inflows and outflows do not always align with when revenue or expenses are recorded. Delayed collections or early payments can temporarily distort cash flow.

Understanding these timing differences is essential for accurate interpretation.

3. Overlooking One Time Investing Or Financing Activities

Large asset purchases, loan repayments, or new funding can significantly impact cash flow in a single period.

These events need to be separated from regular operations to understand underlying performance.

4. Focusing Only On The Net Change In Cash

The headline net cash flow figure does not explain the source of the movement. Positive cash flow driven by borrowing is very different from positive cash flow generated through operations.

Breaking down the components is critical for meaningful analysis.

5. Treating Cash Flow Analysis As Separate From Operations

Cash flow is directly influenced by operational decisions such as pricing, collections, procurement, and inventory management.

Analysing it in isolation from these activities reduces its usefulness.

Where Cash Flow Statements Break Down In Practice

Even when the structure of the cash flow statement is correct, the quality of the report can suffer due to gaps in underlying processes. The issue is rarely the format. It is usually the reliability of the data feeding into it.

1. Delayed Or Incomplete Reconciliation

If transactions are not recorded and reconciled on time, the cash flow statement may not reflect the current financial position accurately.

This reduces its usefulness for decision-making.

2. Weak Expense Categorisation

When expenses are not properly categorised, it becomes difficult to understand where cash is being spent. This limits the ability to analyse patterns or identify inefficiencies.

3. Missing Or Fragmented Documentation

Incomplete invoices or missing receipts create gaps in financial records. This makes it harder to validate transactions and reduces confidence in the report.

4. Unstructured Approval Processes

Without clear approval workflows, spending decisions may not align with budgets or priorities. This leads to inconsistent cash outflows that are difficult to track and control.

5. Limited Visibility Into Real Time Spend

If finance teams rely only on month-end data, they may miss early signals of cash pressure. Limited visibility delays response and reduces the effectiveness of cash management.

How Alaan Helps Improve The Quality Of Cash Flow Reporting

A cash flow statement is only as reliable as the data behind it. Even when the structure is correct, delays in recording, weak categorisation, or missing documentation can reduce its usefulness as a management report.

At Alaan, we focus on improving the execution layer that feeds into cash flow reporting. This helps finance teams move from reactive reporting to more timely and reliable analysis.

- Corporate Cards With Spend Controls And Clear Boundaries

Businesses can issue cards with defined limits and merchant restrictions, ensuring that spending aligns with approved categories and reduces unexpected outflows. - Structured Approval Workflows Before Cash Is Committed

Expenses can be routed through approval flows before transactions occur, helping maintain consistency and control over cash usage. - Real Time Visibility Into Business Spend

Finance teams can track cash outflows as they happen across teams, vendors, and categories, instead of relying only on month-end reports. - Centralised Invoice And Receipt Capture

All supporting documents are linked to transactions, improving accuracy and reducing gaps in reporting. - Seamless Accounting Integration

Integrations with systems like Xero, QuickBooks, NetSuite, and Microsoft Dynamics ensure that transaction data flows directly into accounting, improving the timeliness of financial reports.

This approach ensures that the cash flow statement reflects actual business activity more accurately and can be used confidently for analysis and decision-making.

Also Read:

Conclusion

A cash flow statement is one of the most useful financial reports when it is read correctly. It shows how cash moves through a business, highlights liquidity position, and provides insight into operational strength.

However, the value of the statement depends on how it is interpreted and how reliable the underlying data is. Looking only at the headline numbers without understanding the sources of cash movement can lead to incorrect conclusions.

When finance teams combine structured reporting with strong visibility into spending and approvals, the cash flow statement becomes a powerful tool for planning, control, and decision-making.

If you want to improve how your business tracks and manages cash movement, you can explore how Alaan helps finance teams maintain visibility, enforce approvals, and ensure that financial reporting remains accurate and actionable. Book a Demo Today!

Frequently Asked Questions

1. Why Is A Cash Flow Statement Important Even For Profitable Businesses

Profit does not always reflect actual cash availability. The cash flow statement shows whether the business has enough liquidity to meet its obligations.

2. Which Section Of The Cash Flow Statement Matters The Most

Operating cash flow is usually the most important because it reflects the cash generated from core business activities.

3. Can A Business Have Positive Cash Flow And Still Face Financial Issues

Yes, positive cash flow may result from borrowing or asset sales, which may not indicate long-term financial strength.

4. How Often Should Businesses Review A Cash Flow Statement

Most businesses review it monthly, but more frequent reviews may be needed when cash position is changing rapidly.

5. What Is The Difference Between A Cash Flow Statement And A Cash Flow Forecast

A cash flow statement shows past cash movement, while a forecast projects future inflows and outflows.

6. Why Does A Cash Flow Statement Matter For Corporate Decision Making

It provides insight into liquidity, helps evaluate financial decisions, and supports planning for investments, expenses, and funding needs.