A company can report strong profits and even positive operating cash flow, yet still have limited cash available for shareholders. This happens because cash must first cover reinvestment needs such as capital expenditure, working capital, and debt obligations before anything can flow to equity holders.

Free cash flow to equity (FCFE) helps answer a more precise question: after all operating needs, reinvestment, and financing effects, how much cash is actually available to shareholders?

In this blog, we will explain what free cash flow to equity means, how to calculate FCFE, how it differs from FCFF, and how finance teams can interpret it for valuation and shareholder cash flow analysis.

TL;DR / Key Takeaways

- Free cash flow to equity measures cash available to equity holders after operating needs, reinvestment, and debt effects.

- The core formula is FCFE = Cash Flow From Operations − Capex + Net Borrowing.

- FCFE differs from FCFF because it includes debt impact and focuses only on equity holders.

- Positive FCFE does not guarantee dividends, and negative FCFE is not always a problem.

- FCFE is only meaningful when operating cash flow, capex, and debt data are accurately recorded.

What Free Cash Flow To Equity Means

Free cash flow to equity represents the cash that remains available to common shareholders after a business has:

- Generated cash from its operations

- Invested in assets required to sustain or grow the business

- Accounted for borrowing and debt repayments

It is often referred to as a levered cash flow metric because it reflects the effect of debt on the company’s cash position.

Unlike accounting profit, FCFE focuses only on actual cash movement. This focus has become more important in recent financial analysis, where free cash flow is widely treated as a primary measure of liquidity, operational efficiency, and investment capacity.

For finance teams, FCFE is particularly useful because it links operational performance, reinvestment decisions, and financing structure into a single measure of shareholder cash capacity.

Also Read: Cash Flow Operating Activities Guide

Free Cash Flow To Equity Formula

There are multiple ways to calculate FCFE depending on the starting point, but the most commonly used version starts from operating cash flow.

FCFE = CFO - Capex + Net\ Borrowing

This formula shows that FCFE is derived from three core components:

- Cash Flow From Operations (CFO)

Cash generated from the company’s core business activities - Capital Expenditure (Capex)

Cash spent on assets such as equipment, infrastructure, or technology - Net Borrowing

New debt raised minus debt repayments

An expanded version starting from net income is also commonly used:

FCFE = Net\ Income + Non\ Cash\ Charges - Fixed\ Capital\ Investment - Working\ Capital\ Investment + Net\ Borrowing

This version is particularly useful in financial modelling when working directly with income statement and balance sheet data.

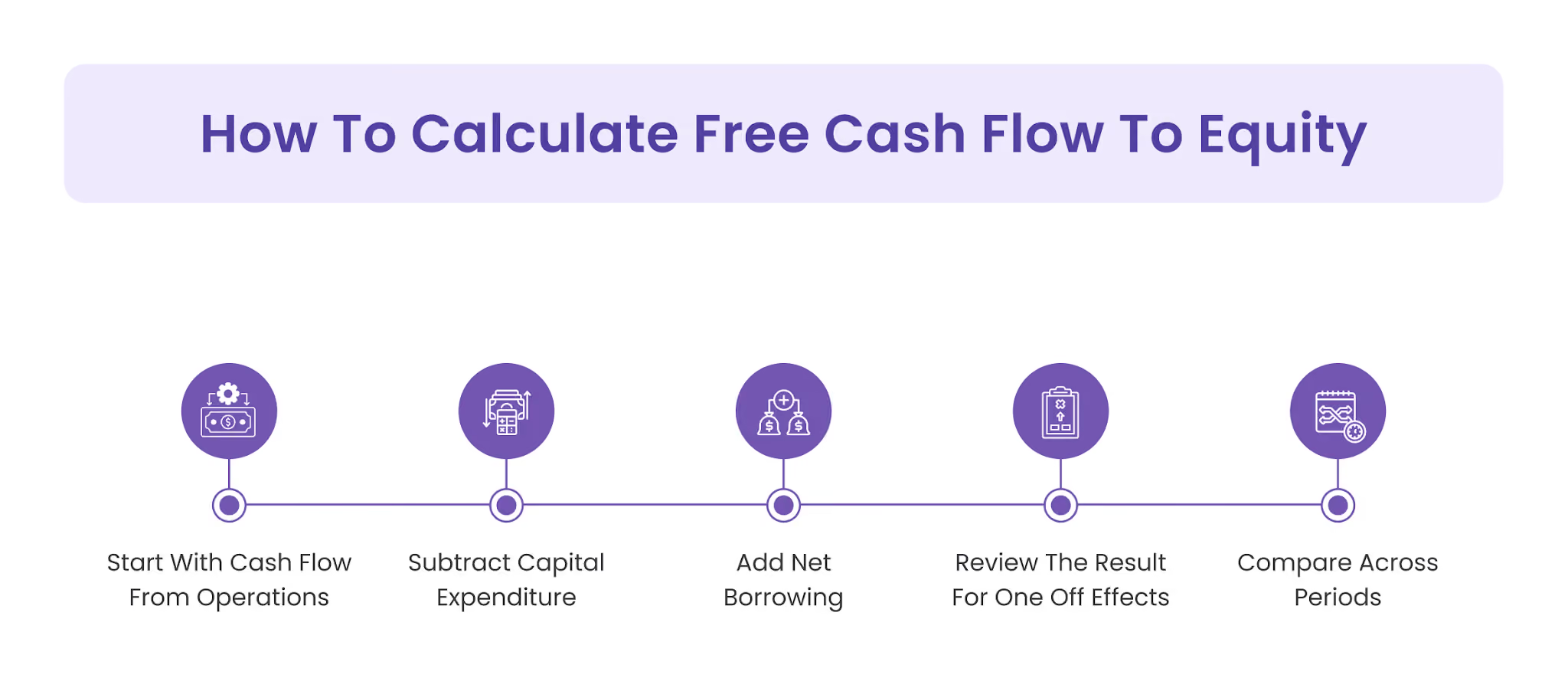

How To Calculate Free Cash Flow To Equity

The calculation becomes clearer when broken into steps. Finance teams typically follow a structured approach.

1. Start With Cash Flow From Operations

Use the operating cash flow figure from the cash flow statement. This already reflects changes in working capital.

2. Subtract Capital Expenditure

Remove cash used to invest in long-term assets. This step accounts for reinvestment needed to sustain or grow operations.

3. Add Net Borrowing

Include new debt raised and subtract debt repayments. This step adjusts for financing activity that affects cash available to equity holders.

4. Review The Result For One Off Effects

Large capex, unusual borrowing, or temporary working capital changes can distort FCFE in a single period.

5. Compare Across Periods

A single FCFE figure is less useful than a trend. Finance teams should review FCFE over multiple periods to understand stability and sustainability.

Related: Efficient Financial Statement Preparation Guide

FCFE Example With AED Values

A simple example helps illustrate how the formula works in practice.

- Cash Flow From Operations: AED 2,400,000

- Capital Expenditure: AED 700,000

- New Debt Raised: AED 500,000

- Debt Repaid: AED 300,000

- Net Borrowing: AED 200,000

Applying the formula:

FCFE = 2{,}400{,}000 - 700{,}000 + 200{,}000

FCFE = AED 1,900,000

This means the business generated AED 1.9 million in cash that is theoretically available to equity holders after operating needs, reinvestment, and debt movement.

This does not mean the company will distribute this amount. It simply represents the capacity to do so.

FCFE From Net Income

When cash flow statement data is not readily available, FCFE can be calculated starting from net income.

FCFE = Net\ Income + Depreciation - Capex - \Delta Working\ Capital + Net\ Borrowing

Each adjustment plays a specific role:

- Depreciation is added back because it is a non-cash expense

- Capex is subtracted because it represents actual cash outflow

- Working capital increases are subtracted because they tie up cash

- Net borrowing is added because it increases available cash

This approach is common in valuation models and FP&A analysis where detailed financial statements are used.

FCFE Vs FCFF

Free cash flow to equity is often compared with free cash flow to the firm (FCFF). The distinction is important because both metrics are used in valuation, but they answer different questions.

FCFE focuses only on equity holders, while FCFF represents cash available to all capital providers, including both debt and equity.

The relationship between the two is:

FCFE = FCFF - Interest(1 - Tax\ Rate) + Net\ Borrowing

This shows how debt-related cash flows move the analysis from a firm-level perspective to an equity-level perspective.

For finance teams, the choice between FCFE and FCFF depends on whether the goal is to value the entire business or only the equity portion.

Also Read: Understanding Financial Statements Beginners Guide

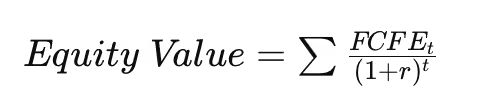

How FCFE Is Used In Equity Valuation

FCFE is widely used in equity valuation models because it directly measures cash available to shareholders. In practice, CFA Institute data shows that nearly 78.8% of analysts use discounted cash flow methods, and among those, the majority rely on free cash flow models for valuation.

The idea is straightforward: estimate how much cash a business can generate for shareholders in the future, and then adjust that value to what it is worth today.

In practice, this means projecting future free cash flow to equity (FCFE) and discounting it using the required return on equity.

Here:

- FCFE represents the cash available to shareholders in each future period

- r is the return investors expect for taking that risk

For more stable businesses, this can be simplified using a constant growth assumption:

Where:

- FCFE₁ is the expected cash flow for the next period

- g is the expected long-term growth rate

This approach is particularly useful when:

- The dividend policy does not reflect the actual cash capacity

- The business retains earnings rather than distributing them

- Equity investors want to understand intrinsic value

However, the accuracy of this method depends heavily on assumptions around growth, reinvestment, and cost of equity.

What Positive And Negative FCFE Mean

FCFE is often interpreted incorrectly because it is treated as a simple “good or bad” metric. In reality, the meaning depends on context.

Positive FCFE

Positive FCFE indicates that the business has cash available after covering operations, reinvestment, and financing needs.

This may allow the company to:

- Pay dividends

- Repurchase shares

- Reduce debt

- Build cash reserves

- Invest in new opportunities

However, positive FCFE does not guarantee distributions. Management may choose to retain cash.

Negative FCFE

Negative FCFE means that the business is using more cash than it generates for equity holders.

This can happen due to:

- Heavy capital expenditure for growth

- Significant working capital investment

- Debt repayment exceeding new borrowing

- Operating losses

Negative FCFE is not always a concern. In high-growth businesses, it may reflect investment rather than weakness. The key is to understand whether the negative cash flow is strategic or unsustainable.

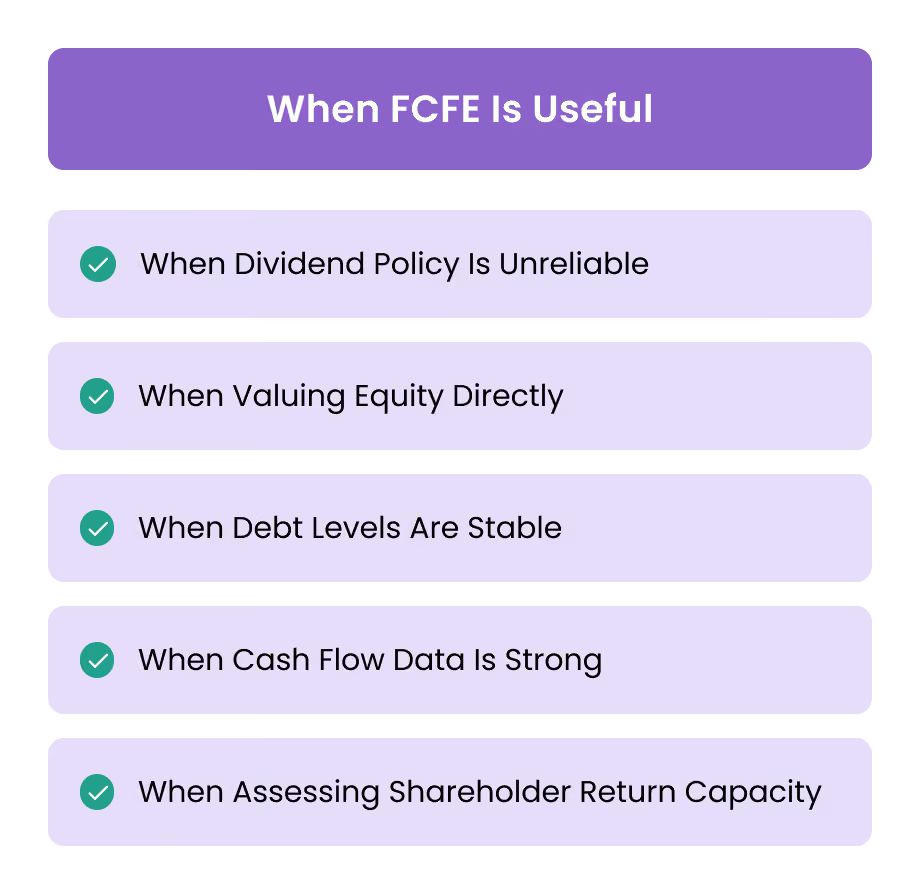

When FCFE Is Useful

FCFE is most useful in situations where shareholder cash flow and equity valuation are the primary focus.

1. When Dividend Policy Is Unreliable

If a company does not pay dividends or pays inconsistent dividends, FCFE provides a better measure of cash available to shareholders.

2. When Valuing Equity Directly

FCFE allows analysts to estimate equity value without first calculating enterprise value.

3. When Debt Levels Are Stable

Stable borrowing patterns make FCFE easier to interpret because debt-related distortions are limited.

4. When Cash Flow Data Is Strong

Reliable operating cash flow, capex, and financing data improve the accuracy of FCFE calculations.

5. When Assessing Shareholder Return Capacity

FCFE helps evaluate whether the business can sustain dividends or buybacks over time.

When FCFE Can Be Misleading

Despite its usefulness, FCFE can produce misleading signals if interpreted without context.

1. Debt Issuance Inflates FCFE

New borrowing increases FCFE, even if operating performance has not improved.

2. High Capex Suppresses FCFE

Growth investments can reduce FCFE in the short term, even when the business is expanding successfully.

3. Working Capital Changes Distort Results

Large changes in receivables, inventory, or payables can significantly impact FCFE in a single period.

4. Changing Capital Structure Adds Volatility

Frequent changes in debt levels make FCFE less stable and harder to interpret.

5. Single Period Analysis Leads To Errors

A single year’s FCFE may not reflect long-term trends or sustainable performance.

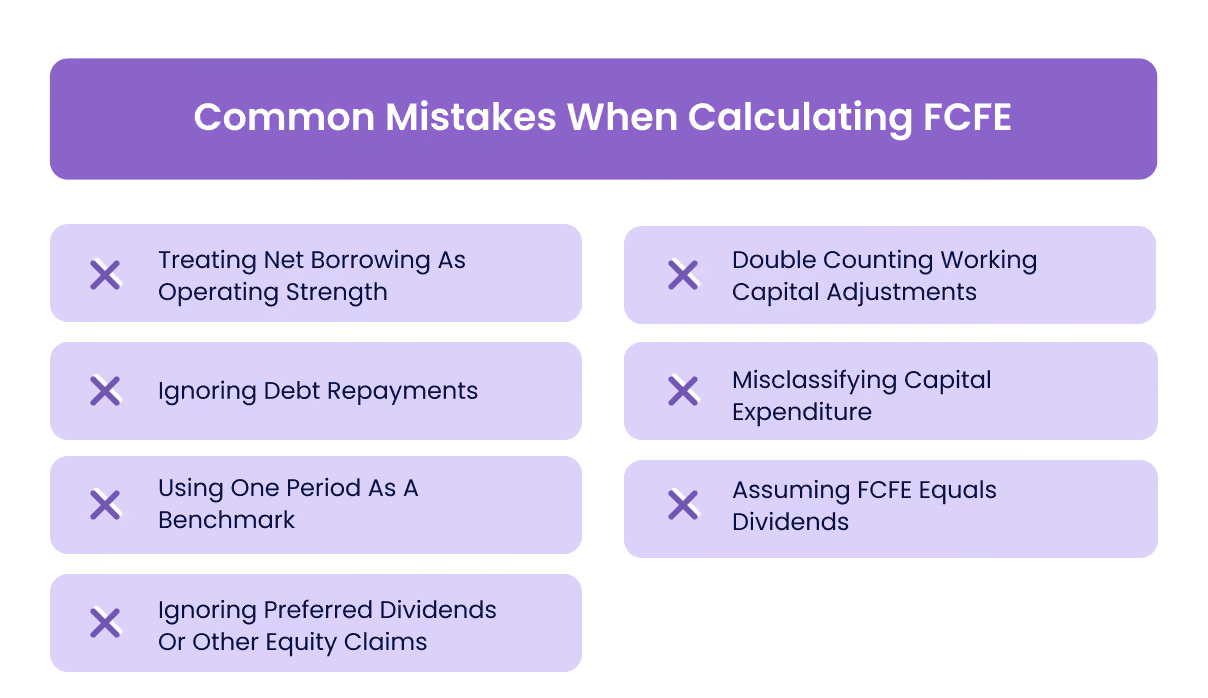

Common Mistakes When Calculating FCFE

Even when the formula is applied correctly, FCFE can still be misinterpreted due to errors in inputs or classification. These mistakes are often subtle but can materially affect valuation and analysis.

1. Treating Net Borrowing As Operating Strength

Net borrowing increases FCFE, but it does not reflect core business performance. A company may show strong FCFE simply because it raised new debt, not because operations improved.

2. Double Counting Working Capital Adjustments

When using the cash flow from operations method, working capital changes are already included. Adjusting them again separately leads to incorrect results.

3. Ignoring Debt Repayments

Some calculations include new debt but forget to subtract repayments. This overstates net borrowing and inflates FCFE.

4. Misclassifying Capital Expenditure

Confusing capital expenditure with operating expenses can distort the calculation. Capex must be treated separately because it represents reinvestment, not ongoing operating cost.

5. Using One Period As A Benchmark

FCFE can fluctuate due to timing of capex, borrowing, or working capital changes. Relying on a single period can lead to incorrect conclusions.

6. Assuming FCFE Equals Dividends

FCFE shows capacity, not actual payout. Companies may retain cash for growth, debt reduction, or liquidity purposes.

7. Ignoring Preferred Dividends Or Other Equity Claims

Where applicable, FCFE should reflect cash available to common equity holders after other equity-related obligations.

How Alaan Helps Improve The Inputs Behind Cash Flow Analysis

Free cash flow to equity is only as reliable as the underlying financial data. If expense records are incomplete, capex is misclassified, or cash flow entries are delayed, the resulting FCFE figure becomes harder to trust.

Alaan does not calculate FCFE or perform valuation. Instead, it strengthens the operational data layer that feeds into financial analysis, helping finance teams work with cleaner and more reliable inputs.

Corporate Cards With Structured Spend Controls

Alaan allows businesses to issue corporate cards with predefined limits, merchant restrictions, and usage controls. This ensures that day-to-day operating expenses are captured consistently rather than spread across unmanaged payment methods.

When operating expenses are tracked in a structured way, finance teams can more accurately separate operating cash flow from other types of spending, which directly supports FCFE calculations.

Real Time Visibility Into Operating Expenses

Finance teams can monitor spending across departments, categories, and vendors as it happens. Instead of waiting for month-end reports, they can see how cash is being used during the period.

This improves the reliability of cash flow from operations, which is a key input in FCFE. It also helps identify unusual expense patterns that may affect cash flow trends.

Centralised Receipt And Invoice Capture

Every transaction can be supported by linked receipts and invoices, reducing gaps in documentation. This makes it easier to validate whether expenses are operating in nature or should be classified differently.

Clear documentation also helps distinguish between operating expenses and capital expenditure, which is critical for accurate FCFE calculation.

Approval Workflows Before Spend Occurs

Alaan enables structured approval flows before expenses are incurred. This adds discipline to how money leaves the business and improves predictability.

For finance teams, this reduces unexpected cash outflows and makes forecasting more accurate, which supports better interpretation of FCFE over time.

Cleaner Reconciliation And Accounting Sync

With integrations into systems like Xero, QuickBooks, NetSuite, and Microsoft Dynamics, expense data flows into accounting systems in a structured way.

This reduces reconciliation gaps and ensures that financial statements reflect actual transactions, improving the accuracy of both cash flow statements and FCFE inputs.

Better Visibility For Financial Planning And Analysis

Because expense data is categorised and accessible in real time, finance teams can build more reliable forecasts and models.

This supports deeper analysis of how operating cash flow, reinvestment, and financing decisions affect shareholder cash flow over time.

Alaan’s role is not to replace financial modelling, but to ensure that the underlying data used in that modelling is consistent, complete, and easier to interpret.

Also Read: Cash Flow Forecasting

Conclusion

Free cash flow to equity provides a focused view of how much cash a business generates for its shareholders after accounting for operations, reinvestment, and financing.

It is a powerful metric for valuation and analysis, but it requires careful interpretation. Debt movements, capital expenditure, and working capital changes can all affect the result in ways that are not immediately obvious.

For finance teams, the goal is not just to calculate FCFE, but to understand what is driving it. Consistent classification, accurate cash flow data, and disciplined financial processes are essential for making the metric meaningful.

If you want to strengthen how your business tracks expenses and builds reliable financial data, you can explore how Alaan helps finance teams improve visibility, maintain control, and support better cash flow analysis. Book a demo to see how structured expense management contributes to more accurate financial insights.

Frequently Asked Questions

1. Why Can FCFE Be Positive Even When Net Income Is Low

FCFE may be positive due to non-cash expenses being added back, lower capital expenditure, or net borrowing, even if accounting profit is relatively low.

2. Why Do Growing Companies Often Have Negative FCFE

High-growth businesses may invest heavily in assets and working capital, which reduces cash available to equity holders in the short term.

3. Should FCFE Always Be Distributed As Dividends

No, FCFE represents available cash, not actual payout. Companies may retain cash for growth, debt reduction, or liquidity management.

4. Is FCFE Better Than FCFF For Valuation

It depends on the objective. FCFE is used for equity valuation, while FCFF is used to value the entire business before considering capital structure.

5. How Does New Debt Affect FCFE

New borrowing increases FCFE because it adds cash available to equity holders, while debt repayment reduces FCFE.

6. Can FCFE Be Used For Private Company Analysis

Yes, FCFE can be applied to private companies, provided reliable financial data is available for operating cash flow, capex, and debt movement.