Inventory is one of the most operationally “real” items in financial statements because it represents capital that has not yet become cash. In many industrial organisations, inventory can account for up to 40% of capital and as much as 33% of total assets, illustrating how materially it shapes liquidity and working-capital positioning.

Holding inventory also carries an economic cost. Businesses typically incur annual carrying costs equal to roughly 15–30% of inventory value, reflecting financing, storage, risk, and obsolescence exposure that directly influence profitability.

Because of this dual operational and financial impact, inventory accounting is not merely a technical classification. It determines how capital is represented, how margins are measured, and how control risks surface in reporting. This guide explains what inventory means in accounting terms, how it is valued, and how finance teams maintain accuracy across recognition, measurement, and journal treatment.

TL;DR

- Inventory is a financial bridge between operations and profitability. It simultaneously locks working capital, shapes fulfilment capability, and determines gross margin through the timing of cost recognition into COGS.

- Accounting treatment hinges on timing and classification, not physical movement. Inventory remains a current asset until sale, and misalignment between physical flow and ledger recognition is a primary source of reporting distortion.

- Valuation discipline is the credibility anchor. Consistent cost formulas, adherence to lower-of-cost-and-NRV measurement, and policy stability under IAS 2 are what prevent artificial margin volatility and asset misstatement.

- Control failures tend to be procedural, not technical. Weak cut-off controls, poor count reconciliation, delayed write-downs, and inconsistent costing methods account for the majority of inventory accounting issues.

- Upstream spend governance strengthens downstream accounting integrity. Structuring purchasing documentation, approvals, and audit trails through platforms like Alaan improves the reliability of inventory cost inputs before they enter financial reporting workflows.

What Is Inventory In Accounting

In accounting, inventory refers to goods a business holds for sale or uses to produce goods for sale. That typically includes raw materials, work-in-progress, and finished goods.

Inventory matters because it bridges two parts of the business that rarely move at the same speed: purchasing/production and sales. Holding the right level of inventory helps meet demand without tying up excessive capital or increasing obsolescence risk.

From a reporting perspective, inventory is carried on the balance sheet until it is sold. When it is sold, its cost moves out of inventory and is recognised on the income statement as cost of goods sold (COGS), which is what makes inventory accounting so influential on gross profit.

Also Read: Understanding Financial Statements for Beginners Guide

What Type Of Account Is Inventory

Inventory is generally a current asset on the balance sheet. It is classified as current because it is expected to be sold or used within the normal operating cycle of the business (which may vary by industry).

A common confusion is treating inventory as an “expense account.” Inventory itself is not an expense while it is held. It becomes an expense only when the related goods are sold, and the cost is recognised as COGS. This is why inventory errors often show up as margin problems, not just balance sheet problems.

In practical finance workflows, this means two controls matter disproportionately:

- Valuation discipline (what costs are included and how they are assigned)

- Count-to-book accuracy (how well physical inventory reconciles to records)

Both determine whether the asset on the balance sheet and the expense in COGS are credible.

Inventory Types Businesses Track

Most businesses track inventory in three core categories. These terms matter because they change how value accumulates and how costs are assigned.

- Raw Materials

Inputs purchased to manufacture products (or to assemble deliverables) but not yet used in production. - Work In Process

Goods that are partway through production. Costs here typically include a combination of raw materials, direct labour, and an allocation of production overhead, depending on your costing approach and policy. - Finished Goods

Products completed and ready for sale. Once sold, the related costs move out of inventory and into COGS.

Some businesses also track items like packaging, spare parts, or consumables. Whether those are treated as inventory, supplies, or another asset category depends on how they are used and on accounting policy consistency.

Also Read: Types of Expenses Every Business Should Know

Inventory Accounting Basics

Inventory accounting is the set of rules and processes that ensure inventory is recorded correctly from purchase or production through to sale. The core relationship is simple: inventory sits on the balance sheet until the goods are sold, and then its cost is recognised as COGS.

Perpetual Versus Periodic Systems

Businesses usually use one of two systems.

- Perpetual Inventory System

Inventory is updated continuously as purchases, production, and sales occur. This relies on strong transaction discipline and often integrates with POS, ERP, or inventory tools. - Periodic Inventory System

Inventory is updated at set intervals, typically based on physical counts. COGS is then derived using an accounting calculation at period end. This approach can work in smaller environments, but it increases the importance of accurate counts and cut-off discipline.

In practice, the more volume you have and the more dispersed your stock is, the more fragile periodic accounting becomes without strong controls.

Why Inventory Errors Hit Gross Margin

Because COGS is tied to inventory, misstatements often show up as margin swings. If ending inventory is overstated, COGS is understated and gross profit is inflated; if ending inventory is understated, the opposite happens. This is why inventory is a high-focus area during audits and internal reviews.

Also Read: Guide to Preparing Financial Statements Efficiently

Inventory Valuation And Costing Methods

Inventory valuation determines the amount recorded as an asset and the cost recognised in COGS. Under IFRS, the main standard governing inventory is IAS 2 Inventories.

Measurement Rule Under IFRS

IAS 2 requires inventory to be measured at the lower of cost and net realisable value (NRV).

- Cost generally includes purchase costs and conversion costs (and other costs incurred to bring inventory to its present location and condition, as defined in the standard).

- NRV is the estimated selling price in the ordinary course of business, less estimated costs of completion and the estimated costs necessary to make the sale.

If NRV falls below cost (for example, due to damage, obsolescence, or price decline), inventory is written down, and that write-down affects profit.

Cost Formulas Commonly Used

For items that are interchangeable, IAS 2 permits cost assignment using methods such as:

- FIFO (First In, First Out)

- Weighted Average Cost

- Specific Identification (typically for non-interchangeable items or high-value unique stock)

A key point for IFRS environments: LIFO is not permitted under IAS 2.

Also Read: Chart of Accounts: A Practical Guide for UAE Businesses

Common Inventory Journal Entries

Inventory accounting becomes easier to control when the journal logic is clear. The same economic events show up repeatedly: you acquire inventory, you sell goods, you recognise COGS, and sometimes you adjust inventory values.

Below are common entries shown at a high level. Exact accounts and sequencing vary by system (perpetual vs periodic) and by whether your revenue recognition and inventory tracking tools post automatically.

1. Purchase Of Inventory

When inventory is purchased on credit:

- Dr Inventory

- Cr Accounts Payable

When inventory is purchased with cash:

- Dr Inventory

- Cr Cash / Bank

This reflects inventory as an asset until it is sold.

2. Sale Of Inventory

A sale typically creates two accounting impacts:

- Revenue recognition

- Dr Cash / Accounts Receivable

- Cr Sales Revenue

- Recognition of cost (COGS)

- Dr Cost Of Goods Sold

- Cr Inventory

The second entry is what moves cost from the balance sheet into the income statement.

3. Inventory Write-Down To NRV

Under IFRS, inventory is measured at the lower of cost and NRV. If NRV falls below cost, an adjustment is required.

At a high level, this is often recorded as:

- Dr Inventory Write-Down Expense (or similar expense account)

- Cr Inventory (or a valuation allowance, depending on policy)

The accounting form can differ, but the principle is consistent: the carrying value is reduced when recovery through sale is not expected.

Also Read: Understanding General Ledger in Double-Entry Accounting

Inventory Metrics Finance Teams Actually Use

Inventory metrics matter because they reveal whether inventory is acting as a productive asset or a cash drag. Finance teams typically focus on a small set of indicators rather than dozens of operational measures.

1. Inventory Turnover

Inventory turnover reflects how many times inventory is sold and replaced over a period. Higher turnover generally indicates faster movement; lower turnover can signal overstocking, weak demand, or slow-moving items.

This metric is commonly analysed alongside gross margin, because high turnover with poor margin can still be unhealthy, and strong margin with stagnant turnover often hides cash inefficiency.

2. Days Sales Of Inventory (DSI)

DSI estimates how long inventory sits before it is sold. It is often used to monitor working capital efficiency, especially when inventory is a major balance sheet component.

3. Shrinkage Rate

Shrinkage is the gap between recorded inventory and actual inventory, often driven by loss, theft, damage, or process error. Even moderate shrinkage becomes material when volume is high because it affects both asset value and COGS accuracy.

Also Read: Cash Flow from Operating Activities Explained

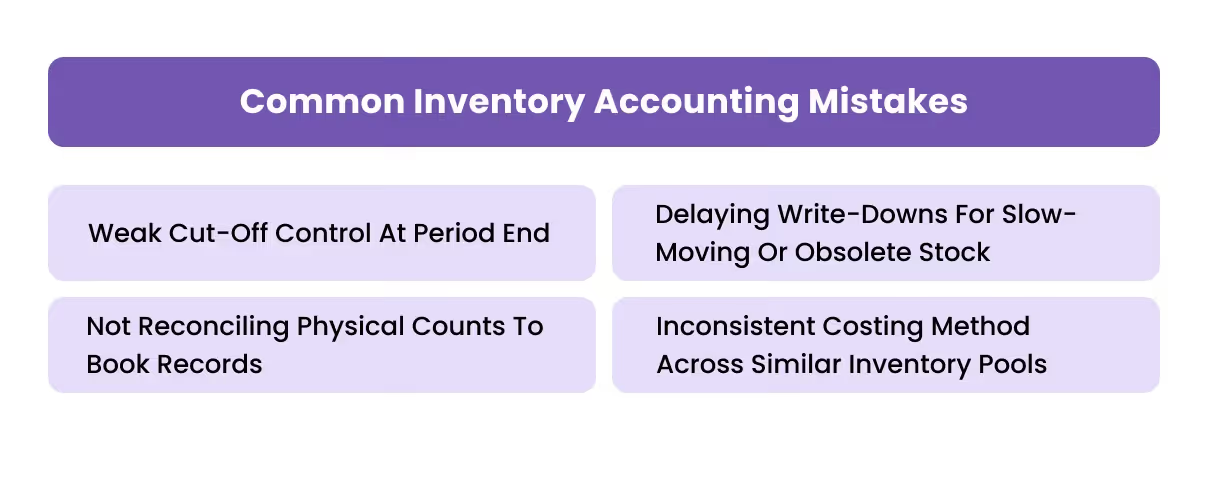

Common Inventory Accounting Mistakes

Most inventory accounting problems are predictable. They typically come from weak operational discipline rather than complex standards.

1. Weak Cut-Off Control At Period End

If purchases, returns, or sales are recorded in the wrong period, inventory and COGS distortions follow. This is one of the fastest ways to create unexplained margin variance during close.

2. Not Reconciling Physical Counts To Book Records

Even with a perpetual system, physical verification matters. Differences between book inventory and physical inventory must be investigated and resolved to maintain reporting credibility.

3. Delaying Write-Downs For Slow-Moving Or Obsolete Stock

Under IFRS IAS 2, inventory should not remain carried above its recoverable value, which is why the lower of cost and NRV rule exists. Delaying recognition of write-downs often creates sudden margin shocks later.

4. Inconsistent Costing Method Across Similar Inventory Pools

IAS 2 requires consistent use of cost formulas for inventories of a similar nature and use to the entity. Changing methods or mixing approaches without a clear policy creates comparability and control issues.

Also Read: How to Prepare a Bank Reconciliation Statement: A Complete Guide

How Alaan Supports Governance Around Inventory-Related Spend

Inventory accounting outcomes are shaped long before valuation or journal treatment begins. Cost accuracy depends on how purchasing activity is documented, approved, and recorded upstream. Fragmented procurement records or missing invoice trails often create downstream reconciliation work, margin distortions, and audit exposure.

Alaan does not manage stock levels or warehouse processes. Instead, we support governance around the financial inputs feeding inventory valuation by structuring spend capture, approval discipline, and accounting continuity.

- Corporate Cards And Procurement Spend Visibility

We provide corporate cards that allow procurement teams to execute inventory-related purchases while capturing transaction data instantly within a centralised environment. Finance leaders gain real-time visibility into supplier spend patterns and purchasing concentration, supporting oversight before costs enter inventory valuation workflows. - Invoice Capture And Approval Workflows

Invoices and supporting documents can be collected digitally and routed through configurable approval chains. This ensures purchasing intent is reviewed before payment execution and maintains a clear audit trail for costs that may later be capitalised into inventory. Structured documentation reduces ambiguity during classification, valuation, and audit review. - Accounting Integration For Cost Continuity

Transaction data and associated documentation synchronise with accounting integrations, keeping procurement records connected to financial postings. This reduces manual duplication, supports consistent cost coding, and improves reconciliation discipline when inventory balances and COGS are reviewed during close cycles. - Spend Analytics For Supplier And Cost Oversight

Categorisation and analytics provide visibility into vendor trends, cost behaviour, and purchasing frequency. These insights help finance teams monitor procurement discipline, identify inefficiencies, and maintain control over cost structures feeding inventory accounts as operational scale increases.

By strengthening visibility, approval structure, and documentation continuity around purchasing activity, we help organisations maintain cleaner cost inputs and reduce friction in downstream inventory accounting processes. This supports more reliable valuation outcomes and stronger financial reporting discipline without altering existing inventory or ERP systems.

Also Read: Accounts Payable Automation and Invoice Management Software

Conclusion

Inventory is a balance sheet asset, but it behaves like an operational system. It ties up cash, affects service delivery, and directly shapes gross margin through COGS. That is why inventory accounting matters: errors distort both financial reporting and management decisions.

The core controls are consistent across industries. Track inventory types correctly, use a defensible valuation method, reconcile physical counts to records, and apply write-down discipline when NRV falls below cost under IFRS.

At Alaan, we help finance teams govern inventory-related spend with stronger visibility, approvals, and documentation so the upstream cost pipeline stays controlled and reconciliation stays clean. Book a Demo Today!

FAQs

1. Does inventory accounting differ between service and product businesses?

Yes. Pure service businesses typically have little or no inventory, while hybrid models may track consumables or work inputs differently depending on accounting policy and materiality.

2. How often should physical inventory counts be performed?

Frequency depends on scale and risk profile. Many organisations use annual full counts supplemented by cycle counts to maintain accuracy throughout the year.

3. Can automation tools replace inventory controls?

Automation improves record accuracy but does not replace governance. Physical verification, approval discipline, and valuation review remain essential control components.

4. How does inflation affect inventory valuation?

Cost formulas like FIFO or weighted average react differently to price changes, influencing reported margins and asset values during inflationary periods.

5. Are inventory write-downs reversible?

Under IFRS, write-downs can be reversed if circumstances improve, but only up to the amount previously written down.

6. When should inventory be expensed immediately?

Items not intended for resale or production may be classified as supplies or expenses depending on use, materiality, and accounting policy.