For most businesses, month-end is the point where finance has to answer a simple but high-stakes question: are the numbers complete, accurate, and reliable enough to report? If the answer is no, management decisions start getting built on partial information. If the answer is yes, the business gets a clearer view of performance, cash movement, margins, and financial position.

That is why the month-end closing process in accounting matters far beyond bookkeeping. It is the process that turns a month of transactions, expenses, invoices, accruals, reconciliations, and adjustments into usable management reporting. Period close guidance from enterprise finance systems reflects the same logic: closing the month is tied to reconciliation, ledger review, consolidation, reporting, and forecast updates rather than just posting final entries.

In this article, we explain how the month-end closing process in accounting works, what a practical close checklist should include, which entries need closer review, what reports management should receive, and where better spend control helps reduce friction before close begins.

TL;DR / Key Takeaways

- The month-end closing process confirms that the period is complete enough, accurate enough, and reviewed enough for reporting.

- A reliable close depends on reconciliations, cut-off checks, accruals, review controls, and clean supporting documents.

- The close should end with useful management reporting, not just technically closed ledgers.

- Most close delays begin upstream in missing invoices, late expenses, weak approvals, and fragmented records.

- Faster close depends on stronger process discipline during the month, not only more effort at month end.

- Alaan helps finance teams reduce close friction through earlier spend visibility, receipt capture, approval workflows, and cleaner reconciliation support.

Related: Modern Expense Management Guide

What Is The Month End Close Process

The month-end close process is the structured review that finance teams perform at the end of each month to confirm that the books are ready for reporting. It usually includes recording any remaining transactions, checking the cut-off, posting adjustments, reconciling balances, reviewing exceptions, and preparing internal reports.

In practice, the month-end close is less about “finishing accounting” and more about proving that the numbers can be trusted. That is why close frameworks across larger finance systems link the process to subledger review, reconciliation, ledger accuracy, and reporting readiness rather than treating it as a single closing task.

- Why Businesses Perform a Month-End Close

Businesses close the month so that management can work from a consistent financial view rather than a moving set of incomplete records. Without that process, profit, cash position, liabilities, and spending trends are harder to interpret properly. - What Happens Before The Books Are Closed

Finance teams typically review pending invoices, expenses, payroll activity, bank movement, accruals, prepayments, and account balances before they finalise the period. The close only works well when those inputs are complete enough to support accurate reporting. - Why Management Depends On A Reliable Close

Month end reporting often informs decisions on costs, budgets, hiring, payment timing, collections, and forecasting. If the close is delayed or weak, management may still receive reports, but not necessarily reports they should rely on.

Also Read: Understanding Financial Statements Beginners Guide

Why The Month End Closing Process Matters

A reliable month end close gives finance teams something more useful than technical completion. It gives them a stable reporting base. Once balances are reviewed and key exceptions are addressed, the business has a clearer foundation for management reporting, variance analysis, cash monitoring, and internal control.

It also improves finance operations more broadly. Reconciliation-focused close guidance consistently treats faster reporting as dependent on cleaner balances and fewer unresolved differences, which is why the quality of the close matters as much as the speed of the close.

- Financial Accuracy

Month end close reduces the risk of reporting income, expenses, assets, or liabilities in the wrong period. That matters because even small timing issues can distort how the month looks to management. - Management Reporting

A close is useful only if it supports decisions. Finance teams need to move from raw transactions to reporting that helps management understand what changed, why it changed, and what requires attention. - Cash Visibility

When bank balances, payables, receivables, card spend, and accruals are not reconciled properly, cash reporting becomes less reliable. A good close improves the quality of that visibility. - Internal Control And Audit Readiness

A disciplined monthly close creates a cleaner trail of support, review, and correction. That makes later audit work easier and reduces the amount of rework required when questions arise. - Faster Variance Analysis

Teams can analyse movements more confidently when the close process has already addressed obvious errors, unreconciled balances, and missing adjustments.

Related: Account Reconciliation Importance Steps

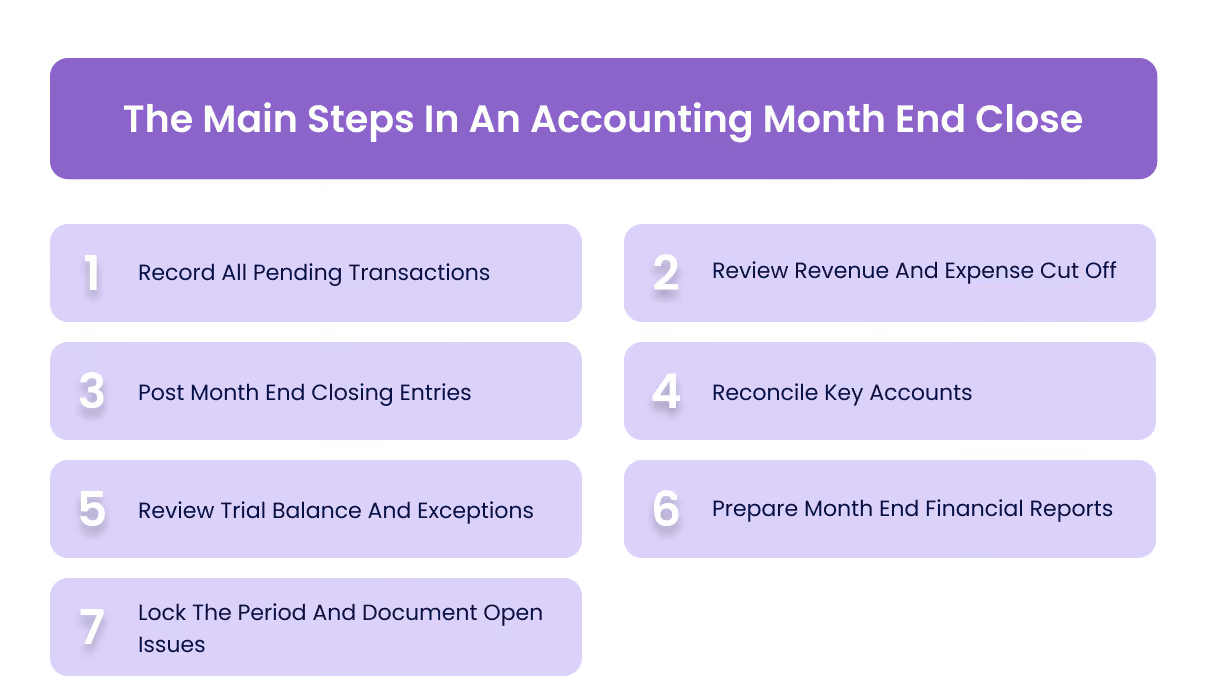

The Main Steps In An Accounting Month End Close

A strong accounting month end close works best when the sequence is clear. The exact process differs by business size and system complexity, but the core logic stays fairly consistent: record what is missing, adjust what needs correction, reconcile what matters, review the output, and prepare reports.

1. Record All Pending Transactions

Before the month can be closed properly, finance needs a complete enough record of activity for the period. That includes supplier invoices, employee expenses, payroll items, bank transactions, internal charges, and any other financial activity that belongs in the month but has not yet been posted.

If this stage is weak, the rest of the close becomes less reliable. Finance may still be able to produce reports, but those reports will contain gaps that later need correction.

2. Review Revenue And Expense Cut Off

Cut off review is what keeps income and costs in the correct month. Revenue recognised too early or expenses recorded too late can make results look stronger or weaker than they really are, which is why this step matters even in smaller businesses.

A proper cut off review usually focuses on timing around invoices, service periods, deliveries, prepaid costs, accrued expenses, and unearned income where relevant.

3. Post Month End Closing Entries

Month end closing entries are the adjustments needed to reflect the month accurately after routine transaction posting is done. These usually include accruals, prepayments, depreciation, amortisation, provisions, payroll adjustments, and reclassifications where required.

This is one of the most important parts of month end accounting because it is where the books move from transactional completeness to reporting accuracy.

4. Reconcile Key Accounts

Reconciliation is often where the real close quality shows up. Finance teams typically review bank accounts, card balances, receivables, payables, payroll balances, petty cash, tax balances, and other control accounts that should not be left unreconciled at month end.

Close and reconciliation guidance across the current ranking set makes the same point: faster reporting depends heavily on reducing unresolved differences and improving the quality of matching and review.

5. Review Trial Balance And Exceptions

Once entries and reconciliations are complete, finance should review the trial balance for unusual movements, unexpected balances, duplicate postings, unsupported entries, or accounts that do not make sense in context.

This step helps catch issues before reports are circulated. It is often faster to resolve a problem here than to explain it later once management has already seen the numbers.

6. Prepare Month End Financial Reports

The close should end with usable month end financial reports, not just technically closed ledgers. At a minimum, management usually needs a clear view of profit and loss, balance sheet position, major variances, and cash-related movements.

This is the point at which the month end close becomes decision-useful. The reporting pack should help management understand performance, not simply prove that accounting work has been completed.

7. Lock The Period And Document Open Issues

Once the numbers have been reviewed, the period should be closed operationally so late changes do not quietly alter the reporting base. At the same time, any open issues that could not be resolved before close should be documented clearly for follow-up.

That creates discipline for both reporting and subsequent correction. It also helps finance separate what was finalised this month from what still needs attention in the next cycle.

Also Read: Understanding Recording Business Expenses Efficiency Strategies

Month End Closing Entries To Review Carefully

Not every journal entry carries the same weight at month end. Some entries matter more because they directly affect whether profit, liabilities, and the overall financial position are being reported in the right period. That is why finance teams usually review a smaller group of month end closing entries more carefully than routine daily postings.

The goal here is not to overcomplicate the close. It is to make sure the entries that shape reporting quality are supported, reviewed, and posted consistently before management sees the final numbers.

- Accruals

These entries recognise costs or income that belong to the month even if the invoice or cash movement has not yet appeared. They are essential for keeping month end accounting aligned with actual business activity. - Prepayments

Prepaid costs need to be split properly so only the relevant portion hits the current month. Without that adjustment, expenses can be overstated in one month and understated in another. - Depreciation And Amortisation

These entries allocate asset cost over time and help reflect the true period cost of using long-term assets or intangibles. Even when automated, they should still be reviewed for completeness and logic. - Payroll Adjustments

Payroll often creates timing issues around salaries, benefits, leave accruals, or related liabilities. These balances should be reviewed carefully because payroll errors can affect both expense reporting and liabilities. - Expense Reclassifications

Some costs are posted to the wrong account during the month and need to be reclassified before reporting is finalised. These adjustments matter because management decisions often depend on category-level cost visibility. - Provisions And Other Adjustments

Depending on the business, finance may also need to review provisions, bad debt adjustments, deferred items, or other month-specific entries that affect how results are presented.

Related: Deferred Meaning Accounting Revenue Expenses

A Practical Month End Close Checklist

A month-end close checklist helps finance teams reduce delays, avoid missed steps, and keep responsibilities clearer across the close calendar. It is not there to make the process longer. It is there to make the process more consistent.

In many businesses, close quality improves simply because the checklist makes it harder for routine gaps to slip through. That is especially useful where the close still depends on multiple teams, manual handoffs, or incomplete supporting documents.

- All Month Transactions Recorded

- Supplier Invoices Reviewed And Posted

- Employee Expenses Submitted And Checked

- Bank Accounts Reconciled

- Corporate Card Activity Matched

- Accounts Payable Reviewed

- Accounts Receivable Reviewed

- Payroll Posted And Checked

- VAT And Tax Balances Reviewed

- Accruals And Prepayments Posted

- Key Balance Sheet Accounts Reconciled

- Trial Balance Reviewed For Exceptions

- Month-End Financial Reports Prepared

- Period Closed Or Locked

- Open Issues Logged For Follow Up

A checklist like this becomes even more useful when it is linked to owners and deadlines rather than treated as a passive list. That is usually where finance teams move from a recurring scramble to a more controlled close process.

Also Read: Expense Report Filling Guide

What Month-End Financial Reports Should Management Receive

Closing the books is not the end goal. The end goal is to give management a set of month-end financial reports that are clear enough to support action. A business can complete its accounting month-end close and still fail to deliver reporting that helps decision-makers understand what actually changed.

That is why the reporting pack matters. It should move beyond raw accounting completion and show management where profit moved, where cash stands, and which issues still need attention.

- Profit And Loss Statement

This gives management a view of revenue, direct costs, operating expenses, and overall profitability for the month. - Balance Sheet

This shows the financial position at month's end, including assets, liabilities, and equity balances that need to be understood alongside the P&L. - Cash Position Or Cash Flow View

Many management teams need a direct view of available cash, major inflows, and near-term pressure points rather than waiting for a formal annual-style cash flow presentation. - Budget Versus Actual Summary

This helps explain whether the business performed in line with the plan and where the biggest deviations need review. - Aged Receivables And Payables

These reports matter because cash pressure often sits in collection delays or unpaid supplier obligations rather than only in the headline P&L. - Key Spend Variance Summary

This is where finance can help management understand which categories moved unexpectedly and whether the movement was operational, seasonal, one-off, or structural. - Commentary On Material Movements

Management usually needs more than numbers. They need a short explanation of what changed and why it matters. - Open Issues Affecting Accuracy Or Timing

If any balances are still under review or if certain items were estimated pending final support, that should be communicated clearly.

Related: Analyze Business Expense Analysis

Why Month-End Close Gets Delayed

Month-end close delays usually come from process friction, not from the existence of month-end work itself. The close becomes slower when finance spends too much time chasing documents, fixing records, waiting on approvals, or correcting issues that should have been resolved earlier in the month.

That pattern is consistent with close and reconciliation guidance more broadly. Faster reporting tends to depend on cleaner data, fewer unreconciled items, and better workflow discipline rather than on pushing the finance team to work harder during the final days of the month.

- Missing Supplier Invoices

If invoices arrive late or are not submitted on time, finance either delays the close or relies on estimates that later need revision. - Late Expense Submissions

Employee expenses submitted after the cut-off create avoidable delay, especially where receipts are missing or approvals are still pending. - Weak Receipt Capture

If supporting documents are scattered across email, chat, or paper records, finance spends more time chasing support than reviewing the numbers. - Manual Journal Bottlenecks

Repetitive entries handled manually can slow the close and increase the chance of posting errors or omissions. - Unreconciled Bank Or Card Activity

When bank or card transactions are not matched on time, finance loses confidence in the balances and spends longer investigating differences. - Delayed Approvals

A close process weakens quickly when approvals, invoice approvals, or payment reviews are still incomplete near the month-end. - Poor Ownership Across Teams

If responsibilities are unclear, finance ends up doing extra follow-up just to gather what should already have been ready. - Too Much Spreadsheet Dependency

Spreadsheets can work, but when the close relies on too many disconnected files and manual updates, review time usually expands.

Also Read: Automate Expense Management Approvals

How To Improve The Month End Closing Process

Improving the month-end closing process usually starts with discipline before it starts with software. The first gains often come from clearer timing, better ownership, and cleaner supporting data. Automation then becomes more effective because it is improving a defined process rather than compensating for a weak one.

At the same time, close improvement is not only about saving hours. It is about getting to reliable reporting faster, with fewer unresolved items and less manual rework. Finance-automation and reconciliation guidance tends to point in the same direction: stronger workflows and earlier visibility improve both speed and accuracy.

1. Set A Clear Close Calendar

A defined close calendar helps everyone understand what needs to be done, by when, and in which sequence. That reduces the amount of last-minute coordination finance teams usually face.

2. Assign Owners For Each Reconciliation

Each key account should have a clear owner. Without ownership, reconciliations tend to drift until finance has to chase them close to reporting time.

3. Standardise Supporting Documents

The easier it is to locate invoices, receipts, approvals, and supporting schedules, the easier it is to review the month without repeated follow-up.

4. Reduce Manual Journal Work Where Possible

Recurring entries, standard allocations, and routine adjustments should be simplified or automated where appropriate. That frees time for review rather than repetitive posting.

5. Capture Expenses Earlier In The Month

Expenses become easier to close when they are submitted, coded, and reviewed continuously instead of arriving in a batch near month end.

6. Review Exceptions Before Final Reporting

It is faster to escalate unusual balances, missing support, or large variances before the reporting pack is finalised than to explain them afterwards.

7. Automate Repetitive Parts Of The Close

Automation works best in tasks such as transaction capture, workflow routing, matching, and standard reporting support. It is most useful where the process is already clear and repeatable.

Related: ERP Integration Benefits Explained

How Alaan Helps Reduce Month End Close Friction

Month end usually slows down before finance starts posting final entries. The real delays often begin earlier, when expenses are submitted late, receipts are missing, approvals are still pending, and card transactions are harder to match than they should be. That is where Alaan is relevant. It helps finance teams manage spend through corporate cards, spend controls, approval workflows, receipt capture, AI verification, and accounting integrations, so the close begins with cleaner inputs and fewer avoidable gaps.

- Corporate Cards With Spend Limits And Vendor Controls

Alaan lets businesses issue corporate cards with spending limits and vendor restrictions. That gives finance teams better control over card activity during the month and reduces off-policy spend that becomes harder to explain at close. - Approval Workflows Before Month End Pressure Builds

Alaan supports custom approval workflows, so expenses can be reviewed and approved while the month is still active instead of piling up unresolved near reporting cut-off. - Earlier Visibility Into Spend Activity

Finance teams can see transactions in real time across employees, vendors, and categories. That makes it easier to identify missing submissions, unusual spend, or items that need follow-up before the close window tightens. - Receipt Capture And Supporting Documentation

Employees can upload receipts and invoices through the mobile app, Chrome extension, or email, so finance gets cleaner supporting records attached to transactions instead of chasing documents during close. - AI Verification And Duplicate Detection

Alaan extracts receipt data, matches it to transactions, and flags inconsistencies or duplicates. That helps reduce manual checking and improves the quality of records reaching accounting. - Accounting Integration For Cleaner Reconciliation

Alaan integrates with Xero, QuickBooks, NetSuite, and Microsoft Dynamics, allowing expense data to sync in real time. That makes month end reconciliation smoother and reduces manual re-entry when finance is trying to close the books.

In practice, that means finance teams reach month end with fewer unresolved expenses, better documentation, and a cleaner starting point for reconciliations and reporting.

Also Read: Corporate Card Reconciliation Guide

Conclusion

The month end closing process works best when it is treated as a control routine, not just a final accounting exercise. A reliable close depends on whether the business has captured activity properly, reviewed key balances, and resolved enough issues before management starts relying on the numbers.

That is why close quality depends on more than month-end effort alone. It depends on how well expenses, approvals, receipts, and reconciliations are managed throughout the month.

Alaan helps finance teams strengthen that upstream layer with corporate cards, spend limits, approval workflows, real-time visibility, cleaner documentation, and faster reconciliation. That makes the close easier to manage, easier to trust, and easier to complete without unnecessary month-end friction. Book a Demo Today!

FAQs

1. How many days should a month end close take?

That depends on business size, transaction volume, and system maturity. A smaller business may close in a few days, while a more complex environment may need longer. The more useful benchmark is whether the process is consistent and produces numbers that management can trust.

2. What is the difference between month end close and year end close?

Month end close is mainly about producing reliable internal reporting on a recurring basis. Year end close usually carries more statutory, audit, tax, and disclosure pressure, so the level of review is broader and more formal.

3. Which accounts usually cause the most month end delay?

Bank accounts, card activity, accruals, employee expenses, payables, and other control accounts often create the most friction because they depend on timely documents, approvals, and reconciliation support.

4. Is it better to close faster or more accurately?

Speed matters, but only if accuracy holds. A fast close that still leaves material gaps, unsupported balances, or unresolved exceptions does not help management much. The better goal is a repeatable close that is both timely and dependable.

5. Why do month end issues often repeat every cycle?

Because many close problems are process problems, not one-off errors. If receipts arrive late, approvals stay informal, or reconciliations depend on manual follow-up, the same bottlenecks usually return each month.

6. Should finance wait for every item to be final before closing?

Not always. Some items may need reasonable estimates or documented follow-up if waiting would delay reporting too much. What matters is that unresolved items are visible, controlled, and not hidden inside the final numbers.