In the UAE today, delayed payments and rising defaults are squeezing financial control. A recent survey indicates that 58% of credit-based sales in the UAE are paid late, mainly due to administrative delays or customer liquidity stress. That kind of strain forces finance teams to scramble, reconciling accounts on the fly, chasing missing receipts, and plugging holes often only when month-end arrives.

Your schedule is already packed, overseeing growth targets, approval flows, VAT compliance, and strategic planning. Yet bank reconciliation still stands as a pillar you can't afford to sideline.

Done in real-time, it instantly links each transaction to its source, surfaces mismatches early, and provides sharp clarity across accounts. If relegated to a month-end chore, discrepancies accumulate, duplicates infiltrate, and financial visibility becomes blurred.

Key Takeaways

- Types of Reconciliation: Continuous reconciliation offers real-time accuracy, while periodic and inter-company methods support scheduled and multi-entity reporting needs.

- Manual vs Automated: Automation replaces manual checks with instant transaction matching and live updates, reducing delays and errors.

- 6-Step Process: Structured reconciliation ensures all entries align, discrepancies are resolved, and books close accurately each cycle.

- Automation Benefits: AI-driven systems enhance efficiency, maintain VAT compliance, and provide real-time financial visibility.

- Alaan’s Role: Alaan streamlines reconciliation by integrating corporate cards, expense automation, and accounting sync, simplifying control for finance teams.

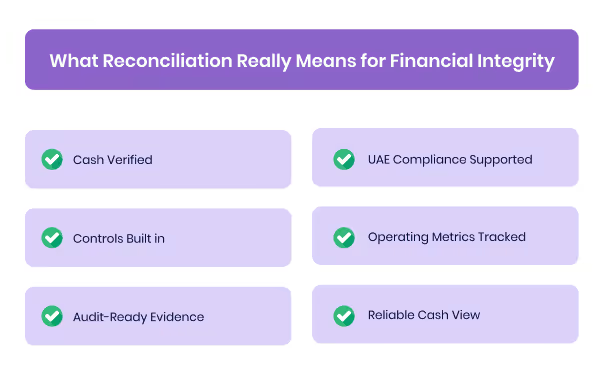

What Reconciliation Really Means for Financial Integrity

Reconciliation is a control that proves your cash and confirms your reported results. It means that every entry in the ledger is supported by the bank and documented, with a clear owner for each exception.

In the UAE, this also ensures the accuracy of VAT and corporate tax. If postings are late, receipts are missing, or card spend lacks proof, your filings and audits are at risk. Moving from month-end checks to daily or real-time checks closes that gap.

What good reconciliation looks like:

- Cash verified: The ledger matches the bank. Differences are logged, assigned, and cleared within a set time window.

- Controls built in: Adjustments follow maker–checker. Policy checks happen before spending. Access is role-based.

- Audit-ready evidence: Each match links the bank line, journal entry, and receipt. Auditors can follow the trail in minutes.

- UAE compliance supported: VAT amounts tied to paid invoices with valid receipts. Period cut-offs are clean for corporate tax.

- Operating metrics tracked: Close time, exception rate per 1,000 transactions, and ageing of unreconciled items are monitored and improved.

- Reliable cash view: Treasury uses reconciled intraday balances for payment runs, FX plans, and working-capital calls.

Reconciliation done this way is not extra work. It is how finance teams keep numbers correct, fillings safe, and cash visibility dependable, every day.

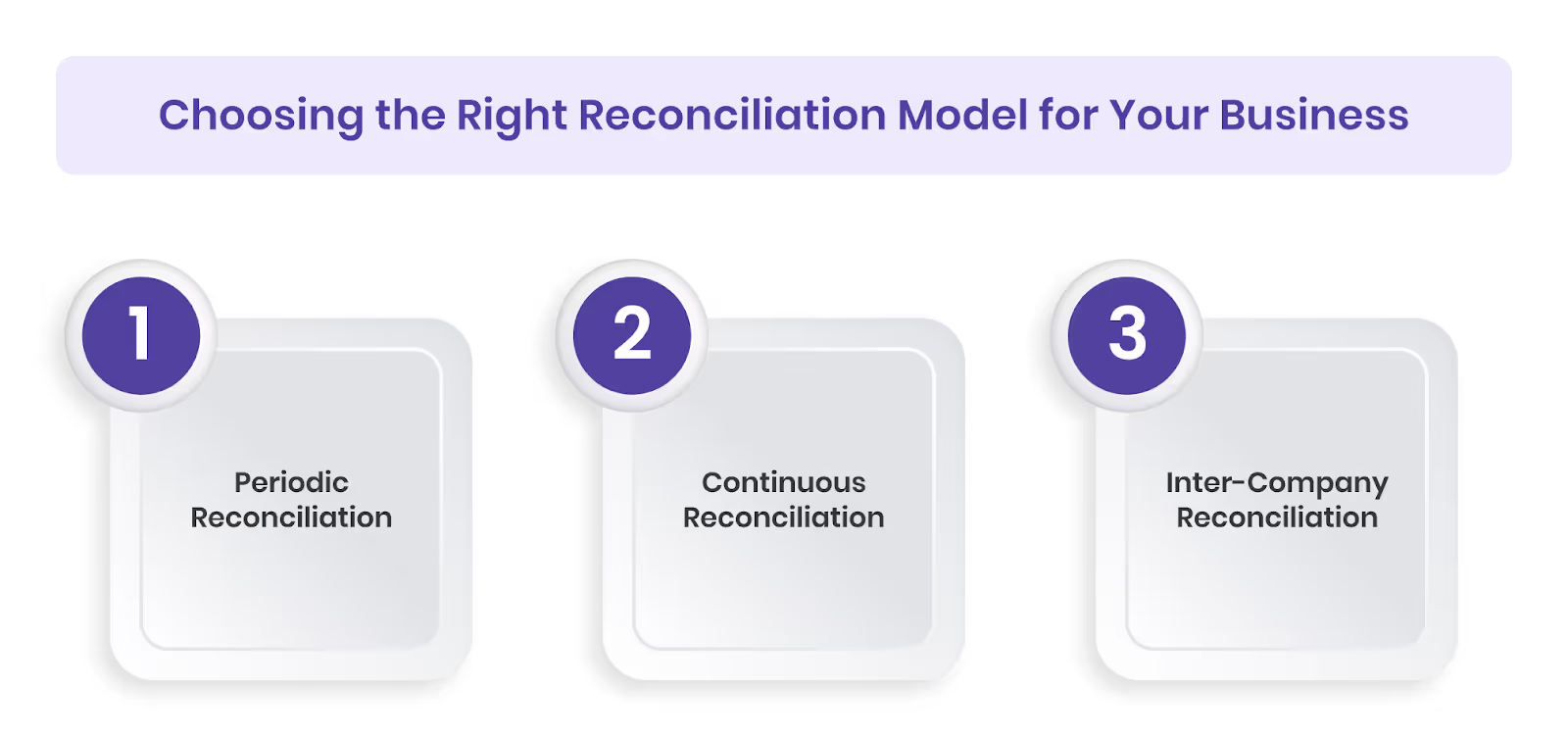

Choosing the Right Reconciliation Model for Your Business

Different businesses need different reconciliation models. The right one depends on how many transactions you handle, how fast you move money, and how much control you need.

1. Periodic Reconciliation (Weekly or Monthly)

This is the traditional approach used by smaller teams or companies with limited transactions.

- Best for: Companies with predictable cash flow and few bank accounts.

- How it works: The team reconciles at fixed intervals, usually weekly or month-end, matching all entries against the bank statement.

- Benefits: Easy to manage and less setup needed.

- Limitations: Errors may be caught late, leading to last-minute adjustments during closing.

2. Continuous Reconciliation (Daily or Real-Time)

Used by modern finance teams that rely on up-to-date numbers.

- Best for: Businesses with high transaction volumes or daily cash movements.

- How it works: Transactions are matched automatically as they occur through connected bank feeds.

- Benefits: Instant visibility, fewer surprises during audits, and stronger VAT accuracy.

- Limitations: Needs automation tools and consistent process ownership.

[cta-11]

3. Inter-Company Reconciliation (For Group Entities)

Designed for businesses operating across multiple entities or regions.

- Best for: Companies with internal transfers, shared services, or foreign currency transactions.

- How it works: Matches entries between related entities to ensure internal balances align.

- Benefits: Clean consolidation and fewer cross-entity mismatches.

- Limitations: More complex setup and monitoring.

Quick Way to Decide

Different models fit different businesses, but all serve one goal: maintaining financial integrity and control.

Also Read: Cash Flow Optimisation Strategies for UAE Businesses in 2025

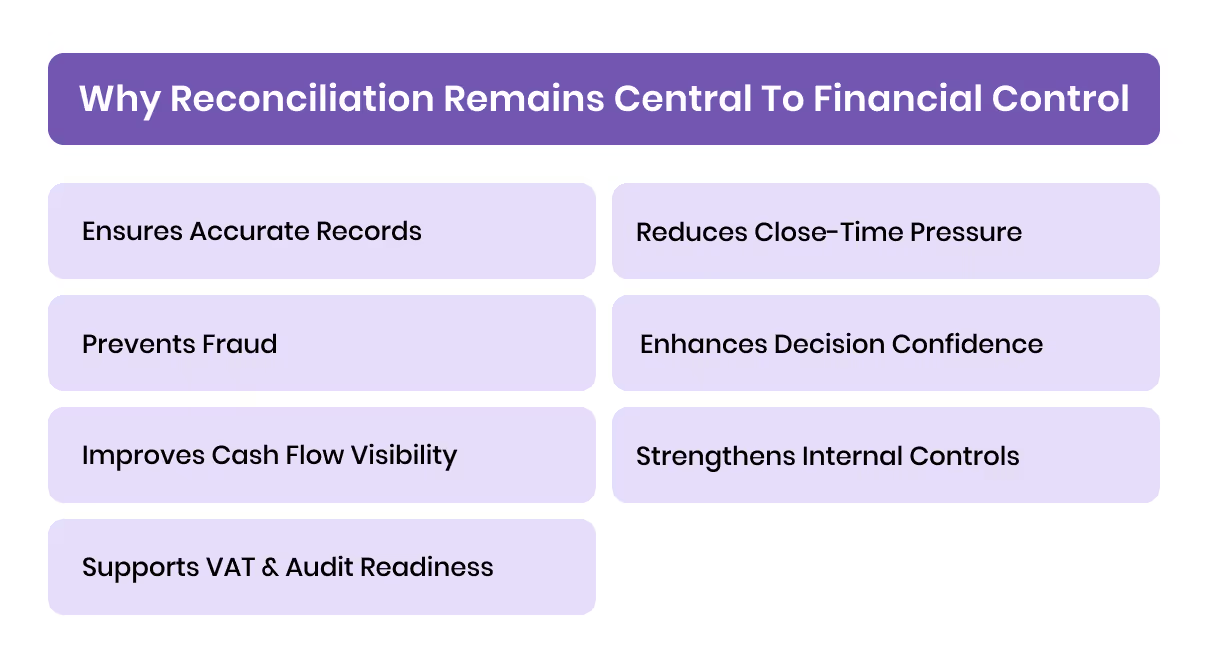

Why Reconciliation Remains Central to Financial Control

Reconciliation is how finance teams protect accuracy, prevent misuse, and maintain trust in reported numbers. Here are the key advantages:

- Ensures Accurate Records: Confirms that every entry in the ledger matches the bank, reducing the risk of misstatements and delayed adjustments.

- Prevents Fraud: Identifies duplicate, missing, or unauthorised transactions early, limiting financial and reputational risk.

- Improves Cash Flow Visibility: Provides a clear, updated view of available cash, helping plan payments and manage liquidity effectively.

- Supports VAT and Audit Readiness: Keeps receipts, journals, and approvals linked to each transaction to meet UAE regulatory requirements.

- Reduces Close-Time Pressure: Maintains accuracy continuously, preventing end-of-month reconciliations from turning into crisis management.

- Enhances Decision Confidence: Enables CFOs and business heads to rely on verified data for forecasting and strategic planning.

- Strengthens Internal Controls: Establishes accountability by tracking who reviews, approves, and resolves each variance.

As businesses scale and financial complexity rises, manual reconciliation becomes a bottleneck. The solution? Automation.

Automated Reconciliation: The New CFO Standard

Manual reconciliation may still be practical when transaction volumes are low and complexity is minimal. However, once your company expands, the number of cards, approvals, and line items increases, and so do the delays, errors, and blind spots. That's when automation becomes not a luxury, but a necessity.

For most finance teams, automation isn't optional; it's essential. Alaan brings together smart corporate cards, AI-based expense matching, and seamless accounting integration to make real-time reconciliation the standard, not the exception. Let Alaan take over the repetitive work, so your team can focus solely on exceptions and insights.

[cta-1]

See how Alaan can turn reconciliation from a burden into a core financial control by booking a demo today.

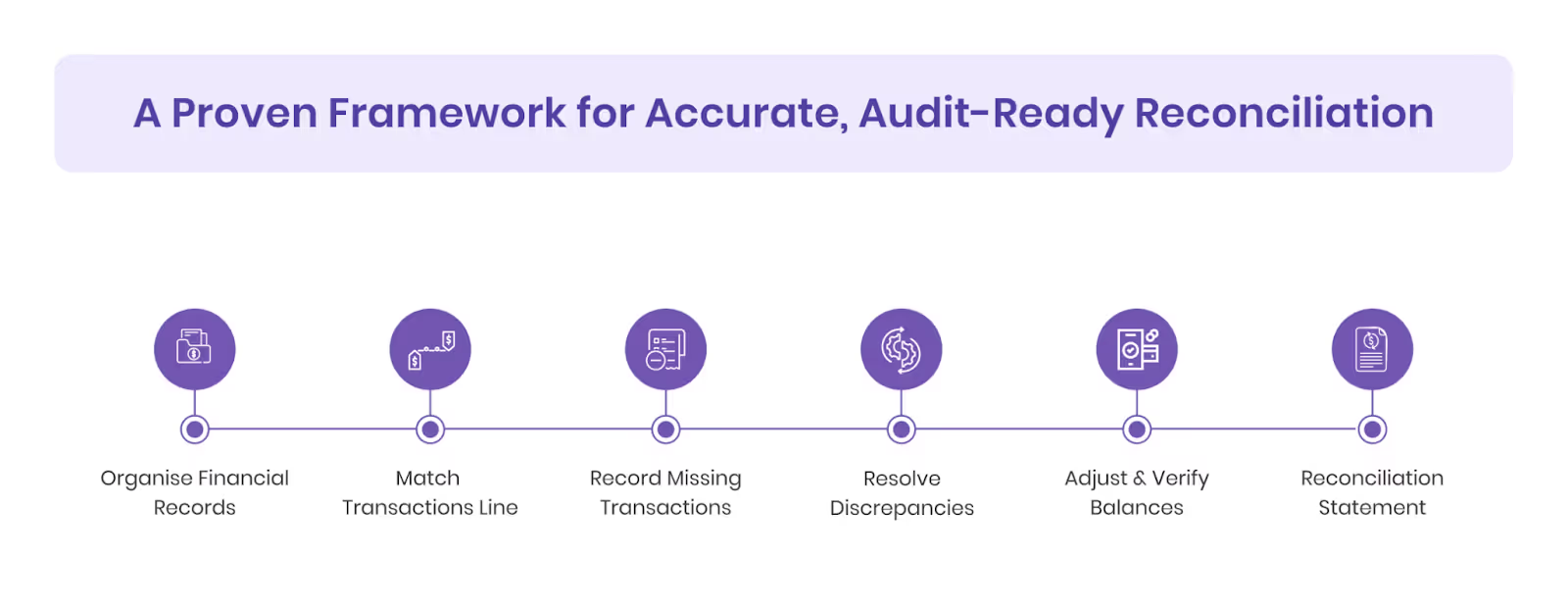

A Proven Framework for Accurate, Audit-Ready Reconciliation

A reliable reconciliation process establishes accuracy, control, and audit readiness. The framework below outlines a clear, repeatable approach that keeps your books consistent and compliant.

Step 1: Gather and Organise Financial Records

Before you begin, ensure all supporting data is complete and up to date.

- Collect bank statements, general ledgers, payment vouchers, and receipts for the same reporting period.

- Use a standard checklist to confirm nothing is missing.

- Keep source documents organised digitally for easier tracking during audits.

Step 2: Match Transactions Line by Line

This is where accuracy begins.

- Compare each entry in your ledger with the bank statement.

- Mark off every match and isolate unverified items such as pending deposits or uncleared cheques.

- Use transaction codes or references to ensure precise matching across accounts.

Step 3: Identify and Record Missing Transactions

Gaps between your books and the bank are common, what matters is how quickly they’re fixed.

- Add entries that appear on the bank statement but not in your books (e.g., bank fees, direct debits, interest, or FX differences).

- Validate each new entry with supporting evidence like payment slips or emails.

- Record the posting date accurately to avoid period mismatches.

Step 4: Investigate and Resolve Discrepancies

Every unresolved item should have a clear explanation and owner.

- Trace errors such as double postings, delayed entries, or unauthorised payments.

- Assign responsibility and set resolution timelines.

- Document findings in a reconciliation log to maintain a full audit trail.

Step 5: Adjust and Verify Balances

Once discrepancies are resolved, update and confirm the final balances.

- Adjust the ledger and bank balances with approved corrections.

- Recheck that both figures match exactly.

- Obtain sign-off from reviewers or finance leads before finalising.

Step 6: Prepare the Reconciliation Statement

Turn your work into a clear, audit-ready summary.

- Include the opening balance, adjustments, and final reconciled amount.

- Attach supporting documents and variance explanations.

- File the statement in your monthly close package as permanent evidence of control.

Once this framework becomes a reliable rhythm, scaling it manually becomes harder than it looks. Alaan complements the same process by issuing unlimited virtual and physical corporate cards, enforcing spend controls, integrating with accounting systems, and using AI to assist in matching and reconciliation.

[cta-2]

Also Read: How to Automate Your Accounting Workflow Process: A Complete Guide

Where Most UAE Finance Teams Lose Time (and Accuracy)

Many finance teams stumble not because reconciliation is hard, but because their systems and methods are outdated. Below are the common pitfalls, all avoidable with better design.

- Heavy Manual Work: Teams still spend entire days exporting CSVs and manually matching line by line. Manual reconciliation has an average error rate of about 19.2%, while automation reduces it to nearly zero.

- Timing Gaps Across Systems: Bank entries and internal ledgers often clear on different days. This "between-systems lag" leads to variances that remain unresolved until month-end, hurting daily cash visibility.

- Overlooked or Late Entries: Bank fees, interest, or FX adjustments frequently show up in statements but are recorded late, or not at all. These gaps accumulate and distort reports over time.

- Compliance Overhead: In the UAE, every transaction must carry proof (receipt, invoice). When reconciliation lag or documentation is missing, audits drag and risk surfaces.

- Disconnected Platforms: Banking, card, and accounting systems often don’t talk to each other. Finance teams chase data across apps and spreadsheets, slowing down checks and creating gaps.

- No Performance Metrics: Most teams don’t track how long exceptions linger, match rates, or monthly close speed. Without such metrics, inefficiency hides under the radar.

- Technology Adoption Gap: About 49% of UAE finance teams have adopted AI, but only 37% report measurable ROI. Many implementations fail to deliver value due to partial automation or lack of real-time reconciliation.

Addressing these challenges through automation ensures accuracy, improves reporting reliability, and supports confident decision-making.

How Leading UAE Finance Teams Reconcile in Real Time with Alaan

Modern finance teams in the UAE are moving away from month-end reconciliation and adopting continuous, automated processes.

Alaan helps finance teams achieve this transformation by integrating spend management, automation, and accounting in one workflow.

- Instant Expense Recording: Each time a payment is made using an Alaan corporate card, the transaction automatically appears in the platform with real-time tracking. This eliminates the need for manual data entry during reconciliation.

- AI-Powered Receipt Matching: Alaan’s platform uses AI to extract data from uploaded receipts and match it with card transactions, reducing the chances of mismatched or missing entries.

- Accounting Integration: Alaan integrates with leading accounting tools such as Xero, QuickBooks, NetSuite, and Microsoft Dynamics, automatically syncing verified transactions into ledgers for reconciliation and reporting.

- Integrated Corporate Cards: Payments made using Alaan’s Visa-powered cards, physical or virtual, are instantly logged in the expense system. This reduces the traditional lag between spending and reconciliation.

- Real-Time Spend Visibility: Finance teams can view all expenses, transactions, and approvals on a single dashboard. This transparency ensures that any anomalies are visible before the monthly close, improving control and oversight.

- VAT Compliance and Record Accuracy: For UAE-based businesses, Alaan automatically reads and validates VAT data from receipts, helping maintain accurate, audit-friendly expense records aligned with Federal Tax Authority requirements.

- Automated Workflows and Approvals: The platform supports customised approval flows so that expenses are reviewed and approved in line with company policy before being reconciled or booked in accounting systems.

[cta-3]

Alaan does not replace bank statement feeds but complements them by automating the most time-intensive parts of reconciliation, expense tracking, transaction validation, and accounting sync.

This allows finance teams to reconcile faster, maintain compliant records, and achieve near real-time financial visibility without manual review.

Conclusion

Manual reconciliation slows teams down, invites errors, and limits visibility. Automation turns this challenge into control, enabling real-time accuracy, faster closes, and audit-ready confidence.

At Alaan, we transform this process by giving finance teams instant visibility and control over every transaction.

Ready to modernise your reconciliation process? Book a Demo Now.

FAQs

1. Why is bank reconciliation important for financial control?

Regular bank reconciliation ensures the company’s recorded balance matches the actual bank balance, helping finance teams identify errors, unauthorised transactions, and timing differences early. It strengthens internal control and supports cleaner financial reporting.

2. What is the best way to reconcile bank accounts efficiently?

The most efficient way is to automate the process. Using platforms like Alaan, every card transaction and expense is captured instantly, matched with receipts, and synced to accounting systems, reducing manual reconciliation time and improving accuracy.

3. How can automation improve bank reconciliation accuracy?

Automation removes the risk of human error by matching transactions, flagging inconsistencies, and updating records in real time. With AI verification and VAT validation, automated systems ensure data is both accurate and compliant with UAE tax standards.

4. Does Alaan handle both bank account and expense reconciliation?

Yes. Alaan links corporate card transactions directly with accounting and expense systems. This means most expenses are pre-verified and recorded before reconciliation begins, making the bank reconciliation process faster and easier for finance teams.

5. How often should businesses reconcile their bank accounts?

Monthly reconciliation is standard practice, but many UAE-based companies prefer weekly or automated daily reconciliation to maintain real-time visibility. With Alaan, reconciliations can effectively happen continuously as transactions occur.