As the UAE’s tax environment evolves, businesses are feeling increasing pressure to plan their finances strategically before year-end.

Many companies miss out on valuable deductions and incentives because of last-minute planning, potentially leaving millions in avoidable taxes on the table. With a 9% corporate tax on profits above AED 375,000 and ongoing VAT responsibilities, now is the ideal time to take control of your year-end tax strategy.

This guide shows UAE businesses the essential steps to maximise deductions, stay VAT-compliant, optimise employee benefits, and meet key deadlines, helping you close the year confidently and set the stage for a financially strong 2027.

Key Takeaways:

- Understand the UAE Tax System - Corporate tax at 9% applies to profits above AED 375,000, VAT remains at 5%, and businesses must comply with deadlines to avoid penalties.

- Review Financial Statements Early - Analysing revenue, expenses, profit margins, assets, liabilities, and cash flow helps identify opportunities for deductions and better financial planning.

- Maximise Deductions and Incentives - Record all eligible expenses, use government incentives, reclaim VAT, claim capital allowances, optimise employee benefits, and plan for future investments.

- Forecast Future Tax Obligations - Project income, expenses, tax credits, and deductions, accounting for regulatory changes, business growth, and operational adjustments.

- Track Key Deadlines = Ensure VAT, corporate tax, employee-related filings, and audit/reporting deadlines are met to prevent penalties.

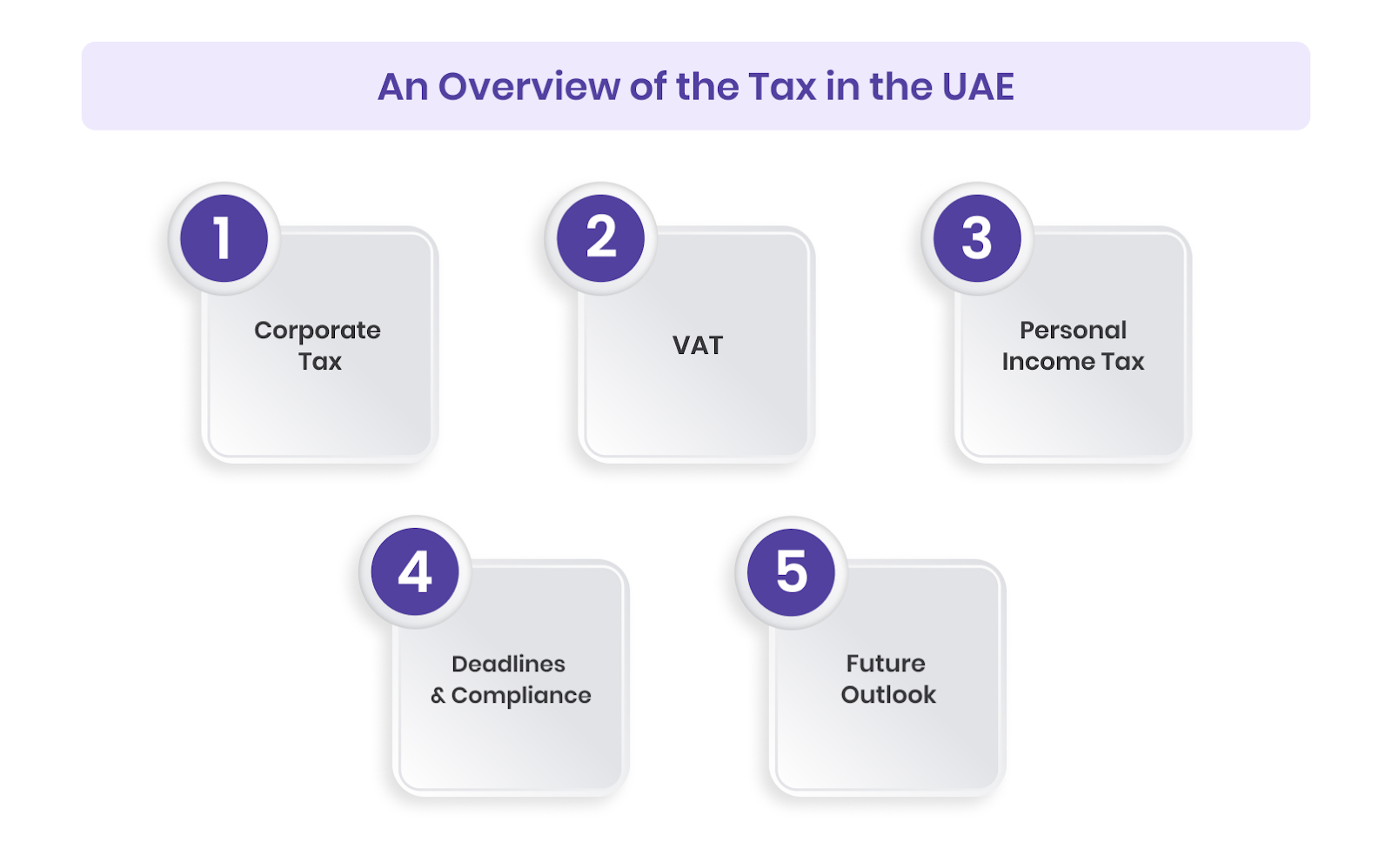

An Overview of the UAE Tax System

The UAE’s tax system in 2026 continues to evolve. With the introduction of corporate tax and ongoing VAT compliance requirements, businesses need to stay updated to remain compliant and make smart financial decisions. Below is an overview of the Tax in the UAE.

1. Corporate Tax

Since 2023, the UAE has applied a 9% corporate tax on profits above AED 375,000. Most businesses fall under this rule, except for certain free zone entities that still enjoy exemptions under specific conditions.

For all companies, understanding how the new tax regime applies is essential to avoid surprises and ensure proper filing.

2. VAT

VAT remains at 5% in 2025 and applies to most goods and services. Any business with taxable supplies exceeding the AED 375,000 threshold must register for VAT, file accurate returns, and maintain complete records.

While VAT-registered businesses can reclaim input VAT on eligible purchases, missing documents or errors in filing can quickly lead to penalties.

3. Personal Income Tax

The UAE does not levy personal income tax, which continues to make it appealing for professionals and entrepreneurs. That said, certain income streams, such as property sales or business-related income, may still attract taxes under corporate tax rules.

Sole proprietors and business owners should pay close attention to how these changes might apply to them.

4. Deadlines and Compliance

The Federal Tax Authority (FTA) sets strict deadlines for corporate tax and VAT filings, which may be quarterly or annual, depending on the business.

Missing these deadlines can result in fines. Staying organised and using reliable tools, such as Alaan, can make filing smoother and help businesses avoid penalties.

5. Future Outlook

The UAE’s tax framework is still evolving. Businesses should keep an eye on potential changes, whether that’s adjustments to corporate tax rates, VAT thresholds, or the introduction of new taxes.

Proactive planning and staying informed will be the key to managing risks and making the most of opportunities in this shifting environment.

Knowing the tax rules makes it easier to review your financial statements and see where adjustments are needed.

Also Read: What is a VAT Compliance Health Check and How to Stay Audit-Ready in the UAE

Review of Financial Statements and Key Metrics

A thorough review of financial statements and key metrics is one of the most important steps businesses can take before closing the tax year. By analysing performance early, businesses can spot trends, measure progress against goals, and identify potential risks before they become bigger challenges.

Here are some of the most important financial metrics to review:

- Revenue: Comparing current revenue with projections and past periods helps assess whether the business is meeting its growth and financial targets.

- Expenses: Looking closely at operational and non-operational expenses reveals opportunities to cut costs while making the most of tax-deductible items.

- Profit Margins: Both gross and net profit margins provide valuable insights into profitability and efficiency, helping businesses understand how well they’re converting sales into actual profits.

- Assets and Liabilities: A balance sheet review shows the company’s financial stability. Strong assets paired with manageable liabilities create room for growth and reduce debt-related risks.

- Cash Flow: Healthy cash flow ensures there’s enough liquidity to cover day-to-day operations and prevent shortages that can disrupt business activities.

Once you have a clear picture of your finances, you can focus on maximising deductions and taking advantage of incentives.

Also Read: Cash Flow Optimisation Strategies for UAE Businesses in 2026

How to Maximise Deductions and Incentives?

Maximising deductions and incentives before the tax year closes is one of the smartest ways businesses can strengthen their tax planning. By making the most of available opportunities, companies can lower taxable income, improve cash flow, and stay aligned with local regulations.

Here are some practical strategies businesses in the UAE can use to get the best out of deductions and incentives before the year ends.

1. Review Business Expenses for Tax Deductions

A good starting point is making sure all eligible expenses are properly recorded. In the UAE, legitimate operating costs can be deducted from taxable income. These typically include:

- Operational Costs: Day-to-day expenses like rent, utilities, office supplies, and maintenance.

- Employee Benefits: Salaries, bonuses, training programmes, and benefits such as health insurance.

- Travel and Accommodation: Costs related to business travel, including transport, stays, and meals, provided they are supported with proper documentation.

- Depreciation: Assets like machinery, vehicles, or equipment can be depreciated over time. Keeping accurate records here can lead to meaningful tax savings.

2. Take Advantage of Government Incentives

The UAE has rolled out a range of incentives to promote business growth and innovation, many of which can ease the overall tax burden. Examples include:

- Investment in R&D: Companies investing in research, particularly in technology and innovation, may qualify for tax credits or special allowances.

- Free Zone Incentives: Businesses in free zones often enjoy tax exemptions, reduced import/export duties, and other benefits. Since rules vary across free zones, understanding the specific framework is key.

- Sustainability Initiatives: As green growth remains a policy and business priority, companies adopting renewable energy or eco-friendly practices may access additional tax advantages.

3. Maximise VAT Recovery

For VAT-registered businesses, year-end is the right time to ensure no VAT recovery opportunities are missed. Key steps include:

- Review VAT Invoices: Submit all eligible VAT-paid invoices to the Federal Tax Authority before the year ends.

- Input Tax Recovery: Reclaim VAT paid on business-related purchases like supplies, equipment, and services.

- Compliance Checks: Ensure all claims follow UAE VAT laws, as errors or missed filings can invite penalties.

4. Consider Capital Allowances

Capital allowances allow businesses to deduct the cost of fixed assets against taxable income. This can significantly reduce tax liability over time.

Ensure eligible assets are depreciated in line with tax guidelines. In some cases, businesses can fast-track depreciation to increase deductions in the current year.

5. Optimise Employee Benefits and Bonuses

How compensation packages are structured can also influence tax efficiency. Businesses can optimise deductions by looking at:

- Employee Bonuses: Bonuses are deductible, and paying them before the year ends ensures they count in the current tax cycle.

- Retirement Contributions: Depending on the scheme, contributions to employee pension or savings plans may also be deductible.

- Health Insurance and Benefits: Offering employee-friendly benefits such as health cover or wellness initiatives can provide both value to staff and tax relief for the company.

6. Plan for Future Investments

Year-end planning focuses on the present and preparing for growth. Businesses can:

- Accelerate Purchases: Bringing forward large asset purchases before year-end allows you to claim deductions earlier.

- Invest in Growth: Reinvesting profits into expansion through new locations, product launches, or hiring can open the door to future tax incentives.

By combining short-term actions with long-term planning, businesses can optimise their tax position today while building a stronger foundation for tomorrow.

Alongside deductions, another important factor is your business structure, which can influence overall tax efficiency.

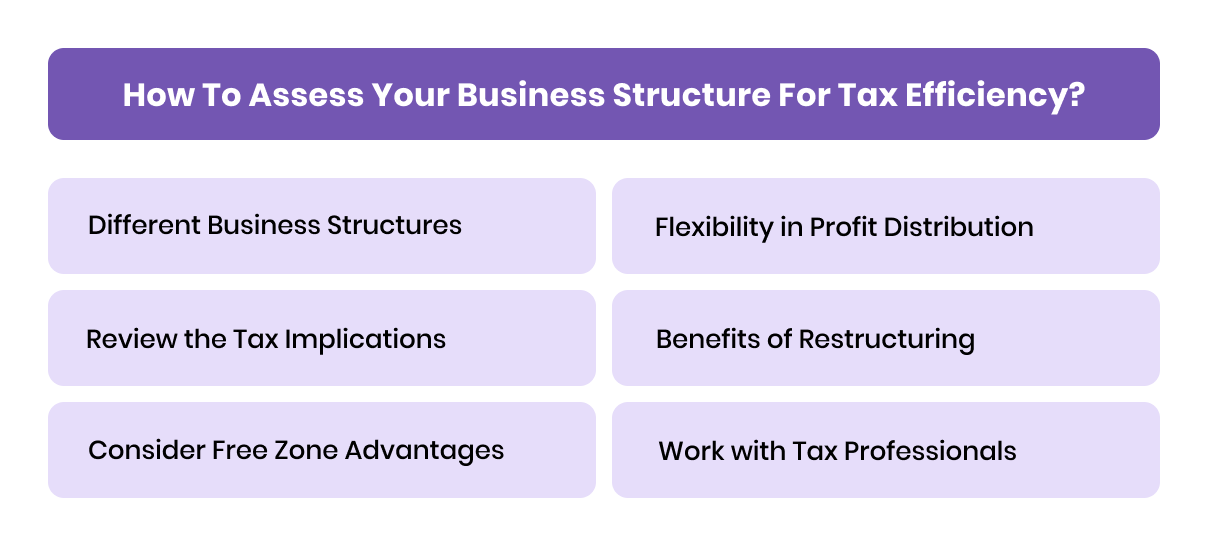

How to Assess Your Business Structure for Tax Efficiency?

Choosing the right business structure is a key step in maximising tax efficiency and reducing liabilities. In the UAE, businesses can choose from several structures, each with different tax implications. Here's how to assess your business structure for tax efficiency:

1. Understand the Different Business Structures in the UAE

The UAE offers a variety of business structures, each with its own benefits and requirements:

- Sole Proprietorship: Owned and managed by a single individual. This structure is simple to set up, but it may limit flexibility in tax planning, especially as the business grows.

- Limited Liability Company (LLC): A popular option where owners’ liability is limited to their shares. LLCs are subject to corporate tax but offer more flexibility in ownership and liability protection.

- Free Zone Company: Companies in free zones enjoy tax exemptions, such as corporate tax holidays, usually for a fixed period. However, these benefits often come with restrictions on trading outside the free zone.

- Branch of a Foreign Company: Foreign businesses can open a branch in the UAE. Branches follow the same tax rules as local businesses but may have additional reporting requirements.

2. Review the Tax Implications of Your Current Structure

Each business structure has specific tax implications that can affect your overall liability:

Corporate Tax: LLCs and other taxable entities pay corporate tax on profits. Check for:

- VAT: Businesses exceeding AED 375,000 in taxable supplies must register for VAT, unless exempt or zero-rated. How VAT applies can vary depending on your business structure and activities.

- Employee Costs: While the UAE does not levy personal income tax, businesses must consider employee-related costs like end-of-service benefits. Structuring compensation and benefits strategically can create tax efficiencies.

3. Consider Free Zone Advantages

Free zones offer several benefits that can reduce tax burdens:

- Tax Holidays: Many free zones provide corporate tax exemptions for 15 to 50 years, helping reduce early-stage tax liabilities.

- 100% Foreign Ownership: Entrepreneurs can retain full control of their business without requiring a local partner.

- Customs Duty Exemptions: Free zone businesses often enjoy exemptions from import and export duties, lowering operational costs.

4. Assess Flexibility in Profit Distribution

Different business structures offer varying flexibility in how profits are distributed:

- LLCs: Profit distribution usually follows ownership percentages, allowing owners to structure payouts efficiently.

- Free Zone Companies: Some free zones allow full profit repatriation, meaning profits can be transferred abroad without additional tax.

- Sole Proprietorships: All profits belong to the owner, but options for reinvesting or splitting income for tax purposes are limited.

5. Consider the Costs and Benefits of Restructuring

If your current structure limits tax efficiency, restructuring could be worth considering:

- Reduce Tax Liabilities: Switching to a more tax-efficient structure may lower corporate taxes or unfold exemptions.

- Increase Operational Flexibility: A different structure can provide more options for capital investment, ownership changes, or access to incentives.

- Simplify Compliance: Certain structures make accounting and regulatory reporting easier, particularly for tax filings.

6. Work with Tax Professionals

Optimising your business structure for tax efficiency requires expertise in UAE tax laws and regulations. Tax professionals can help:

- Identify the most tax-efficient structure for your business based on size, industry, and growth plans.

- Go through complex regulations and ensure compliance with evolving tax laws.

- Provide tailored advice on restructuring, VAT optimisation, and capital investments.

Optimising the structure also helps in planning employee-related taxes, such as bonuses and benefits.

Tax Planning for Employees: Bonuses and Benefits

Tax planning for employee bonuses and benefits plays an important role in optimising tax efficiency and reducing liabilities. When compensation is structured effectively, businesses can save on taxes while offering meaningful rewards to their teams.

Below are some practical ways companies in the UAE can make the most of bonuses and benefits.

1. Optimising Employee Bonuses

Paying out bonuses before the end of the tax year allows businesses to claim them as deductible expenses. For employees, receiving a bonus within the current year means they can benefit from their existing tax bracket.

Performance-based bonuses tied to company or individual achievements help align rewards with results. Alternatively, structuring bonuses as stock options or profit-sharing plans can create long-term tax advantages for both parties.

2. Managing Employee Benefits

Employer-provided health insurance is exempt from VAT, making it one of the most attractive benefits businesses can offer. Also, contributing to employee retirement or pension plans can lower taxable income for the companies. Providing transportation services or allowances can also reduce taxable income.

3. Structuring Benefits for Tax Efficiency

Offering employees a choice between different benefits, such as insurance, allowances, or education support, ensures packages meet personal needs while optimising tax efficiency.

Also, certain allowances, like housing or school fees for expatriate employees, may be partially or fully exempt from tax in the UAE. Including these in compensation plans can significantly enhance the overall value without adding extra tax costs.

4. Regular Review of Compensation Packages

Regularly reviewing and adjusting benefits ensures packages remain competitive and aligned with both employee expectations and regulatory requirements.

Updating compensation structures helps maintain a balance between tax obligations and employee satisfaction. Consistent reviews keep packages market-relevant and ensure they remain tax-efficient over time.

5. Seek Professional Tax Advice

Partnering with tax experts helps businesses ensure their compensation packages comply with UAE regulations while maximising savings. This support provides peace of mind for employers and ensures employees benefit from well-structured, compliant rewards.

After addressing current obligations, forecasting future taxes ensures smooth financial planning for the year ahead.

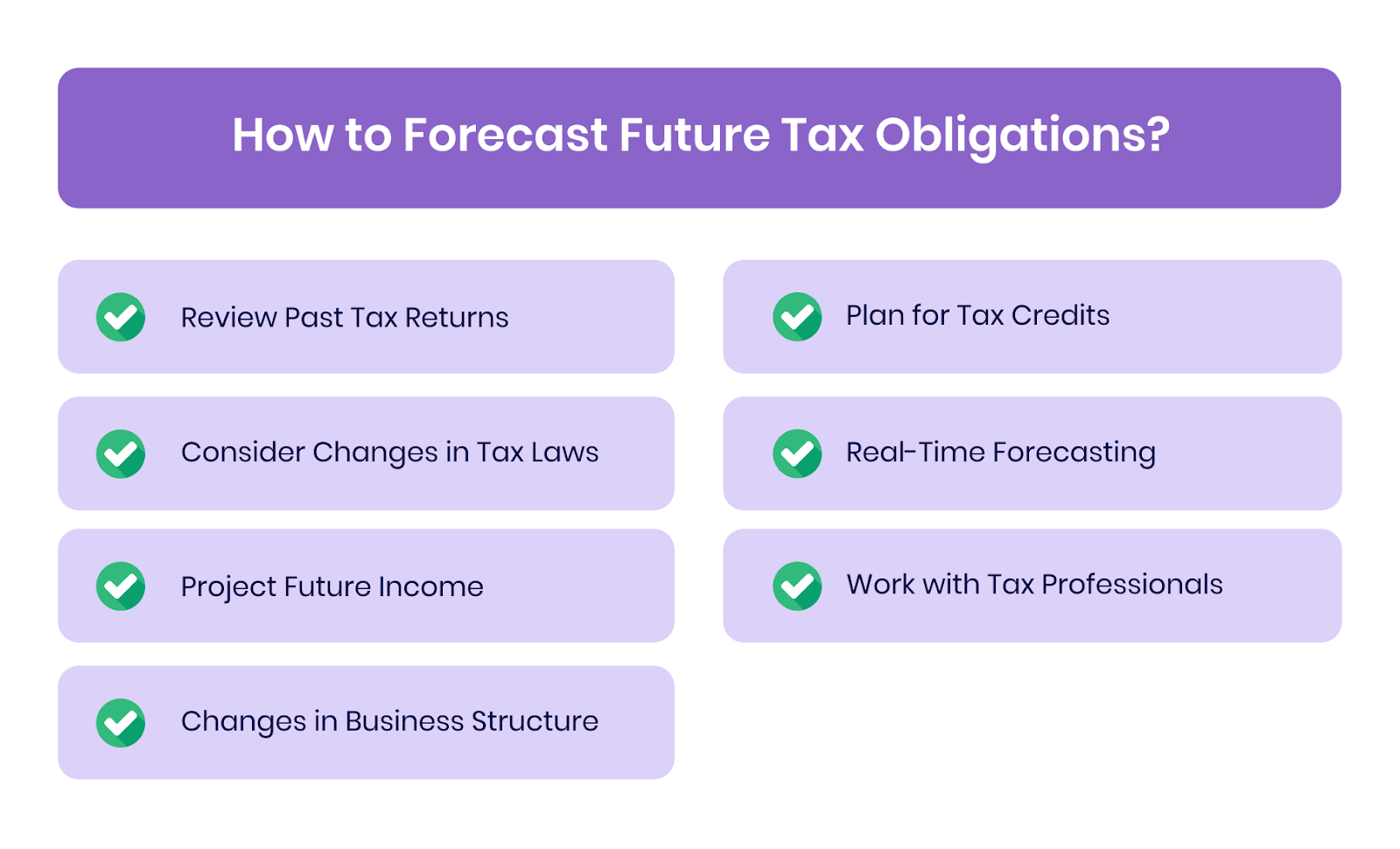

How to Forecast Future Tax Obligations?

Forecasting future tax obligations is a crucial aspect of tax planning. By estimating tax liabilities in advance, businesses can manage cash flow more effectively, avoid unexpected surprises, and make confident financial decisions. Here's how to forecast future tax obligations:

1. Review Past Tax Returns and Financial Statements

Look back at past tax returns and financial statements. Track how revenue has changed year-on-year and compare it with industry benchmarks to better predict future income and related tax obligations.

Review the key expense categories, such as operating costs, employee benefits, and capital investments, that could influence taxable income.

2. Consider Changes in Tax Laws and Regulations

Tax laws don’t remain static, and even small changes can significantly alter future obligations. With the introduction of corporate tax in the UAE, businesses must consider how updates to these rules may impact their liabilities.

Any change in VAT rates or exemptions could shift future obligations. This makes it essential to monitor government policies and international agreements.

3. Project Future Income and Expenses

Accurate projections of income and expenses form the backbone of tax forecasting. Estimate sales using existing contracts, market conditions, and expected seasonal fluctuations, while also considering potential new revenue streams.

Project operating costs include rent, salaries, raw materials, and utilities. Don’t forget to include planned investments or cost-saving initiatives that could shift expense patterns.

4. Account for Changes in Business Structure or Operations

Strategic changes in how a business operates can have a direct tax impact. If you are restructuring, launching new products, or expanding into fresh markets, these shifts should be part of the forecast.

Moving into new regions may bring different tax rates or exemptions, especially for businesses in free zones. Also, changing legal structures, such as converting from a sole proprietorship to an LLC, can alter tax responsibilities significantly.

5. Plan for Tax Credits and Deductions

Tax credits and deductions can lighten the tax load, but only if they’re anticipated and included in forecasts. Companies in sectors like renewable energy, R&D, or technology may qualify for specific tax breaks that reduce overall liability.

Also, capital spending on equipment, property, or infrastructure can sometimes qualify for accelerated depreciation or other deductions.

6. Use Financial Software for Real-Time Forecasting

Modern financial software enables more accurate and time-efficient tax forecasting by providing real-time insights. Many tools integrate directly with accounting systems, offering up-to-date calculations based on current data.

Businesses can model different “what-if” scenarios, such as higher sales or changes in tax laws, to see how outcomes would affect their obligations.

7. Work with Tax Professionals for Accurate Forecasting

Tax advisors can highlight risks, identify saving opportunities, and recommend strategies like income deferral or accelerated deductions. Since tax laws are constantly evolving, professionals can ensure compliance while helping businesses capitalise on new opportunities.

Working with experts helps companies gain clarity, minimise liabilities, and strengthen their overall tax planning strategy.

Accurate forecasts are most effective when aligned with the legal and regulatory requirements that apply to your business.

Legal and Regulatory Considerations

In the UAE, businesses operate within a layered framework of local, federal, and even international regulations, all of which can directly influence how they plan and manage their taxes. Below are the key legal and regulatory considerations.

1. Compliance with Federal and Local Tax Laws

In the UAE, businesses must comply with both federal and local tax requirements. These include corporate tax and VAT at the federal level, along with emirate-specific regulations that may influence tax obligations.

Businesses earning profits above AED 375,000 are required to pay corporate tax. Also, they need to register for VAT where required, issue VAT-compliant invoices, and submit timely and accurate VAT returns.

2. Free Zones and Special Tax Regimes

Each free zone operates under its own set of requirements, and exemptions usually apply only when businesses meet certain conditions. For instance, conducting business outside the free zone can attract additional tax obligations.

While many zones offer long-term tax holidays, businesses must meet operational requirements to retain these benefits. This may include maintaining a minimum workforce, focusing on specific industries, or generating revenue in line with free zone policies.

3. Employment Law and Employee Benefits Compliance

Employers must provide benefits such as end-of-service gratuity, health insurance, and other statutory entitlements. Companies employing expatriates also need to ensure compliance with visa regulations and, where relevant, home-country tax rules.

All contracts must follow the UAE Labour Law. Deviating from prescribed standards in areas such as wages, working hours, or termination procedures could result in disputes or legal action.

4. International Tax Considerations

The UAE has signed several agreements to minimise double taxation and ease global business activities. Double Tax Treaties (DTTs) allow businesses to avoid paying tax twice on the same income by providing credits or exemptions for taxes already paid abroad.

Companies with related entities across different jurisdictions must follow transfer pricing rules. These require transactions to be priced as if the entities were independent, helping prevent profit shifting and ensuring fair taxation.

5. Data Privacy and Financial Reporting Regulations

Modern tax planning also involves compliance with data protection and reporting requirements. Businesses that handle personal or financial data must comply with UAE data protection regulations.

Certain businesses, particularly larger entities, must conduct annual audits and file financial reports with the relevant authorities.

6. Penalties for Non-Compliance

The UAE enforces strict penalties for failing to comply with tax and regulatory requirements. Late or inaccurate VAT returns can result in fines and interest charges.

Businesses that fail to file corporate tax returns on time or underreport taxable income may face financial penalties and audits from the Federal Tax Authority (FTA).

Following regulations closely also helps businesses stay on top of key tax deadlines.

Key Deadlines to Remember

Meeting tax deadlines allows you to stay compliant and avoid penalties. The main deadlines cover VAT, corporate tax, employee-related filings, and financial reporting. Here are the key timelines every business should keep in mind:

VAT Filing Deadlines

VAT-registered businesses must file returns either quarterly or annually, depending on their registration. The deadline for filing:

- Quarterly VAT Filings: Returns are due within 28 days after the quarter ends.

- Q1 (January–March): Due April 28

- Q2 (April–June): Due July 28

- Q3 (July–September): Due October 28

- Q4 (October–December): Due January 28

- Annual VAT Filings: For businesses on an annual cycle, returns are due within 28 days after the end of the tax year.

Missing deadlines can result in penalties and interest charges.

Corporate Tax Filing Deadlines

Businesses subject to corporate tax must file returns within nine months of the financial year-end. For example, if the financial year ends on December 31, the return is due by September 30 of the following year.

Corporate tax payment is due at the same time as filing. Businesses should ensure funds are available to avoid late fees.

Employee-Related Deadlines

Companies must also track deadlines linked to employee benefits and payroll. End-of-service benefits must be accurately calculated and accounted for by the end of the tax year. Payroll taxes and contributions must be filed on time as per the UAE Ministry of Labour’s requirements.

Audit and Financial Reporting Deadlines

Some businesses are required to conduct annual audits and submit financial statements. Audit reports must be completed and filed within 3–6 months after the financial year-end, depending on company requirements.

Staying on Track

Automated reminders through accounting software or working with tax professionals can help businesses manage deadlines efficiently. Regular consultation with tax advisors also ensures filings are accurate and up to date.

How Alaan Can Help with End-of-Year Tax Planning?

End-of-year tax planning often feels complex, especially with corporate tax and VAT requirements in the UAE. At Alaan, we make it easier with our AI-powered platform that helps businesses optimise tax strategies and stay compliant. Here’s how Alaan helps:

- Automated Tax Calculation: Alaan takes the complexity out of tax reporting by automating VAT and corporate tax calculations. This ensures filings are accurate, timely, and free from manual errors, reducing risk while keeping your business fully compliant with UAE regulations.

- Real-Time Financial Tracking: Stay on top of your finances with real-time insights that make it easier to forecast tax obligations and maximise year-end deductions. With greater visibility, you can plan ahead and make more informed decisions.

- Smooth Integration with Accounting Software: Alaan connects smoothly with accounting tools like QuickBooks, Xero, and Oracle NetSuite. This integration keeps your financial records up to date, simplifies reporting, and eliminates the need for manual data entry.

- Customisable Spend Limits: Set tailored spending controls to match your business needs. These limits support VAT compliance, prevent unauthorised expenses, and ensure your financial policies are followed while optimising tax savings.

- AI-Powered Efficiency: Alaan’s AI speeds up everyday financial tasks like receipt matching and expense categorisation while detecting errors early. This saves your team valuable time and allows them to focus on strategy.

With Alaan, end-of-year tax planning becomes a seamless process, helping you stay compliant, reduce liabilities, and focus on growing your business with confidence.

Wrapping Up

End-of-year tax planning is essential for UAE businesses to stay compliant and strengthen financial performance in 2026. Reviewing financial statements, maximising deductions, and staying updated on regulations can help reduce tax liabilities and improve cash flow.

At Alaan, we know how important efficient tax planning is, which is why our AI-powered platform is designed to make the process easier. From simplifying expense tracking to integrating with accounting systems and ensuring compliance, we help businesses save time, cut down on errors, and stay in control.

Book a quick demo today and see how Alaan can support your tax strategy and enhance overall business efficiency.

FAQs

1. What government incentives can businesses take advantage of in 2026?

In the UAE, sectors like R&D, sustainability projects, and investments in free zones often come with tax incentives. By using these opportunities, businesses can lower their overall tax burden while supporting growth initiatives.

2. Why is reviewing financial statements important at the end of the tax year?

Looking over profit and loss statements, balance sheets, and cash flow reports helps businesses spot areas for improvement. It also gives a clear picture of financial performance, supporting smarter decisions for the year ahead.

3. What impact do free zones have on end-of-year tax planning?

Companies operating in UAE free zones can benefit from tax exemptions or reduced rates, but they must follow specific operational rules. Understanding these requirements helps businesses make the most of tax advantages before the year closes.

4. How can businesses manage cash flow with upcoming tax payments?

Setting aside funds throughout the year for taxes helps avoid cash flow crunches. Forecasting tax obligations ensures businesses have enough liquidity to cover payments on time without disrupting operations.

5. How can businesses reduce tax liability through charitable donations?

Donations made before year-end are often tax-deductible, lowering taxable income. By planning charitable contributions strategically, businesses can support the community while improving their tax position.