A payment can leave the sender’s account and still create work for the recipient. The problem is not always whether money was sent. It is often whether the receiving finance team can tell what the payment covers, which invoice it belongs to, or whether one transfer is clearing several items at once. That is where remittance advice matters. It acts as the information layer between payment initiation and payment allocation, helping the receiving side apply funds faster and with less ambiguity. It is especially useful for large payments, urgent settlements, international transfers, and combined payments, and it is generally used as an operational courtesy rather than a mandatory requirement.

For finance teams, that makes remittance advice far more practical than the term sometimes suggests. It is not just a banking label. It is a reconciliation tool. When payment context is weak, accounts receivable teams spend more time chasing references, accounts payable teams field unnecessary queries, and cash application slows down for reasons that have nothing to do with whether the payment itself was made.

This article explains what remittance advice is, what details it should include, how it differs from proof of payment, and why it helps businesses reconcile payments faster.

TL;DR / Key Takeaways

- Remittance advice provides context for a payment, helping recipients understand what it covers before reconciliation.

- It is most useful for combined payments, international transfers, and situations where bank references are not enough.

- Poor remittance advice usually fails due to missing invoice details, late delivery, or a weak reference structure.

- Strong handling reduces manual reconciliation, follow-ups, and payment allocation errors. Alaan helps finance teams keep payments, approvals, and supporting documents connected, making transaction tracking and reconciliation easier.

Also read: Understanding the procure-to-pay process

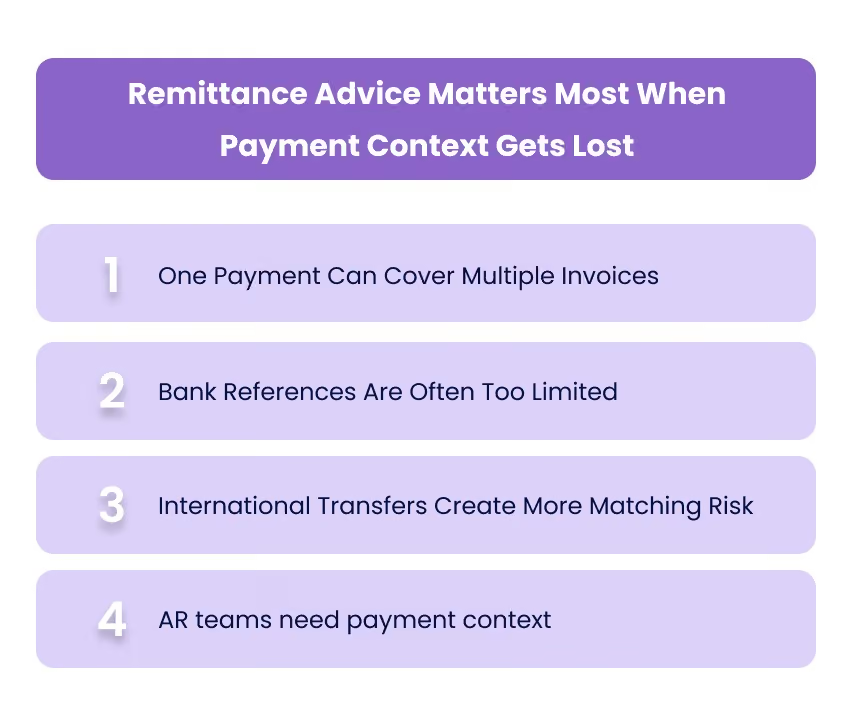

Remittance Advice Matters Most When Payment Context Gets Lost

The value of remittance advice becomes obvious when a payment reaches the bank account but does not arrive with enough context to be applied cleanly.

One Payment Can Cover Multiple Invoices

This is one of the most common scenarios. A business sends a single transfer to settle several invoices, but the receiving side still needs invoice-level detail to allocate the amount accurately. Without that detail, the payment exists, but reconciliation slows down because the recipient has to infer what was cleared and what remains open.

Bank References Are Often Too Limited

A transfer reference can help, but it is rarely enough on its own. References are often abbreviated, inconsistent, or too short to carry the full payment story, especially where multiple invoices, internal coding, or partial settlements are involved. That leaves the receiving team with a payment record, but not enough clarity to match it confidently.

International Transfers Create More Matching Risk

Cross-border payments introduce more room for ambiguity because routing details, currencies, value dates, and intermediary processing can all add complexity. When the payment route is less direct, clear remittance detail becomes more valuable on the receiving side because it helps identify what the funds are intended to settle before the full bank trail is obvious.

AR Teams Need Payment Context Before Cash Is Fully Allocated

A receivable is not operationally closed just because funds are expected or have landed. The receiving finance team still needs to know how to apply the amount in the ledger. That is exactly the gap remittance advice helps close.

Related: AP automation and accounts payable systems

What Remittance Advice Actually Tells The Recipient

A good remittance advice should answer a very simple question quickly: what exactly is this payment for?

At its best, it tells the recipient that payment has been initiated or sent, how much is being paid, which invoice or invoices the transfer relates to, and whether any discount, deduction, or partial settlement affects the amount. That lets the receiving finance team move from uncertainty to application much faster. Common remittance advice content includes invoice references, payment amount, payment date, payer and payee information, payment method, and any deductions or settlement notes.

In practical terms, the recipient should be able to see:

- Who Sent The Payment

- Who The Payment Was Sent To

- How Much Was Paid

- When The Payment Was Made Or Initiated

- Which Invoice Or Invoices It Covers

- Whether Any Discount, Deduction, Or Partial Settlement Applies

- Which Reference Should Be Used For Matching

That is why remittance advice is best understood as payment context rather than payment proof. Its role is to make the payment easier to identify and easier to apply before manual follow-up starts.

What A Good Remittance Advice Should Include

A remittance advice does not need to be long to be useful, but it does need to be specific. The main objective is to remove uncertainty at the point where the recipient is trying to match money received to open items.

The core fields usually include:

- Payer Name

- Payee Name

- Payment Date

- Payment Amount

- Invoice Number Or Numbers

- Invoice Date

- Reference Number

- Currency

- Discounts Or Deductions

- Partial Payment Note, If Relevant

- Payment Method Or Bank Reference

Those fields matter because they reduce the most common sources of payment confusion: unclear invoice coverage, missing references, and unexplained differences between invoice value and transfer value.

A strong remittance advice is not about formality. It is about speed of understanding. The faster the recipient can identify what the payment is doing, the less reconciliation friction the transaction creates.

Related: Receipt scanning methods for efficiency

Where Remittance Advice Fits In The Payment Workflow

Remittance advice is most useful when it is treated as part of the payment workflow rather than an afterthought sent later.

In a typical business-payment sequence, the invoice is issued first, the payment is then initiated, remittance advice is sent with the relevant payment detail, and the recipient uses that information to match the transfer to open invoices before reconciliation is completed. The operational value sits in that middle step. It gives the recipient context before cash application becomes manual.

This is also why remittance advice should not be confused with other payment-related documents. It does not replace the invoice, and it does not function as final evidence of payment completion. Its specific role is to bridge the communication gap between the sending of funds and the receiving team’s allocation of those funds.

Also read: Reconcile in accounting: understanding the process

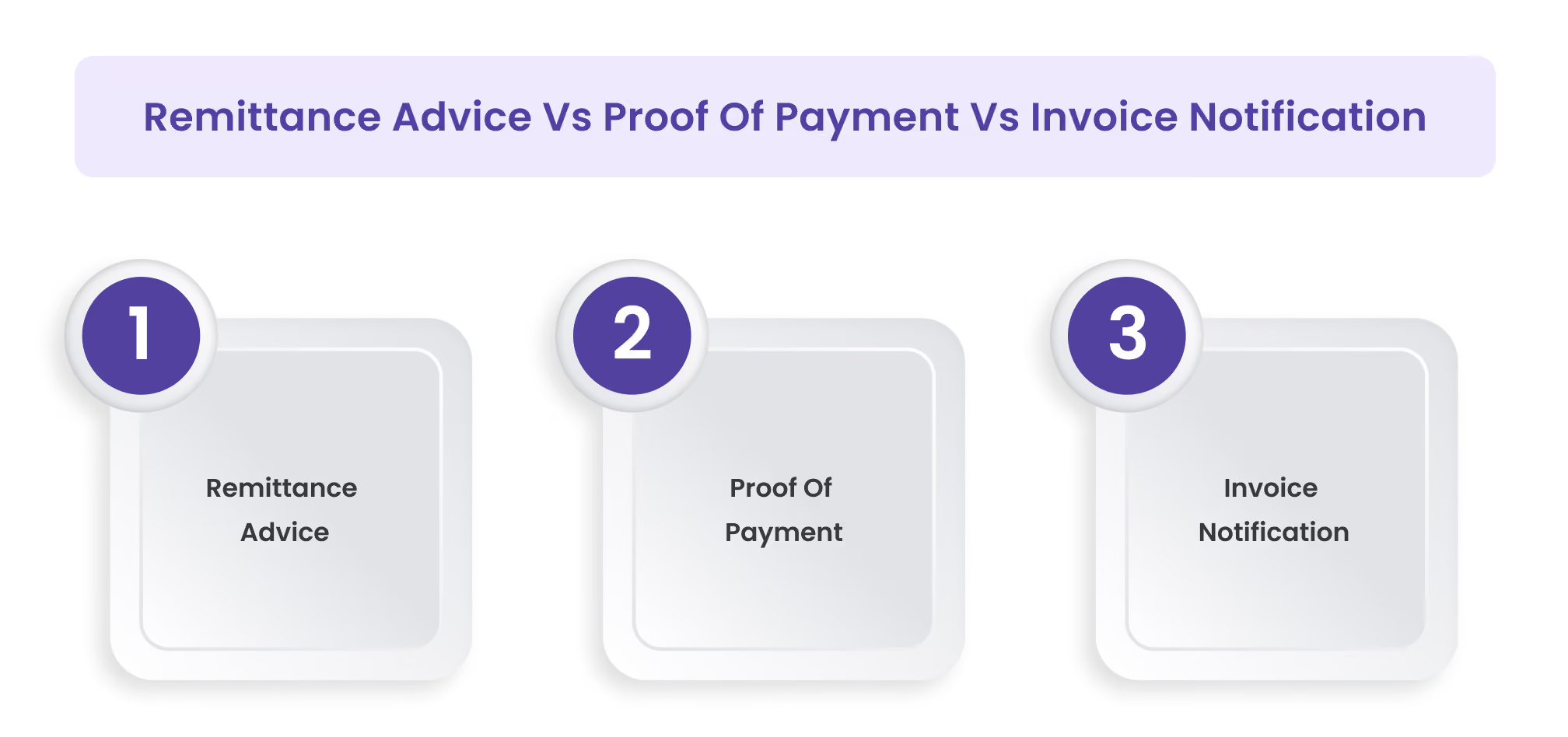

Remittance Advice Vs Proof Of Payment Vs Invoice Notification

These terms are often used loosely, but they do different jobs.

Remittance Advice

Remittance advice is a payment notice. It tells the recipient that a payment has been sent or initiated and explains what that payment relates to. Its value lies in helping the recipient allocate the amount correctly. It is generally used as a practical courtesy rather than a legal requirement in normal business payments.

Proof Of Payment

Proof of payment is confirmation that the payment has actually been made. It is evidence of the transfer itself rather than a communication tool for invoice allocation.

Invoice Notification

Invoice notification belongs at the billing stage. It tells the customer that an invoice has been issued or is due. It does not explain that payment has been sent against that invoice.

This distinction matters because finance teams often assume a bank confirmation or invoice email already solves the same problem. In many cases, it does not. One confirms payment, one announces billing, and one explains what the payment is intended to settle.

Related: Efficient financial statement preparation guide

Why Remittance Advice Still Matters In Cross-Border And Bank-Routed Payments

Even where payments are fully digital, bank-routed transfers still depend on accurate instruction data, beneficiary details, account references, and transfer-purpose information. In the UAE, outward and inward remittance processes continue to rely on structured banking fields such as beneficiary name, beneficiary account details, bank-routing information, value date, and transfer-purpose inputs, and some payment instructions can be rejected or delayed if critical details such as IBAN or valid transfer purpose are missing.

That is exactly why remittance advice remains useful. It does not replace the banking instruction itself, but it gives the receiving side a cleaner way to understand what the payment is meant to settle, especially where multiple invoices, currencies, or references are involved. In cross-border and bank-routed environments, that extra clarity can significantly reduce the time spent on matching and follow-up.

Also read: Trade finance automation solution process

Where Finance Teams Usually Get Remittance Advice Wrong

Remittance advice is simple in theory, but it often fails in execution. The issue is rarely the absence of a payment notice. It is the absence of useful detail at the moment it is needed.

Sent Too Late To Be Useful

Remittance advice should arrive alongside the payment, not after the recipient has already started investigating it. When it is delayed, finance teams still end up chasing references and reconciling manually.

Missing Invoice-Level Detail

One of the most common issues is sending a payment confirmation without specifying which invoices are being settled. This is especially problematic when a single transfer covers multiple items.

Combined Payments Without Allocation Breakdown

When businesses bundle several invoices into one payment but do not include a clear breakdown, the receiving side is forced to interpret the allocation. That introduces delays and increases the risk of misapplication.

Treating Bank Reference As Sufficient

Payment references alone are rarely enough, particularly when they are abbreviated, internal, or inconsistent. Without structured detail, the reference does not reduce reconciliation effort.

Not Storing It With The Transaction Record

Even when remittance advice is sent correctly, it often lives in email threads instead of being attached to the transaction record. That weakens traceability and makes future reviews or audits more difficult.

Also read: Corporate card reconciliation guide

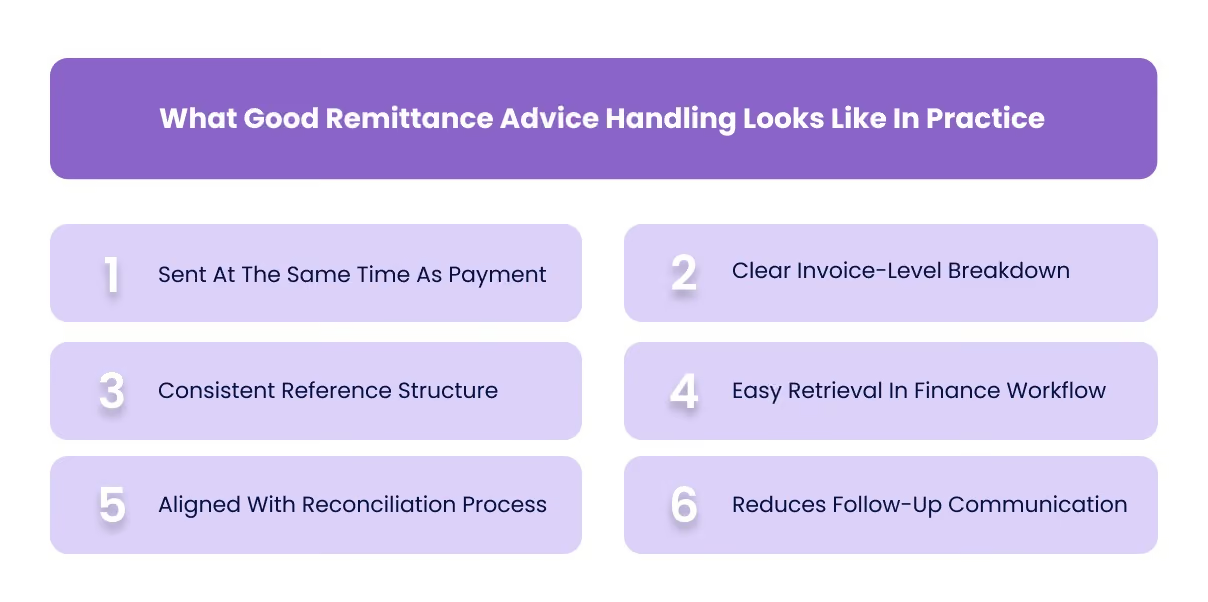

What Good Remittance Advice Handling Looks Like In Practice

Well-managed remittance advice does not create extra work. It removes it. In practice, strong handling looks like this:

- Sent At The Same Time As Payment

The recipient receives context before or alongside the funds, not after. - Clear Invoice-Level Breakdown

Each invoice covered by the payment is listed explicitly, including partial settlements where applicable. - Consistent Reference Structure

Payment references align with invoice identifiers and remain usable across systems. - Easy Retrieval In Finance Workflow

The remittance advice is stored with the transaction, not buried in inboxes. - Aligned With Reconciliation Process

The information provided matches how the receiving team actually applies and clears payments. - Reduces Follow-Up Communication

The recipient does not need to ask what the payment relates to.

When handled this way, remittance advice becomes part of a clean payment process rather than an additional step.

Related: Automated account reconciliation benefits steps

How Alaan Helps Keep Payment Documentation Clear And Traceable

Remittance advice solves one part of the payment-context problem. Finance teams still need approvals, invoices, receipts, and transaction records to stay connected in one place.

That is where execution systems matter.

Alaan helps finance teams keep payment-related documentation structured, visible, and easier to retrieve across the full spend workflow.

- Approval Visibility Before Money Moves

Transactions can be routed through approval workflows before spend happens, which ensures that payments are tied to approved business activity rather than reviewed after the fact. - Receipt And Invoice Capture

Invoices and receipts are captured and linked directly to transactions, reducing fragmented documentation and making it easier to understand what each payment relates to. - Real-Time Spend Visibility

Finance teams can see where money is moving across teams, vendors, and categories, which improves context around outgoing payments and reduces surprises. - Cleaner Accounting Sync

Integrations with systems like Xero, QuickBooks, NetSuite, and Microsoft Dynamics help transaction data flow into accounting systems more cleanly, reducing reconciliation friction. - Better Audit And Retrieval Readiness

When approvals, transactions, and supporting documents are connected, finance teams can retrieve payment context quickly without relying on scattered records.

Conclusion

Remittance advice is not a complex concept, but it solves a very practical problem. Payments without context create unnecessary friction between sending and receiving teams. The issue is rarely whether money moved. It is whether the movement can be understood quickly and applied correctly.

That is why remittance advice still matters. It reduces ambiguity, speeds up allocation, and helps finance teams close transactions without avoidable follow-up.

For businesses handling multiple invoices, cross-border transfers, or high transaction volumes, that clarity becomes even more important. Without it, reconciliation slows down, communication increases, and the same payment requires more effort than it should.

And beyond remittance advice, the broader challenge remains the same: keeping payment activity, approvals, and documentation connected. That is where Alaan helps finance teams maintain cleaner, more traceable spend workflows. Book a demo to see how Alaan helps reduce friction across payments, documentation, and reconciliation.

FAQs

1. What Is Remittance Advice In Simple Terms?

Remittance advice is a payment notice sent by the payer to explain what a payment is for. It typically includes invoice references, amounts, and payment details to help the recipient apply the payment correctly.

2. Is Remittance Advice Mandatory?

In most business cases, remittance advice is not mandatory. It is used as a best practice to improve clarity and reduce reconciliation effort.

3. What Should Be Included In Remittance Advice?

It should include payer and payee details, payment amount, date, invoice references, and any adjustments such as discounts or partial payments.

4. What Is The Difference Between Remittance Advice And Proof Of Payment?

Remittance advice explains what a payment relates to, while proof of payment confirms that the payment has been completed.

5. When Should Remittance Advice Be Sent?

It should be sent at the same time as the payment or immediately after initiation so the recipient has context before reconciliation begins.

6. Does Remittance Advice Help With Reconciliation?

Yes. It reduces ambiguity, helps match payments to invoices faster, and minimises follow-up communication between finance teams.