UAE businesses and residents regularly send money to the United States, paying suppliers, settling USD-denominated SaaS invoices, funding operations, or transferring personal funds. These flows sit within a much larger outbound payments ecosystem: the UAE’s cross-border remittance market is valued at roughly $39 billion annually (≈ AED 143 billion), reflecting its position as one of the world’s major money-sending hubs.

The economic linkage between the two markets reinforces this activity. The United States imported approximately $7.8 billion worth of goods from the UAE in 2024 (≈ AED 28.6 billion), illustrating the depth of commercial interaction that frequently requires cross-border settlement.

While the mechanics of sending funds are typically straightforward, execution outcomes vary when beneficiary instructions are incomplete, charges are misunderstood, or compliance reviews intervene. This guide focuses on operational realities, choosing the right payment rail, preparing US bank identifiers correctly, and avoiding workflow gaps that lead to delays or unexpected deductions.

TL;DR

- International wires are governance tools, not just payment channels. Their primary value lies in traceability, dispute resolution capability, and audit defensibility rather than execution convenience.

- Routing identifiers drive execution reliability. Accurate capture of US wire instructions, especially routing frameworks and institutional identifiers, is the single largest controllable factor affecting settlement success.

- Charge selection shapes commercial outcomes. Fee responsibility choices influence supplier relationships, reconciliation clarity, and variance handling, making them financial decisions rather than administrative toggles.

- Landed-value thinking prevents reconciliation friction. Capturing expected credit value and routing assumptions at approval reduces downstream disputes and variance investigation workload.

- Payment performance improves when embedded in spend control workflows. Integrating invoice capture, approvals, and execution, as enabled through platforms like Alaan, reduces fragmentation and prevents international transfers from becoming month-end exception handling exercises.

Quick Decision Guide

Use this as a simple starting point.

- Bank Wire Transfer (SWIFT)

Best for higher-value payments, supplier invoices, and anything that needs a clean audit trail. - Bank Digital International Transfer

Best for routine transfers where you still want bank rails but prefer app-based execution. - Money Transfer Operators

Best for personal transfers or situations where the recipient prefers consumer-first flows and dedicated tracking references.

What You Need Before You Start

Most “failed transfers” are just bad inputs. For US destinations, the same two issues come up repeatedly: missing routing identifiers and incomplete recipient/bank details.

Recipient And Bank Details To Collect

For a US bank deposit, you typically need:

- Beneficiary full legal name (as per bank account)

- Beneficiary address

- Beneficiary account number

- Receiving bank name and address

- SWIFT/BIC code (commonly used for international wires)

- ABA routing number (often requested in US wire instructions)

A US ABA routing number is a nine-digit institution identification number used to route payment transactions and identify institutions in the Federal Reserve system.

US banks can request different identifiers depending on whether the payment is routed as an international wire (SWIFT/BIC) or handled via domestic wire frameworks (ABA/RTN). Many banks publish this distinction clearly in their wire instructions and FAQs.

Charges And Who Pays Them

When sending an international bank transfer, you may be asked to choose how charges are handled:

- BEN: beneficiary bears charges (deductions reduce the credited amount)

- SHA: charges are shared

- OUR: sender pays charges, but a full receipt is not always guaranteed in countries without a charge-back system, such as the USA

This behaviour is explicitly described in the UAE bank transfer guidance, including the US exception.

Also Read: Building a Robust Cash Management Control System for UAE Businesses

Main Payment Methods Used by UAE Businesses

UAE organisations sending funds to India typically rely on three established routes. Each is shaped by different operational characteristics: traceability depth, cost transparency, and documentation expectations, rather than simply execution convenience. Understanding these distinctions helps finance teams choose deliberately rather than defaulting to familiar channels.

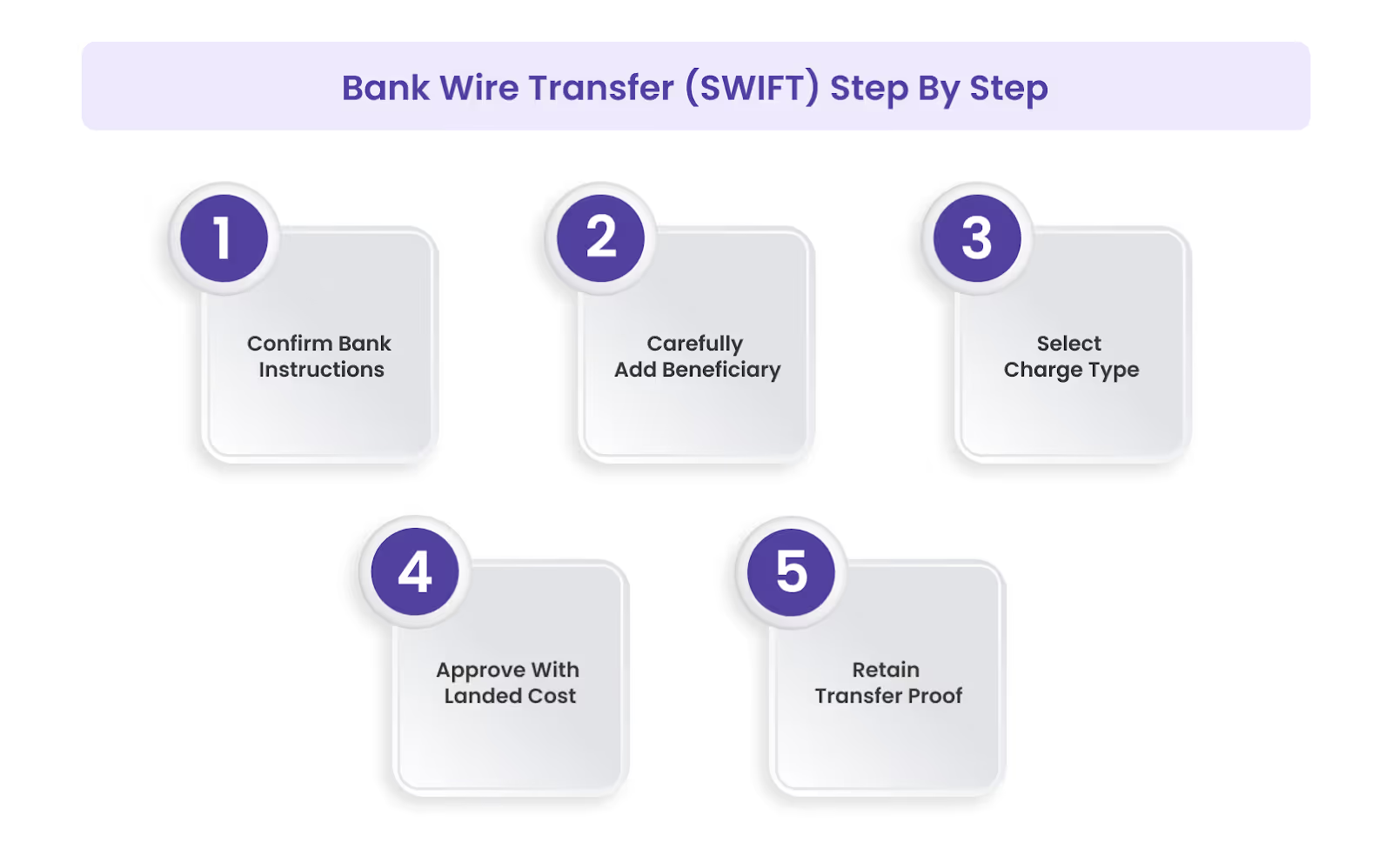

1. Bank Wire Transfer (SWIFT) Step By Step

For most UAE finance teams, a bank wire is the default method for paying US vendors because it creates a clean audit trail and supports formal proof of payment when needed.

How The Payment Typically Moves

A UAE bank processes your transfer as an international payment and routes it through correspondent and intermediary banks where required. That routing can affect timing and deductions, which is why two identical transfers can settle differently depending on the banks involved.

Steps To Execute A Clean UAE To USA Wire

- Confirm The US Bank Instructions Before You Touch The Bank Portal

US beneficiaries often provide “wire instructions” that specify exactly what identifiers must be used (SWIFT/BIC, ABA routing number, bank address, and sometimes an intermediary path). Treat this as the source of truth to prevent rejections and repair fees. - Add The Beneficiary Carefully

Use the beneficiary’s full legal name, account number, receiving bank name, and bank address. For US destinations, routing identifiers frequently include an ABA routing number, which is a nine-digit institution identifier used for routing in the US. - Choose The Charge Type Intentionally

You’ll typically see BEN, SHA, or OUR. This determines who bears fees and influences whether the recipient gets the full USD amount. Some banks explicitly flag that even with OUR, a full receipt is not always guaranteed in countries without a charge-back system, such as the USA. - Approve With Landed Cost Captured

At approval time, record: AED debited, expected USD credited, FX rate shown, charge type, and transfer reference. This prevents “we don’t know why it doesn’t match” during close. - Retain Transfer Proof

Keep the transfer reference and the transaction advice/confirmation record. This is what resolves vendor disputes quickly when a US recipient claims non-receipt or delayed credit.

Fees And FX Costs To Compare

The cost of a UAE→USA transfer is rarely just “the fee.” For USD wires, the two cost drivers that matter are FX spread and fees applied along the chain.

What Often Changes The Final USD Credited

- FX Spread Embedded In The Rate

A “low fee” transfer can still be expensive if the conversion rate is meaningfully off the market rate. The operational fix is simple: treat the FX rate as part of the cost, not a background detail. - Chain Fees And Deductions

When payments route through correspondent/intermediary banks, additional charges can apply, especially for SWIFT transfers. Some banks publish separate guidance noting that additional charges may apply where intermediaries are involved. - BEN, SHA, And OUR Behaviour

Charge type determines whether deductions happen to the delivered USD amount. “OUR” helps reduce surprises, but it is not a guarantee of full receipt for every destination. The USA is explicitly called out as a market where charge-back handling can differ, affecting net receipt.

A Simple Example Finance Teams Actually Use

If a supplier invoice is USD 10,000 net, you approve the payment using OUR and capture “expected USD credited = 10,000.” If the payment chain still deducts charges, the supplier may receive less than 10,000, creating a short-pay dispute and rework. The control is to (a) choose the right charge type, and (b) confirm whether your bank can evidence expected net credit for the corridor based on routing and fee handling.

Also Read: Cash Flow Optimisation Strategies for UAE Businesses in 2025

3. Bank Digital International Transfers

For routine UAE→USA payments, many teams still use bank rails but prefer a digital flow because it reduces manual entry, creates repeatable beneficiary templates, and keeps approvals cleaner inside the organisation.

Where Digital Transfers Fit Best

- Recurring vendor payments (monthly SaaS invoices, retainer-based agencies, contractor payments)

- Lower operational risk through saved beneficiary profiles and reduced re-keying

- Better cost predictability when the app shows live rates and the total cost before you confirm

What Not To Assume

Some banks market fee benefits for mobile-led international transfers, but these are still subject to eligibility, channel rules, and product terms. Treat “no fees” as a product condition to verify, not a default expectation.

Also Read: Simple Steps to Track and Manage Business Expenses

4. Money Transfer Operators

Money transfer operators are often the most straightforward option for personal remittances and situations where the recipient wants consumer-first delivery modes (including cash payout in supported markets). For business payments, they are typically used only when a vendor explicitly accepts that method, and you can still maintain documentation discipline.

When They Make Sense

- Personal transfers where speed and simple tracking matter

- Recipient-led preferences (the receiver wants a specific channel)

- Situations where you need a clear consumer tracking reference for confirmation and follow-up

What To Expect In Practise

After you pay and send, you receive a tracking number (MTCN) and can use it to track the transfer status. Keep that reference stored like you would store a bank transfer reference, especially if you need proof for follow-up.

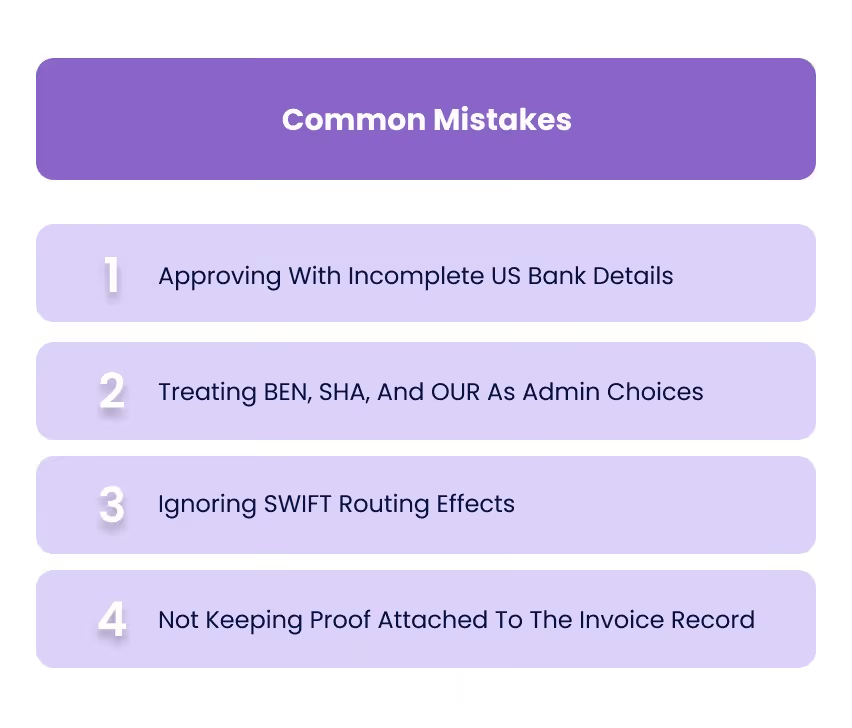

Common Mistakes When Sending Money From The UAE To The USA

Most delays, short-credits, and supplier escalations come from predictable mistakes. Fixing them is less about “better rails” and more about input control and approvals.

1. Approving With Incomplete US Bank Details

US wire instructions often require a combination of identifiers (commonly SWIFT/BIC and, depending on the bank’s setup, an ABA routing number). Missing bank address details or using the wrong routing framework can trigger repair, delays, or rejections.

2. Treating BEN, SHA, And OUR As Admin Choices

Charge type is a financial decision because it changes the net amount credited. Selecting OUR reduces deductions risk, but it does not guarantee full receipt in every destination corridor; the USA is explicitly called out as an exception in some UAE banking guidance.

3. Ignoring SWIFT Routing Effects

SWIFT-routed transfers may incur additional fees depending on routing. This becomes visible when a payment is credited short, or when a finance team tries to reconcile expected USD versus received USD without having captured the fee responsibility and expected landed value at approval time.

4. Not Keeping Proof Attached To The Invoice Record

Operationally, the fastest way to resolve “not received” disputes is to have a single record that includes the invoice, approval, transfer reference, and the transaction advice. Banks can provide transaction advice for international SWIFT transfers, which helps close investigations quickly.

Also Read: Importance and Steps in Account Reconciliation

Compliance And Documentation Reality

Cross-border transfers from the UAE can trigger verification checks even when the payment is legitimate. This is normal. UAE-regulated institutions are required to ensure that specific originator and beneficiary information accompanies money transfers, and gaps in that information can result in delays or requests for clarification. (rulebook.centralbank.ae)

In practical terms, the payments most likely to get queried are first-time transfers to a new beneficiary, higher-value payments, and transactions where the stated purpose does not align cleanly with the supporting documents. The best way to reduce friction is to keep beneficiary details accurate, use consistent payment references, and ensure invoice narratives match the reason for payment.

On the receiving side, beneficiary institutions have requirements to identify transfers that lack required information and take risk-based action, which can include holding a transfer pending clarification. (rulebook.centralbank.ae)

Also Read: Creating a Sample Business Expense Policy with Guidelines and Examples

Where Alaan Fits For UAE To USA Business Payments

Sending money to the United States is rarely difficult at the execution stage. The friction usually comes earlier or later, invoices arriving across channels, rushed approvals, payment execution inside separate banking tools, and reconciliation rebuilt from references afterwards. This fragmentation creates short-credit disputes, duplicated effort, and delayed close cycles.

At Super Pay, Alaan, we approach cross-border supplier payments as part of a governed workflow that connects invoice capture, approval discipline, execution visibility, and accounting continuity.

- Invoice Capture And Validation Before Scheduling Payment

Invoices are collected centrally and reviewed before any transfer is scheduled. This helps ensure beneficiary details, supporting documentation, and payment intent are validated early, reducing errors that commonly cause routing delays or repair requests when sending funds to US accounts. - Approval Structure That Separates Spend Legitimacy From Timing

Invoice approval and payment approval are handled as separate steps. Operational teams confirm the validity of the expense, while finance teams determine when funds should be released. This reflects how UAE finance teams manage supplier settlements and support clearer cash-flow control. - Transfers Executed Within Supported Corridors

For supplier or vendor payments requiring bank-style settlement, transfers can be executed within supported corridors, including the United States. Payments occur within the same environment used for approvals, keeping documentation and references connected instead of shifting between systems. - Cost Visibility Prior To Approval

For supported international transfers, payment cost implications are visible before approval. This allows finance teams to evaluate expected impact before execution rather than resolving differences after settlement. - Connected Records For Reconciliation And Audit Trail

Invoices, approvals, and payment records remain linked and synchronise with accounting integrations. This reduces manual tracking and helps finance teams respond more quickly to supplier queries, internal reviews, or reconciliation checks.

By connecting upstream controls with transfer execution and record continuity, we help organisations send supplier payments internationally while maintaining visibility and documentation discipline across the full workflow.

Also Read: Understanding the Importance of Business Spend Management and Its Tools

Conclusion

Sending money from the UAE to the USA becomes predictable when the process is treated as a controlled workflow. The method you choose should match what you’re optimising for auditability, landed USD receipt, speed expectations, or recipient convenience, but the same fundamentals reduce issues across all rails: correct US bank instructions, intentional fee responsibility selection, capturing landed-cost inputs at approval, and retaining transaction advice for tracking and reconciliation.

At Alaan, we help UAE finance teams connect invoices, approvals, payments, and reconciliation in one governed workflow so international payments do not become a recurring month-end clean-up project. If you want to see how this works for supplier and vendor payments, book a demo with our team. Book A Demo Today!

FAQs

1. How Long Does It Take To Send Money From The UAE To The USA

International transfers typically take 1–5 business days, depending on cut-off times, routing, compliance checks, and the receiving bank’s processing windows.

2. What Is The Difference Between SWIFT, ABA, And IBAN For US Transfers

SWIFT/BIC identifies banks internationally, while ABA routing numbers (9 digits) identify US institutions for routing within US payment systems. The US generally does not use IBANs the way many other regions do, so wire instructions usually rely on SWIFT and/or ABA plus the account number.

3. Do I Need Both SWIFT And ABA To Send Money To A US Bank

Not always. Some US banks provide international wire instructions that require SWIFT/BIC, while others also require an ABA/Fedwire routing number as part of the routing details. The safest approach is to follow the beneficiary bank’s published wire instructions.

4. Can I Cancel Or Reverse A UAE To USA Transfer After Sending

Sometimes, but not reliably. Once an international wire is processed and credited, reversing it can be difficult and may depend on timing, intermediary status, and recipient bank cooperation. The practical control is to verify beneficiary details before you submit. (Bank process norms vary by institution.)

5. Why Does The US Recipient Sometimes Receive Less Than Expected

Common causes include fee responsibility selection (BEN/SHA/OUR), intermediary deductions in the routing chain, and the FX spread embedded in the applied rate. Even where “sender pays fees” is selected, net receipt can still vary by corridor and routing behaviour.

6. What Is The Cut-Off Time For International Transfers In The UAE

Cut-offs vary by bank and channel. Some UAE bank support pages publish operational cut-off times for foreign currency local/international transfers, which can determine whether a request is processed same-day or the next working day.