VAT refunds are no longer a back-office afterthought for UAE businesses. In 2026, they sit at the intersection of cash flow management, audit readiness, and VAT compliance.

According to the Federal Tax Authority, over AED 115.4 million in VAT refunds were processed in a single late-2025 cycle, reflecting both growing adoption and tighter verification standards. For finance teams, this means one thing: VAT refunds are accessible, but only when data, documentation, and filings are aligned.

This guide explains how to claim a VAT refund in the UAE for business purposes in 2026, including eligibility, the VAT311 process, common pitfalls, and how to strengthen refund readiness year-round.

Key Takeaways

- Approval depends more on accurate VAT data, compliant invoices, reconciliations, and year-round record discipline than on simply filing Form VAT311.

- Success hinges on clean VAT returns, consistent accounting records, penalty-free status, and well-organised supporting documentation.

- The 2026 shift to structured e-invoicing improves audit trails, minimises manual errors, and aligns transactions more closely with FTA expectations.

- Common blockers include non-compliant invoices, VAT mismatches, unpaid penalties, claiming non-recoverable VAT, and weak recordkeeping.

- Automated expense systems (such as Alaan) help keep transactions documented, categorised, and audit-ready, turning VAT refunds into a predictable working-capital lever rather than a reactive exercise.

VAT Refunds and Their Impact on Business Cash Flow in 2026

A VAT refund allows eligible businesses or individuals in the UAE to reclaim Value Added Tax paid on expenses when their input VAT exceeds output VAT for a given tax period. In simple terms, if you paid more VAT on purchases and business expenses than you collected from customers, the excess amount can be claimed back from the Federal Tax Authority (FTA).

In the UAE VAT system, registered businesses must file periodic VAT returns detailing sales, purchases, output VAT collected, and input VAT paid. After offsetting input VAT against output VAT, one of two outcomes applies:

- VAT payable: Output VAT is higher than input VAT, and the balance must be paid to the FTA.

- VAT refundable: Input VAT is higher than output VAT, and the excess amount becomes eligible for a refund.

A VAT refund is different from a routine VAT adjustment. Instead of merely reducing future VAT liability, a refund results in the excess VAT being returned to the taxpayer, improving cash flow.

Why VAT Refunds Are No Longer a Routine Compliance Task

For many UAE businesses, VAT refunds in 2026 are not about occasional recovery, but about ongoing working capital optimisation.

Who Can Claim a VAT Refund in the UAE

VAT refunds in the UAE are relevant mainly for VAT-registered businesses whose input VAT exceeds their output VAT for a given tax period.

- VAT-registered UAE businesses: Companies with an active TRN that file accurate VAT returns and hold FTA-compliant tax invoices can claim refunds using Form VAT311.

- Startups and scaling businesses: Businesses with high upfront costs, capital expenditure, or export-led models often generate excess input VAT, especially in early growth stages.

- Project-based or seasonal businesses: Companies with uneven revenue cycles, such as real estate, logistics, or hospitality, commonly experience refundable VAT positions.

- Non-resident businesses without a UAE establishment: Eligible foreign businesses may claim VAT refunds annually, subject to specific FTA conditions and documentation.

VAT Refunds and Business Registration Thresholds

For businesses, VAT refunds are closely tied to registration status. A company must register for VAT if its taxable supplies exceed the mandatory registration threshold of AED 375,000. Once registered, the business can offset input VAT against output VAT and claim refunds where applicable.

In practice, VAT refunds are most common for businesses with high upfront costs, export-heavy models, or seasonal revenue patterns. In 2026, ensuring refund eligibility is less about knowing the rule and more about maintaining clean data, valid tax invoices, and audit-ready processes throughout the year.

Also read: Simple Steps to Track and Manage Business Expenses

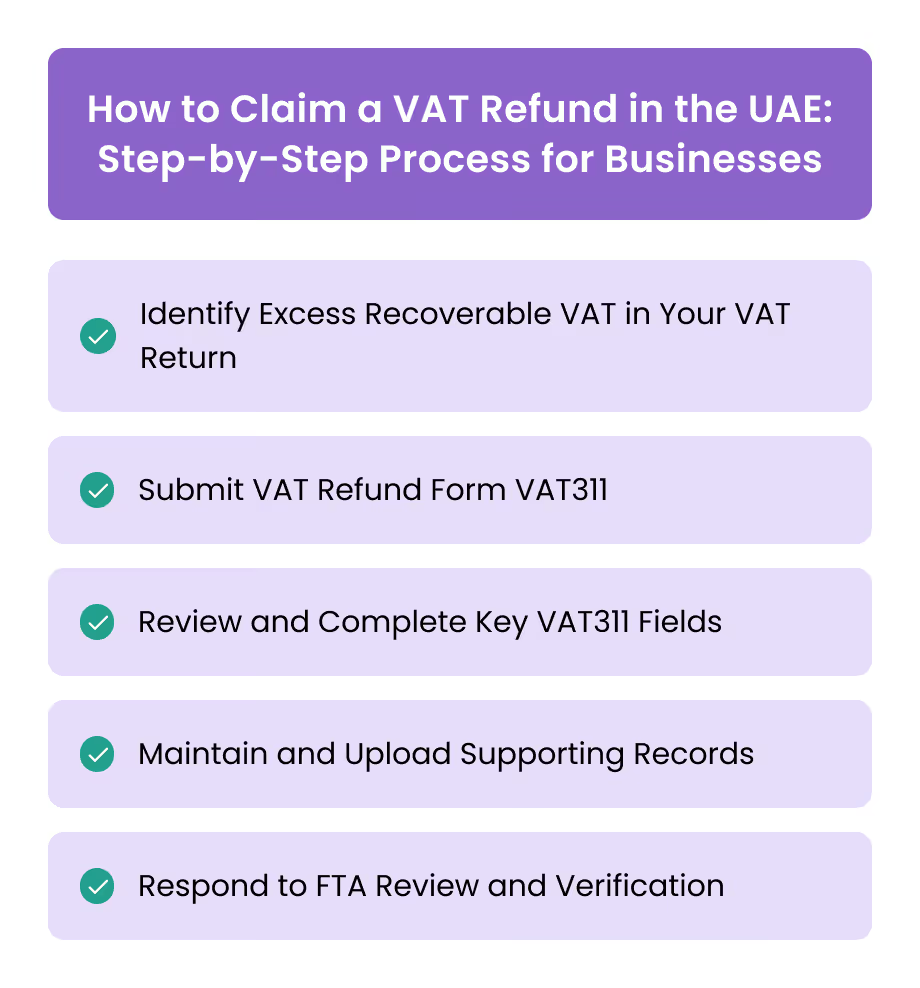

How to Claim a VAT Refund in the UAE: Step-by-Step Process for Businesses

For VAT-registered businesses in the UAE, claiming a VAT refund is a structured process managed through the Federal Tax Authority (FTA) via the EmaraTax portal. In 2026, the mechanics remain largely the same, but scrutiny around accuracy, penalties, and documentation is tighter, making precision essential.

Here’s a step-by-step process of how you can claim VAT refunds:

Step 1: Identify Excess Recoverable VAT in Your VAT Return

When filing your VAT return, the system automatically calculates whether your input VAT exceeds output VAT for the tax period.

If there is excess recoverable tax, you will see an option in Box 15 asking whether you wish to request a refund.

- Select “Yes” to initiate a refund request

- Select “No” if you prefer to carry the excess forward to offset future VAT liabilities or penalties

This choice matters. Once carried forward, the excess is not refunded unless you explicitly apply for it later.

Step 2: Submit VAT Refund Form VAT311

After submitting the VAT return, you must complete Form VAT311 to formally request the refund.

Process overview:

- Log in to the FTA EmaraTax portal

- Navigate to VAT → VAT Refunds

- Select VAT Refund Request

- Open and complete Form VAT311

Most fields are auto-populated based on your FTA profile and latest VAT returns, which makes profile accuracy critical.

Step 3: Review and Complete Key VAT311 Fields

While much of the form is automated, finance teams should carefully review the following sections:

- TRN and legal entity details: Pulled from your FTA profile; errors here can delay approval

- Total excess refundable tax (AED): Calculated from filed VAT returns, net of any administrative penalties

- Refund amount requested: Must be equal to or less than the eligible refundable balance

- Remaining excess refundable tax: Any balance not requested remains available for future periods

- Late registration penalty field:

- Zero if no penalty exists or if it has been paid

- AED 20,000 if a late registration penalty exists and remains unpaid

- Authorised signatory and declaration: Must be reviewed and confirmed before submission

Once complete, submit the form electronically.

Step 4: Maintain and Upload Supporting Records

Although VAT311 itself is concise, refund approval depends heavily on your underlying records. Businesses must maintain:

- Valid VAT tax invoices for all claimed input VAT

- Accurate records of taxable supplies and expenses

- Proper classification of VAT-recoverable and non-recoverable costs

In some cases, the FTA may request additional documentation to validate the claim, especially for higher-value refunds or recurring requests.

Step 5: Respond to FTA Review and Verification

After submission, the FTA reviews the refund request. During this stage:

- Additional information or clarification may be requested

- Delays often occur due to missing invoices, mismatched figures, or unresolved penalties

Once approved, the refund is processed, and you receive confirmation by email. Refund status and payment history can be tracked under My Payments → Transaction History in the portal.

Note: In 2026, VAT refunds are increasingly treated as an audit-linked process, not a standalone request. Clean filings, penalty-free accounts, and consistent documentation significantly reduce review time and improve approval confidence.

For finance teams, the real risk is not rejection, but delays caused by incomplete data or misalignment between VAT returns and refund applications.

To know more about VAT refunds, it is also advisable to go through the user guides of UAE Federal Tax Authority.

Common Pitfalls to Avoid When Claiming a VAT Refund in the UAE

Even when businesses are eligible for a VAT refund, applications are often delayed or rejected due to avoidable mistakes.

Understanding these pitfalls helps finance teams protect cash flow and reduce unnecessary follow-ups with the Federal Tax Authority:

Submitting Invoices That are Not VAT-Compliant

One of the most frequent issues is using receipts or invoices that do not meet FTA requirements. Missing supplier TRNs, incorrect VAT amounts, or simplified receipts where full tax invoices are required can invalidate input VAT claims.

Claiming VAT on Non-Recoverable Expenses

Not all VAT paid is refundable. Claiming VAT on blocked or restricted categories, such as certain entertainment, personal expenses, or non-business costs, increases the risk of refund rejection and further scrutiny.

Mismatches Between VAT Returns and Refund Forms

Differences between figures reported in VAT returns, Form VAT311, and accounting records often trigger reviews. Even small inconsistencies can delay processing while the FTA seeks clarification.

Ignoring Outstanding Penalties or Compliance Issues

Unsettled administrative penalties, particularly late registration penalties, can reduce refundable amounts or delay approvals. Applying for a refund without resolving these issues may lead to automatic deductions or rejection.

Poor Record Retention and Organisation

VAT refunds are assessed with audit-level scrutiny. Disorganised records, missing supporting documents, or unclear transaction trails make it difficult to substantiate claims when queried by the FTA.

Treating VAT Refunds as One-Off Events

Some businesses only focus on VAT compliance when applying for a refund. This reactive approach often exposes gaps in recordkeeping and reporting. VAT refunds work best when they are part of an ongoing, well-managed VAT process.

Delayed Responses to FTA Queries

Failure to respond promptly to information requests from the FTA can stall or cancel a refund application. Timely and accurate responses demonstrate compliance maturity and help keep the process moving.

Avoiding these pitfalls allows finance teams to approach VAT refunds as a predictable, controlled process rather than a high-risk, time-consuming exercise, particularly as VAT enforcement in the UAE continues to tighten.

Related: Deductible and Non Deductible Expenses Under UAE Corporate Tax

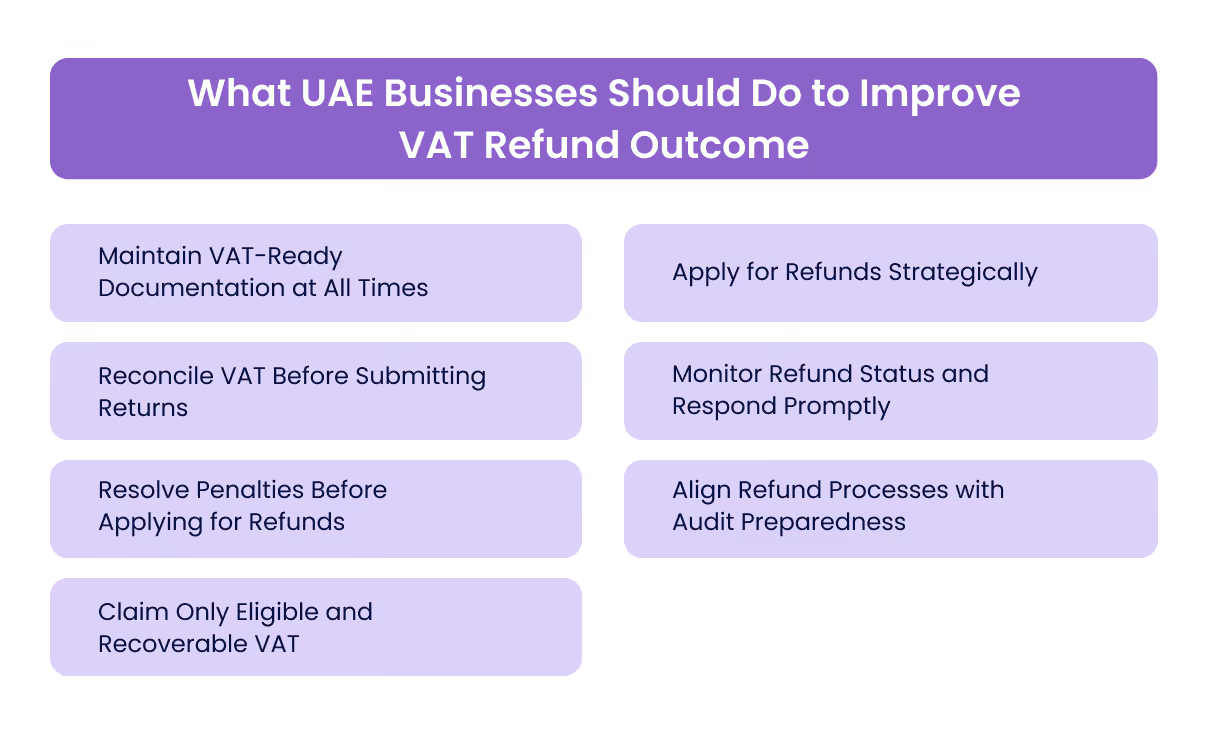

What UAE Businesses Should Do to Improve VAT Refund Outcome

Claiming a VAT refund is not just a compliance exercise; it is a test of how disciplined and audit-ready your finance processes are. Businesses that treat refunds as part of routine VAT management experience fewer delays and lower rejection risk.

Here are some of the best practices you can follow:

Maintain VAT-Ready Documentation at All Times

VAT refunds rely on the quality of your records. Ensure all input VAT claims are supported by valid tax invoices that meet Federal Tax Authority requirements, including supplier TRN, invoice date, taxable amount, and VAT charged. Incomplete or non-compliant invoices are one of the most common causes of refund delays.

Reconcile VAT Before Submitting Returns

Before filing your VAT return and requesting a refund, reconcile input VAT, output VAT, and general ledger balances. This helps identify mismatches early and prevents inconsistencies between VAT returns, refund forms, and accounting records, which may trigger FTA queries.

Resolve Penalties Before Applying for Refunds

Unpaid administrative penalties, particularly late registration penalties, can reduce or block refundable amounts. Settling penalties in advance avoids automatic deductions and improves the likelihood of a smooth refund process.

Claim Only Eligible and Recoverable VAT

Not all VAT paid is recoverable. Review expense categories carefully to exclude blocked or partially recoverable VAT, such as certain entertainment or personal-use costs. Over-claiming increases the risk of review and may delay approval.

Apply for Refunds Strategically

Businesses are not required to claim refunds every tax period. In some cases, carrying forward excess input VAT to offset future liabilities may be more practical. Consider cash flow needs, expected output VAT, and audit readiness before requesting a refund.

Monitor Refund Status and Respond Promptly

Once a refund request is submitted, track its progress through the EmaraTax portal and monitor FTA communications. Prompt responses to information requests reduce processing time and signal strong compliance practices.

Align Refund Processes with Audit Preparedness

Treat VAT refund requests as audit-triggering events. Ensure records are well-organised, approval trails are clear, and figures can be easily explained. This approach not only supports faster refunds but also strengthens your overall VAT compliance posture.

Automation closes the gap between policy intent and real-world behaviour by embedding controls directly into daily workflows.

To see how this works in practice, read how Washmen put its spend management on autopilot and saved 80+ hours per week using Alaan.

How Alaan Helps UAE Businesses Stay VAT-Ready for Refunds

Claiming VAT refunds in the UAE is not only about submitting Form VAT311. In practice, successful refunds depend on accurate records, VAT-compliant documentation, and consistent reporting across expense, accounting, and VAT returns. This is where many finance teams face friction as volumes grow.

Alaan supports UAE finance teams by strengthening the foundations that VAT refunds rely on.

As an AI-powered spend and expense management platform built for the UAE and wider MENA region, Alaan helps businesses maintain clean, compliant, and audit-ready VAT data throughout the spend lifecycle, rather than fixing issues only at refund time.

In practice, Alaan supports VAT refund readiness through:

- Corporate cards that create refund-ready transaction trails: Alaan’s corporate cards capture every business transaction digitally, making it easier to trace VAT-bearing expenses during VAT return reviews and refund submissions.

- Real-time expense capture with complete documentation: Expenses are recorded as they occur and linked with digital receipts through Alaan’s spend management workflows. This helps ensure that input VAT being claimed is supported by valid invoices when a VAT refund is requested.

- Receipt checks aligned with Federal Tax Authority expectations: Alaan helps finance teams review whether uploaded receipts include required VAT information such as supplier details, invoice dates, and VAT amounts, reducing the likelihood of input VAT being disallowed during refund assessment.

- Structured categorisation for accurate input VAT reconciliation: Expenses are categorised consistently, allowing finance teams to reconcile input VAT figures more easily with VAT returns and supporting documentation submitted with VAT311 refund forms.

- Accounting automation that reduces refund delays: Through accounting integrations, approved expenses flow into accounting systems with mapped categories, helping maintain consistency between expense records, VAT returns, and refund claims.

Together, Alaan’s corporate cards, spend management, and accounting automation help finance leaders approach VAT refunds with greater confidence, fewer documentation gaps, and stronger audit readiness.

For UAE businesses, this means VAT refunds are more likely to be processed smoothly, without last-minute data clean-ups or prolonged back-and-forth with the Federal Tax Authority.

Also read: Modern Expense Management Systems

Conclusion

A well-defined expense policy is critical for maintaining financial discipline, regulatory compliance, and consistency across an organisation. When reimbursement rules, approval thresholds, documentation standards, and VAT expectations are clearly set, finance teams reduce ambiguity and strengthen audit readiness.

That said, policies only work when they are embedded into everyday spending workflows. Manual reviews, delayed submissions, and fragmented systems often weaken enforcement and reduce visibility into real costs.

Alaan helps UAE businesses reinforce expense policies in practice through controlled corporate cards, automated expense capture, VAT-aware validation, and real-time spend visibility, giving finance teams stronger oversight with significantly less manual effort.

To see how Alaan can help your team apply expense policies with clarity and control, book a free demo today!

Frequently Asked Questions (FAQs)

1. How long does the FTA typically take to process a VAT refund?

VAT refund timelines vary depending on the completeness of documentation and whether the Federal Tax Authority requests additional clarification. In straightforward cases, refunds are usually processed within several weeks after submission. However, applications flagged for review or requiring supporting evidence may take longer, especially during peak filing periods.

2. Can VAT refunds be offset against future VAT liabilities instead of being paid out?

Yes. Businesses may choose not to request a cash refund and instead carry forward excess input VAT to offset future VAT liabilities. This option can be useful for companies with predictable output VAT or those aiming to reduce future payment obligations rather than receive a direct refund.

3. What happens if the FTA partially rejects a VAT refund claim?

If part of a VAT refund claim is rejected, the FTA will typically specify the reason, such as insufficient documentation or ineligible expenses. Approved amounts may still be refunded, while disallowed amounts can either be corrected in future returns or addressed through reconsideration or clarification if supporting evidence becomes available.

4. Are VAT refunds affected by errors in past VAT returns?

Yes. Inconsistencies between VAT returns, accounting records, and refund claims may trigger additional reviews or delays. If errors are identified, the FTA may request corrections or voluntary disclosures before processing the refund. Maintaining consistent records across reporting periods is critical for smoother refund outcomes.

5. Is there a deadline for claiming VAT refunds on excess input tax?

While excess input VAT can generally be carried forward, refund requests are tied to submitted VAT returns and subject to statutory time limits. Delaying refund claims for extended periods may increase the risk of documentation gaps or reconciliation issues, particularly during audits. Finance teams are advised to review excess VAT positions regularly rather than accumulating them indefinitely.