By introducing the Corporate Tax, the UAE Ministry of Finance aims to strengthen its status as a prominent global hub for business and investment. An important objective of this tax is to generate additional funds to drive economic growth and meet various public sector needs. The government aims to reaffirm its commitment to meeting international standards for tax transparency.

The new Corporate Tax rules, applicable for certain businesses, specify a 9% tax on the net profit shown in the company’s financial statements. This taxable profit refers to the income that the business earns after accounting for all applicable deductions and excluding exempted income. The rules allow for the reduction of any foreign taxes paid from the profit of corporations shown in the financial statement.

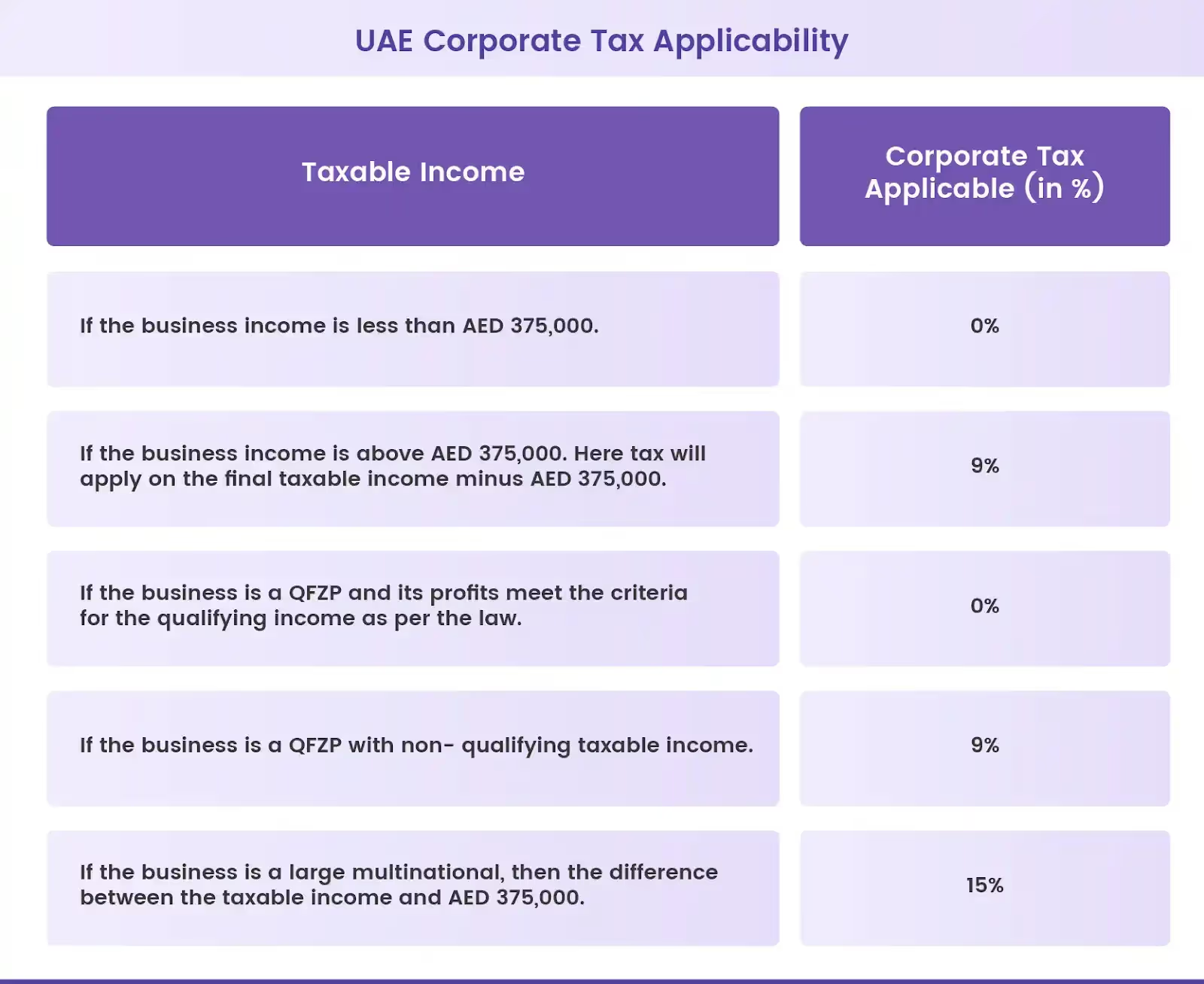

The Corporate Tax is applicable on taxable income exceeding AED 375,000 in a financial year. If your enterprise has earnings below this threshold, it will be subject to a 0% Corporate Tax rate.

Understanding how to calculate Corporate Tax can be a complex task, given the various factors and calculations involved. This blog aims to simplify this process and provide a detailed guide on how corporation tax is calculated in the UAE.

Calculating the UAE Corporate Tax manually can be tiresome and prone to errors. To make this process easier, use our Corporation Tax Calculator which is designed to provide accurate calculations, saving you time and effort.

Corporate Tax Framework in the UAE Explained

The Corporate Tax rate in the UAE is 9%, but the calculation is not as simple. This 9% Corporate Tax will only be levied if the taxable net profit exceeds 375,000 AED. In other words, net profits up to 375,000 AED is taxed at 0%.

The law also has specific provisions for businesses operating from free zones. If a taxpayer is classified as a Qualified Free Zone Person (QFZP), they would be subject to different tax rules. QFZPs enjoy tax benefits, including a 0% tax rate on qualifying income as per the criteria specified in the UAE CT law.

On the other hand, mainland businesses in the UAE are subject to a standard tax rate of 9% on their taxable income over AED 375,000. Unlike free zone companies, mainland companies can conduct business in the local market and internationally without restrictions.

Let’s understand the process of CT calculation with an example.

Consider the case of a company XYZ Corp. that operates in the UAE. For the financial year 2023-2024, XYZ Corp. reports a net profit of AED 500,000 in its financial statements. This is the amount calculated after all applicable deductions and excluding exempted income.

The first step to calculating the Corporate Tax is to determine if the company’s taxable income exceeds AED 375,000. In this case, XYZ Corp.'s net profit of AED 500,000 is higher than the exemption threshold.

Next, we subtract the threshold amount from the net profit to get the taxable income. So, for XYZ Corp., the taxable income would be AED 500,000 - AED 375,000 = AED 125,000.

Now, we apply the Corporate Tax rate of 9% to the taxable income. So, the Corporate Tax for XYZ Corp. would be 9% of AED 125,000, which equals AED 11,250.

Hence, XYZ Corp. is liable to pay a Corporate Tax of AED 11,250 for the financial year 2023-2024.

Consider Adjustments While Calculating Corporate Tax

When calculating Corporate Tax in the UAE, you need to consider certain adjustments to finalize your taxable income for the applicable period. Let’s have a look at some of the most important adjustments:

Deductible Expenditures

Understanding the business expenses that you can deduct from your business profits to reduce the taxable income is crucial.

- Deductible Expenditures: These are the business expenses that your company incurred to generate taxable income. Examples of such expenditures include rent, salaries, utilities, depreciation, and amortization.

- Limitations on Deductions: You must note that not all expenses are fully deductible. Certain deductions, like entertainment and interest expenses, are limited.some text

- Entertainment Expenses: Only 50% of entertainment expenses can be deducted. Such costs must have been incurred for customers, shareholders, suppliers, or other business partners to be eligible for tax deduction.

- Interest Expenses: Net interest expenditures are allowed up to 30% of a business’s earnings before interest, tax, depreciation, and amortization (EBITDA). This deduction is subject to the OECD’s Base Erosion and Profit Shifting Project Action 4, EBITDA rules.

- Non-deductible Expenses: Certain expenses cannot be deducted at all. These include fines, penalties, dividends, personal expenses, and taxes imposed outside the UAE.

Tax Loss Relief

The concept of tax loss relief is another important aspect of how corporation tax is calculated in the UAE. Here are some key points you must know:

- Tax Loss Relief: As per Article 37 of UAE Corporate Tax law, if your business incurs a tax loss in one tax period, you can offset this loss against the taxable income of subsequent periods. This provision helps reduce your taxable income and, in turn, ensures a lower Corporate Tax liability for your company.

- Limitations: At present, there is no limit on how long losses can be carried forward for tax relief. But you should offset any tax loss carried forward against the taxable income of the next tax period. Only then can you consider carrying any leftover tax loss into the following period.

Current rules state that you cannot offset more than 75% of your taxable income with tax loss in any tax period. This rule ensures fairness, allowing enterprises to avail the benefits of Tax Loss Relief without abusing the process.

Unrealized Gains or Losses

Unrealized gains or losses are changes in the value of assets, such as property that haven’t been sold yet. Let’s understand the way it affects how much taxes a business pays:

- Unrealized Gain: An unrealized gain is an increase in the value of an asset or investment that has not been realized in cash. For example, if your company bought stocks at AED 200 per share and the price rises to AED 250 per share, then you have an unrealized gain of AED 50 per share.

- Unrealized Loss: An unrealized loss is a decrease in the value of an asset or investment that has not been suffered in cash. For example, if your company purchased office space for AED 150,000 and the value decreases to AED 135,000, then your business has an unrealized loss of AED 15,000.

In the UAE, your enterprise can choose to recognize these gains or losses for Corporate Tax purposes only when they are realized, i.e., when the asset is sold. This means that unrealized gains are not taxable, and unrealized losses are not deductible until they are actually realized.

Exempt Income

In the context of how corporation tax is calculated, it’s also crucial to understand different income types exempt from the UAE Corporate Tax.

- Exempt Income: Certain types of income are not calculated for Corporate Tax purposes. These include personal income, foreign income, income from investments, income earned from real estate, businesses registered in the free zones, and businesses involved in the extraction of natural resources.

- Group Relief: The Corporate Tax rules permit relief on intra-group transfers of assets and liabilities among UAE resident companies that share at least 75% common ownership. This provision facilitates smoother financial operations within closely linked corporate groups. The assets and liabilities must remain within the same group for at least three years to avail relief.

Small Business Relief

The UAE Corporate Tax Law provides a provision known as the Small Business Relief, designed to support start-ups and other small or micro businesses by reducing their Corporate Tax burden and compliance costs.

- Eligibility: You, as a resident taxable person, can take advantage of the Small Business Relief if your revenue doesn't exceed AED 3 million in the tax period in question and in each of the previous periods. This means your business will be treated as not having derived any taxable income in a given tax period where the revenue did not exceed the threshold. However, once your revenue crosses the AED 3 million mark in any tax period, you will no longer be eligible for this relief.

- Time Frame: The revenue cap of AED 3 million is relevant for tax periods starting on or after June 1, 2023. It remains applicable for all subsequent tax periods ending on or before December 31, 2026.

- Exclusions: If you're a Qualifying Free Zone Person (QFZP) or part of a Multinational Enterprises Group (MNE Group) as outlined in Cabinet Decision No. 44 of 2020, you won't be able to use the Small Business Relief. An MNE Group refers to a cluster of companies with cross-border operations and consolidated revenues exceeding AED 3.15 billion.

- Carry Forward: For any tax periods where you choose not to claim Small Business Relief, you can carry forward any Tax Losses or Net Interest Expenditures that were not allowed. You can then apply these in future tax periods where the Small Business Relief is not chosen.

How the UAE Corporate Tax Impacts Businesses

With the new UAE Corporate Tax regime in place, you are now required to register and submit the company tax return annually to the Federal Tax Authority (FTA). This means you must maintain proper accounting records and comply with tax laws, any failure to do so can lead to penalties and fines.

But this is not all, with the 9% tax, your company might start feeling the extra financial burden. Hence, you should take every step to prevent unnecessary cash leakages. One effective way to manage this is by automating expense management with a robust spend management solution.

With an expense management solution like Alaan, you can:

- Identify Tax-Deductible Expenses: Manage cash flow in real-time and identify expenses that can be deducted from taxable income. This will help optimize your tax strategy and potentially increase your savings.

- Save Time and Money: Reduce potential errors in tax filing, saving both time and money. This feature allows you to focus more on your core business operations.

- Gain Valuable Insights: Understand where the company spends its money so that you can use this information to implement strategic cost control measures and improve your bottom line.

- Accuracy and Compliance: Maintain compliance and avoid penalties by automatically applying tax codes and rules to expenses. This not only saves you from costly mistakes but also reduces the stress associated with tax penalties.

With an in-depth understanding of Corporate Tax calculations, you are well-equipped to navigate the new tax landscape in the UAE effectively.

Meanwhile if you are looking for corporate card and expense management solutions to streamline your business spend, get in touch with the experts at Alaan!

We are always here to help!