UAE finance teams do not have a “foreign currency problem” once a year. They have it every close. When your receivables, payables, loans, or bank balances sit in USD, EUR, GBP, or INR, the AED value of open balances moves with rates, even if nothing operational changed. If you keep those balances at old rates, your financial statements quietly drift away from reality.

This matters in the UAE because cross-border activity is structural, not occasional. The Central Bank of the UAE publishes daily exchange rates against AED for VAT-related obligations, which is a good indicator of how routinely UAE businesses must convert foreign currency amounts into AED for compliance and reporting workflows.

For most UAE entities using IFRS, FX revaluation accounting is the discipline that prevents period-end distortion. Under IAS 21, the closing rate is the spot exchange rate at the end of the reporting period, and monetary items are remeasured accordingly, with the resulting exchange differences recognised in profit or loss (with limited exceptions).

In this blog, we break down FX revaluation accounting for UAE reporting, what gets revalued, which rates apply, and the practical FX revaluation accounting entries that keep the month-end accurate.

TL;DR

- FX revaluation accounting updates open foreign-currency monetary balances to the period-end closing rate so financial statements reflect current AED values.

- Unrealised FX differences arise at period-end revaluation; realised FX differences arise at settlement against the latest carrying amount.

- The journal entry pattern is consistent: adjust the monetary balance sheet account and post the offset to FX gain/loss.

- Most revaluation errors come from misclassifying monetary vs non-monetary items, inconsistent rates, and mishandling partial settlements.

- Cleaner FX close depends on better invoice, approval, and payment traceability. Alaan helps finance teams keep foreign-currency spend easier to track and reconcile.

FX Revaluation Accounting Rules For UAE Reporting Frameworks

The “rules” matter because revaluation is not applied to everything that looks foreign-currency related. The core logic is: revalue monetary items at the closing rate at each reporting date, and recognise the resulting exchange difference in profit or loss (with limited exceptions under specific standards).

What FX Revaluation Means In Practice

FX revaluation updates the carrying amount (book value) of eligible foreign-currency balances at period-end. It does not change the original invoice, contract, or agreed foreign-currency amount. It changes the AED equivalent you report at the reporting date.

Monetary Vs Non-Monetary Items

This is the most common source of mistakes.

- Monetary items are amounts to be received or paid in a fixed or determinable number of currency units. Examples: cash, foreign-currency bank balances, trade receivables, trade payables, loans. These are retranslated at the closing rate at each reporting date.

- Non-monetary items are not settled in a fixed number of currency units (e.g., inventory at cost, fixed assets at cost, prepayments). These are generally not retranslated when measured at historical cost (they stay at the historical rate used when first recognised).

Unrealised Vs Realised FX Differences

- Unrealised FX gain/loss: The exchange difference created by revaluing an open (unsettled) monetary balance at period-end.

- Realised FX gain/loss: The exchange difference recognised when the transaction is settled (cash moves), compared to the carrying amount at that settlement point.

Functional Currency Basics

Revaluation is done in your functional currency (often AED for UAE-based businesses). IAS 21 sets the framework for determining functional currency and translating foreign currency transactions when IFRS applies.

When FX Revaluation Is Required

FX revaluation is typically a close activity, but the underlying logic is consistent: open foreign-currency monetary items should reflect the reporting-date rate, and settlement should recognise any remaining exchange difference.

1. Month-End And Year-End Close

At each reporting date (month-end/quarter-end/year-end), foreign-currency monetary items are translated using the closing rate and exchange differences are recognised (subject to limited exceptions under other standards).

2. Settlement Date Treatment

When the receivable/payable is settled, any difference between:

- the carrying amount (after the most recent revaluation), and

- the actual AED amount settled

is recognised as a realised FX gain or loss.

Which Rates Are Typically Used

In practice, you’ll see three “rate moments” in the system:

- Transaction-date rate: Used when the foreign-currency transaction is first recorded.

- Closing rate: Used at period-end revaluation for monetary items.

- Settlement rate: The executed rate when cash is paid/received.

A separate but related point: for UAE VAT-related conversions, businesses often refer to the Central Bank of the UAE’s “exchange rates against UAE Dirham for VAT-related obligations.” That is a VAT conversion reference, not a replacement for period-end financial statement translation under IAS 21.

Also Read: Guide to Preparing Financial Statements Efficiently

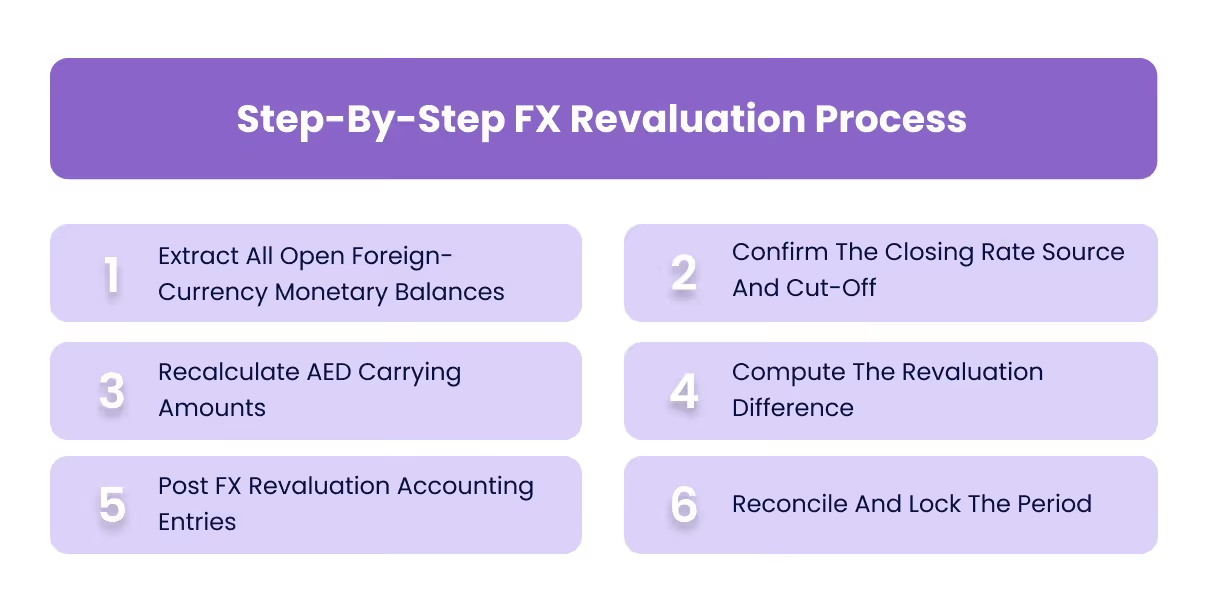

Step-By-Step FX Revaluation Process

FX revaluation is easiest to run as a close checklist. The goal is consistency: identify all open foreign-currency monetary balances, apply the correct closing rate, post the revaluation entries, and reconcile the results so nothing is missed or double-counted.

1. Extract All Open Foreign-Currency Monetary Balances

Start with the balances that are still open at period-end:

- Accounts receivable invoices outstanding in foreign currency.

- Accounts payable bills outstanding in foreign currency.

- Foreign-currency bank accounts and cash balances.

- Foreign-currency loans, intercompany balances, and advances (where relevant).

The key is to capture the foreign-currency amount and the current carrying amount in AED for each balance.

2. Confirm The Closing Rate Source And Cut-Off

Define one closing-rate source for the period-end cut-off (and document it). Under IFRS, the closing rate is the spot exchange rate at the reporting date.

In practice, teams typically standardise on:

- A central bank reference rate (where applicable to their policy), or

- A consistent market data source used across finance systems.

What matters is that the rate source is consistent, auditable, and applied uniformly across the close.

3. Recalculate AED Carrying Amounts

For each open monetary balance:

- Take the foreign-currency amount (e.g., USD 100,000).

- Multiply by the closing rate (e.g., 3.70 AED/USD).

- Compare that result to the current AED carrying amount in the ledger.

4. Compute The Revaluation Difference

The difference between the newly calculated AED amount at the closing rate and the current AED carrying value is your unrealised FX gain or loss for that balance at period-end.

5. Post FX Revaluation Accounting Entries

Post the journal entries that:

- Adjust the balance sheet account (AR/AP/Bank/Loan).

- Recognise the unrealised FX gain or loss in your FX P&L account(s).

The entry pattern is consistent; only the direction changes depending on whether the asset/liability increases or decreases in AED.

6. Reconcile And Lock The Period

Before you close:

- Tie the revaluation report back to the GL balances.

- Confirm no open items were excluded (especially partially settled invoices).

- Confirm revaluation entries were not posted twice by different users/systems.

FX Revaluation Accounting Entries

FX revaluation accounting entries follow a simple rule: adjust the AED carrying amount of the foreign-currency monetary balance, and post the offset to an unrealised FX gain/loss account. At settlement, any remaining difference becomes realised FX gain/loss.

1. FX Revaluation Accounting Entries For Receivables

If a foreign-currency receivable increases in AED value at period-end, you record an unrealised gain.

Example (USD Receivable):

- Invoice: USD 100,000

- Original booking rate: 3.67 → AED 367,000

- Closing rate: 3.70 → AED 370,000

- Unrealised gain: AED 3,000

Journal Entry (Period-End Revaluation):

2. FX Revaluation Accounting Entries For Payables

If a foreign-currency payable increases in AED value at period-end, you record an unrealised loss (because the liability is higher in AED).

Example (EUR Payable):

- Bill: EUR 50,000

- Original booking rate: 4.00 → AED 200,000

- Closing rate: 4.10 → AED 205,000

- Unrealised loss: AED 5,000

Journal Entry (Period-End Revaluation):

Account

3. FX Revaluation Accounting Entries For Foreign-Currency Bank Accounts

Foreign-currency bank balances are monetary items, so they are also revalued at period-end.

Example (USD Bank Balance):

- Balance: USD 20,000

- Carrying rate in books: 3.66 → AED 73,200

- Closing rate: 3.68 → AED 73,600

- Unrealised gain: AED 400

Journal Entry (Period-End Revaluation):

4. Settlement Entries And Realised FX Gain Or Loss

At settlement, you compare the settlement AED amount to the carrying amount at that time (which may already reflect period-end revaluation). The difference becomes realised FX gain/loss.

Example (Settlement After Period-End Revaluation):

Continuing the USD receivable above, assume it was revalued to AED 370,000 at period-end, then settled later at 3.69.

- Receivable carrying amount: AED 370,000

- Cash received: USD 100,000 × 3.69 = AED 369,000

- Realised FX loss on settlement: AED 1,000

Journal Entry (On Receipt):

5. Common Variations (Intercompany, Loans, Advances)

The same logic applies to other foreign-currency monetary items, but teams often separate accounts for reporting clarity:

- Loans and intercompany balances may post FX differences to finance costs rather than operating lines, depending on internal reporting policy.

- Advances need classification discipline: if they are monetary (repayable in a fixed amount), they are revalued; if they are non-monetary in substance, they may not be.

Also Read: Understanding General Ledger in Double-Entry Accounting

Practical Examples Of FX Revaluation Journal Entries

Examples help because FX revaluation is mechanically simple, but easy to mispost when rates, partial settlements, and period-end timing collide. The key is to keep the foreign-currency amount constant, and let the AED equivalent move as rates change.

1. Period-End Revaluation Of A USD Receivable

A UAE business issues an invoice for USD 100,000.

- Transaction date rate: 3.67 AED/USD → recorded at AED 367,000

- Period-end closing rate: 3.70 AED/USD → should be AED 370,000

- Unrealised FX gain at period-end: AED 3,000

Period-End Revaluation Entry

2. Period-End Revaluation Of A EUR Payable

A UAE business records a supplier bill for EUR 50,000.

- Transaction date rate: 4.00 AED/EUR → recorded at AED 200,000

- Period-end closing rate: 4.10 AED/EUR → should be AED 205,000

- Unrealised FX loss at period-end: AED 5,000

Period-End Revaluation Entry

3. Partial Settlement, Then Period-End Revaluation, Then Final Settlement

This is where many teams double-count or revalue the wrong amount.

A UAE business records a supplier bill for USD 50,000.

Initial Recognition

- Transaction date rate: 3.66 AED/USD → recorded at AED 183,000

Partial Payment Before Period-End

The business pays USD 20,000 at 3.65 AED/USD.

- Carrying value of the portion settled: USD 20,000 × 3.66 = AED 73,200

- Cash paid: USD 20,000 × 3.65 = AED 73,000

- Realised FX gain on the settled portion: AED 200

Entry At Partial Settlement

Period-End Revaluation On The Remaining Open Balance Only

Remaining payable is USD 30,000.

- Carrying amount before revaluation: USD 30,000 × 3.66 = AED 109,800

- Period-end closing rate: 3.70 AED/USD → USD 30,000 × 3.70 = AED 111,000

- Unrealised FX loss at period-end on remaining balance: AED 1,200

Period-End Revaluation Entry

Final Settlement After Period-End

The business pays the remaining USD 30,000 at 3.68 AED/USD.

- Carrying amount at settlement (post revaluation): AED 111,000

- Cash paid: USD 30,000 × 3.68 = AED 110,400

- Realised FX gain on final settlement: AED 600

Entry At Final Settlement

Common Mistakes And How To Avoid Them

FX revaluation problems rarely come from complex maths. They come from classification mistakes, inconsistent rates, and process gaps during close. Fixing these issues early reduces audit pain and prevents recurring variance “mysteries.”

1. Revaluing Non-Monetary Items Incorrectly

A classic error is revaluing items that should stay at historical rates when measured at cost (for example, inventory at cost or prepayments). The result is noise in FX gain/loss that does not reflect the accounting framework.

How to avoid it: Maintain a clear mapping of which GL accounts are monetary and included in revaluation, and which are excluded.

2. Using Inconsistent Rates Across Systems

If AR is revalued using one rate source and AP using another, you create unexplained differences that are hard to reconcile and harder to defend.

How to avoid it: Define one period-end closing-rate policy (rate source + cut-off timestamp) and apply it consistently across the close.

3. Double-Counting Realised And Unrealised FX

This happens when teams revalue an item at period-end, then also treat the full difference at settlement as “new” FX rather than comparing settlement to the latest carrying amount.

How to avoid it: Always settle against the post-revaluation carrying amount, so only the incremental difference becomes realised FX.

4. Missing Partially Settled Invoices

If you revalue the original invoice amount instead of the open balance, the revaluation entry will be wrong and will not reverse cleanly.

How to avoid it: Revalue only open amounts as of the reporting date and ensure partial settlements are posted before the revaluation run.

5. Revaluing The Wrong Currency Or Functional Currency

Some organisations accidentally revalue using a presentation currency or an internal reporting currency rather than the functional currency used in the general ledger.

How to avoid it: Confirm the functional currency at the entity level and ensure revaluation is performed in that currency with consistent settings in the accounting system.

Also Read: The Essential Guide to Cross-Border Payments in the UAE

How Alaan Helps Keep FX Close More Manageable

FX revaluation is still handled in the accounting system, but month-end gets harder when foreign-currency invoices, approvals, payments, and supporting records are scattered across different tools. Alaan helps finance teams keep that workflow more structured, visible, and easier to reconcile.

- Invoice Capture

Alaan helps teams capture invoice and spend records in a more structured workflow, so the source documents behind foreign-currency transactions are easier to trace during close. - Approval Workflows

Custom approval workflows help finance teams keep better control over spend before it moves through payment and reconciliation, which reduces confusion at period-end. - Receipt Verification And Matching

Alaan Intelligence can extract invoice and receipt data, match it to transactions, and flag discrepancies or duplicates. That makes supporting records easier to review when investigating FX-related balance movements. - Accounting Integrations

Alaan integrates with systems such as Xero, QuickBooks, NetSuite, and Microsoft Dynamics, with real-time syncing that helps reduce manual rework and supports smoother reconciliation. - Vendor Management And Payment Controls

Through Super Pay, Alaan also adds vendor management, invoice approvals, payment approvals, and automation rules, giving teams more control over international supplier payment workflows. - Better Cross-Border Payment Visibility

Super Pay is positioned around connected international payment workflows, easier reconciliation, and better visibility into FX impact before payment approval, which is especially relevant for UAE businesses managing foreign-currency supplier payments.

In practice, that means finance teams can keep foreign-currency activity better documented from invoice through payment. Alaan does not replace FX revaluation accounting, but it can make the workflow around cross-border spend cleaner, more traceable, and easier to manage at close.

Conclusion

FX revaluation accounting is not about complicated calculations. It is about discipline: correctly identifying monetary items, applying a consistent closing rate at each reporting date, and ensuring settlement FX is measured against the latest carrying amount so you do not double-count gains or losses. When those basics are right, FX volatility stops hijacking close with unexplained variances and messy reconciliations.

At Alaan, we help finance teams keep international spend workflows traceable. When invoices, approvals, payment references, and supporting documents stay connected through the payment lifecycle, FX review and reconciliation become faster and easier to defend. If your close is repeatedly slowed by cross-border supplier payments and missing context, book a demo to see how Alaan can bring more control and visibility to the workflow.

FAQs

1. Do You Revalue Foreign-Currency Revenue And Expense Accounts At Period-End

In most cases, revenue and expense lines are recognised at the transaction-date rate (or an approved average rate policy) and are not “revalued” like monetary balance sheet items. The revaluation focus is typically open monetary balances (AR, AP, bank, loans) at the reporting date.

2. Should You Revalue Inventory And Prepayments Denominated In Foreign Currency

If inventory or prepayments are non-monetary items carried at historical cost, they generally remain at the historical rate used on initial recognition. They are not retranslated at every period-end the way monetary items are. The key is classification, not the currency label.

3. What Happens To The Unrealised FX Gain Or Loss When The Invoice Is Finally Settled

At settlement, you compare the cash amount (at the settlement rate) to the latest carrying amount (which may include prior period-end revaluation). Any remaining difference becomes realised FX gain or loss at settlement.

4. How Do You Handle FX Revaluation For Foreign-Currency Bank Accounts With Many Transactions

Many teams revalue the ending balance only (as a monetary item) using the closing rate, and rely on the accounting system’s cash module for transaction-date entries. The important control is that the foreign-currency balance and the AED equivalent reconcile cleanly at close.

5. How Often Should A UAE Business Perform FX Revaluation

The common practice is at each reporting date (monthly for many businesses, at minimum quarterly or annually depending on reporting requirements). The frequency should align with your reporting cadence and materiality of FX exposure.