Zakat is widely recognised as a core obligation in Islam, yet when it comes to actual calculation, it often becomes a point of uncertainty. The challenge is rarely about understanding its importance. It is about determining what qualifies as zakatable wealth, when the obligation is triggered, and how the amount should be calculated accurately.

In practice, zakat sits at the intersection of faith and financial discipline. It applies to accumulated wealth, not just income, and requires clarity on asset types, thresholds, and time-based conditions. In the UAE, this process is supported through official channels such as Awqaf, which provide structured guidance and digital access for calculation and payment.

For business owners and individuals managing complex finances, zakat can extend beyond personal savings to trade inventory, receivables, and certain business-related assets. That makes it important to understand what qualifies, what does not, and how the calculation should be approached clearly.

This guide breaks down what zakat means, who needs to pay it, how nisab works, and how to calculate it in a practical, UAE-relevant context.

TL;DR / Key Takeaways

- Zakat applies to accumulated qualifying wealth, not simply to income as it is earned.

- The real complexity in zakat usually comes from asset classification, especially when savings, inventory, investments, and receivables are involved.

- For founders and finance leaders, zakat becomes easier to manage when financial records are structured and visibility over assets is strong.

- Official UAE channels have made zakat calculation and payment more accessible, reducing friction in the final step.

- A disciplined zakat process depends on consistency, accurate review cycles, and clear separation between personal-use assets and zakatable wealth.

What Is Zakat?

Zakat is an obligatory form of giving in Islam that applies to eligible Muslims whose wealth meets specific conditions. It is not a voluntary contribution. It is a defined financial responsibility based on the amount and type of wealth owned.

The obligation is tied to accumulated wealth rather than day-to-day earnings. Once qualifying assets reach a minimum threshold, known as nisab, and remain at or above that level for one lunar year, zakat becomes payable at a standard rate.

The key point is that zakat is based on qualifying wealth held over time, not simply on income earned during the year.

Why Is Zakat Important?

Zakat plays a dual role. It is both a religious obligation and a structured mechanism for wealth distribution.

At a financial level, zakat introduces discipline into how wealth is evaluated. It requires periodic assessment of savings, gold holdings, investments, and business-related assets. This process creates visibility into what is owned, what is liquid, and what qualifies as part of the zakatable base.

For business leaders, this becomes particularly relevant when wealth is not limited to personal accounts but extends into inventory, retained profits, or receivables. The obligation itself may be individual, but the inputs often sit within broader financial systems.

Also Read: How to Create a Financial Plan for Your UAE Business

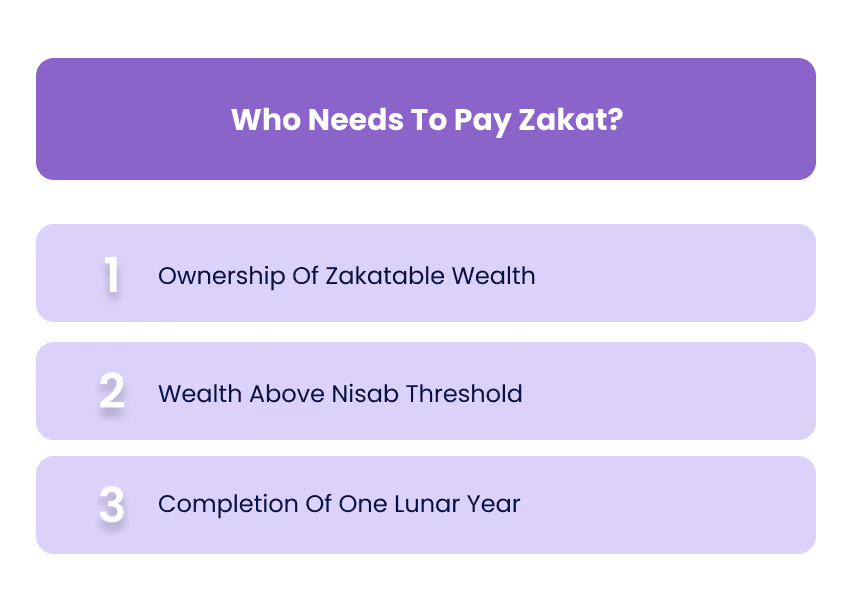

Who Needs To Pay Zakat?

Zakat becomes due when three conditions are met simultaneously. These conditions define whether the obligation applies at all.

1. Ownership Of Zakatable Wealth

The individual must own assets that qualify for zakat, such as savings, gold, investments, or trade-related assets.

2. Wealth Above Nisab Threshold

Total qualifying wealth must exceed the minimum threshold required for zakat to apply.

3. Completion Of One Lunar Year

The wealth must remain at or above the nisab level for one full lunar year.

This framework ensures that zakat is not triggered by temporary income or short-term balances. It applies to sustained, accumulated wealth.

For founders and finance leaders, this distinction is critical. Business cash flows may fluctuate throughout the year, but zakat is assessed based on retained value rather than movement alone.

What Wealth Is Usually Included In Zakat?

Zakat generally applies to assets that are held for accumulation, growth, or trade. The classification of these assets is what determines the zakatable base.

1. Cash And Savings

Balances held in bank accounts, reserves, or liquid funds are included once they meet nisab and complete the lunar-year condition. The standard zakat rate applied is 2.5%.

2. Gold And Silver

Precious metals are directly included in zakat calculations and also serve as reference points for determining nisab thresholds.

3. Trade Goods And Inventory

Inventory held for sale is considered zakatable wealth. For businesses, this often represents a significant portion of the zakat base.

4. Investments And Shares

Financial investments may be included depending on their purpose, whether for trading, income generation, or long-term holding.

5. Receivables Likely To Be Collected

Amounts owed to the business or individual that are expected to be recovered can form part of the zakatable total.

From a finance perspective, this is where zakat moves beyond theory. The classification of assets requires judgment, especially when separating operational assets from those that qualify for zakat.

What Is Usually Not Included In Zakat?

Zakat does not apply to assets held purely for personal use or essential living purposes. This distinction ensures that zakat is applied to wealth accumulation rather than basic consumption.

Common exclusions include:

- Primary Residence

- Personal-Use Vehicle

- Household Furniture And Equipment

- Personal Clothing And Essentials

For businesses, this principle translates into excluding operational infrastructure that is not held for trade or resale.

Related: What Qualifies As A Business Expense

What Is Nisab?

Nisab is the minimum amount of qualifying wealth a person must own before zakat becomes due. It acts as the financial threshold that determines whether the obligation applies at all. For anyone assessing zakat properly, this is the first checkpoint before moving into calculation. Awqaf’s zakat guidance states that nisab begins at 85 grams of gold or 595 grams of silver. It also notes that the nisab for cash is equivalent to the value of 85 grams of gold, while trade goods follow the cash-value threshold.

This becomes especially relevant in a business or finance context because zakat is not triggered by revenue alone. It is triggered when net qualifying wealth crosses the threshold. That distinction matters for founders, business owners, and finance leaders evaluating retained balances, inventory values, or collectible receivables rather than looking only at top-line inflows.

How The Lunar-Year Rule Works

Crossing nisab is only part of the calculation. Zakat also depends on time. Awqaf explains that once qualifying wealth first reaches nisab, one lunar year begins from that point. Changes in wealth during the year do not usually interrupt the zakat cycle unless the amount falls below nisab. If it does fall below the threshold, the count resets and a new zakat year starts only once wealth returns to or exceeds nisab again.

For finance teams, this rule helps separate temporary volatility from actual zakat liability. A fluctuating bank balance, seasonal sales cycle, or uneven receivables pattern does not automatically change the zakat position every time values move. The more useful lens is whether qualifying wealth remained above the threshold across the full lunar cycle.

How To Calculate Zakat Step By Step

Once the threshold and timing rules are clear, the calculation itself becomes much more manageable. In most cases, the process begins by identifying all qualifying assets, removing personal-use items and non-zakatable assets, confirming that the total remains above nisab, and then applying the zakat rate. Awqaf states that zakat on cash is calculated at 2.5%.

A structured finance-led approach usually looks like this:

- Identify Qualifying Cash Balances

- Add Gold, Silver, And Eligible Investments

- Include Trade Inventory Held For Sale

- Review Receivables Likely To Be Collected

- Exclude Personal-Use And Non-Trade Assets

- Confirm Wealth Remains Above Nisab

- Apply The 2.5% Zakat Rate

For example, if total qualifying zakatable wealth equals AED 100,000, the zakat amount at 2.5% would be AED 2,500. The real challenge is rarely the percentage itself. It is defining the correct asset base with consistency, especially where business and personal finances intersect.

How To Pay Zakat In The UAE

In the UAE, zakat can be calculated or paid through official digital channels rather than informal or manual processes alone. Awqaf’s service guide lists several access channels for zakat calculation, including its website, WhatsApp, call centre support, smart applications, and DubaiNow for zakat on money and gold. It also notes a proactive reminder after one Hijri year from the service request date. TAMM similarly outlines a flow where users log in with UAE PASS, select zakat or calculation services, and calculate zakat across the specified asset list.

That practical accessibility matters. For professionals managing multiple obligations, delays often come from uncertainty and fragmented records rather than unwillingness to pay. A clearer process, supported by official UAE channels, makes the final step far easier to complete on time and with more confidence.

Also Read: Modern Expense Management Guide

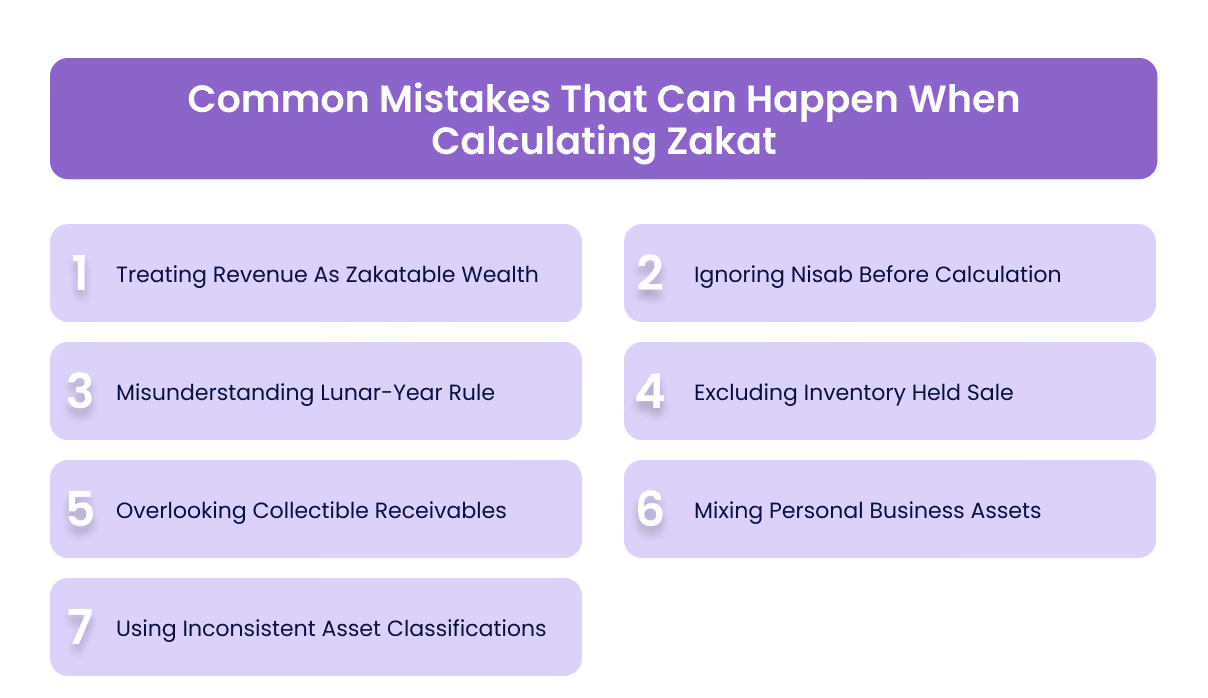

Common Mistakes That Can Happen When Calculating Zakat

Zakat calculation usually goes wrong at the classification stage, not the percentage stage. For finance leaders, the risk is rarely the 2.5% rate itself. It is the treatment of cash, inventory, receivables, and mixed personal-business balances. The mistakes below are the ones most likely to distort the final number or weaken internal clarity.

1. Treating Revenue As Zakatable Wealth

A business may generate strong revenue and still not hold the same amount as zakatable wealth. Zakat is not assessed on topline sales. It is assessed on qualifying wealth that remains in hand and meets the nisab and lunar-year conditions.

This matters in operating businesses where cash is constantly moving through payroll, supplier payments, tax obligations, and working capital requirements. Looking at revenue instead of retained qualifying wealth can materially overstate zakat exposure.

2. Ignoring The Nisab Threshold Before Starting The Calculation

Some people begin with asset totals and jump straight to the 2.5% rate. That skips the first gate in the process. If qualifying wealth has not crossed nisab, zakat is generally not due.

For founders and finance managers reviewing personal and business-linked balances, this threshold check should happen before any detailed asset consolidation begins.

3. Misunderstanding The Lunar-Year Requirement

Zakat is not triggered every time money enters an account. It becomes due when qualifying wealth remains at or above nisab for one full lunar year. Fluctuating balances during the year do not automatically create a new cycle unless wealth falls below the threshold.

This is especially relevant in businesses with uneven collections, seasonal demand, or volatile inventory cycles, where month-end balances alone do not tell the full story.

4. Excluding Trade Inventory Held For Sale

Inventory is one of the most commonly missed items in zakat calculation for business owners. If goods are held for sale, they may form part of the zakatable base.

This issue tends to surface in trading, retail, distribution, and product-led businesses where management is focused on margin and stock turnover, but not necessarily reviewing inventory from a zakat perspective.

5. Overlooking Receivables That Are Likely To Be Collected

Receivables are often ignored because they are not yet cash in the bank. But where collection is likely and commercially realistic, they may still need to be considered as part of qualifying wealth.

For finance leaders, the real issue is not whether every receivable should be counted identically. It is whether receivables are being reviewed with a consistent, documented logic rather than excluded by default.

6. Mixing Personal And Business Assets Without A Clear Boundary

This is one of the most important errors in founder-led businesses. Owner balances, retained business cash, reimbursements, and personal savings can become blurred when financial boundaries are weak.

That makes zakat harder to assess and also creates broader finance control issues. A cleaner separation between personal and business finances improves not only zakat calculation, but also reporting discipline and internal visibility.

7. Using Inconsistent Asset Classifications Across Review Periods

A balance that is treated as operational in one review and zakatable in another will distort the final outcome. The same problem appears when inventory, receivables, or reserves are assessed differently every year without a defined internal approach.

For businesses, consistency matters more than ad hoc estimation. Once finance teams define how specific asset categories will be reviewed, the process becomes easier to repeat and defend.

Related: Taking Control of Your Account Reconciliation

How Alaan Helps Finance Teams Manage Outgoing Payments With Better Control

Zakat is a personal religious obligation, but in many businesses, charitable disbursements, founder-led giving, and approved social contribution payments still move through company finance processes. Once that happens, the challenge is no longer only about intent. It becomes a matter of visibility, approval control, documentation, and reconciliation.

Alaan supports finance teams at this execution layer, helping businesses ensure that outgoing payments remain structured, visible, and properly documented.

- Corporate Cards With Smart Spend Controls

Alaan enables businesses to issue corporate cards with predefined controls, helping teams manage spending limits and keep outgoing payments within approved boundaries. - Approval Workflows Before Money Moves

Payments can be routed through structured approval flows before spend happens, reducing the risk of undocumented or unapproved disbursements. - Real-Time Visibility Across Business Spend

Finance teams get a clearer view of where money is going across entities, functions, and teams, making outgoing payments easier to track and review. - Centralised Receipt And Invoice Capture

Supporting documents can be collected and linked to transactions in one place, reducing fragmented records and making internal verification easier. - Faster Reconciliation And Accounting Sync

With integrations into systems such as Xero, QuickBooks, NetSuite, and Microsoft Dynamics, payment data flows more cleanly into accounting workflows with less manual effort. - Better Audit Readiness For Outgoing Transactions

Each transaction carries a clearer trail of approvals, documents, and categorisation, helping teams maintain stronger internal control and cleaner records.

In practice, this means that once an outgoing payment is approved, finance teams can execute it with better visibility and stronger operational control.

Conclusion

Zakat is a structured financial obligation built around qualifying wealth, minimum thresholds, and the completion of one lunar year. While the final calculation may appear simple, the real challenge often lies in classifying assets correctly and applying the rules with consistency.

For founders, business owners, and finance leaders, that makes financial clarity especially important. The better the visibility over savings, inventory, receivables, and outgoing payments, the easier it becomes to manage zakat-related decisions accurately and without confusion.

And when approved business payments need to be executed with stronger control, visibility, and documentation, Alaan helps finance teams keep the process structured from approval through reconciliation. Book a Demo Today

FAQs

1. Is Zakat Calculated On Revenue Or On Profit?

Zakat is not usually calculated on revenue alone. It is generally assessed on qualifying wealth that has been retained and meets the nisab and lunar-year conditions. For businesses, that often makes asset classification more important than topline income.

2. Can Business Owners Pay Zakat From Company Funds?

That depends on ownership structure, internal policy, and how the payment is being treated. In practice, finance leaders should separate personal zakat obligations from company-authorised charitable or social disbursements to avoid accounting confusion.

3. Do Fluctuating Bank Balances Affect Zakat Every Month?

Not necessarily. Day-to-day balance movements do not automatically create a new zakat calculation cycle. The more important question is whether qualifying wealth remained above nisab across the relevant lunar period.

4. Is Zakat Still Due If Wealth Is Tied Up In Stock Or Receivables?

In many cases, yes. Trade inventory and receivables likely to be collected may still form part of zakatable wealth, which is why businesses should review asset composition carefully rather than focusing only on cash in the bank.

5. Should Founders Separate Personal And Business Assets Before Calculating Zakat?

Yes, that is usually the cleanest approach. Mixing personal savings, owner withdrawals, company reserves, and operating assets can distort the zakat base and make the final number less reliable.

6. Why Do Finance Teams Struggle With Zakat Even When The Rate Is Simple?

The difficulty is rarely the 2.5% rate itself. The challenge usually comes from identifying which assets qualify, what should be excluded, and whether records are accurate enough to support a consistent calculation.