Unpaid invoices can make a business look stronger than it feels. Sales have been made, customers owe money, and revenue may already be recorded, but the cash is still locked in receivables. Meanwhile, payroll, supplier payments, rent, and operating expenses continue on schedule.

Accounts receivable factoring helps close that timing gap by converting unpaid invoices into earlier cash. The trade-off is cost. A business may receive cash faster, but it gives up part of the invoice value through fees, reserves, and sometimes customer collection control.

In this blog, we will explain the cost of factoring accounts receivable, how factoring fees and advance rates work, what affects the final cost, and how finance teams should decide whether factoring is worth using.

TL;DR / Key Takeaways

- Accounts receivable factoring gives businesses earlier cash by selling unpaid invoices to a factoring company.

- The cost usually includes a factoring fee, reserve holdback, and possible service or transfer charges.

- The advance rate is not the cost. It only shows how much of the invoice value is paid upfront.

- Recourse factoring usually costs less but leaves more customer non-payment risk with the business.

- Factoring should be judged against cash flow benefit, margin impact, customer risk, and reporting complexity.

What Accounts Receivable Factoring Means

Accounts receivable factoring is a working capital arrangement where a business sells unpaid customer invoices to a factoring company at a discount. In return, the business receives part of the invoice value before the customer pays.

This is different from simply waiting for standard payment terms to run their course. If a customer is due to pay in 30, 60, or 90 days, factoring allows the business to access cash earlier, often to cover operating needs or fund growth.

In the UAE, delayed collections remain a major issue, with Atradius reporting that 58% of B2B invoices are overdue.

The factoring company then collects payment from the customer, depending on how the arrangement is structured. Once the customer pays, the factor deducts its fees and releases any remaining balance to the business.

For finance teams, the key point is that factoring improves timing, not total value. The business receives cash sooner, but the final amount retained is lower than the invoice value.

Also Read: Understanding Trade Receivables Key Concepts

How Business Accounts Receivable Factoring Works

Business accounts receivable factoring follows a structured flow. The exact process depends on the factoring company and the agreement, but the core steps are generally similar.

1. The Business Issues Customer Invoices

The business delivers goods or services and raises invoices with agreed payment terms. These invoices represent amounts owed by customers.

2. The Invoices Are Submitted To The Factor

The business selects eligible invoices and submits them to the factoring company for funding consideration.

3. The Factor Reviews The Customer And Invoice

The factoring company reviews the customer’s credit quality, invoice validity, invoice amount, payment terms, and risk profile. The customer’s ability to pay often matters more than the business’s own credit profile.

4. The Business Receives An Advance

If approved, the factor advances a percentage of the invoice value. This is known as the advance rate.

5. The Customer Pays The Factor

In many factoring arrangements, the customer pays the factoring company directly. This is one of the main differences between factoring and some other receivables finance structures.

6. The Factor Releases The Balance

After the customer pays, the factor deducts the factoring fee and any agreed charges. The remaining balance is then released to the business.

What Makes Up The Cost Of Factoring Accounts Receivable

The cost of factoring accounts receivable is not limited to the headline rate. Finance teams need to look at the full structure, including the advance rate, fee basis, reserve holdback, and any additional charges.

1. Factoring Fee

The factoring fee is the main cost of the facility. It is usually charged as a percentage of the invoice value and may vary based on customer credit quality, invoice volume, industry, and payment terms.

A lower fee may look attractive, but it should always be reviewed alongside the rest of the agreement. Some facilities charge a flat fee, while others increase the cost if the customer takes longer to pay.

2. Advance Rate

The advance rate is the percentage of the invoice value paid upfront. For example, an 85 percent advance rate on an AED 100,000 invoice means the business receives AED 85,000 immediately.

This is not the cost of factoring. It only shows how much cash is released before the customer pays.

3. Reserve Holdback

The reserve is the portion of the invoice value held back by the factor until the customer pays. If the advance rate is 85 percent, the remaining 15 percent is typically held as a reserve.

After payment is collected, the factor deducts fees and releases the remaining balance to the business.

4. Additional Charges

Some factoring arrangements may include other charges. These can include due diligence fees, administration fees, transfer fees, collection fees, minimum fees, or charges linked to late customer payment.

These costs matter because they can change the effective cost of funding even when the factoring rate appears reasonable.

5. Customer Payment Timing

Payment timing can materially affect the final cost. If fees are charged over time, a customer who pays late may increase the total cost of factoring. This is why finance teams should review not only the rate but also how the fee is calculated over the payment period.

Cost Of Factoring Accounts Receivable Formula

Understanding the structure is useful, but finance teams ultimately need a way to quantify the cost and cash impact of factoring.

The calculation can be broken into a few simple components.

Cash Advanced = Invoice Value × Advance Rate

Factoring Fee = Invoice Value × Factoring Fee Rate

Reserve Held = Invoice Value − Cash Advanced

Estimated Net Cash Received = Invoice Value − Total Fees

In practice, the sequence may vary. Some factors deduct fees upfront from the advance, while others deduct them when the customer pays and the reserve is released.

The key point is that the business does not receive the full invoice value. The difference between the invoice value and the final cash received represents the true cost of factoring.

Example Cost Calculation With AED Values

A practical example makes the cost structure clearer.

- Invoice Value: AED 100,000

- Advance Rate: 85 percent

- Cash Advanced: AED 85,000

- Factoring Fee: 3 percent of invoice value

- Factoring Fee Amount: AED 3,000

- Reserve Held: AED 15,000

Once the customer pays:

- The factor deducts AED 3,000 as fees

- The remaining reserve (AED 12,000) is released

Final Outcome

- Total Cash Received: AED 97,000

- Total Cost Of Factoring: AED 3,000

This assumes there are no additional charges and the customer pays on time. If fees increase with delayed payment or if extra charges apply, the effective cost becomes higher.

The example shows why the factoring rate alone does not tell the full story. The timing of payment and fee structure both affect the final outcome.

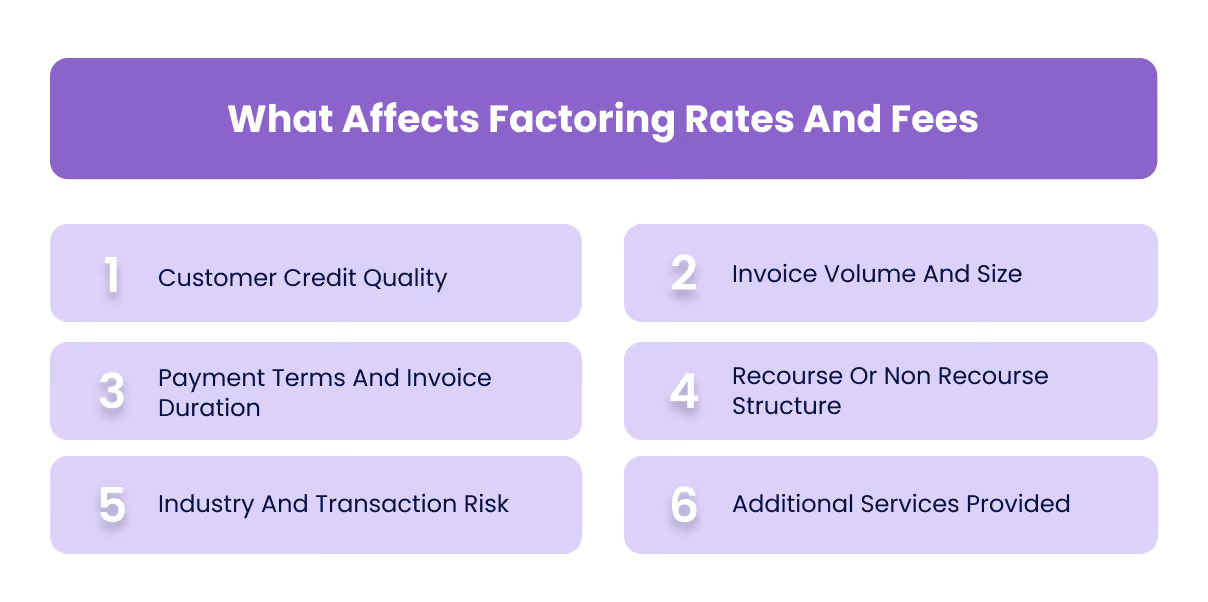

What Affects Factoring Rates And Fees

Factoring costs vary widely depending on the risk and structure of the agreement. Understanding what drives pricing helps finance teams evaluate offers more effectively.

1. Customer Credit Quality

Factoring companies assess the likelihood that the customer will pay. Stronger customer credit profiles usually lead to lower fees.

2. Invoice Volume And Size

Higher volumes or larger invoices can lead to better pricing because the factor earns more consistent fee income across the relationship.

3. Payment Terms And Invoice Duration

Longer payment cycles increase the factor’s exposure and may lead to higher fees.

4. Recourse Or Non Recourse Structure

In recourse factoring, the business retains responsibility if the customer does not pay, which usually results in lower fees. Non recourse structures shift more risk to the factor and therefore cost more.

5. Industry And Transaction Risk

Certain industries carry higher risk due to frequent disputes, longer payment cycles, or complex documentation requirements.

6. Additional Services Provided

If the factor manages collections, credit checks, reporting, or account management, those services may be reflected in pricing.

Also Read: Cash Flow Forecasting

Recourse Factoring Vs Non Recourse Factoring

The choice between recourse and non recourse factoring has a direct impact on both cost and risk.

It is important to note that non recourse factoring does not always cover every type of non-payment. Disputes, contract issues, or documentation gaps may still fall back on the business depending on the agreement.

Factoring Vs Accounts Receivable Financing

Factoring is often confused with accounts receivable financing, but the structure and cost implications are different.

In factoring:

- The business sells its receivables

- The factor may take over collections

- The cost is built into the discount applied to invoices

In accounts receivable financing:

- The business borrows against receivables

- The business usually retains ownership and collections

- The cost may resemble interest on a secured facility

This distinction matters because it affects control, reporting, and customer relationships. It also changes how costs appear in financial statements and cash flow analysis.

Related: Cash Management Control System UAE

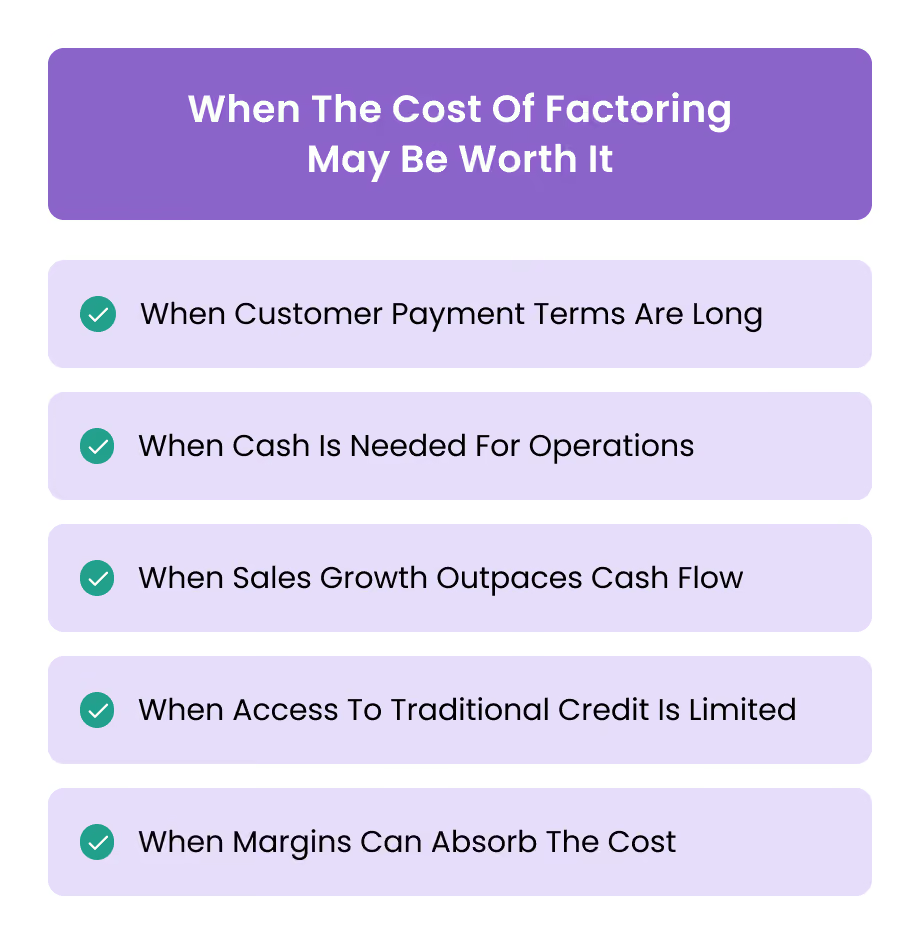

When The Cost Of Factoring May Be Worth It

Factoring is not inherently good or bad. Its value depends on whether the cash flow benefit outweighs the cost.

1. When Customer Payment Terms Are Long

If customers take 60 to 90 days to pay, factoring can reduce the gap between revenue and cash.

2. When Cash Is Needed For Operations

Factoring can help meet payroll, supplier payments, or urgent working capital needs.

3. When Sales Growth Outpaces Cash Flow

Rapid growth often increases receivables faster than cash inflow. Factoring can help stabilise operations during this phase.

4. When Access To Traditional Credit Is Limited

Businesses with strong customers but weaker balance sheets may find factoring easier to access than loans.

5. When Margins Can Absorb The Cost

The business must ensure that factoring fees do not materially reduce profitability.

Also Read:

Manage Business Cash Flow Effectively

Related:

Cash Flow Optimisation Strategies Techniques

When Factoring Costs Can Become Too High

Factoring can improve cash flow timing, but it can also become expensive if not managed carefully. The cost is not always obvious upfront and may increase depending on how invoices behave over time.

1. When Customers Regularly Pay Late

If factoring fees increase over time or are charged per period, late-paying customers can significantly raise the effective cost of funding. This risk becomes more visible in the UAE, where average B2B payment terms already stretch close to 50 days before additional delays are considered.

2. When Margins Are Already Thin

In low-margin businesses, even a small percentage fee can materially reduce profitability. Factoring should be evaluated against gross margin, not just cash needs.

3. When Invoice Disputes Are Common

Disputed invoices can delay payment, trigger additional charges, or fall outside non-recourse protection. This creates both cost and operational friction.

4. When Additional Fees Are Not Fully Understood

Administrative fees, minimum charges, transfer costs, or collection-related fees can increase the total cost beyond the headline rate.

5. When Factoring Is Used Continuously

Using factoring as a permanent solution rather than a temporary working capital tool can result in ongoing cost leakage over time.

6. When It Replaces Basic Cash Flow Discipline

Factoring should not compensate for weak collections processes, poor invoicing practices, or unclear payment terms.

Common Mistakes Businesses Make With Factoring Costs

Even when businesses understand the basics, errors in evaluation or execution can lead to higher costs than expected.

1. Focusing Only On The Factoring Fee Rate

The headline percentage does not reflect the full cost. Advance rate, reserve, and additional charges must also be considered.

2. Confusing Advance Rate With Funding Value

A higher advance rate improves cash timing but does not reduce the cost of factoring.

3. Ignoring The Impact Of Payment Timing

Late customer payments can increase the total fee if pricing is time-based.

4. Overlooking Reserve Release Timing

The timing and conditions for releasing the reserve affect actual cash flow.

5. Not Comparing Alternatives

Factoring should be compared with credit lines, supplier renegotiation, and improved receivables collection.

6. Factoring Without Tracking Profit Impact

The cost of factoring should always be evaluated against margins to ensure it does not erode profitability.

7. Treating Factoring As A Fix For Structural Issues

Factoring brings cash forward, but it does not fix pricing, cost structure, or inefficient operations.

How Factoring Affects Cash Flow Reporting

Factoring changes the timing and structure of cash flow, but it does not eliminate the underlying economic reality of the transaction.

From a reporting perspective:

- Cash is received earlier than under standard payment terms

- The total cash realised is reduced due to fees

- The difference between invoice value and final cash must be tracked clearly

- Factored receivables should be monitored separately from standard collections

- Forecasting models should reflect earlier inflows and reduced final value

For finance teams, this means adjusting how receivables, cash flow, and working capital are analysed. Factoring improves liquidity, but it changes how performance should be interpreted.

Also Read:

Account Reconciliation Importance Steps

Related:

Understanding Financial Statements Beginners Guide

How Alaan Helps Finance Teams Maintain Better Cash Visibility

Factoring decisions are stronger when finance teams already have clear visibility into how cash is being used and where pressure is coming from.

Alaan does not provide factoring or receivables financing. Instead, it supports the operational layer that helps finance teams make better working capital decisions.

- Real Time Visibility Into Business Spend

Finance teams can track expenses as they happen across teams, categories, and vendors, reducing reliance on delayed reports. - Corporate Cards With Spend Controls

Controlled spending helps prevent unexpected cash outflows that increase reliance on external funding. - Structured Approval Workflows

Expenses are reviewed before they occur, improving predictability of cash requirements. - Centralised Receipt And Invoice Capture

Documentation is linked to transactions, making it easier to track obligations and verify costs. - Cleaner Reconciliation And Reporting

With structured data and integrations into accounting systems, finance teams can maintain more accurate financial records.

By improving visibility into cash outflows and expense behaviour, Alaan helps businesses understand whether factoring is truly necessary and how much liquidity they actually need.

Also Read:

Modern Expense Management Guide

Related:

Track And Manage Business Expenses

Conclusion

The cost of factoring accounts receivable goes beyond the headline fee. It includes the factoring rate, advance structure, reserve holdback, additional charges, and the timing of customer payments.

For finance teams, the decision should not be based on speed alone. Factoring improves cash flow timing, but it reduces the total amount received. The trade-off must be evaluated against margins, customer risk, and operational needs.

Factoring can be effective when used selectively and with clear visibility into costs. However, relying on it without strong financial discipline can lead to higher long-term costs.

If you want to improve how your business tracks and manages cash, you can explore how Alaan helps finance teams maintain visibility, control expenses, and keep financial data accurate. Book a demo to see how better spend management supports stronger cash flow decisions.

Frequently Asked Questions

1. Why Is The Advance Rate Not The Same As The Cost Of Factoring

The advance rate determines how much cash is received upfront, while the cost is determined by fees and charges deducted from the invoice value.

2. Can Factoring Fees Increase If Customers Pay Late

Yes, some factoring agreements apply fees over time, which means late customer payments can increase the total cost.

3. Is Accounts Receivable Factoring Cheaper Than A Business Loan

It depends on the structure, fees, and risk profile. Factoring may be easier to access but can be more expensive depending on terms.

4. Does Factoring Accounts Receivable Affect Customer Relationships

In some cases, customers may interact directly with the factoring company for payment, which can affect communication and perception.

5. Should A Business Factor All Invoices Or Only Selected Ones

Many businesses factor selectively, focusing on specific customers, invoices, or periods where cash flow needs are higher.

6. How Should Factored Receivables Be Tracked In Financial Reports

Factored receivables should be tracked separately, with clear visibility into fees, reserves, and final cash realised to maintain accurate reporting.