The most expensive tax mistake in your LLC probably will not come from the FTA. It will come from expenses your company cannot properly explain six months later, such as a supplier payment without a compliant invoice or a founder's expense hidden within operational spend. Even the missing receipt that transforms a deductible business cost into taxable profit.

In fact, most UAE businesses are not overpaying tax because they earn more. They are overpaying because their financial visibility breaks long before filing season begins. That pressure is rising fast, with the UAE’s Federal Tax Authority now overseeing more than 640,000 corporate tax registrations.

For UAE businesses, LLC income tax is no longer just about compliance. It is about whether your operational systems are quietly increasing your tax exposure without you even realising it.

Key Takeaways:

- Corporate Tax Is Based on Profit: UAE LLCs pay 0% tax up to AED 375,000 taxable profit and 9% above it, making expense tracking critical to lowering tax exposure.

- Undocumented Spend Creates “Shadow Profit”: Missing invoices, invalid TRNs, and founder-related spending can turn already-spent money into taxable income.

- Not Every Expense Is Fully Deductible: Client entertainment is often only 50% deductible, while fines and personal expenses remain non-deductible.

- The UAE Is Tightening Financial Visibility: With 640,000+ Corporate Tax registrations and e-invoicing rollout, businesses now need stronger audit trails and real-time documentation.

- Operational Control Helps Reduce Leakage: Businesses are increasingly using systems like Alaan to centralise approvals, invoices, spend tracking, and payments before leakage compounds.

What Is LLC Income Tax in the UAE?

LLC income tax in the UAE refers to the Corporate Tax applied on the taxable profits of Limited Liability Companies operating in the country. But one of the biggest misconceptions businesses still have is this: the UAE is not taxing your revenue — it is taxing what remains after allowable business expenses, adjustments, exemptions, and deductions are properly accounted for.

Under the UAE Corporate Tax regime:

- Taxable income up to AED 375,000 is taxed at 0%,

- Taxable income above AED 375,000 is taxed at 9%.

For LLCs, this changes how businesses think about everyday operations. Expense categorisation, procurement controls, invoice tracking, founder withdrawals, related-party transactions, and VAT-compliant documentation now directly affect how much profit becomes taxable at the end of the financial year.

Another important shift is that Corporate Tax applies across mainland UAE entities regardless of the owner’s nationality. Many businesses also assume free zone LLCs are automatically exempt, but eligibility depends on whether they meet the conditions of a Qualifying Free Zone Person under the UAE Corporate Tax Law.

Most importantly, LLC income tax is not just a year-end accounting event anymore. The UAE’s tax framework increasingly expects businesses to maintain proper transaction records, supplier documentation, financial visibility, and audit-ready reporting throughout the year, not only during filing season.

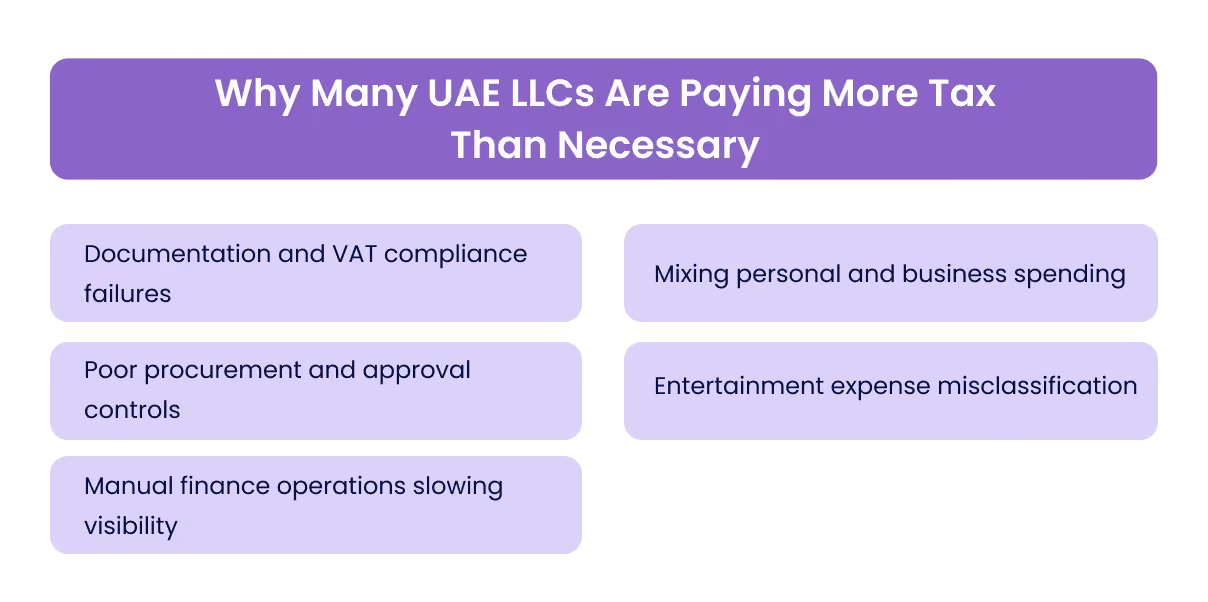

Why Many UAE LLCs Are Paying More Tax Than Necessary

Under the UAE Corporate Tax framework, expenses are generally deductible only when they are incurred “wholly and exclusively” for business purposes and properly documented. That sounds straightforward in theory, but operationally, this is where many LLCs quietly lose money.

Some of the biggest reasons UAE LLCs end up increasing their taxable profit unnecessarily include:

- Documentation and VAT compliance failures

Missing invoices, invalid TRNs, incomplete receipts, and weak audit trails can simultaneously weaken VAT recovery and Corporate Tax deductibility, turning legitimate operational spending into avoidable taxable exposure. - Mixing personal and business spending

Founder meals, travel, subscriptions, or personal purchases routed through company accounts can create partial or fully non-deductible expense exposure. - Poor procurement and approval controls

Off-policy purchases, duplicate vendor payments, and fragmented department spending often create “invisible leakage” that finance teams only discover after taxable profit has already been inflated. - Entertainment expense misclassification

Many businesses still incorrectly assume client entertainment is fully deductible, even though UAE Corporate Tax rules restrict deductibility for many entertainment-related expenses to 50%. - Manual finance operations slowing visibility

Businesses still dependent on spreadsheets, WhatsApp approvals, and delayed reconciliations often struggle to identify non-deductible or high-risk expenses early enough to correct them properly.

Want a clearer estimate of how much Corporate Tax your UAE LLC may actually owe? Try the Alaan Corporate Tax Calculator to quickly assess your potential tax liability based on your business profits and deductions.

Even businesses that understand the basics of Corporate Tax often make operational decisions based on assumptions that no longer hold true under the UAE’s evolving tax framework.

The Biggest Misconceptions About LLC Income Tax in the UAE

One of the biggest problems with the UAE’s Corporate Tax rollout is that many LLC owners still operate using assumptions from the pre-tax era. The result is not just compliance confusion; it is businesses making financial decisions based on rules they only partially understand.

Here are some of the most common misconceptions still affecting UAE LLCs in 2026:

Understanding how the FTA actually treats different expense categories is where Corporate Tax planning becomes operational instead of theoretical.

Also Read: B2B VAT Rules in the UAE: A Practical Guide for Businesses

What Expenses UAE LLCs Can and Cannot Deduct

For many UAE LLCs, the real challenge is knowing which expenses actually survive Corporate Tax scrutiny later. Two businesses can spend the same amount operationally and still report very different taxable profits depending on how those expenses are structured, documented, and classified throughout the year.

Here are some of the most important expense categories UAE businesses should understand in 2026:

The real financial impact begins when these documentation gaps and restricted expenses start compounding across hundreds of everyday transactions.

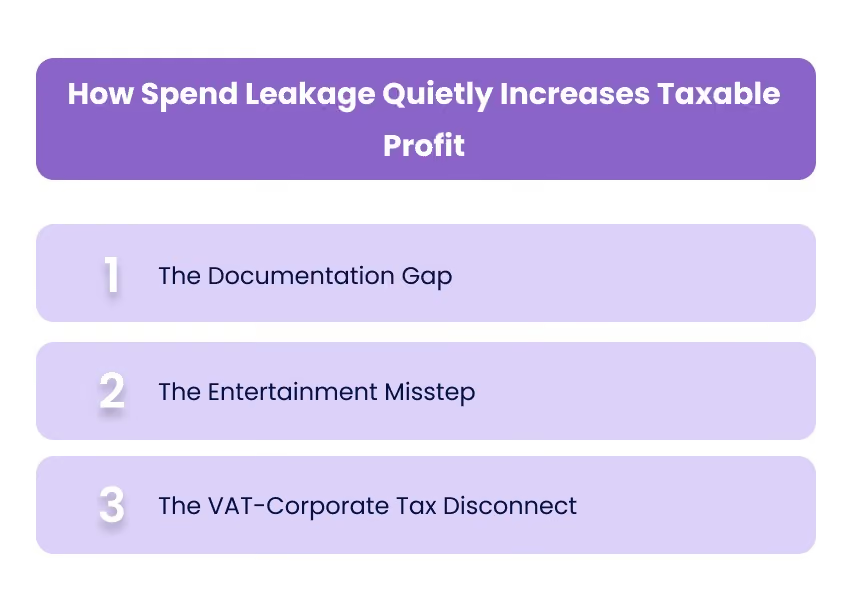

How Spend Leakage Quietly Increases Taxable Profit

Spend leakage has evolved from a minor accounting headache into a direct drain on your bottom line. For a UAE Limited Liability Company, every dirham spent that lacks a compliant audit trail is effectively treated by the Federal Tax Authority as profit that never left your pocket.

In fact, spend leakage creates a financial disconnect through three specific pressure points:

- The Documentation Gap: Under the wholly and exclusively rule, an expense without a valid, TRN-compliant invoice is legally invisible to the FTA. If your LLC has AED 100,000 in leaked spending, ranging from unrecorded petty cash to untracked digital subscriptions, that amount is added back to your taxable income. You essentially pay a 9% penalty on money the business has already spent.

- The Entertainment Misstep: While the earlier sections of this guide highlight that client hospitality is only 50% deductible, leakage occurs when the specific business purpose of a meeting isn't recorded at the moment of spend. Without this real-time context, even legitimate business lunches are often disqualified in full during a review, turning a necessary commercial cost into a 100% taxable event.

- The VAT-Corporate Tax Disconnect: By 2026, the UAE’s digital tax systems will have become increasingly integrated. A leaked expense typically results in a double loss: you fail to recover the 5% input VAT, and you lose the 9% Corporate Tax deduction. This creates a 14% total loss on every undocumented transaction, making invisible spending far more expensive than it appears.

Also Read: UAE E-Invoicing Regulatory Framework 2025–2026 Guide

Why Internal Friction Triggers External Scrutiny

Fragmented spending, such as small, recurring SaaS fees or vendor payments made outside of formal procurement, often creates high-frequency leakage. While these individual gaps may seem small, they signal to tax authorities that your internal controls are insufficient.

In the current enforcement climate, these patterns can trigger a Comprehensive Tax Audit, placing your entire financial history under a microscope.

To see how this plays out practically, it helps to look at how small operational gaps can snowball into real tax liability over a single financial year.

How a UAE LLC Loses Money Before Filing Taxes

To understand how spend leakage functions in practice, consider a typical service-based consultancy operating in Dubai. In 2026, this firm reported healthy revenue, but at the end of the financial year, the leadership found that the company's bank balance did not align with its reported taxable profit.

The gap between actual operational spending and what the Federal Tax Authority (FTA) considers a deductible expense created a significant hidden liability.

The Breakdown of the Loss

The business spent AED 85,000 on these items throughout the year. However, because these costs were either legally restricted, poorly documented, or personal in nature, the FTA ignores them during the tax calculation.

As a result, the company is required to pay 9% tax on that AED 85,000 as if it were still sitting in the company's bank account as profit. This effectively costs the firm AED 7,650 in unnecessary tax payments; capital that could have been reinvested into growth or staff bonuses had the spending been captured and classified correctly.

As Corporate Tax enforcement matures in the UAE, visibility is becoming less about bookkeeping convenience and more about financial defensibility.

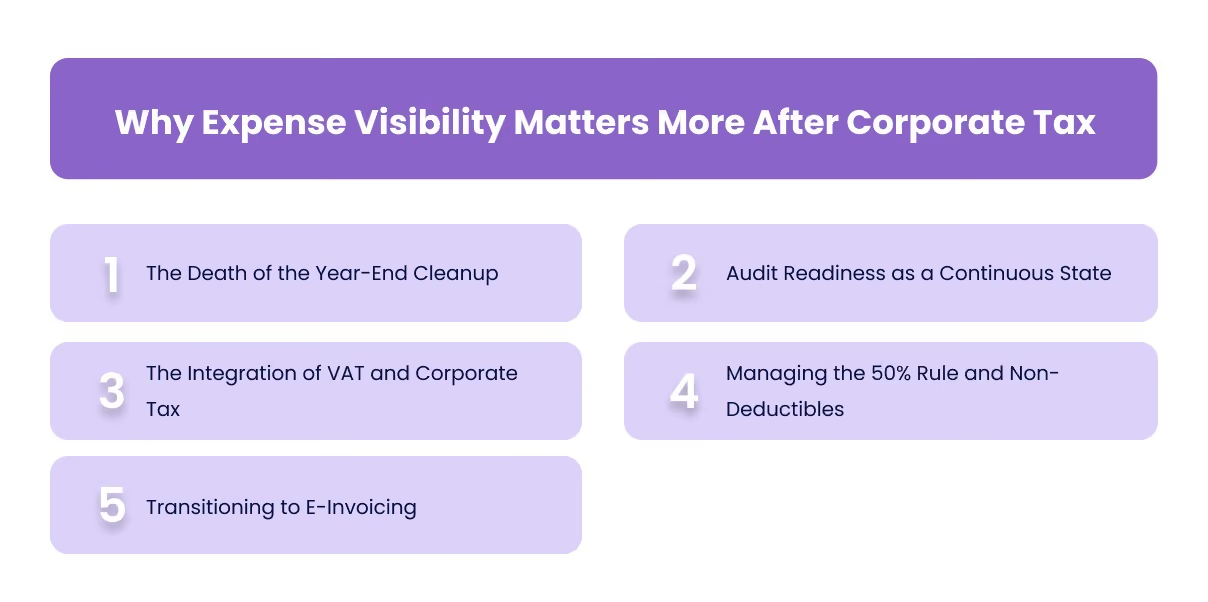

Why Expense Visibility Matters More After Corporate Tax

With Corporate Tax now fully operational, the distance between your daily spending and your year-end tax return must be zero. Here is why seeing every dirham in real-time is the only way to protect your LLC.

1. The Death of the Year-End Cleanup

Historically, many UAE businesses waited until the end of the financial year to clean up their books. Under the new regime, this approach is a major liability. The FTA increasingly expects transaction-level visibility, where every expense is recorded, categorised, and backed by evidence at the time it occurs.

Waiting six months to find a missing invoice often means the deduction is already lost, as retrospective documentation is rarely accepted during a formal review.

2. Audit Readiness as a Continuous State

In 2026, audits are no longer random; they are risk-based and data-driven. The FTA’s digital systems look for inconsistencies between your VAT filings and your Corporate Tax declarations.

- The 48-Hour Rule: If the FTA requests supporting records, businesses are often required to produce them within a very tight window (sometimes as little as 48 hours).

- The Buried Detail: Without real-time visibility, identifying the specific business purpose for an obscure payment made months ago becomes nearly impossible, leading to a disallowed deduction and potential penalties.

3. The Integration of VAT and Corporate Tax

Your VAT records are now the primary evidence for your Corporate Tax claims. If you have full visibility, you can ensure that every supplier invoice includes the necessary Tax Registration Number (TRN) and meets the mandatory formatting requirements.

If an expense is visible enough to recover VAT, it is usually "visible" enough to survive Corporate Tax scrutiny. Without this symmetry, you risk paying tax twice on the same transaction.

Also Read: Preparing UAE VAT Tax Invoice Format

4. Managing the 50% Rule and Non-Deductibles

As highlighted in our earlier breakdown, not all spending is treated equally. Real-time visibility allows you to tag expenses as they happen.

- Automated Tagging: Tagging a meal as Client Entertainment immediately triggers the 50% disallowance in your tax projections, giving you a real-time view of your true tax liability.

- Fines and Personal Spend: Instant visibility prevents government fines or shareholder personal expenses from being accidentally mixed into operational spend, which is a common red flag that triggers deeper FTA investigations.

5. Transitioning to E-Invoicing

With the UAE’s move toward mandatory e-invoicing starting in mid-2026, the FTA will soon have a direct window into your B2B transactions. Expense visibility is no longer just about what you see; it is about what the government sees. Ensuring your internal systems are ready for this level of transparency is the difference between a seamless filing and a compliance crisis.

For UAE LLCs, reducing tax leakage now depends less on year-end corrections and more on how operational systems are structured throughout the year.

How UAE LLCs Should Prepare for 2026

The transition from a tax-free environment to a structured corporate tax regime requires more than just a change in accounting software. To protect your profit margins and ensure full compliance in 2026, UAE Limited Liability Companies must adopt a proactive, year-round strategy.

The following steps are essential for any LLC looking to navigate the current fiscal landscape effectively:

1. Evaluate Eligibility for Small Business Relief

The UAE government has extended Small Business Relief (SBR) to support resident taxable persons. If your LLC’s revenue remains below the AED 3 million threshold for the current and previous tax periods, you may be able to elect for this relief.

- The Benefit: Your business will be treated as having no taxable income for that period.

- The Caveat: You must still register for Corporate Tax and maintain rigorous records to prove your revenue stayed below the limit.

Also Read: How to File Business Taxes for Small Businesses

2. Standardise Procurement and Documentation

In 2026, the Federal Tax Authority (FTA) is placing greater emphasis on the quality of documentation. A simple bank statement is no longer sufficient to justify an expense.

- Collect Valid Tax Invoices: Ensure every supplier provides a full tax invoice that includes their TRN and your company’s legal name.

- Define Expenditure Policies: Implement clear rules on what constitutes a business expense versus a personal one to avoid non-deductible leaks before they happen.

3. Review Related-Party Transactions

For many LLCs, transactions between sister companies or payments to shareholders are common. Under the Corporate Tax Law, these must meet the Arm’s Length Principle.

- Market Value: Ensure that any services, loans, or rent payments between related parties are conducted at fair market value.

- Transfer Pricing Documentation: Maintain a transfer pricing file to justify these costs, as the FTA closely scrutinises these transactions to prevent profit shifting.

4. Align VAT and Corporate Tax Reporting

One of the most frequent mistakes LLCs make is having a mismatch between their VAT returns and their Corporate Tax filings.

- Reconcile Quarterly: Regularly compare your VAT-reported turnover and expenses with your ledger.

- Address Discrepancies: If your VAT returns show AED 1 million in revenue but your Corporate Tax filing shows AED 900,000, it will likely trigger an automated red flag within the FTA’s risk engine.

5. Prepare for the E-Invoicing Rollout

The UAE is moving toward a mandatory e-invoicing framework (the Decentralised Revenue Model) through 2026.

- Digital Integration: Ensure your financial systems can generate and receive structured e-invoices that comply with the new UAE standards.

- Real-Time Reporting: This shift means the FTA will have near-instant visibility into your B2B transactions, making manual, retrospective adjustments a thing of the past.

6. Conduct a Professional Tax Impact Assessment

If your LLC operates across different jurisdictions or holds a Free Zone license, your tax position is significantly more complex.

- Qualifying Income: Determine if your Free Zone LLC meets the strict criteria to remain a Qualifying Free Zone Person (QFZP) at a 0% rate.

- Deduction Optimisation: Work with a tax consultant to identify all legitimate deductions, such as capital allowances and interest expenditure limits, that can legally reduce your taxable profit.

This is exactly why many UAE finance teams are rethinking how spending, approvals, invoices, and accounting workflows connect operationally.

How Alaan Helps UAE LLCs Reduce Tax Leakage

For many UAE LLCs, tax leakage is not caused by major fraud or accounting failure. It usually builds slowly through operational blind spots: expenses approved without context, invoices uploaded too late, payments spread across disconnected systems, and finance teams trying to reconstruct business intent months after the transaction happened.

This is the operational gap Alaan is designed around.

Rather than functioning only as a corporate card provider or expense tracker, Alaan operates as a spend management infrastructure layer for UAE businesses. The platform connects employee spending, approvals, invoices, reimbursements, accounting sync, and vendor payments into one system, so transactions remain traceable from the moment money leaves the business.

Some of the ways Alaan helps reduce spend leakage operationally include:

- Alaan Corporate Cards connect transactions directly to employees, departments, approvals, merchants, and receipts, reducing the number of expenses that later become difficult to justify or reconcile.

- Real-time spend visibility gives finance teams earlier visibility into missing invoices, duplicate subscriptions, unusual transactions, or off-policy purchases before month-end reconciliation begins.

- Expense management workflows centralise receipts, reimbursements, and supporting documentation so finance records are not fragmented across email threads, spreadsheets, and chat approvals.

- Automated accounting sync reduces manual reconciliation pressure and lowers the probability of transaction mismatches between operational records and accounting systems.

- Invoice capture and categorisation tools help businesses retain supporting proof closer to the point of transaction instead of depending on retrospective collection later.

- Department-level spend controls and budgets help reduce uncontrolled operational purchases that often create undocumented or non-deductible spending exposure over time.

- SuperPay, Alaan’s vendor and international payment infrastructure, centralises supplier payouts, payment approvals, invoice mapping, and transfer tracking into one workflow rather than spreading them across banking portals and manual finance processes.

- Unified spend and payment records make it easier for finance teams to connect invoices, approvals, payment trails, and accounting entries when preparing for VAT or Corporate Tax reviews.

Conclusion

The businesses that will handle Corporate Tax best over the next few years will not necessarily be the ones spending less. They will be the ones who can explain their spending fastest.

For many founders, the next practical step is not hiring larger finance teams or overcomplicating compliance. It is tightening the small habits that shape taxable profit over time: reviewing recurring software spend every quarter, creating stricter rules around personal purchases, standardising vendor invoices early, and reducing how many transactions live across scattered chats, emails, and spreadsheets.

That operational clarity is exactly why more UAE businesses are adopting platforms like Alaan to bring spending, approvals, invoices, reimbursements, and payments into one connected workflow instead of trying to piece everything together months later.

If you are evaluating how your LLC can reduce spend leakage before it turns into avoidable tax exposure, exploring a personalised demo with Alaan could be a useful place to start.

FAQs

1. Does every LLC in the UAE have to pay Corporate Tax?

No. UAE Corporate Tax applies only when an LLC earns taxable profit above AED 375,000. Taxable profit below that threshold is currently taxed at 0%, while profit above it is taxed at 9%. Certain Free Zone entities may also qualify for different treatment if they meet QFZP conditions.

2. Are all business expenses tax deductible in the UAE?

No. Expenses must be incurred wholly and exclusively for business purposes to qualify as deductible. Certain categories, such as fines, personal expenses, and portions of entertainment spending, may be restricted or fully non-deductible.

3. Is client entertainment fully deductible under UAE Corporate Tax?

Usually not. Many client entertainment and hospitality expenses are only 50% deductible under UAE Corporate Tax rules, depending on how the expense is classified and documented.

4. What records should UAE LLCs maintain for Corporate Tax compliance?

Businesses should maintain tax invoices, receipts, approvals, contracts, accounting records, VAT documents, payroll records, and supporting transaction evidence. The Federal Tax Authority generally requires businesses to retain records for at least seven years.

5. What triggers higher Corporate Tax exposure for UAE LLCs?

Poor invoice management, undocumented operational spending, personal expenses routed through company accounts, VAT mismatches, and weak approval controls are some of the most common reasons businesses unintentionally increase taxable profit.