Monthly cash flow is where revenue assumptions meet actual bank movement. A business may invoice customers, approve supplier payments, process card spend, reimburse employees, and settle taxes across the same month, but those activities do not always appear clearly in one place.

This is why timing discipline matters. JP Morgan Chase Institute analysed more than 470 million transactions across 597,000 small businesses and found that half held a cash buffer large enough to cover only 27 days of typical outflows. Monthly cash flow calculations become more useful when they show not just whether cash increased, but how much room the business has before pressure builds.

For finance teams, calculating monthly cash flow means tracking actual cash received, actual cash paid, opening cash balance, and closing cash balance. The formula is simple, but the result is only reliable when card spend, reimbursements, supplier payments, VAT, subscriptions, and pending outflows are captured properly.

In this blog, we will cover how to calculate monthly cash flow, what to include in inflows and outflows, how to derive closing cash balance, and how to use this calculation to improve financial visibility and control.

TL;DR / Key Takeaways

- Monthly cash flow tracks actual cash received and paid during the month, not revenue earned or expenses recognised.

- The basic calculation is total cash inflows minus total cash outflows, but finance teams should also reconcile opening and closing balances.

- Unpaid invoices should not be counted as inflows, and delayed card spend, reimbursements, VAT, and supplier payments should not be missed from outflows.

- Monthly cash flow becomes useful when it is compared with forecasts, planned spend, and upcoming obligations.

- Real-time expense tracking, approval workflows, and reconciliation discipline make monthly cash flow calculations more reliable.

What Monthly Cash Flow Means

Monthly cash flow tracks how much cash actually moved in and out of the business during a given month. It focuses on real transactions, money received and money paid, rather than accounting entries that may not yet reflect cash movement.

This distinction is important. Revenue can be recorded before payment is collected, and expenses can be recognised before they are paid. Monthly cash flow removes that timing distortion and shows the business’s real liquidity position.

For finance teams, this becomes the most practical way to understand short-term financial health. It answers a simple but critical question: after all receipts and payments during the month, did cash increase or decrease?

Also Read: Manage Business Cash Flow Effectively

Monthly Cash Flow Formula

At its core, monthly cash flow is calculated using a straightforward structure:

Monthly Cash Flow = Total Cash Inflows − Total Cash Outflows

This shows whether the business generated positive or negative cash movement during the month.

However, to make this calculation useful for financial control, it should always be combined with opening and closing balances:

Closing Cash Balance = Opening Cash Balance + Total Cash Inflows − Total Cash Outflows

This gives a complete monthly picture:

- Opening balance shows where the business started

- Inflows show what came in

- Outflows show what went out

- Closing balance shows what remains

This structure is consistent with how cash flow statements are built and how finance teams track liquidity month to month.

What To Include In Monthly Cash Inflows

Monthly cash inflows should only include money that is actually received during the month. This sounds obvious, but in practice, it is one of the most common sources of error. Many businesses include invoiced revenue that has not yet been collected, which distorts the final calculation.

Atradius’ 2025 UAE payment practices report found that overdue invoices affect 58% of B2B sales, which is exactly why monthly cash flow should count only collected cash, not invoices that are still outstanding.

- Customer Payments Received

Payments collected against invoices during the month, regardless of when the invoice was issued. - Cash Sales

Immediate payments from customers, including retail or point-of-sale transactions. - Loan Or Financing Proceeds

Any funds received from banks or financial institutions during the month. - Owner Or Investor Contributions

Additional capital introduced into the business. - Tax Refunds Or Rebates

Any refunds received from tax authorities or other entities. - Other Cash Receipts

This may include asset sale proceeds or one-off income received in cash.

The key principle is simple: if the cash has not entered the bank or equivalent accounts during the month, it should not be counted.

Related: Understanding Trade Receivables Key Concepts

What To Include In Monthly Cash Outflows

Cash outflows should capture all payments made during the month, regardless of when the expense was recorded in the accounting system. In many businesses, this is where visibility gaps appear, especially when payments are spread across multiple tools and workflows.

To maintain accuracy, outflows must include every form of cash leaving the business.

- Payroll And Employee Costs

Salaries, bonuses, reimbursements, and related payments. - Supplier And Vendor Payments

Payments made for goods, services, or operational needs. - Rent And Utilities

Office rent, electricity, internet, and other recurring costs. - Software And Subscriptions

SaaS tools, licences, and recurring digital expenses. - Loan Repayments

Principal and interest payments made during the month. - Taxes And VAT Payments

Any statutory payments made within the period. - Inventory Or Material Purchases

Cash spent on stock or production inputs. - Capital Expenditure Payments

Payments made for equipment or long-term assets. - Employee Expense Spend

Corporate card transactions, travel expenses, and operational spending.

In practice, missing smaller but frequent expenses, especially card spend and reimbursements, can significantly distort monthly cash flow.

Also Read: Track And Manage Business Expenses

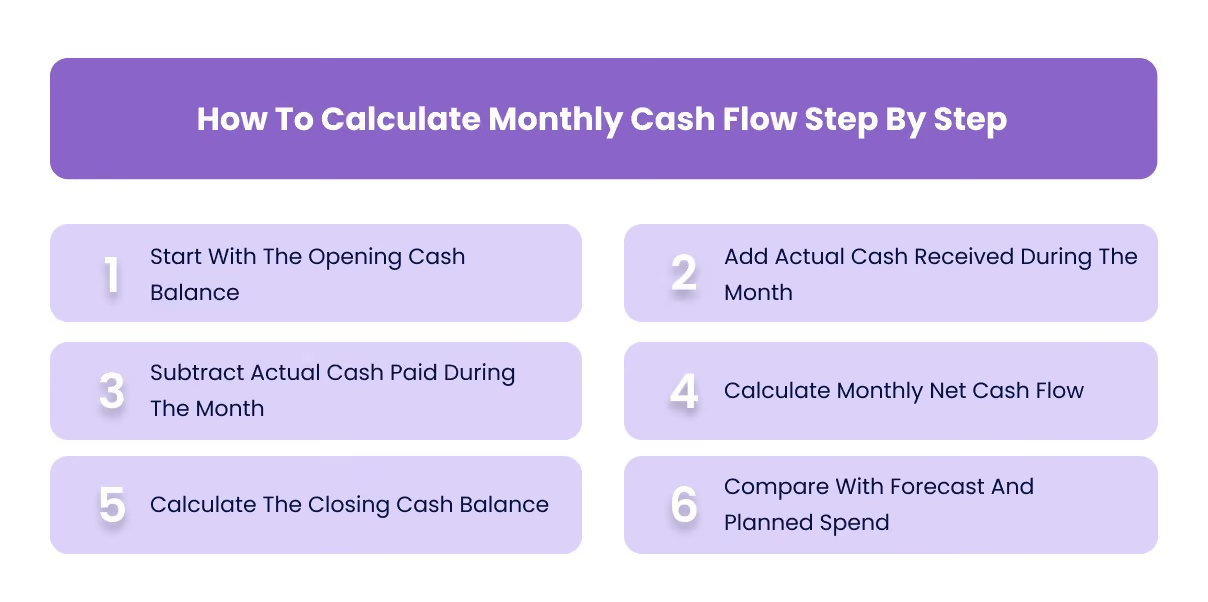

How To Calculate Monthly Cash Flow Step By Step

A structured calculation ensures consistency across months and reduces the risk of missing key inputs. This process should ideally become part of the monthly finance routine.

1. Start With The Opening Cash Balance

The opening balance is the total cash available at the beginning of the month. This typically includes bank balances and any accessible cash equivalents.

This number should match the closing balance from the previous month.

2. Add Actual Cash Received During The Month

Collect all inflow data from bank statements, payment platforms, and other sources. Only include payments that were actually received during the month.

This step ensures that the calculation reflects real liquidity rather than expected revenue.

3. Subtract Actual Cash Paid During The Month

Capture all outgoing payments, including vendor payments, payroll, corporate card spend, reimbursements, subscriptions, and taxes.

This is where fragmented systems often create gaps. Missing even small categories of spend can lead to inaccurate results.

4. Calculate Monthly Net Cash Flow

Subtract total outflows from total inflows.

- A positive result means the business generated more cash than it spent.

- A negative result indicates a cash deficit for the month.

This number shows the direction of cash movement but does not give the full picture on its own.

5. Calculate The Closing Cash Balance

Add the net cash flow to the opening balance.

This gives the cash position at the end of the month. It should align with actual bank balances after accounting for timing differences.

6. Compare With Forecast And Planned Spend

The calculation becomes significantly more useful when compared with expected inflows and planned outflows.

This helps finance teams:

- Identify gaps between expected and actual cash movement

- Adjust payment timing

- Improve future cash flow forecasts

Related: Difference Between Budgeting And Financial Forecasting

Example Monthly Cash Flow Calculation

A simple example helps illustrate how the calculation works in practice.

- Opening Cash Balance: AED 120,000

- Cash Inflows During The Month: AED 250,000

- Cash Outflows During The Month: AED 210,000

Monthly Net Cash Flow = AED 40,000

Closing Cash Balance = AED 160,000

On the surface, this looks like a healthy month. The business generated positive cash flow and increased its cash position.

However, the real insight comes from understanding the composition of those numbers. If inflows included delayed customer payments from previous months, or if outflows excluded upcoming supplier obligations, the result may not reflect ongoing stability.

This is why monthly cash flow should always be analysed alongside timing, consistency, and upcoming commitments.

How Monthly Cash Flow Differs From Profit

Monthly cash flow and profit often move in different directions, especially in businesses that operate on credit terms or have delayed payment cycles.

Revenue may be recognised before customers pay. Expenses may be recorded before cash leaves. Non-cash items such as depreciation affect profit but do not impact cash. On the other hand, loan repayments and inventory purchases reduce cash even if they are not fully reflected in profit for that period.

This creates timing gaps between what the financial statements show and what the bank balance reflects.

Understanding this difference is critical. A business that appears profitable may still face cash shortages if collections are delayed or payments are front-loaded.

Related: Understanding Financial Statements Beginners Guide

Which Monthly Cash Flow Method Should A Business Use

Monthly cash flow can be calculated using two approaches. While both are valid, they serve slightly different purposes depending on how the business wants to use the data.

1. Direct Method

The direct method calculates cash flow by tracking actual cash received and actual cash paid during the month. It focuses on real inflows and outflows, making it the most practical approach for day-to-day financial control.

For most businesses, especially those managing monthly liquidity closely, this method is more useful. It provides a clearer view of how cash is moving through operations and makes it easier to identify where delays or inefficiencies exist.

2. Indirect Method

The indirect method starts with profit and adjusts for non-cash items and changes in working capital. This approach is commonly used in formal financial reporting.

While it is useful for preparing financial statements, it is less intuitive for understanding monthly cash movement because it relies on accounting adjustments rather than actual transactions.

For operational decision-making, the direct method is usually more actionable.

Related: Account Reconciliation Importance Steps

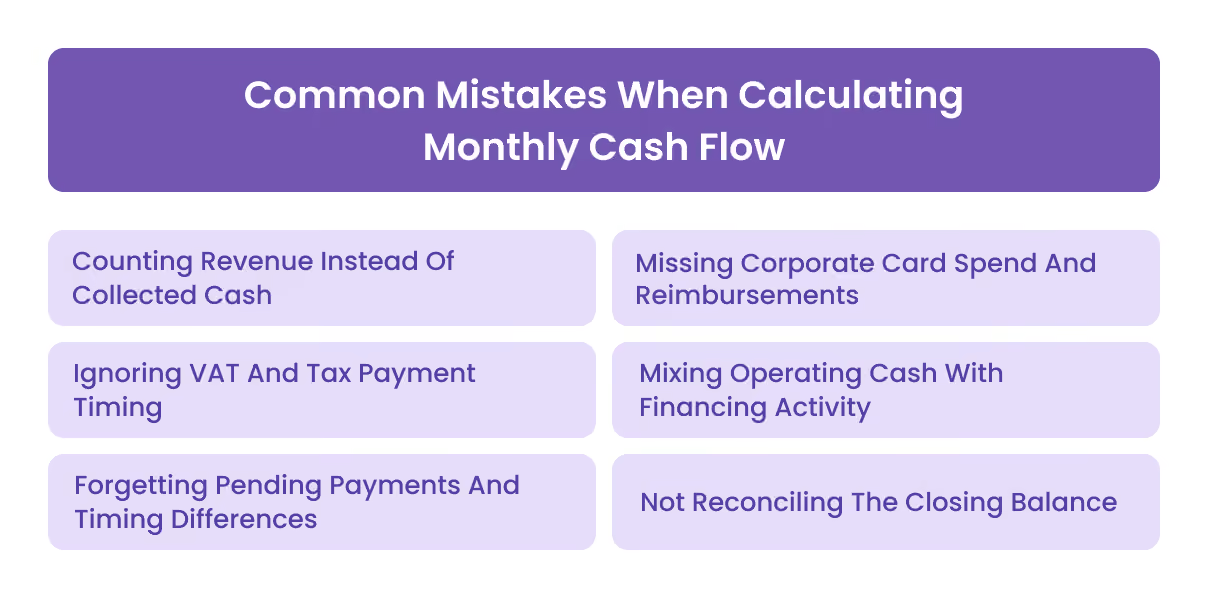

Common Mistakes When Calculating Monthly Cash Flow

Even though the formula is straightforward, the calculation can become unreliable if key inputs are incomplete or misclassified. These mistakes often lead to incorrect conclusions about the business’s cash position.

1. Counting Revenue Instead Of Collected Cash

Including invoiced revenue that has not yet been paid inflates inflows and gives a misleading view of liquidity.

2. Missing Corporate Card Spend And Reimbursements

Expenses made through cards or employee reimbursements are often recorded late or outside the main system, leading to understated outflows.

3. Ignoring VAT And Tax Payment Timing

Tax obligations can create significant cash outflows that are not evenly distributed across months. Ignoring these can distort monthly results.

4. Mixing Operating Cash With Financing Activity

Loan inflows or repayments can temporarily improve or reduce cash flow but do not reflect the underlying operating performance of the business.

5. Forgetting Pending Payments And Timing Differences

Payments initiated at the end of the month or collections received just after month-end can create timing gaps if not properly accounted for.

6. Not Reconciling The Closing Balance

If the calculated closing balance does not match actual bank balances, the data used in the calculation is incomplete or inaccurate.

Also Read: Corporate Card Reconciliation Guide

How To Use Monthly Cash Flow For Better Decisions

Calculating monthly cash flow is only the first step. The real value comes from how the results are used to guide financial decisions and improve control.

A consistent monthly view helps finance teams identify patterns rather than reacting to isolated events. It becomes easier to see whether cash flow issues are recurring or temporary, and whether they are driven by collections, spending, or timing mismatches.

This insight can be applied in several ways:

- Adjusting payment timing to avoid unnecessary cash pressure

- Prioritising collections where delays are increasing

- Identifying categories of spend that are growing faster than expected

- Planning for upcoming obligations such as payroll, rent, or taxes

- Setting minimum cash thresholds to maintain operational stability

Over time, this turns cash flow from a reporting exercise into a decision-making tool. It allows businesses to move from reactive adjustments to more predictable financial management.

Also Read: Cash Management Control System UAE

How Alaan Helps Businesses Track Cash Movement More Reliably

Calculating monthly cash flow is only as reliable as the underlying data. In many businesses, that data is fragmented. Expenses may be spread across bank transfers, corporate cards, reimbursements, invoices, and subscriptions, making it difficult to capture a complete picture of cash outflows in real time.

At Alaan, we focus on improving the accuracy and visibility of that data so finance teams can work with a more reliable view of cash movement.

- Corporate Cards With Built In Spend Controls

Businesses can issue cards with defined limits and merchant restrictions, helping control how cash is spent before it leaves the business. - Structured Approval Workflows Before Spend Happens

Expenses can be routed through approval flows, ensuring that spending decisions are reviewed and aligned with budgets. - Real Time Visibility Into Expenses

Finance teams can see spend as it happens, rather than waiting for end-of-month reports to understand cash outflows. - Centralised Receipt And Invoice Capture

All supporting documents are linked directly to transactions, reducing record gaps and improving accuracy. - Accurate Payment Impact Before Cash Leaves The Business (SuperPay)

For invoice-based or transfer payments, SuperPay allows finance teams to see the full impact of a payment before execution, including FX rates, fees, and final settlement amounts. This helps ensure that calculated cash outflows align closely with actual cash movement, improving the accuracy of monthly cash flow reporting. - Seamless Accounting Integration

Integrations with systems like Xero, QuickBooks, NetSuite, and Microsoft Dynamics ensure that expense data flows cleanly into accounting systems, reducing manual effort.

By improving how expenses are captured, approved, and recorded, Alaan helps ensure that monthly cash flow calculations reflect actual business activity rather than incomplete or delayed data.

Conclusion

Calculating monthly cash flow is not complex, but making it reliable requires discipline. A business needs to consistently track actual cash received, actual cash paid, and reconcile those movements against its opening and closing balances. Without that structure, even a correct formula can produce misleading results.

The real value of monthly cash flow comes from how it is used. When reviewed regularly, it helps finance teams anticipate pressure, plan payments more effectively, and maintain a clearer view of liquidity. Over time, it shifts cash management from reactive adjustments to more predictable control.

If you want to improve how your business tracks and manages cash movement, you can explore how Alaan helps finance teams maintain visibility, enforce approvals, and keep expense data accurate from transaction to reconciliation. Book a demo to see how better spend control can lead to more reliable cash flow management.

Frequently Asked Questions

1. What Is The Formula To Calculate Monthly Cash Flow

The basic formula is:

Monthly Cash Flow = Total Cash Inflows − Total Cash Outflows

To get a complete view, you should also calculate:

Closing Cash Balance = Opening Cash Balance + Inflows − Outflows

2. Is Monthly Cash Flow The Same As Monthly Profit

No, monthly cash flow and profit are different. Profit is based on accounting recognition of revenue and expenses, while cash flow reflects actual money received and paid. Timing differences between invoicing and payments create this gap.

3. Should Unpaid Invoices Be Included In Monthly Cash Flow

No, unpaid invoices should not be included. Monthly cash flow only considers cash that has actually been received during the period.

4. How Do You Calculate Closing Cash Balance For The Month

Closing cash balance is calculated by adding net cash flow to the opening balance:

Closing Balance = Opening Balance + (Inflows − Outflows)

This should match the actual bank balance after adjustments.

5. What Is A Good Monthly Cash Flow For A Business

A good monthly cash flow is generally positive and consistent. However, the right level depends on the business model, payment cycles, and operating costs. Stability is often more important than short-term spikes.

6. How Often Should A Business Review Monthly Cash Flow

Monthly cash flow should be reviewed at least once every month. Many businesses also track it weekly to improve visibility and respond faster to changes in cash position.