Overseas business payments sit at the centre of global growth. If you pay international suppliers, remote contractors, freight partners, marketplaces, or subscription vendors, the quality of your payment process directly affects cost control, delivery timelines, and cash flow predictability.

For finance leaders across the UAE and wider MENA, the problem is rarely “how do we send money.” It is how to run a repeatable business foreign payment process with clear costs, fewer delays, clean compliance, and fast reconciliation. Market research estimates the UAE’s cross-border remittance and transfer market at roughly USD 39 billion, which gives a sense of how much volume flows through international rails.

This guide breaks down how overseas payments work in practice, where cost and delays hide, and what to change so international payments stop becoming exceptions.

TL;DR

- Overseas business payments become expensive when cost and tracking are unclear at approval time.

- Most recurring problems come from fee deductions, FX spread visibility gaps, cut-off timing, and missing payment context.

- Separating invoice-based supplier transfers from merchant spend improves control and reduces operational noise.

- Standardised beneficiary data and upfront documentation reduce holds, failures, and return cycles.

- A structured workflow makes reconciliation faster because invoice, approval, payment, and confirmation stay connected.

What Overseas Business Payments Include

Most finance teams treat overseas payments as “supplier transfers,” but cross-border spend usually shows up in multiple forms. Defining scope up front prevents blind spots in cost control, compliance, and reconciliation.

1. Supplier And Trade Payments

These are invoice-based payments to overseas vendors for inventory, raw materials, logistics, or professional services. They typically require bank-account payouts, payment references, and supporting documents to avoid delays or returns.

2. Contractor And Service Provider Payouts

These are overseas payments to agencies, consultants, and freelancers. The operational risk is usually timing certainty and proof of payment, especially when contracts require settlement confirmation before work continues.

3. Merchant Payments For Digital Services

Some overseas business payments are merchant-based rather than invoice-to-bank-account. This category includes software subscriptions, advertising platforms, travel bookings, and other online services billed by card or online checkout. Alaan’s own international payment process guide explicitly calls out corporate cards as common for this type of recurring international spend.

Also Read: Understanding the Procure-to-Pay (P2P) Process

The Main Ways To Make Overseas Business Payments

Different overseas payment types need different rails. Trying to force one method across all scenarios is how finance teams end up with higher costs, weak tracking, and messy reconciliation. The methods below are the common, factual “buckets” that cover most business foreign payment flows.

1. International Bank Transfers

This is the standard route for overseas supplier invoices and contractor payouts to bank accounts. Transfers can involve intermediary routing and can take multiple business days depending on corridor, cut-offs, and compliance checks. This method is reliable for invoice-to-bank payments, but cost and tracking can be less predictable.

2. Card-Based Payments To International Merchants

Cards apply when the overseas vendor is a merchant that accepts card payments (for example, SaaS subscriptions, digital services, advertising platforms, and travel). This is not a substitute for supplier bank transfers, it’s a separate spend category.

Two factual cost notes matter here:

- Card transactions can include foreign transaction fees, typically a percentage of the transaction depending on issuer.

- Currency conversion depends on the card network/issuer rate mechanics (Visa provides an exchange rate calculator for card usage across currencies).

3. Cross-Border Payment Platforms For Business Transfers

Specialist platforms are typically used for overseas supplier payments and contractor payouts, with an emphasis on improving predictability, clearer fees/FX visibility, better tracking, and cleaner reporting compared to manual bank-portal execution.

Also Read: How International Payment Processing Works in the UAE?

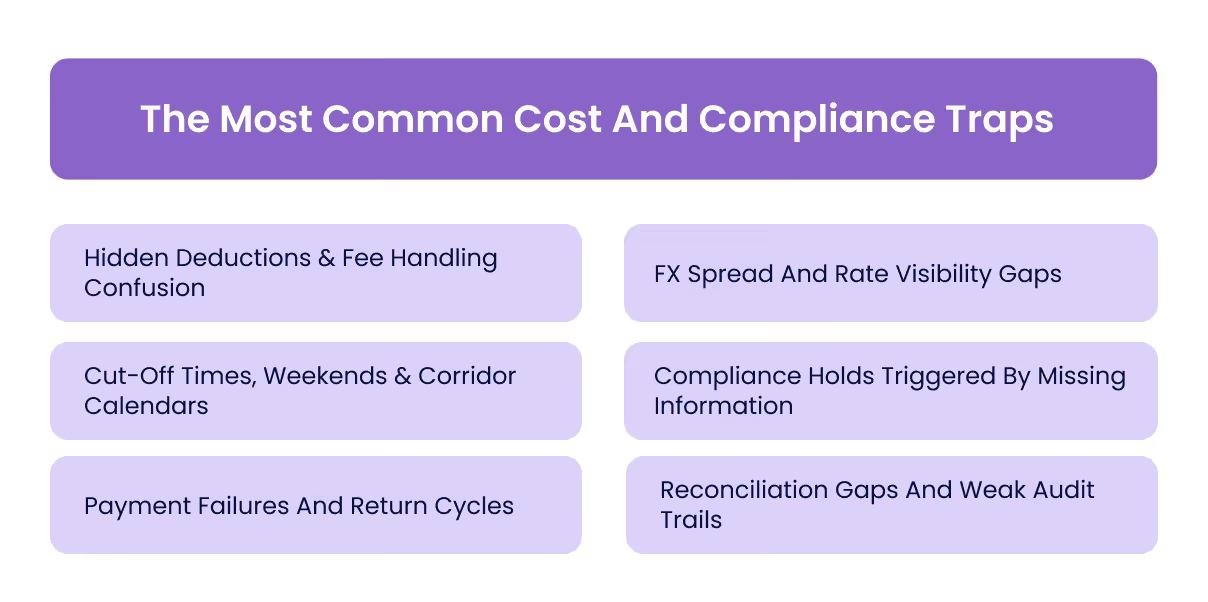

The Most Common Cost And Compliance Traps

Overseas business payments tend to look predictable until the first few exceptions hit: a supplier receives less than expected, a transfer goes “pending” for days, or an invoice can’t be reconciled cleanly at month-end. Most of these issues trace back to a handful of traps that finance teams can identify and control once they know where to look.

1. Hidden Deductions And Fee Handling Confusion

A common surprise is that the beneficiary receives less than the invoiced amount. This usually happens when fees are deducted along the route, or the fee-sharing method is not aligned with supplier expectations. The operational consequence is predictable: supplier follow-ups, shortfall top-ups, and time lost resolving avoidable disputes.

2. FX Spread And Rate Visibility Gaps

Many teams track the market rate but miss the effective rate applied at execution. The difference is usually the spread or markup. When rate visibility is unclear at approval time, budgeting and cost forecasting become less reliable, especially for recurring overseas payments.

3. Cut-Off Times, Weekends, And Corridor Calendars

International transfers run on processing windows. Missing a cut-off time can push processing to the next business day. Differences in weekends and holidays across countries can extend timelines further. The impact is strongest when payments are tied to shipment release, service delivery, or contract milestones.

4. Compliance Holds Triggered By Missing Information

Transfers can be paused when the payment purpose is unclear, the beneficiary details do not match expected records, or the documentation is incomplete. Holds often appear after initiation, which is why they create operational churn: someone must gather the right documents and respond quickly to unblock the payment.

5. Payment Failures And Return Cycles

Overseas payments can fail or be returned due to data quality issues, such as incorrect beneficiary details or missing required fields. Return cycles are expensive because they create duplicate work, delay settlement, and force finance teams into reactive follow-up mode.

6. Reconciliation Gaps And Weak Audit Trails

When invoices, approvals, payment confirmations, and FX outcomes live in different places, reconciliation becomes manual. This is where overseas payments quietly become a month-end problem, not just a payments problem.

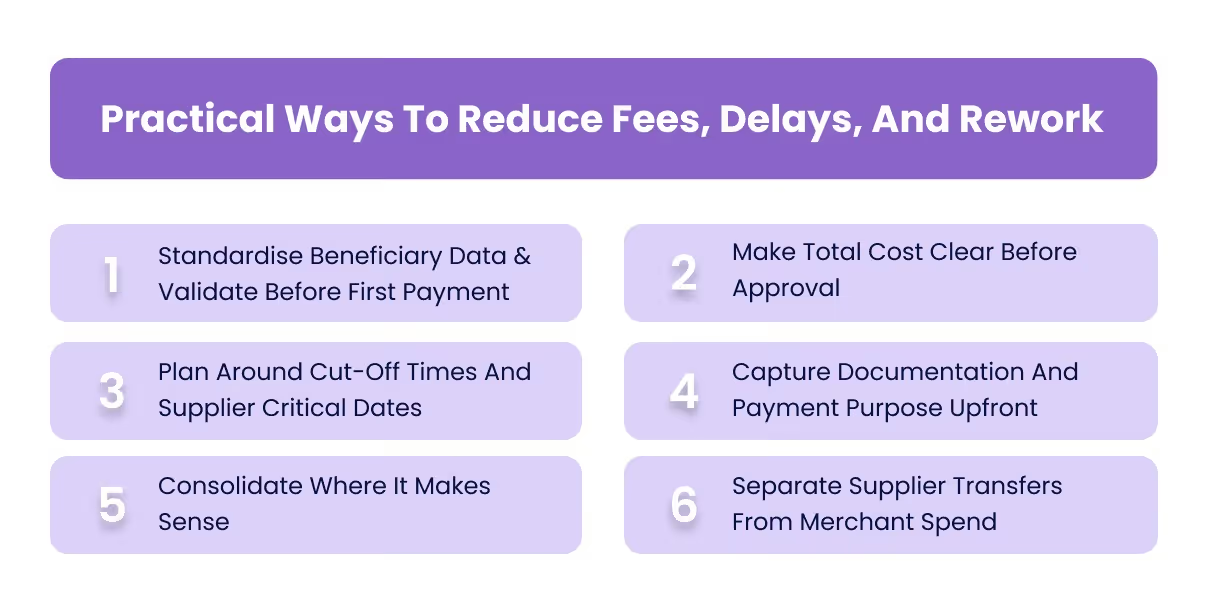

Practical Ways To Reduce Fees, Delays, And Rework

Optimising overseas business payments does not require a complete overhaul. Most improvements come from tightening inputs, enforcing governance at the approval stage, and choosing execution methods that provide cost clarity and traceable records. The actions below are designed to reduce recurring exceptions rather than solve one-off cases.

1. Standardise Beneficiary Data And Validate Before First Payment

Beneficiary errors are one of the most common drivers of delays and returns. The practical fix is to treat beneficiary details as controlled master data.

- Use A Single Approved Beneficiary Record Per Supplier, including consistent legal naming and bank details.

- Validate Details Before The First High-Value Payment, so the first transfer is not a trial run.

- Restrict Who Can Edit Beneficiary Records, and require review for changes.

2. Make Total Cost Clear Before Approval

Overseas payments become unpredictable when approvals are made without a clear view of total cost. Ideally, finance teams should be able to see how fees and FX affect the outcome before execution.

Where possible, align on:

- Expected Delivered Amount, so suppliers are not short-paid unexpectedly.

- Fee Responsibility, so deductions do not trigger disputes.

- Effective FX Rate, not just a headline market rate.

3. Plan Around Cut-Off Times And Supplier Critical Dates

Timing improves when payments are planned around processing windows rather than calendar intent. This is especially important when suppliers release goods or services only after settlement confirmation.

A practical approach is to align payment planning with:

- Cut-Off Times For The Payment Method Used.

- Local Weekends And Bank Holidays In The Destination Country.

- Supplier Timelines For Release Against Payment Confirmation.

4. Capture Documentation And Payment Purpose Upfront

Many compliance holds are avoidable if the payment purpose and supporting documentation are captured during approval instead of after initiation.

This works best when you standardise:

- Payment Purpose Format, so it is consistent and specific.

- Supporting Documents, such as invoices or contracts, stored alongside the payment record.

- Reference Fields, such as invoice number, supplier ID, and internal approval reference.

5. Consolidate Where It Makes Sense

Consolidation can reduce per-transaction fees and administrative workload, but it should not compromise supplier terms. The best candidates are recurring small payments to the same supplier or multiple invoices that can be settled together without affecting service continuity.

6. Separate Supplier Transfers From Merchant Spend

Operational control improves when you treat these as different categories. Supplier invoices typically require transfers, documentation, and tracking. Merchant spending, such as SaaS and advertising, is often better controlled through spend policies, vendor restrictions, and clean transaction data.

Also Read: Expense Management Software for Business Spend Tracking

How Alaan Helps You Manage Overseas Supplier Payments

Most overseas business payments break down when the workflow is fragmented. Invoices sit in one place, approvals happen in another, transfers are executed in a bank portal, and reconciliation is handled at month-end through manual stitching. At Alaan, we built SuperPay to bring international supplier payments into one connected flow, with clearer pricing and stronger control before funds move.

- One Workflow For Invoices, Approvals, And Cross-Border Transfers

With SuperPay, you can manage invoices, approvals, and cross-border transfers in one place, instead of treating overseas payments as a separate banking task. - Transparent FX And Predictable Costs

Cost surprises usually come from unclear FX pricing and unexpected deductions. SuperPay is built around clearer pricing and upfront FX visibility, helping finance teams reduce uncertainty around transfer costs and execution. - Built-In Controls Before Money Moves

Overseas payments become risky when they bypass approvals. SuperPay routes transfers through the same approval workflows and spend policies your organisation already uses, reducing side-channel execution and tightening governance. - Centralised Visibility And Cleaner Month-End Close

SuperPay is designed to keep payment status and context visible across cards and transfers, and to reduce reconciliation friction by making transfers structured and traceable from day one.

Conclusion

Optimising overseas business payments is not about picking a single “best” method. It is about reducing the repeatable failure points: unclear total cost, FX opacity, avoidable delays, compliance holds, and reconciliation gaps. When finance teams standardise beneficiary data, make total cost visible before approval, and keep documentation tied to the payment record, overseas payments become faster, more predictable, and easier to defend at month-end.

At Alaan, we built SuperPay to help UAE and MENA finance teams run overseas supplier payments with transparent FX, built-in approvals, centralised visibility, and a cleaner close. Book a Demo to see how SuperPay fits your payment workflows.

FAQs

1. How Long Do Overseas Business Payments Usually Take

It varies by corridor and method. SWIFT says 75% of payments on its network reach beneficiary banks within 10 minutes, but final crediting can still be delayed by compliance checks, cut-offs, bank processing, or repair cycles.

2. What Payee Details Are Typically Required For International Transfers

Common requirements include payee name, account number/IBAN, bank name, and a routing identifier (such as a national clearing code where IBAN isn’t used).

3. What Is The Best Fee Option To Avoid Short-Paying Suppliers

In many cases, choosing the option where the sender covers charges prevents the supplier receiving less than invoiced. Banks may show this as OUR (or ISO 20022 DEBT).

4. Why Do Overseas Payments Fail Even When The Bank Details Look Correct

Name mismatches, missing mandatory fields for the corridor, intermediary requirements, or inconsistent remittance information can still trigger repairs/returns. “Looks correct” is not the same as “meets corridor rules.”

5. What’s The Difference Between Sending A Transfer And Paying An Overseas Vendor Invoice

A transfer is just the movement of funds. An invoice payment process includes approvals, supporting documents, remittance references, and reconciliation evidence—this is where most finance workload sits.

6. Can You Schedule Overseas Payments To Avoid Cut-Off And Holiday Delays

Yes, operationally many teams plan around cut-offs by batching payments earlier in the day/week, and by mapping corridor holidays. The best practice is to make timing part of the payment run, not a last-minute action.