Procurement spending can seem under control during the quarter, but the full picture often only emerges at quarter-end, when costs across software, logistics, agencies, and suppliers are consolidated across multiple teams and systems.

This complexity is growing in the UAE, where authorities are mandating e‑invoicing from mid‑2026. It's a move expected to cut processing costs by up to 66 % and highlight the financial benefits of improved procurement visibility.

For finance leaders, this makes procurement opportunity analysis essential. Unfolding fragmented vendor spending, underused contracts, and pricing inefficiencies helps organisations identify hidden costs and optimise supplier arrangements.

In this blog, you’ll learn how procurement opportunity analysis works, where inefficiencies typically appear, and how finance teams can prioritise supplier improvements while managing risk effectively.

TL;DR Key Takeaways:

- Procurement inefficiencies surface through financial signals: Margin pressure, pricing gaps, and liquidity strain often reveal hidden supplier cost issues before reporting cycles do.

- Leakages are identified through structured analysis: Category-level spend, supplier exposure, contract alignment, and cost variance highlight procurement inefficiencies.

- Opportunity analysis is triggered by deviation: Finance teams act when cost behaviour diverges from margin, pricing, or working capital expectations.

- Prioritisation depends on financial impact and execution risk: Teams focus on opportunities that improve margin, cash flow, or cost stability without introducing operational disruption.

- Real-time spend visibility enables earlier intervention: Platforms like Alaan help finance teams structure supplier data and act on procurement opportunities before decisions are locked.

Why Procurement Opportunities Stay Hidden Until Quarter-End?

Procurement opportunities often go unnoticed because teams only bring supplier spend together after reporting cycles. In UAE businesses, this delay becomes even more pronounced due to cross-border procurement and VAT-linked cash flows.

Companies pay import VAT (5%) upfront and recover it later through input VAT claims, which makes liquidity planning harder when procurement costs are not visible early on.

As a result, by the time they have full visibility, supplier pricing, contract terms, and purchasing volumes are already locked in, limiting their ability to renegotiate or optimise costs.

Here's why procurement opportunities go unnoticed until quarter-end:

1. Supplier Exposure Is Underestimated During Negotiation Cycles

When teams do not consolidate supplier spend before negotiation cycles, finance underestimates actual purchasing volume.

- Teams miss volume-based pricing thresholds even when total spend is high enough

- Contracts get priced below the discount tiers that the business could have achieved

- Teams assess supplier concentration at a department level instead of across the whole business

- Negotiations rely on partial data, which weakens leverage

Decision trigger: Finance teams usually step in when margins start to shrink without any clear pricing change, or when supplier spend increases without better commercial terms.

Decision impact: The business locks supplier contracts at pricing levels that are not optimal for the entire contract cycle.

Trade-off: Flexibility for individual departments vs stronger, consolidated pricing power at the enterprise level.

2. Procurement Decisions Are Locked Before Finance Intervention

When teams have procurement visibility only during reporting cycles, finance is no longer involved in decision-making.

- Teams select suppliers without checking the impact on margins

- They commit to purchase volumes without validating cost thresholds

- They finalise pricing decisions before seeing the full cost picture

- They identify budget deviations only after execution

Decision trigger: Finance usually steps in only when a budget variance exceeds acceptable limits or when profitability declines. By then, procurement commitments are already fixed.

Decision impact: Finance can explain why costs went over budget, but it cannot prevent those overruns.

Trade-off: Faster procurement execution vs tighter cost control and margin protection.

3. Cost Timing Misalignment Distorts Margin and Liquidity Decisions

In UAE operations, procurement costs, VAT treatment, and supplier payments do not line up with revenue timing.

- Teams record supplier invoices after recognising revenue, which distorts margin signals

- Import VAT creates immediate cash outflows, while recovery depends on input VAT claims

- Payment terms vary across international suppliers, making liquidity harder to plan

- Freight and landed costs are tracked separately, which delays full cost visibility

Decision trigger: Finance teams revisit pricing or working capital when liquidity pressure rises without a matching increase in revenue, or when they cannot link margin changes to known cost drivers.

Decision impact: Teams make pricing, margin, and cash-flow decisions based on incomplete cost data.

Trade-off: Accurate margin visibility is affected by timing gaps in cost capture. Liquidity stability is impacted by delayed VAT recovery and supplier payment cycles.

4. Supplier Complexity Expands Faster Than Governance

As organisations grow across the UAE and GCC, procurement becomes more complex, but control mechanisms do not always keep up.

- Multiple vendors operate in the same category across different business units

- Teams make procurement decisions in a decentralised way, which reduces visibility into total spend

- Smaller, recurring suppliers build up outside review thresholds

- Teams delay supplier rationalisation until periodic reviews

Decision trigger: Finance steps in when supplier fragmentation leads to inconsistent pricing, rising category costs, or difficulty enforcing procurement policies across departments.

Decision impact: Cost structures develop without central oversight, which weakens pricing discipline.

Trade-off: Decentralised procurement provides flexibility but reduces control over costs and supplier optimisation.

5. Sector-Specific Procurement Pressures Change Decision Priorities

Procurement challenges manifest differently depending on the business model, which directly affects how finance teams respond.

Retail and E-commerce:

- Margins come under pressure due to landed cost gaps, discounting, and fulfilment charges

Decision: Adjust pricing or absorb higher costs to maintain volume

Logistics and Distribution:

- Costs are driven by fuel, subcontractors, and contract pricing

Decision: Renegotiate contracts or improve utilisation

Construction and Infrastructure:

- Procurement depends on project phases, subcontractor timing, and milestone billing

Decision: Reforecast project cash flows or adjust procurement schedules

SaaS and Technology:

- Vendor spend is concentrated in subscriptions and infrastructure

Decision: Control how costs scale or support growth and product expansion

Decision trigger: Finance leaders step in when unit economics move away from expected margins or when costs grow faster than revenue.

At Alaan, we bring corporate cards, invoice capture, and approval workflows into a single system, enabling finance teams to act on procurement data while decisions are still reversible.

Understanding why these opportunities are missed also helps identify where procurement leakages typically occur.

Where Do Finance Teams Typically Identify Hidden Procurement Leakages?

Procurement leakages become visible when cost behaviour diverges from expected margin, pricing, or working capital outcomes. These leakages originate from how suppliers spend, contracts, and procurement decisions are structured across the organisation.

They are typically identified only after aggregation, at which point the underlying cost decisions have already affected financial performance.

Below are some of the most common areas where finance teams identify procurement leakages.

1. Category-Level Spend Consolidation

Leakages become easier to spot when total spend within a category does not lead to better pricing outcomes:

- Total spend crosses the thresholds needed to unlock better pricing

- Vendor spread prevents teams from consolidating purchasing volume

- Cost per unit stays the same even as total spend increases

Decision trigger: Step in when category-level spend goes up, but negotiated pricing or discount tiers do not improve.

2. Supplier Concentration and Exposure Analysis

Leakages occur when supplier exposure is not reflected in the agreed commercial terms:

- Total supplier spend is split across different business units

- Pricing negotiations do not reflect the full, enterprise-level exposure

- Teams assess supplier dependence at a local level instead of across the business

Decision trigger: Step in when total supplier exposure should support renegotiation, but pricing and terms remain unchanged.

3. Contracted Cost vs Actual Spend Alignment

Leakages appear when actual procurement activity does not match agreed contract terms:

- Actual spend goes beyond, or bypasses, negotiated contract pricing

- Teams continue procuring outside the agreed supplier contracts

- Committed cost levels no longer match how the business actually operates

Decision trigger: Step in when realised procurement costs move away from contracted pricing without a clear operational reason.

4. Aggregated Recurring Spend Review

Leakages build up when small, low-value transactions add up into a meaningful cost over time:

- Individual transactions stay below approval thresholds

- Total category spend rises beyond expected levels when combined

- Cost increases only become visible after financial consolidation

Decision trigger: Step in when recurring spend increases without a matching rise in output, utilisation, or revenue contribution.

5. Pricing Variance Across Comparable Cost Structures

Leakages become clear when similar inputs are priced differently across the organisation:

- Cost differences exist across business units without changes in scope or volume

- Supplier pricing is not standardised across the business

- Similar procurement categories show inconsistent cost structures

Decision trigger: Step in when cost differences cannot be explained by operational or contractual factors.

Suggested Read: How UAE Businesses Can Reduce Procurement Costs with These 20 Strategies

Once these leakage areas are identified, finance teams can begin analysing them to identify procurement opportunities.

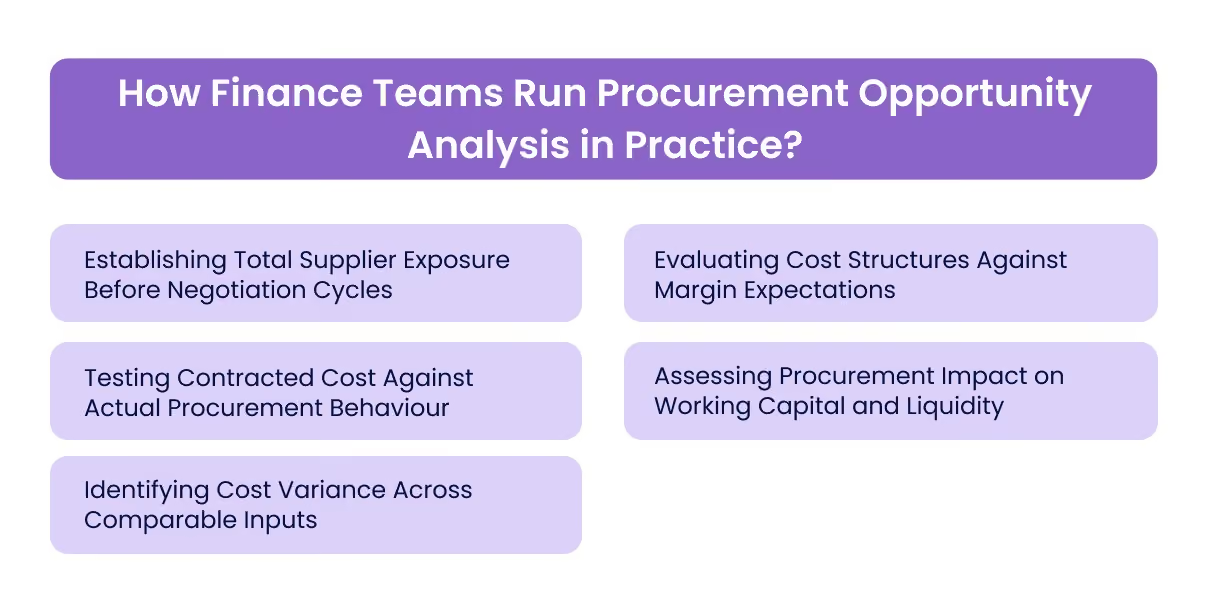

How Finance Teams Run Procurement Opportunity Analysis in Practice?

Finance teams run procurement opportunity analysis to identify where cost structures diverge from expected pricing, margin, and working capital assumptions.

The objective is not visibility alone, but to determine where procurement decisions require intervention before they affect financial outcomes.

Here's how you can put procurement opportunity analysis into practice:

1. Establishing Total Supplier Exposure Before Negotiation Cycles

The analysis starts by checking whether supplier exposure reflects the business’s actual purchasing power:

- Teams review total spend across all procurement channels before negotiation cycles begin

- They compare category-level exposure with pricing tiers and discount thresholds

- They assess supplier concentration across the entire business, not just by department

Decision trigger: Act when total supplier exposure is strong enough to support renegotiation, but current pricing does not reflect that scale.

2. Evaluating Cost Structures Against Margin Expectations

Finance teams assess whether procurement costs align with margin targets and pricing assumptions:

- They compare cost inputs with expected unit economics

- They separate procurement-driven cost increases from changes in demand or pricing

- They analyse margin pressure in relation to supplier cost behaviour

Decision trigger: Act when margins decline without any clear change in pricing strategy or revenue mix.

3. Testing Contracted Cost Against Actual Procurement Behaviour

This analysis checks whether agreed contract terms actually translate into cost efficiency:

- Teams compare real procurement activity with contracted pricing structures

- They identify deviations from agreed terms at a transaction level

- They test contract assumptions against current operating patterns

Decision trigger: Act when actual procurement costs go beyond contracted benchmarks without a clear operational reason.

4. Assessing Procurement Impact on Working Capital and Liquidity

In UAE operations, procurement analysis also focuses on cash flow timing and VAT impact:

- Teams review supplier payment cycles alongside cash flow forecasts

- They assess VAT outflows against recovery timelines

- They align procurement commitments with overall liquidity planning

Decision trigger: Act when procurement-related cash outflows start to strain liquidity without matching revenue inflows.

Also Read: A Simple Guide to Cash Flow Statement of Construction Companies

5. Identifying Cost Variance Across Comparable Inputs

Finance teams check whether cost structures stay consistent across the business:

- They compare similar inputs across business units and contracts

- They assess pricing differences based on volume, scope, and supplier terms

- They test cost inconsistencies to understand the root cause

Decision trigger: Act when cost differences exist without any operational or contractual explanation.

Procurement opportunity analysis depends on having accurate and well-structured cost data before decisions are made.

At Alaan, we make sure procurement-related spend is captured, categorised, and approved at the point of transaction. This helps finance teams move away from after-the-fact analysis and make decisions at the point where they can still influence procurement outcomes.

Once opportunities are identified, finance teams often use cost-benefit analysis to prioritise which ones to act on first.

5 Steps to Prioritise Procurement Opportunities Using Cost-Benefit Analysis

Finance teams prioritise procurement opportunities by identifying where cost interventions materially improve margin, pricing flexibility, or working capital without introducing execution risk.

The focus is on determining which actions warrant intervention based on their financial impact and timing.

Here’s how finance teams priortise procurement opportunities using cost-benefit analysis:

1. Sizing Financial Impact Against Margin Sensitivity

Teams prioritise opportunities by looking at how changes in procurement costs affect margins:

- They assess cost reductions against unit economics and margin thresholds

- They separate procurement-driven cost increases from pricing or demand changes

- They focus on areas where margins are most sensitive to cost changes

Decision trigger: Prioritise when reducing procurement costs improves margins without needing changes in pricing or demand assumptions.

2. Assessing Implementation Friction Against Financial Impact

Finance teams check whether the effort involved is worth the financial benefit:

- They assess supplier changes for execution risk

- They evaluate internal resource requirements against expected savings

- They review process changes for their operational impact

Decision trigger: Prioritise when the financial upside clearly outweighs the effort, complexity, and disruption risk.

3. Prioritising Based on Cost Concentration and Scale

Teams focus on areas where procurement spend has the biggest financial impact:

- They assess high-spend categories for pricing optimisation

- They evaluate supplier exposure for renegotiation opportunities

- They prioritise improvements where scale increases the overall impact

Decision trigger: Prioritise when concentrated spending creates enough leverage to meaningfully reduce costs.

4. Evaluating Impact on Working Capital and Liquidity

In UAE operations, teams also assess how procurement decisions affect cash flow and VAT timing:

- They review supplier payment cycles against cash flow forecasts

- They assess VAT outflows (5% under FTA) alongside recovery timelines

- They align procurement commitments with liquidity constraints

Decision trigger: Prioritise procurement changes that improve cash flow timing or reduce liquidity pressure.

5. Assessing Long-Term Cost Stability

Finance teams also look at whether procurement decisions make costs more predictable over time.

- They assess pricing structures for consistency

- They evaluate supplier relationships for long-term scalability

- They review cost volatility alongside expected savings

Decision trigger: Prioritise when procurement changes improve cost stability without increasing exposure to pricing fluctuations.

Once procurement opportunities are prioritised based on cost and impact, the next step is understanding how this analysis directly shapes better supplier decisions.

How Opportunity Analysis Improves Supplier Decisions?

Supplier decisions directly influence how procurement costs affect pricing, margins, and working capital. Opportunity analysis supports better decision-making by highlighting where supplier terms, cost structures, and performance fall short of expected financial outcomes.

In UAE operations, this becomes more complex because of cross-border supplier arrangements, VAT-linked cost timing, and decentralised procurement across business units.

Here’s how opportunity analysis improves supplier decisions:

1. Identifying When Supplier Performance No Longer Supports Cost Efficiency

Opportunity analysis helps teams spot when supplier performance no longer matches cost expectations:

- Procurement costs go up without any clear improvement in output or delivery reliability

- Supplier performance does not justify the current pricing structure

- Cost per unit moves away from expected benchmarks

Decision trigger: Step in when supplier costs increase or remain high, with no measurable improvement in performance or delivery outcomes.

2. Strengthening Supplier Negotiation Based on Verified Cost Exposure

Opportunity analysis leads to stronger negotiations by linking supplier discussions to actual spend behaviour:

- Teams assess total supplier exposure before starting negotiation cycles

- They evaluate cost concentration against pricing tiers and discount thresholds

- They connect changes in spending patterns with the right timing for negotiations

Decision trigger: Step in when supplier spend supports renegotiation, but pricing or commercial terms have not changed.

3. Aligning Supplier Selection With Financial Performance Requirements

Supplier selection improves when teams base decisions on financial outcomes instead of operational preferences:

- Teams test supplier cost structures against margin expectations

- They align procurement decisions with pricing and cost thresholds

- They choose vendors based on financial impact rather than local optimisation

Decision trigger: Step in when supplier choices lead to margin pressure or cost structures that do not match pricing assumptions.

Must Read: 10 Proven Vendor Management Strategies for UAE Companies

4. Identifying Supplier Structures That Increase Cost Variability

Opportunity analysis also highlights when supplier setups lead to cost inconsistencies:

- Pricing varies for similar inputs without any clear contractual or volume-based reason

- Supplier terms differ across business units, which affects cost predictability

- Cost volatility increases without changes in demand

Decision trigger: Step in when cost differences cannot be explained by scope, volume, or supplier terms.

While improving supplier decisions is important, finance teams must also balance potential opportunities with the risks each supplier brings.

5 Ways to Balance Procurement Opportunities with Supplier Risk

Procurement opportunities are evaluated not only on their potential to reduce costs but also on how they affect supplier reliability, cost stability, and working capital exposure. The objective is to ensure that cost improvements do not introduce structural risk into pricing, operations, or liquidity.

Below are five ways to balance procurement opportunities with supplier risk.

1. Testing Supplier Stability Against Cost Reduction Opportunities

Finance teams check whether cost savings come at the expense of supplier reliability or consistent performance:

- They assess supplier financial and operational stability against cost reduction targets

- They test whether suppliers can handle required volumes before making consolidation decisions

- They review dependency risk when the business relies on fewer suppliers

Decision trigger: Proceed only when cost reductions do not increase the risk of supplier instability or over-concentration.

2. Evaluating Supplier Dependence Within High-Impact Categories

Teams review procurement changes based on how critical a supplier is to both cost structure and operations:

- They measure supplier dependence against category-level cost impact

- They check if alternative suppliers are available at the required scale

- They assess operational reliance in terms of how flexible procurement can remain

Decision trigger: Limit consolidation or supplier changes when relying on a single vendor increases operational or cost risk.

3. Assessing Contract Structures Against Future Cost Flexibility

Teams evaluate supplier agreements to understand how they affect cost predictability and flexibility over time:

- They test contract commitments against expected changes in demand or pricing

- They assess pricing structures for long-term stability

- They review contract constraints and how they limit procurement flexibility

Decision trigger: Avoid changes when contract structures reduce the ability to adjust costs as market or operational conditions shift.

4. Evaluating Transition Risk Against Immediate Cost Savings

Teams assess supplier changes by weighing execution risk against potential savings:

- They evaluate how complex the transition will be compared to the expected cost-benefit

- They assess execution risk, especially when procurement changes affect core workflows

- They measure short-term disruption against long-term cost improvement

Decision trigger: Delay or phase changes when execution risk is higher than the immediate financial benefit.

5. Protecting Cost Stability in Operationally Critical Categories

Some procurement categories need stable cost structures because they directly affect pricing and operations:

- Teams assess cost volatility in relation to pricing consistency

- They prioritise supplier reliability where cost disruption could affect revenue delivery

- They evaluate procurement changes based on how they impact cost predictability

Decision trigger: Prioritise stability over savings when procurement changes introduce cost variability that affects pricing or margin consistency.

Effectively balancing opportunities and risks also depends on identifying the right timing for a procurement opportunity analysis.

When Should You Conduct an Opportunity Analysis?

Finance teams conduct opportunity analysis when procurement cost behaviour diverges from expected margin, pricing, or working capital assumptions.

This is done to identify and intervene before these deviations become embedded in financial performance.

Below are the key moments that trigger procurement opportunity analysis.

Understanding when to conduct the analysis becomes even more valuable when supported by platforms that help teams act on opportunities efficiently.

How Alaan Helps Finance Teams Identify and Act on Procurement Opportunities?

Procurement opportunity analysis depends on having structured, reliable visibility into supplier spend before decisions are finalised. When spend data is fragmented across systems, supplier exposure and pricing inefficiencies are typically identified only during reporting cycles.

At Alaan, we capture and organise procurement-related spend at the point of transaction, enabling finance teams to identify cost inefficiencies earlier and intervene before they affect margin, pricing, or working capital.

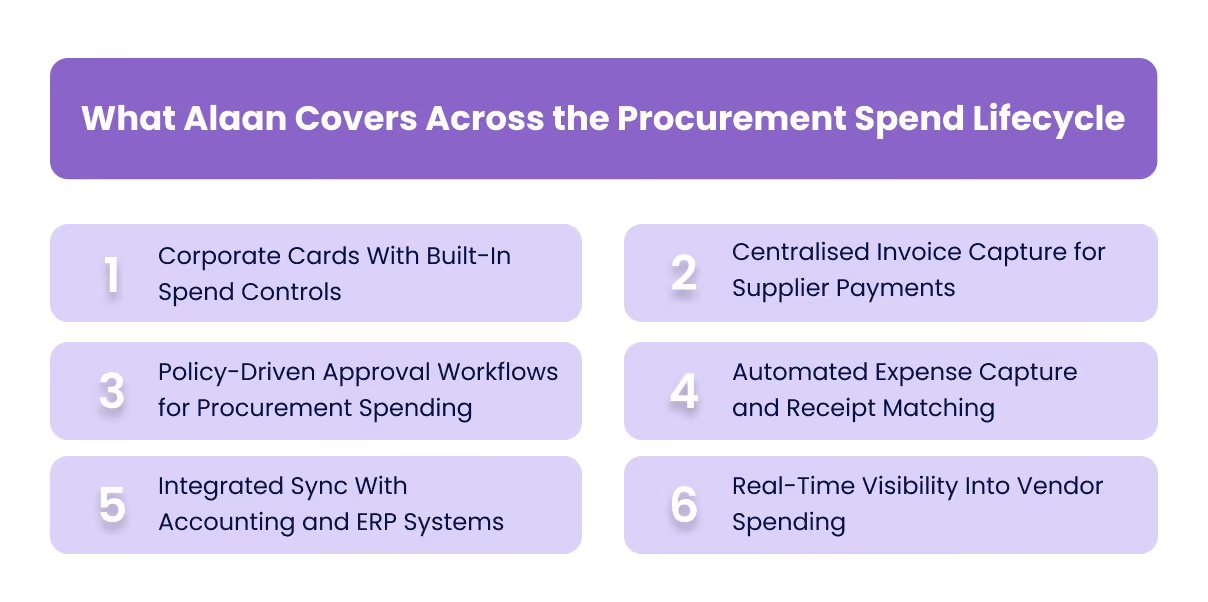

What Alaan Enables Across Procurement Opportunity Analysis

Procurement opportunity analysis depends on accurate supplier data and consistent oversight of operational spending. At Alaan, we strengthen each stage of the procurement spend lifecycle so finance teams can analyse vendor payments, identify inefficiencies, and make informed supplier decisions.

1. Corporate Cards With Built-In Spend Controls

We provide corporate cards with configurable limits and policy controls, allowing finance teams to manage procurement spending before purchases occur.

Admins can:

- Set spending limits by employee, team, or department

- Restrict purchases to approved vendor categories

- Issue virtual or physical cards instantly for operational purchases

- Freeze or block cards in real time if policies are violated.

These controls help organisations prevent unapproved supplier purchases and maintain tighter oversight of operational spending.

2. Centralised Invoice Capture for Supplier Payments

We centralise supplier invoice collection through uploads, email forwarding, and integrated workflows. Vendor invoices are captured and recorded as soon as they enter the system.

This helps finance teams:

- Maintain a single record of supplier payments

- Track vendor spending across departments

- Reduce duplicate or missed invoices.

With supplier invoices recorded in one place, finance teams gain a clearer view of procurement spending patterns.

3. Policy-Driven Approval Workflows for Procurement Spending

Supplier payments flow through structured approval workflows in line with company policies.

These workflows ensure that:

- Procurement purchases align with approved budgets

- Department heads review vendor expenses before payment

- Exceptions or unusual purchases are flagged early.

By strengthening approvals before payments occur, finance teams gain greater control over procurement commitments.

4. Automated Expense Capture and Receipt Matching

Procurement spending often includes smaller operational purchases made through corporate cards. Capturing these transactions accurately is essential for analysing vendor spending.

We automate receipt collection and match it with transaction data to ensure supplier expenses are recorded correctly. This helps finance teams maintain accurate procurement records without relying on manual reconciliation.

5. Integrated Sync With Accounting and ERP Systems

We integrate with accounting systems such as:

- NetSuite

- QuickBooks

- Xero

- Microsoft Dynamics

- Zoho Books

- Odoo

Approved procurement transactions sync automatically with accounting records, ensuring vendor spending is accurately reflected in financial reports. This integration helps finance teams analyse procurement costs using reliable financial data.

6. Real-Time Visibility Into Vendor Spending

We provide dashboards that show procurement spending across the organisation, including:

- Supplier payments by category

- Department-level procurement spending

- Recurring vendor charges

- Outstanding invoices and commitments.

This visibility allows finance leaders to identify procurement inefficiencies earlier rather than waiting for financial reviews.

What Alaan Is (And Is Not)

Alaan is a spend management platform designed to strengthen operational financial control and accuracy in procurement-related spending.

We help finance teams:

- Identify supplier concentration and cost patterns

- Maintain structured, reliable procurement data

- Apply controls before procurement costs are committed

We do not replace your accounting system. We integrate with existing financial tools, enabling procurement decisions to be supported by complete and up-to-date financial data.

Final Thoughts

Procurement opportunity analysis allows finance teams to move from identifying cost issues after reporting cycles to acting on them while decisions are still reversible. By linking supplier spend, contract structures, and cost behaviour to financial outcomes, teams can improve margin control, strengthen pricing discipline, and manage working capital more effectively.

At Alaan, we bring corporate card transactions, invoices, approvals, and accounting data into a single, structured system. This helps finance teams maintain real-time visibility into procurement spend, enforce controls before costs are committed, and make more informed supplier decisions.

Schedule a free demo to see how Alaan helps UAE businesses identify procurement inefficiencies earlier and improve cost control.

FAQs

1. What are the key components of a procurement strategy?

A strong procurement strategy usually includes clear supplier selection criteria, well-defined procurement categories, pricing and contract management, and structured approval workflows. Finance leaders also make sure the strategy aligns supplier spending with budgets, risk policies, and long-term operational goals.

2. What do finance leaders gain from procurement opportunity analysis?

Procurement opportunity analysis helps finance leaders uncover hidden cost inefficiencies, spot vendor consolidation opportunities, and identify areas for pricing optimisation. It also gives better visibility into suppliers across departments, allowing teams to control spending and make smarter procurement decisions.

3. How does market research influence procurement strategy?

Market research helps finance and procurement teams understand supplier pricing trends, explore alternative vendors, and benchmark against industry standards. This insight enables organisations to negotiate better contracts, assess supplier competitiveness, and make procurement decisions based on current market conditions.

4. What are the best practices for managing supplier risk in procurement?

Finance teams manage supplier risk by checking vendor stability, reviewing contract flexibility, and keeping multiple supplier options for critical categories. Regular supplier performance reviews and clear procurement oversight also help reduce operational disruptions and maintain reliable vendor relationships.

5. How does procurement opportunity analysis affect budgeting accuracy?

Procurement opportunity analysis gives finance leaders a clear view of supplier spending across all departments. This helps improve budget forecasts by highlighting recurring vendor costs, contract commitments, and areas where procurement spending might rise.