A Dubai retailer posts their best Ramadan yet: AED 1.2 million in sales, a packed store, and a stockroom emptied by week three. Six weeks later, they can't pay their supplier.

The numbers looked right, but the balance sheet told a different story. That gap between doing well and being financially healthy is exactly what a simple retail balance sheet is built to catch, and why understanding one is no longer just the accountant's problem.

In a market where wholesale and retail trade contribute over 16% of the UAE’s non-oil GDP, retail decisions are becoming more financial than instinctive. That is why understanding a simple retail balance sheet is no longer just an accountant’s job.

Whether you run a supermarket, fashion store, electronics shop, or ecommerce business, this guide will help you understand inventory, liabilities, cash flow, and retail financial health in a way that actually makes operational sense.

Key Takeaways:

- UAE Retail Growth: Wholesale and retail trade contributes over 16% of the UAE’s non-oil GDP, making stronger financial visibility and operational control increasingly important for modern retailers.

- Inventory Pressure: In retail businesses, inventory is often the largest current asset, meaning excess stock, slow-moving SKUs, or poor inventory planning can quietly block working capital and weaken liquidity.

- Financial Visibility: A simple retail balance sheet helps businesses track supplier dues, VAT obligations, POS settlements, and operational spending beyond just sales performance or profitability figures.

- Retail Warning Signs: Metrics like inventory turnover, DIO, and supplier dependency help retailers identify pressure building before it affects cash flow.

- Automation & Reporting: UAE retailers increasingly rely on connected finance systems like Alaan to automate reconciliation, improve VAT-ready reporting, centralise branch-level spending, and reduce manual accounting workflows.

What Is a Retail Balance Sheet?

A retail balance sheet is a financial statement that shows what a retail business owns, what it owes, and what remains with the owner at a specific point in time. Think of it as the financial reality of your store written on paper. It helps retailers understand whether the business is financially stable, overstocked, running on debt, or generating healthy working capital.

Unlike service businesses, retail businesses operate around inventory movement. Every unsold product sitting on a shelf, every supplier payment pending, and every dirham collected through POS systems eventually appears on the balance sheet.

That is why retailers rely heavily on this statement to track stock value, cash flow pressure, vendor obligations, and operational health.

A retail balance sheet is built on a simple accounting equation:

In simple terms:

- Assets are everything the retail business owns, such as cash, inventory, store equipment, and receivables.

- Liabilities are obligations the business needs to pay, including supplier dues, rent, taxes, or loans.

- Owner’s Equity is the remaining value left after liabilities are deducted from assets.

For retail businesses, this document is more than an accounting requirement. It becomes a decision-making tool.

A supermarket preparing for festive demand, a fashion store managing seasonal inventory, or an ecommerce brand handling supplier credit all depend on balance sheet visibility to avoid cash flow stress and make smarter purchasing decisions.

Also Read: What is Inventory Accounting? Types, Valuation And Journal Entries

To understand what your retail business is really telling you financially, you first need to break down the core components behind the balance sheet.

Main Components of a Simple Retail Balance Sheet

For UAE retailers, these three components are never static. Inventory shifts daily, supplier dues reset monthly, and equity either grows or quietly erodes depending on how well the first two are managed.

Here's what that actually looks like on paper.

1. Inventory-Driven Assets

For most retail businesses, assets are not just numbers sitting inside accounting software. They represent products already purchased, stocked, displayed, or awaiting shipment to warehouses for upcoming demand cycles.

Retail assets commonly include:

- Inventory across stores and warehouses

- Cash and bank balances

- POS and card settlements

- Advance supplier payments

- Delivery vehicles and store equipment

- Ecommerce fulfilment stock

What makes retail different is the weight inventory carries financially. In many UAE retail businesses, inventory becomes the largest current asset because they purchase stock in advance to meet seasonal demand, promotions, Ramadan sales, or shopping festivals.

This also creates operational risk. Overstocking, slow-moving SKUs, or inaccurate inventory tracking can block liquidity even during strong sales periods.

2. Operational Liabilities

Retail liabilities are usually tied directly to daily business activity rather than long-term corporate financing structures.

These liabilities commonly include:

- Supplier payables

- VAT obligations

- Warehouse and store lease payments

- Employee salaries

- Logistics and delivery costs

- Short-term inventory financing

For UAE retailers, supplier credit cycles play a major role in cash flow planning. Businesses often purchase inventory months before demand peaks, especially during Ramadan, year-end sales, or tourism-heavy periods. This means liabilities can rise quickly even before revenue catches up.

VAT also becomes a much more active component in retail balance sheets because retailers handle large transaction volumes across both physical and ecommerce channels.

3. Owner’s Equity

In retail, equity is not passive; it is the financial buffer between a bad season and a business crisis. A store with strong equity can absorb a slow February after a record December, hold excess stock without panicking, or wait out a supplier dispute without caving on credit terms.

A store running on thin equity has no such room; every demand spike, every delayed payment, every unsold SKU hits harder and faster. That difference rarely shows up in sales reports. It shows up here.

Also Read: Chart of Accounts: A Practical Guide for UAE Businesses

Once these components start working together inside an actual retail business, the balance sheet becomes far easier to read operationally rather than just financially.

Simple Retail Balance Sheet Example

Imagine a Dubai-based electronics retailer preparing for the Dubai Shopping Festival. The business has already stocked additional gaming consoles, mobile accessories, and smart devices ahead of the seasonal sales rush.

Sales are strong, but a large amount of money is still tied up in warehouse inventory and supplier payments that will become due over the next few weeks.

This is how the retailer’s balance sheet may look at the end of the quarter:

For a finance manager, this table immediately signals one concern: AED 780,000 locked in inventory against AED 622,000 in liabilities means a slow post-Festival month could create a cash squeeze before the next procurement cycle even begins.

That's not a sales problem; it's a timing problem. A balance sheet exposes it early.

Even a well-structured retail balance sheet can become misleading when everyday operational mistakes start affecting how inventory, liabilities, and cash flow are recorded.

Also Read: Understanding Prepaid Expenses on a Balance Sheet: Definition, Journal Entries, and Examples

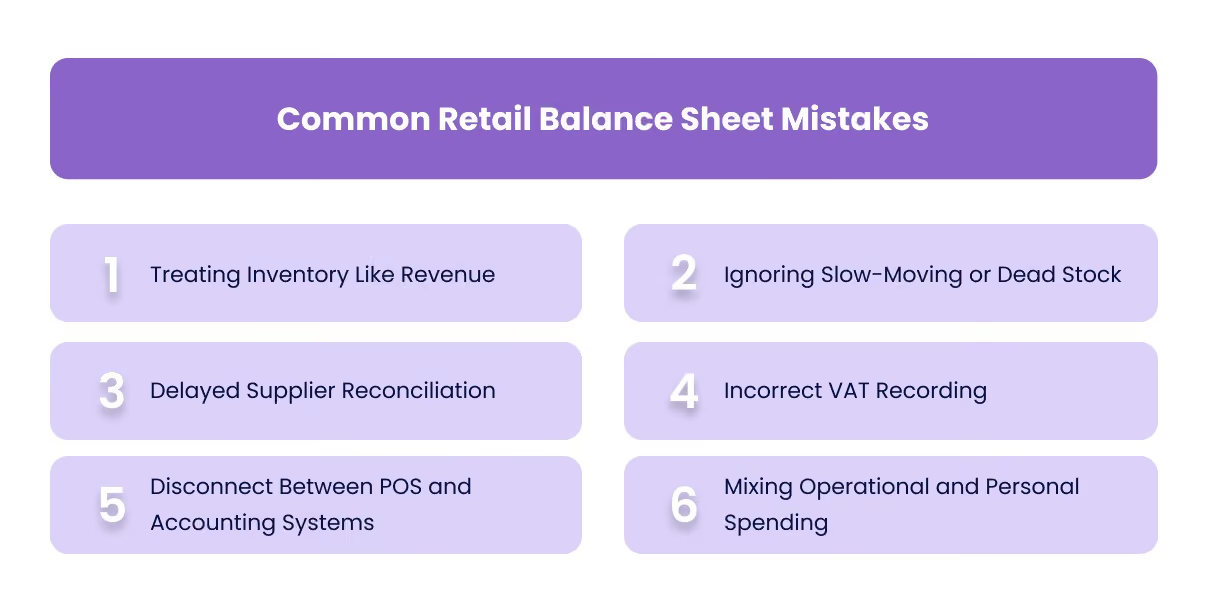

Common Retail Balance Sheet Mistakes

Retail balance sheets often become inaccurate slowly, not suddenly. A few inventory mismatches, delayed reconciliations, or incorrectly recorded supplier payments can quietly distort the financial position of the business over time.

In UAE retail businesses where transaction volumes are high and inventory moves quickly, these mistakes can directly affect cash flow visibility, VAT compliance, and operational planning.

Here are some of the most common mistakes retail businesses make:

1. Treating Inventory Like Revenue

One of the biggest retail mistakes is assuming purchased inventory automatically represents profit. Stock sitting inside warehouses or shelves is still blocked working capital until it is sold.

Excess inventory can make the balance sheet appear stronger while quietly reducing liquidity and increasing storage costs.

2. Ignoring Slow-Moving or Dead Stock

Many retailers continue recording old or unsold inventory at full value even when products are no longer moving realistically.

This creates:

- inflated asset values,

- inaccurate working capital visibility,

- misleading profitability assumptions.

This becomes especially common after seasonal campaigns or trend-driven sales periods.

3. Delayed Supplier Reconciliation

Retail businesses in the UAE often work on rolling supplier credit cycles. When supplier invoices, advance payments, or credit notes are not reconciled properly, liabilities can become understated or duplicated.

This usually creates confusion around:

- actual payable obligations,

- available cash reserves,

- and future purchasing capacity.

4. Incorrect VAT Recording

Retailers process large transaction volumes daily, making VAT tracking more operationally sensitive than in many corporate businesses.

Common mistakes include:

- recording VAT in the wrong reporting period,

- missing compliant invoices,

- incorrect VAT categorisation,

- poor documentation for input tax recovery.

Under UAE regulations, these errors can lead to penalties, reconciliation issues, and audit complications.

5. Disconnect Between POS and Accounting Systems

Many retailers still operate with disconnected POS, inventory, and accounting systems. This creates delays in financial visibility and increases manual entry errors.

As a result:

- sales may not reconcile correctly,

- settlements remain unmatched,

- inventory records become inconsistent,

- And the month-end closing takes significantly longer.

6. Mixing Operational and Personal Spending

This remains one of the most common SME accounting mistakes in the UAE.

When owners use personal cards or accounts for business purchases without proper recording:

- liabilities become unclear,

- expense tracking weakens,

- and financial reporting loses accuracy.

For retailers managing multiple suppliers, stores, or procurement teams, this quickly creates reconciliation blind spots.

Many retail businesses also confuse balance sheets with income statements, even though both reveal very different sides of financial performance.

Retail Balance Sheet vs Income Statement

A retail balance sheet shows the financial position of the business at a specific point in time. An income statement shows how the business performed over a period of time.

For UAE retailers, this difference matters because strong sales do not always mean healthy cash flow. A retailer may report high profits on an income statement while still struggling operationally due to excess inventory, supplier liabilities, or blocked working capital.

Here is how both statements differ in a retail business context:

Once retailers understand how to read a balance sheet properly, it becomes much easier to spot the operational metrics quietly shaping profitability and cash flow behind the scenes.

Key Retail Metrics You Can Understand from a Balance Sheet

Beyond the basic figures, the balance sheet provides a window into the operational efficiency of a retail business. In the UAE’s 2026 economy, where real GDP is projected to grow by 5.3%, monitoring these specific ratios helps retailers navigate rising competition and evolving consumer habits.

1. The Quick Ratio

While the current ratio includes inventory, the Quick Ratio excludes it to measure a retailer’s immediate liquidity. This is vital in the UAE, where luxury and electronics stock can be high-value but slow to move.

A ratio below 1.0 suggests that if sales were to stall tomorrow, the business might struggle to clear its immediate debts without liquidating stock at a discount.

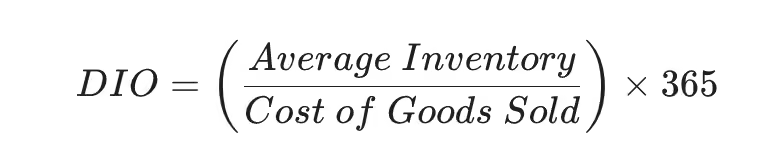

2. Days Inventory Outstanding (DIO)

This metric reveals the average number of days your stock sits in the warehouse or on the shelf before being sold. For UAE retailers managing seasonal fluctuations like Ramadan or the Dubai Shopping Festival, a rising DIO is a red flag for dead stock.

In 2026, efficient retailers are aiming for lower DIOs by leveraging AI-driven demand forecasting to ensure capital isn't trapped in underperforming SKUs.

3. Debt-to-Equity (D/E) Ratio

The D/E Ratio measures how much of your retail expansion is funded by debt versus your own capital. With the UAE’s debt capital market projected to exceed $350 billion in 2026, maintaining a balanced ratio is critical for creditworthiness.

- Retail Benchmark: Most healthy UAE retail businesses operate within a 0.7 to 2.0 range.

- Insight: A ratio significantly higher than 2.0 indicates a heavy reliance on loans, which can be risky if consumer spending dips or interest rates fluctuate.

4. The Working Capital Cycle (Cash Conversion Cycle)

This measures the time (in days) it takes to convert your investment in inventory back into cash. It combines three metrics: DIO (Inventory), DSO (Receivables), and DPO (Payables).

In a market like Dubai, where many retailers benefit from favourable supplier credit terms (high DPO), a negative working capital cycle is the gold standard. It means you sell your goods and collect cash from customers before you even have to pay your suppliers.

5. Inventory-to-Sales Ratio

This ratio helps you determine if you are over-investing in stock relative to your actual sales performance.

If this ratio is climbing while sales are flat, your balance sheet is becoming top-heavy, indicating that your purchasing strategy is out of sync with 2026 market demand.

But tracking these retail metrics accurately becomes difficult when expenses, supplier payments, and operational spending are still managed across disconnected systems or manual workflows.

How Alaan's Expense Management Improves Retail Financial Reporting

Retail finance teams in the UAE handle far more than expense tracking. They manage supplier purchases, store-level spending, VAT documentation, employee cards, reimbursements, inventory-linked payments, and multi-location approvals; often all at the same time.

When these workflows are spread across spreadsheets, WhatsApp approvals, physical receipts, and disconnected systems, financial reporting becomes slower, harder to reconcile, and difficult to scale accurately.

Alaan was built to solve this operational gap for modern UAE businesses. Its platform combines corporate cards, spend management, AI-powered automation, accounting integrations, and real-time financial visibility into one connected system designed for finance and operations teams across the GCC.

For retail businesses, this improves financial reporting in several practical ways:

- Smart corporate cards with spend controls help retailers issue physical or virtual cards for store managers, procurement teams, and operations staff while setting merchant restrictions, spending limits, and approval workflows centrally.

- Supplier payments and overseas inventory transfers become easier to manage with SuperPay™, which combines invoice approvals, cross-border transfers, preferential FX rates, and zero transfer fees into one workflow for UAE finance teams handling international vendors and procurement.

- AI-powered receipt scanning automatically captures vendor details, VAT amounts, TRN information, and matches receipts to transactions in real time, reducing manual reconciliation work for finance teams.

- Real-time spend visibility gives finance managers a live view of operational spending across branches, warehouses, logistics, and supplier payments instead of waiting for month-end reporting.

- Accounting automation integrations sync expense data directly with systems like Xero, NetSuite, QuickBooks, SAP, Dynamics 365, Odoo, and Zoho Books to reduce manual bookkeeping and improve reporting accuracy.

- Custom approval workflows allow retail businesses to create department-level or branch-level approval structures for purchases, reimbursements, and operational expenses.

- VAT-ready expense management helps UAE retailers maintain compliant records by validating invoices, VAT amounts, and transaction details before they enter accounting systems.

- AI-driven spend insights and analytics help finance teams identify unusual spending patterns, duplicate invoices, category mismatches, and operational inefficiencies faster.

- Multi-store financial oversight centralises spending visibility across branches and teams, making it easier for growing retailers to manage operational costs without losing financial control.

Conclusion

Here's the uncomfortable truth: most UAE retailers only look at their balance sheet when something has already gone wrong. By then, the supplier is waiting, the cash is short, and the next purchasing cycle is at risk.

The retailers who stay ahead of that curve aren't necessarily bigger or better-funded; they just see the pressure earlier. That starts with understanding what the balance sheet is actually telling you, and making sure the systems feeding it are accurate.

If your current setup relies on month-end reconciliation, disconnected POS exports, or spreadsheet-based expense tracking, you're always operating one step behind. That's the gap Alaan was built to close.

Book a personalised demo to see how UAE retail teams are using Alaan to get ahead of cash flow problems, before they appear on a bank statement.

FAQs

1. What is included in a retail balance sheet?

A retail balance sheet typically includes inventory, cash and bank balances, POS settlements, supplier payables, VAT liabilities, store equipment, loans, and owner’s equity.

2. Why is inventory the most important part of a retail balance sheet?

Inventory often becomes the largest current asset for retailers because a significant portion of working capital is tied up in stock. Slow-moving inventory can reduce liquidity and increase operational pressure.

3. What is the difference between a retail balance sheet and an income statement?

A retail balance sheet shows what the business owns and owes at a specific point in time, while an income statement shows revenue, expenses, and profitability over a period.

4. How do retailers use balance sheets to manage cash flow?

Retailers use balance sheets to monitor inventory levels, supplier liabilities, liquidity, and working capital so they can plan purchasing cycles, seasonal stocking, and operational spending more effectively.

5. How often should a retail business prepare a balance sheet?

Most retail businesses prepare balance sheets monthly, quarterly, or annually to track financial health, manage liabilities, and monitor inventory performance more accurately.